May 20, 2026

International Graphite Ltd's global processing strategy represents a transformative approach to critical mineral value chain development that addresses fundamental market vulnerabilities while creating competitive advantages across multiple jurisdictions. This distributed processing model demonstrates how strategic positioning can capture enhanced margins through value-added manufacturing rather than traditional concentrate sales.

The graphite sector has witnessed significant transformation as industry evolution trends reshape traditional business models. Furthermore, the strategic importance of graphite in the global energy transition insights has created unprecedented opportunities for vertically integrated processing operations.

Strategic Architecture of Multi-Regional Processing Networks

International Graphite Ltd's global processing strategy demonstrates a sophisticated approach to value chain integration that extends far beyond conventional mining operations. The company's framework encompasses three distinct processing hubs across Australia, Europe, and planned North American facilities, each targeting specific market segments with tailored product specifications.

This distributed processing model addresses several critical industry challenges simultaneously. Geographic diversification reduces single-point-of-failure risks inherent in concentrated production systems, while regional proximity to end customers minimises transportation costs and delivery timelines. Additionally, the staged development approach allows for capital deployment optimisation and market-responsive scaling.

The strategic positioning becomes particularly relevant when considering graphite market dynamics. With China controlling approximately 70% of global graphite processing capacity as of 2024, Western industrial and automotive customers increasingly prioritise supply chain diversification. The global graphite market, valued at approximately USD 15-16 billion in 2023, projects compound annual growth rates of 8-12% through 2030, driven primarily by battery material demand expansion.

Australian Operations: Industrial Manufacturing Foundation

The Collie hub in Western Australia serves as the cornerstone of International Graphite Ltd's global processing strategy. Located within the Collie Light Industrial Area, the facility occupies 6,000 square metres of secured land, positioned strategically opposite the company's existing qualification facility that has been operational since 2023.

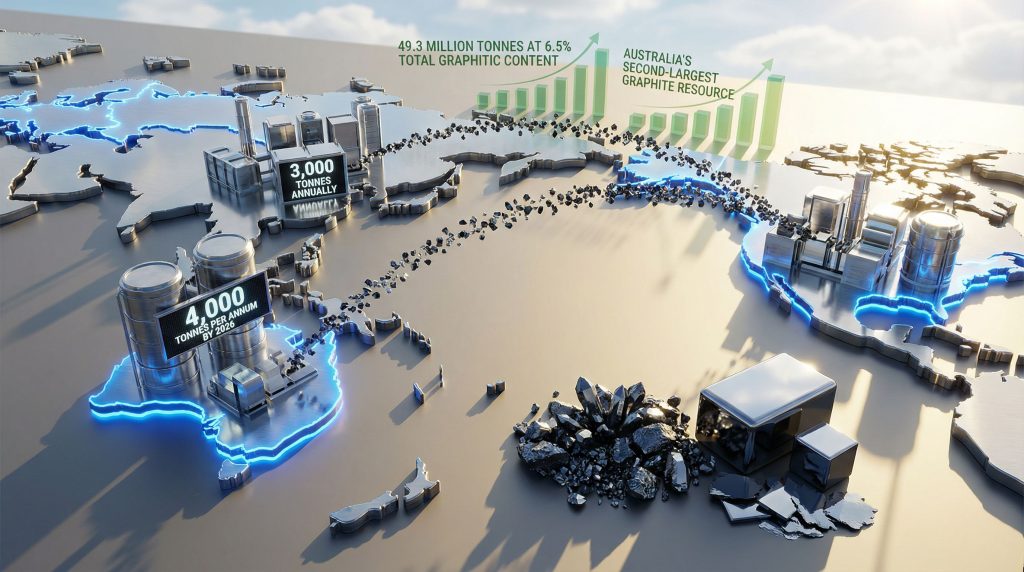

This Australian processing centre targets industrial applications including defence, advanced manufacturing, and specialised industrial uses. The facility's commercial production target of 4,000 tonnes per annum by 2026, with planned expansion to 7,500 tonnes annually, positions it to capture significant market share in premium industrial graphite segments.

