July 13, 2026

The World's Most Dangerous 33 Kilometres: Why Hormuz Holds Global Energy Hostage

Every major maritime chokepoint carries strategic weight, but none concentrates as much geopolitical risk into as little physical space as the Strait of Hormuz. At its narrowest crossing, the waterway measures just 33 kilometres across, with two designated shipping lanes of only 3 kilometres each in width. Through this improbably tight corridor flows roughly 20 to 21 percent of the world's daily crude oil consumption. The Iran attack on ship in Strait of Hormuz incidents of July 2026 have thrown this critical passage into sharp focus, threatening global energy security in ways that extend far beyond the immediate military exchanges.

When big ASX news breaks, our subscribers know first

A Corridor That Cannot Be Replaced

The geography of the Strait of Hormuz is not incidentally dangerous. It is structurally designed by nature to be a pressure point. The Persian Gulf is essentially a semi-enclosed basin, and Hormuz is its only maritime exit. Every barrel of crude oil loaded at Ras Tanura, every liquefied natural gas cargo departing Qatar's North Field, and every fertiliser shipment bound for South Asian agricultural markets must pass through this narrow passage before reaching open ocean.

Partial alternatives do exist on paper. Saudi Arabia operates the East-West Pipeline (Petroline) with a capacity of roughly 5 million barrels per day, and the UAE's Abu Dhabi Crude Oil Pipeline can carry approximately 1.5 million barrels per day to the port of Fujairah, bypassing Hormuz entirely. However, combined pipeline capacity falls significantly short of the roughly 17 to 18 million barrels per day that typically transit the strait, leaving the world structurally dependent on Hormuz remaining open.

This irreplaceability is precisely what gives Iran its outsized leverage. Tehran controls the northern coastline of the strait and possesses a layered anti-access arsenal, including coastal missile batteries, fast-attack naval craft, submarine capabilities, and sea-mine stockpiles. This allows it to threaten the corridor without requiring a conventional naval confrontation with superior powers. Reviewing the current crude oil prices makes clear just how sensitive these markets are to any disruption signal from the region.

The Tanker War Blueprint: History as Strategic Template

The current crisis did not emerge from a vacuum. Between 1984 and 1988, during the Iran-Iraq War, more than 400 commercial vessels were attacked in what became known as the Tanker War, a period that effectively established the strategic playbook still being referenced today. Both Iran and Iraq targeted each other's oil exports as an economic warfare instrument, dragging neutral shipping into the conflict zone.

That historical episode demonstrated several enduring dynamics that analysts continue to track:

- Tanker attacks produce immediate insurance premium spikes that compound shipping costs even when physical damage to individual vessels remains limited

- States with significant energy import dependencies are disproportionately affected, absorbing both price and supply security risk simultaneously

- International naval escorts can partially mitigate but never fully eliminate the risk premium embedded in operating within a contested strait

- Each escalation cycle tends to produce crude oil price responses ranging from 8 to over 30 percent depending on the severity and perceived duration of the disruption

Iran has periodically invoked the threat of strait closure at moments of maximum geopolitical pressure, notably in 2012 during peak nuclear sanctions and again in 2019 following attacks on tankers in the Gulf of Oman. Each episode has produced measurable market volatility, conditioning traders and energy buyers to treat Hormuz incidents as high-priority price signals. For further context, the broader crude oil price analysis for 2025 highlights how fragile these pricing equilibria can be.

July 2026: A 48-Hour Escalation That Collapsed a Ceasefire

What Triggered the Initial Strike?

The events of July 11 and 12, 2026 represent one of the most compressed escalation sequences the strait has witnessed in decades. According to Reuters, Iranian Revolutionary Guard Corps naval forces struck the M/V GFS Galaxy, a Cyprus-flagged container vessel, on July 11. The attack caused significant engine room damage, disabled the ship, ignited an onboard fire, and resulted in one crew member being reported missing. Iranian authorities characterised the strike as a response to the vessel operating on what Tehran considers an unauthorised shipping route.

The routing dispute at the centre of this standoff carries significant legal and strategic weight. Iran's position holds that commercial vessels must use an approved corridor running along the Iranian coastline, effectively placing transiting ships within Iranian oversight and interdiction range. The United States and United Kingdom have formally recommended an alternative passage through Omani territorial waters, a routing that avoids Iranian-controlled lanes but adds transit complexity.

