June 22, 2026

The Strait of Hormuz as a Geopolitical Pressure Valve: What Iran's Contested Ceasefire Means for Global Energy Markets

Few geographic features carry the economic weight of a 33-kilometre-wide waterway threading between Iran and Oman. The Strait of Hormuz has long functioned less as a simple maritime passage and more as a barometric instrument for global risk appetite, one whose readings shift entire commodity markets the moment diplomatic conditions deteriorate. The Iran war ceasefire and Strait of Hormuz closure has intensified scrutiny of this critical waterway, demanding a structured examination of physical geography, geopolitical leverage mechanics, and commodity pricing psychology under uncertainty.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is the World's Most Consequential Shipping Chokepoint

The Numbers That Define Global Energy Dependency

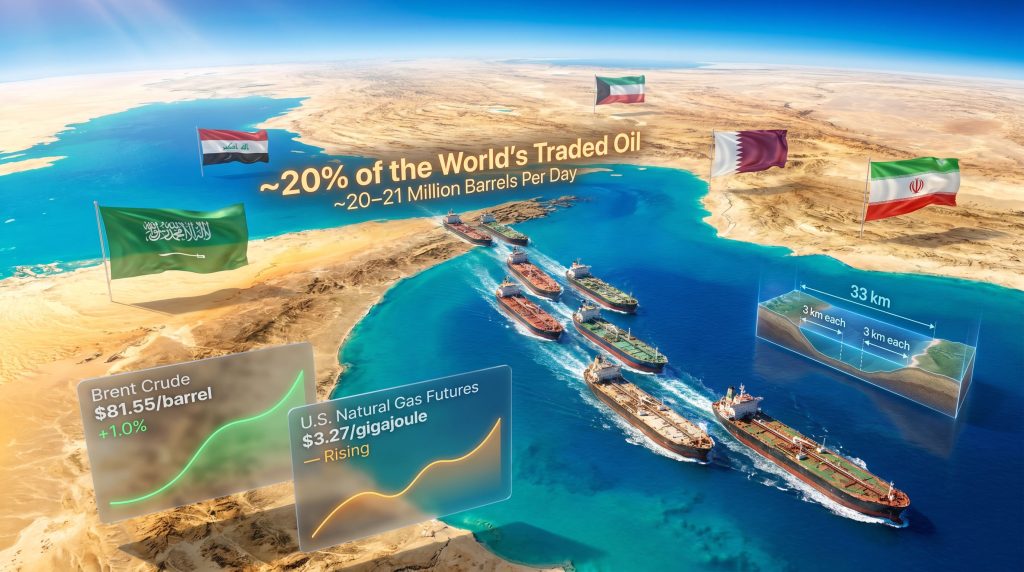

The concentration of global energy flow through a single narrow waterway is a structural vulnerability that decades of infrastructure investment have only partially addressed. Approximately 20% of the world's traded oil, equivalent to roughly 20 to 21 million barrels per day, transits through the Strait of Hormuz. The strait serves as the sole meaningful maritime exit for crude exports from Saudi Arabia, Iraq, the UAE, Kuwait, and Iran itself.

At its most constrained point, the strait measures just 33 kilometres across, and the two designated navigable shipping channels within that space are each only 3 kilometres wide. Traffic management in these lanes is among the most complex in global maritime operations, with inbound and outbound supertankers sharing corridors separated by a 3-kilometre buffer zone.

The energy dependency extends well beyond crude oil. Qatar, one of the world's largest exporters of liquefied natural gas, routes virtually all of its LNG shipments through Hormuz. For Asian importers in particular, including Japan, South Korea, and increasingly India, this creates a compounding exposure across both oil and gas supply chains simultaneously. Furthermore, the LNG supply outlook for 2025 and beyond adds further complexity to an already strained global energy picture.

Key Insight: No other single geographic chokepoint concentrates this level of global energy exposure. A credible closure, even a partial or contested one, is sufficient to trigger immediate commodity repricing across Brent crude, natural gas futures, and energy equities worldwide.

Comparing Hormuz to Other Strategic Chokepoints

| Chokepoint | Daily Oil Flow (approx.) | Viable Bypass Route? | Closure Risk Level |

|---|---|---|---|

| Strait of Hormuz | ~20–21 million bpd | Partial (Saudi East-West pipeline) | Very High |

| Suez Canal | ~9–10 million bpd | Yes (Cape of Good Hope) | Moderate |

| Strait of Malacca | ~16 million bpd | Limited | Moderate |

| Bab el-Mandeb | ~6–7 million bpd | Yes (via Suez bypass) | High |

What distinguishes Hormuz from every other chokepoint is the near-absence of a credible full-scale bypass. The Saudi East-West Abqaiq-Yanbu pipeline can divert approximately 5 million barrels per day around the strait, but this represents less than a quarter of typical Hormuz throughput. For the majority of Persian Gulf oil, there is simply no alternative route.