Key operational advantages include:

• Direct access to the Springdale resource base, minimising concentrate transportation costs

• Established infrastructure connections including confirmed Western Power supply allocation

• Access to Western Australian government transition funding through the Collie Industrial Transition Fund

• Proximity to defence and aerospace customers requiring stringent quality certifications

The micronising process employed at Collie reduces graphite particle size to 1-10 micrometers, suitable for lubricant applications, thermal management systems, refractory applications, and advanced composites manufacturing. Jet milling technology enables particle size reduction without contamination, while classification equipment separates materials into precise size distributions meeting customer specifications.

Industrial graphite markets offer several strategic advantages over battery supply chains. Qualification cycles typically range from 12-24 months, significantly shorter than the 36+ month timelines common in battery manufacturing. Defence sector applications, requiring ISO 9001 and AS9100 aerospace quality certifications, command premium pricing while maintaining established procurement processes.

European Hub: Expandable Graphite Specialisation

The European facility, structured as a 50:50 joint venture with Arctic Graphite AS, focuses specifically on expandable graphite production for fire retardant and thermal insulation markets. Located in Bitterfeld's established chemical park, this operation leverages existing industrial infrastructure while serving the compliance-driven European market.

Expandable graphite production involves acid intercalation of graphite flakes using sulfuric or nitric acid, followed by chemical oxidation and thermal exfoliation. The resulting material expands 200-400 times its original volume when heated, creating essential properties for fire-resistant coatings, thermal insulation boards, and intumescent sealants.

Financial projections for the European facility demonstrate strong economics:

| Metric | 100% Basis | IG6's 50% Share |

|---|---|---|

| Annual Production | 4,200 tonnes | 2,100 tonnes |

| Capital Cost | A$11.2 million | A$5.6 million |

| Annual Operating Cashflow | A$7.6 million | A$3.8 million |

| Pre-tax NPV (25 years) | A$57.9 million | A$29 million |

| Pre-tax IRR | 66% | 66% |

The Bitterfeld location provides critical infrastructure advantages including existing chemical waste treatment systems, established logistics networks, and technical workforce availability. European fire safety regulations, particularly EN standards and EU Construction Products Regulation (CPR 305/2011), create regulatory compliance drivers supporting consistent demand for high-quality expandable graphite materials.

Production startup targeting H2 2027 aligns with the Collie timeline, enabling coordinated market entry across both regions. The joint venture structure with Arctic Graphite AS provides access to proven intellectual property and processing technology, reducing technical execution risks compared to proprietary process development.

Notably, these strategic partnerships reflect broader joint venture strategies becoming increasingly prevalent across the mining sector. Such collaborative approaches enable resource sharing while reducing individual company risk exposure.

North American Market Penetration Strategy

While still in planning phases, the proposed US facility represents the completion of International Graphite Ltd's tri-continental strategy. North America represents approximately 20-25% of global graphite demand, with the largest market segment being battery materials accounting for over 70% of consumption growth.

The North American regulatory environment offers significant advantages through the Inflation Reduction Act (2022), which provides tax credits for battery manufacturing using US-sourced critical materials. Department of Energy Critical Materials Institute support for domestic graphite processing development, combined with potential tariff advantages for US-processed versus imported materials, creates a favourable investment climate.

Strategic positioning elements for North American operations include:

• Access to the world's largest graphite consumption market

• Proximity to emerging battery manufacturing clusters

• Regulatory support through IRA tax credit structures

• Established defence and aerospace customer base requiring domestic supply chains

When big ASX news breaks, our subscribers know first

Economic Advantages of Distributed Processing Architecture

Capital Efficiency Through Staged Development

International Graphite Ltd's multi-hub strategy creates substantial capital efficiency advantages compared to traditional mega-project development approaches. Individual facilities achieving positive cash flow support debt repayment and reinvestment, while lower capital requirements enable funding through diverse sources including debt, grants, and equity.

Current funding structure demonstrates this approach effectively. The company's ASX capital raising activities have been structured to support this phased development approach.

Funding Position (December 31, 2025):

• Cash on hand: A$1.4 million

• Unused financing facilities: A$3.85 million

• Estimated runway: 14.9 quarters at current burn rate

• Key funding sources: Secured R&D loan facility (16% interest), Pioneer Resource Partners agreement (up to $3 million), Western Australian government grants

The staged approach contrasts favourably with traditional mining mega-projects requiring $500+ million upfront capital, which concentrate execution risk and funding requirements. Multi-facility development enables project delays at one location without impacting others, while providing funding flexibility and market responsiveness capabilities.