Within 24 hours, Iranian forces struck a second vessel on July 12, a move that effectively shattered the fragile interim ceasefire arrangement. The Guardian reports that the U.S. military launched retaliatory strikes on both days, targeting Iranian missile storage facilities, drone stockpiles, and coastal radar installations. The Pentagon framed these responses as a direct consequence of Iran's ceasefire violations, establishing an escalation dynamic with no immediate off-ramp visible.

The transition from a single vessel strike to mutual military exchanges involving radar infrastructure and weapons storage facilities within 48 hours illustrates how quickly a localised maritime incident can metastasise into a multi-domain geopolitical confrontation.

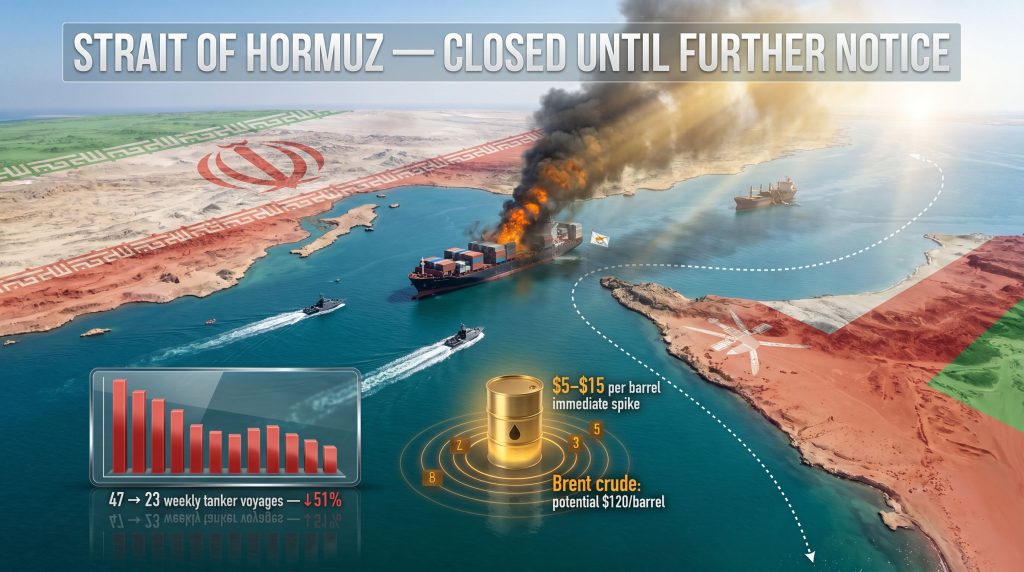

The Shipping Collapse: Quantifying the Immediate Impact

The market response from the shipping industry was rapid and measurable. Weekly tanker voyages through the strait fell from 47 to approximately 23, representing a 51 percent reduction in transit volume within days of the initial attack. This decline reflects not simply vessel damage or physical blockage, but the collective risk recalculation of shipping operators worldwide.

| Metric | Pre-Incident (Weekly) | Post-Incident (Weekly) | Change |

|---|---|---|---|

| Tanker voyages through Hormuz | 47 | 23 | -51% |

| India-bound foreign ships in Persian Gulf | Multiple | Very few | Sharp decline |

| New vessel dispatches planned | Active | Suspended | Indefinite hold |

| Indian vessels west of Hormuz | ~6 | ~6 | Stationary |

Several dynamics are furthermore compounding this traffic collapse:

- Major shipping lines have suspended new vessel dispatch decisions pending a full security reassessment of the corridor

- War risk insurance premiums for Persian Gulf transits are expected to surge, with underwriters recalibrating Gulf exposure models in light of the ceasefire collapse

- Vessels already positioned west of Hormuz are largely engaged in regional trade and are not scheduled for immediate evacuation

- Industry tracking confirms that any return to pre-incident normalcy in shipping movement has been pushed back indefinitely

An important and often overlooked dimension of the war risk insurance market is how quickly premium spikes translate into structural cost increases across the entire supply chain. When insurers reprice Gulf transit risk, the cost increase flows through to freight rates, which in turn flow through to delivered energy prices, creating an inflationary transmission mechanism that operates independently of physical supply disruption.

India's Dual Exposure: Crew Safety and Supply Chain Risk

For India, the July 2026 incidents carry a distinctly elevated level of consequence. The M/V GFS Galaxy carried Indian crew members, immediately elevating the incident beyond a bilateral U.S.-Iran confrontation into a matter with direct humanitarian and diplomatic dimensions for New Delhi. India's maritime regulator, the Directorate General of Shipping (DG Shipping), is actively monitoring developments and may issue updated advisories for Indian seafarers operating in the region.