Market Access Optimisation

Regional processing facilities eliminate long-distance transportation costs for finished products while reducing tariff exposure and logistics timelines. Transportation costs for raw graphite concentrate from Australia to Europe range from $150-300 per tonne, representing significant savings when processing occurs closer to end customers.

Each regional facility develops distinct customer relationships, technical support capabilities, and product specifications tailored to local market preferences. This approach enables:

Market Segmentation Benefits:

• Australia hub: Defence, aerospace, advanced manufacturing (premium pricing, 12-24 month qualification)

• Europe hub: Fire safety, thermal insulation (regulatory-driven demand, moderate pricing)

• North America hub: Battery anode, industrial applications (high volume, competitive pricing)

Resource Foundation and Supply Chain Integration

Springdale Resource Base Characteristics

The Springdale Graphite Project in Western Australia provides foundational resource support for all downstream operations. With 49.3 million tonnes at 6.5% total graphitic content, this deposit ranks as Australia's second-largest graphite resource and among the top 15 globally.

Resource specifications include:

• Global ranking: Top 15 worldwide by size

• Mine construction timeline: Expected 2028

• Supply duration: Multi-decade resource life supporting long-term operations

• Quality profile: Suitable for multiple end-use applications across industrial and battery markets

The proximity of Springdale to the Collie processing facility creates vertical integration opportunities, reducing concentrate transportation costs while ensuring feedstock quality control. Resource scale supports both domestic processing and concentrate exports to European and future North American operations.

Advanced Processing Capabilities Development

International Graphite Ltd's processing strategy encompasses three distinct technological tiers, each targeting different customer segments with varying margin profiles and qualification timelines:

Processing Technology Hierarchy:

-

Primary processing: Micronising and expandable graphite production for industrial applications

-

Secondary processing: Purification to >99% purity levels for specialised applications

-

Advanced materials: Spheroidisation and carbon coating for battery anode materials

The company's non-binding Letter of Intent with Italian chemical specialist ALKEEMIA SpA demonstrates strategic third-party capacity utilisation. Rather than immediately constructing proprietary purification infrastructure, International Graphite has secured access to 200 tonnes-per-year initial capacity, with up to 50% of start-up capacity allocated to IG6.

ALKEEMIA's planned expansion to 20,000 tonnes per year by 2030 offers substantial long-term capacity without requiring IG6 to fund infrastructure development independently. This approach reduces capital intensity while maintaining scalability as demand grows.

Consequently, the focus on sustainable mining transformation principles influences processing facility design and operational protocols across all hubs.

Battery Market Development Strategy

Anode Material Development Pathway

International Graphite's processing capabilities position the company for participation in rapidly growing battery materials markets through spheroidising and purification technologies under development at Collie. The company's pilot program with CarboPhite Pty Ltd tests carbon coating technology for lithium-ion battery anode materials.

Graphite samples have been supplied for half-coin-cell and full-coin-cell evaluation, with electrochemical testing conducted at the University of Melbourne. This development approach enables battery market qualification while prioritising near-term industrial cash flows.

Battery Market Positioning Elements:

• Spheroidising capability development for optimal battery performance

• Advanced purification research targeting >99.95% purity requirements

• Anode material qualification processes with potential customers

• Electric vehicle supply chain participation opportunities

The staged approach allows International Graphite to establish industrial market revenue streams while developing battery market capabilities, reducing dependence on single market segments during qualification periods.

Competitive Positioning and Market Dynamics

Supply Chain Diversification Imperatives

With graphite markets historically dominated by Chinese production, International Graphite's Western-focused processing network addresses growing demand for supply chain diversification among industrial and battery manufacturers. Recent disruptions due to Chinese export restrictions and production capacity constraints have prompted industrial and automotive companies to actively pursue alternative supply sources.

The value-added processing focus enables International Graphite to command higher margins compared to raw concentrate sales. Raw concentrate typically sells for $500-800 per tonne, while processed products command $2,000-5,000 per tonne depending on specifications and applications.