Approximately half a dozen Indian-operated vessels are currently positioned west of Hormuz, though tracking sources confirm that most of these ships are engaged in regional trade operations and are not immediately scheduled for strait transit.

India's energy exposure to this crisis operates across two distinct channels worth separating analytically:

Channel 1: Crude Oil and Petroleum Products

India ranks among the world's largest crude oil importers, with West Asia historically supplying a substantial share of its petroleum input requirements. Senior officials from India's petroleum ministry confirmed that domestic buffer stocks of crude oil, petroleum products, and natural gas are currently at sufficient levels. Cargo sourcing arrangements from non-Gulf producing regions had been pre-positioned as a contingency measure. The official stance characterises the current situation as one of active monitoring rather than emergency response.

Channel 2: Fertiliser Supply Chains

This second dimension receives considerably less attention in mainstream coverage but carries significant strategic weight. The Strait of Hormuz serves as a critical transit corridor for ammonia and urea shipments destined for South and Southeast Asian agricultural markets. The Persian Gulf region is a dominant global producer of nitrogen-based fertilisers. Consequently, any prolonged disruption to Hormuz shipping would directly affect planting-season input availability across import-dependent agricultural economies, including India. Unlike crude oil, fertiliser supply chains have limited alternative routing options and smaller strategic reserve buffers, making this sector particularly vulnerable to sustained disruption.

The next major ASX story will hit our subscribers first

Competing Leverage: What Each Party Stands to Gain or Lose

Understanding the strategic calculus of the key actors is essential for assessing how this crisis is likely to evolve.

Iran's position is built on the asymmetric leverage embedded in Hormuz geography. A declared strait closure, even one that is not fully enforced, produces immediate global energy market disruption that is disproportionate to the naval resources required to threaten it. The routing dispute provides Tehran with a structured justification for interdiction actions that stops short of declaring outright war on international shipping. Striking a second vessel within 24 hours signals a deliberate escalation posture rather than a reactive or accidental incident.

The U.S. strategic constraint is equally structural. Maintaining freedom of navigation through Hormuz is a foundational commitment of American naval doctrine, creating an obligation to respond to Iranian interdiction that is difficult to walk back without signalling strategic retreat. Retaliatory strikes on missile storage and radar infrastructure aim to degrade Iranian interdiction capacity without triggering a full-spectrum military confrontation.

Oman's role deserves particular attention. Muscat has historically served as a back-channel diplomatic intermediary between Washington and Tehran, and the U.S.-UK recommendation to route vessels through Omani territorial waters implicitly positions Oman as a stabilising actor. Gulf Cooperation Council members, particularly the UAE and Saudi Arabia, face direct economic exposure if Hormuz suppression continues, creating additional regional pressure for diplomatic resolution. In this context, OPEC's market influence becomes a critical factor in how quickly stabilising forces can reassert themselves.

Three Scenarios for What Comes Next

The trajectory of this crisis is genuinely uncertain, and investors and supply chain managers should be stress-testing across a range of outcomes rather than anchoring to a single base case.

Scenario 1: Rapid De-escalation

Omani or third-party diplomatic intervention produces a negotiated resumption of standard shipping lane access within days. Tanker traffic recovers toward pre-incident levels within two to three weeks. Oil price impact remains contained below a $10 per barrel premium above pre-incident benchmarks. Assessed as low probability given ceasefire collapse.

Scenario 2: Sustained Partial Closure

Iran maintains selective interdiction, targeting vessels on disputed routes while allowing some traffic through the Omani corridor. War risk insurance premiums remain structurally elevated for 60 to 90 days. Global crude prices stabilise at a 10 to 20 percent premium above pre-incident levels. India accelerates strategic petroleum reserve drawdown and intensifies diversification of import sourcing. Assessed as moderate probability.

Scenario 3: Prolonged Confrontation

Continued U.S.-Iran military exchanges disable Iranian coastal radar and missile infrastructure. Iran retaliates through sea-mine deployment or fast-attack craft campaigns against tanker traffic. Hormuz transit volumes fall below 40 percent of normal capacity for an extended period. Global energy markets enter a sustained supply shock, with Brent crude potentially testing price levels not seen since the 2022 post-invasion energy crisis. Assessed as lower probability but highest impact.