Operational Synergies Across Hub Network

The global processing network creates multiple operational advantages:

Technology Transfer Opportunities:

• Technological developments implemented across facilities compound efficiency gains

• Operational improvements at one hub benefit entire network

• Best practices sharing reduces learning curve timelines

Market Intelligence Advantages:

• Operating across multiple regions provides comprehensive market insight

• Responsive strategy adjustments based on regional demand patterns

• Early identification of market trends and customer requirements

Risk Distribution Benefits:

• Geographic diversification reduces exposure to regional economic fluctuations

• Regulatory change impacts minimised through jurisdiction spreading

• Supply chain disruption risks reduced through multiple operational locations

Strategic Challenges and Execution Requirements

Multi-Jurisdictional Complexity Management

Managing simultaneous development across multiple continents requires sophisticated project management capabilities and regulatory expertise across different legal frameworks. Each jurisdiction presents distinct permitting requirements, environmental standards, and operational protocols.

Execution complexity factors include:

• Regulatory compliance across Australian, European, and North American jurisdictions

• Currency exposure management across multiple operational currencies

• Workforce development and technical expertise across regions

• Quality control standardisation across facilities

Capital Allocation Optimisation

Balancing investment across three continents while maintaining operational excellence at each location presents ongoing strategic challenges. Priority sequencing for capital deployment must consider market development timelines, regulatory approval processes, and customer qualification requirements.

The company's current funding runway of 14.9 quarters provides adequate time for staged development, though additional funding will be required as facilities progress toward commercial production. Strategic funding sources including government grants, debt facilities, and potential equity raises must be coordinated with development timelines.

Market Development Requirements

Each regional market requires distinct customer development approaches, technical specifications, and competitive positioning strategies. Industrial customers in defence and aerospace sectors have different qualification requirements compared to fire safety and battery anode customers.

Market-specific development needs:

• Technical certification processes varying by application and region

• Customer relationship building requiring local presence and expertise

• Product specification optimisation for regional preferences

• Competitive pricing strategies aligned with local market conditions

The next major ASX story will hit our subscribers first

Future Growth Scalability and Market Leadership

Expansion Framework Development

The modular approach to facility development creates a replicable framework for expansion into additional markets or processing capabilities as demand grows. Each successful hub provides operational template and best practices for future development.

Scalability advantages include:

• Proven development processes applicable to new locations

• Established supplier and contractor relationships

• Technology platforms scalable across facilities

• Customer base expansion through geographic proximity

Market Leadership Positioning

By establishing processing capabilities in key consumption regions, International Graphite positions itself as a potential market leader in non-Chinese graphite supply chains. First-mover advantages in Western processing networks, combined with established customer relationships across regions, create defensive competitive positions.

The International Graphite company website provides additional details on operational capabilities and strategic positioning across global markets.

Competitive advantages emerging from the strategy:

• First-mover advantage in Western processing networks providing market positioning benefits

• Established customer relationships across multiple regions and applications

• Proven operational capabilities demonstrating execution competency

• Scalable expansion framework enabling responsive market development

Risk Factors and Mitigation Strategies

Execution Risk Management

The complexity of multi-jurisdictional development creates potential execution risks including regulatory delays, permitting challenges, and technical integration issues. International Graphite Ltd's global processing strategy mitigates these risks by preventing single-point failures from affecting the entire strategy.

Market Risk Considerations

Graphite pricing volatility, customer qualification delays, and competitive responses from established producers represent ongoing market risks. Diversification across industrial, fire safety, and battery markets reduces exposure to single-segment downturns.

Financial Risk Mitigation

The staged capital deployment approach reduces financial risk compared to large single-facility development. Government grant support, joint venture structures, and third-party processing agreements further reduce capital requirements and execution risks.

Strategic Implications for Critical Minerals Sector

International Graphite Ltd's global processing strategy demonstrates how smaller-scale, distributed processing networks can compete effectively with traditional large-scale, centralised production models. The approach addresses multiple market needs simultaneously: supply chain diversification, regional market access, and value-added processing capabilities.

This framework provides insights applicable across critical minerals sectors where geographic concentration creates supply vulnerabilities and customer diversification needs. However, the success metrics will be measured through operational facility performance, customer qualification achievements, and financial returns across the multi-hub network.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and company plans. Actual results may vary significantly from projected outcomes due to market volatility, execution challenges, regulatory changes, and competitive dynamics. Investors should conduct independent research and consider professional advice before making investment decisions.

Looking for Exposure to Critical Minerals Processing?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant graphite and critical minerals discoveries across the ASX, empowering subscribers to identify actionable opportunities in this rapidly evolving sector ahead of the broader market. Explore historic examples of exceptional returns from major mineral discoveries on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to secure your competitive advantage in critical minerals investing.