The critical variable that separates Scenario 2 from Scenario 3 is whether Iran escalates from selective vessel interdiction to active lane denial through mining or sustained naval engagement. The former is manageable with insurance repricing and routing adjustments; the latter triggers a qualitatively different level of global energy market stress.

The broader oil price shock experienced by energy executives in recent years demonstrates just how rapidly market confidence can be shaken by geopolitical events of this nature.

Oil Market Price Discovery: What Monday's Open Will Reveal

At the time of the initial July 11 attack, global energy markets were closed, deferring the price discovery response to the following Monday session. Historical Hormuz disruption events have produced immediate crude price responses in the range of $5 to $15 per barrel, with the magnitude determined primarily by market assessments of disruption duration and the credibility of the threat to sustained supply.

The 51 percent reduction in weekly tanker voyages, if maintained, would represent a supply shock of significant magnitude. However, several moderating factors exist. OPEC+ spare capacity, particularly from Saudi Arabia and the UAE, provides a partial buffer. Strategic petroleum reserves held by IEA member nations represent another potential release mechanism. The uncertainty about whether Iran can actually enforce a full closure rather than a partial interdiction posture will, furthermore, temper the most extreme price responses.

What markets will be pricing on reopening is not just the physical supply impact of current disruption, but the option value of further escalation — a probability-weighted assessment of how bad things could get if the situation continues to deteriorate. That uncertainty premium, rather than current supply shortfalls, is likely to be the dominant driver of initial price movements. In addition, the LNG supply outlook for the broader region will be closely scrutinised as buyers assess alternative sourcing contingencies.

Frequently Asked Questions

What ship did Iran attack in the Strait of Hormuz?

Iranian Revolutionary Guard Corps forces struck the M/V GFS Galaxy, a Cyprus-flagged container vessel, on July 11, 2026. The attack caused engine room damage, triggered an onboard fire, disabled the vessel, and resulted in one crew member being reported missing. The Iran attack on ship in Strait of Hormuz represents one of the most consequential maritime incidents the corridor has witnessed in years.

Why did Iran attack the ship?

Iran characterised the strike as a response to the vessel using an unauthorised shipping route, asserting that commercial ships must use an approved corridor running along the Iranian coastline rather than through the centre of the strait.

Has Iran formally closed the Strait of Hormuz?

Following the July 11 attack, Iranian authorities declared the strait closed until further notice. A full physical enforcement of this closure would require sustained naval operations and would represent a dramatic escalation with significant consequences for global energy markets.

How much oil transits the Strait of Hormuz daily?

Approximately 20 to 21 percent of global daily oil consumption transits the Strait of Hormuz, making it the single most strategically important energy chokepoint in the world. The EIA has historically estimated this at around 17 to 18 million barrels per day.

What is the alternative route being recommended?

The United States and United Kingdom have formally recommended that commercial vessels use an alternative passage through Omani territorial waters to avoid Iranian-controlled shipping corridors during the current period of elevated risk.

What is India's current energy security position?

India's petroleum ministry has confirmed that domestic buffer stocks of crude oil, petroleum products, and natural gas are currently at adequate levels. Cargo sourcing arrangements from non-Gulf regions have been pre-positioned, and India's Directorate General of Shipping is actively monitoring the situation and may issue updated seafarer advisories.

What happened to the U.S.-Iran ceasefire?

The ceasefire arrangement collapsed following the back-to-back vessel attacks on July 11 and 12. U.S. military forces launched retaliatory strikes on both days, targeting Iranian missile storage facilities, drone stockpiles, and coastal radar installations. The Iran attack on ship in Strait of Hormuz, occurring twice in rapid succession, made de-escalation politically untenable for Washington in the short term.

Disclaimer: This article contains forward-looking scenario analysis and market projections based on historical precedent and current geopolitical assessments. Actual outcomes may differ materially from scenarios described. This content does not constitute financial or investment advice. Readers should conduct independent research before making investment decisions based on geopolitical risk assessments.

Want to Know Which ASX Mining Stocks Could Benefit From Rising Energy Market Volatility?

Geopolitical shocks like the Hormuz crisis ripple across commodity markets, creating rapid, time-sensitive opportunities in ASX-listed resource and energy stocks that demand immediate attention. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they are announced — explore historic discoveries and their extraordinary returns to understand the scale of opportunity, then begin your 14-day free trial to ensure you're positioned ahead of the broader market.