What Is Actually Happening: Confirmed Facts Versus Disputed Claims

The Ceasefire Framework: Fragile by Design

Understanding the current situation requires separating verified developments from competing narratives. The sequence of events as reported across multiple international outlets points to a cascading breakdown in diplomatic momentum:

- U.S. and Iranian diplomatic delegations were scheduled to convene in Switzerland with the stated goal of reaching a durable and permanent peace arrangement

- The meeting was cancelled after Israeli military operations resumed in Lebanon, which Tehran characterised as a direct violation of the existing ceasefire architecture

- Iran's conditions for a sustainable agreement reportedly encompass a comprehensive regional ceasefire covering Lebanon, the release of frozen Iranian sovereign assets, and guaranteed maritime security for Persian Gulf shipping corridors

- The framework as it stands is best understood as a contested truce rather than a binding settlement, with both sides maintaining incompatible interpretations of what the ceasefire actually prohibits

The Hormuz Closure Claim: Confirmed and Disputed

| Claim | Source | Status |

|---|---|---|

| Iran announced closure of the Strait of Hormuz | Iranian state media, multiple international outlets | Reported, not independently verified |

| Commercial vessels continued transiting the strait | U.S. officials | Disputes Iran's closure claim |

| Israeli strikes in Lebanon triggered Iran's response | Multiple regional outlets | Broadly reported |

| Ceasefire framework remains nominally active | Diplomatic sources | Contested |

Critical Distinction: The strategic significance of Iran's closure announcement lies not in whether the strait is physically blocked, but in the credible threat signal it sends to energy markets. Even a disputed closure claim is sufficient to reprice risk premiums across global oil benchmarks.

Who Said What: A Competing Narrative Framework

The information environment surrounding the Iran war ceasefire and Strait of Hormuz closure is itself a contested space, with each party advancing a narrative that serves distinct strategic objectives. According to reporting from The Guardian, ceasefire talks remain fragile amid unresolved preconditions:

- Tehran's position: Israeli military actions in Lebanon constituted a ceasefire breach, justifying Iran's closure announcement as both a retaliatory and protective measure

- Washington's counter-position: U.S. officials stated there was no observable evidence of physical disruption, with commercial shipping traffic continuing to move through the waterway without interruption

- Market interpretation: Regardless of physical reality, the announcement itself functions as a geopolitical instrument, a form of economic leverage deployed within a broader negotiating architecture that Iran has refined over decades

How Does a Hormuz Closure, Real or Threatened, Cascade Through Global Commodity Markets?

Scenario 1: Contested Closure (Current Situation)

The current environment represents a classic contested closure scenario, where the threat is credible enough to move markets without the physical disruption required to trigger emergency response protocols. Consequently, this drives oil market volatility well beyond what fundamentals alone would justify:

- Brent crude experiences an immediate risk premium spike of 3 to 8% within 24 to 48 hours of a credible closure announcement

- Natural gas futures, particularly European TTF and U.S. Henry Hub benchmarks, reprice upward as LNG supply uncertainty increases

- Shipping insurance war risk premiums escalate rapidly for vessels operating in the Persian Gulf and Gulf of Oman

- Current market data point: Brent crude was trading at approximately $81.55 per barrel as of 22 June 2026, reflecting roughly a 1% intraday gain attributable to Hormuz-related uncertainty

Scenario 2: Partial Physical Closure (Escalation Path)

Should Iran move beyond announcement to selective enforcement, the market consequences escalate substantially:

- Iranian naval assets enforce transit restrictions targeting specific flag states or vessel categories

- Saudi Arabia activates the East-West Abqaiq-Yanbu pipeline at its capacity ceiling of approximately 5 million barrels per day, providing partial relief but leaving the majority of Gulf exports disrupted

- Global oil prices potentially breach $90 to $100 per barrel within two to four weeks, depending on duration and scope

- OPEC+ emergency response mechanisms are triggered, though spare capacity deployment introduces meaningful time lags before supply relief materialises

Scenario 3: Full Closure with Military Enforcement (Tail Risk)

A complete, enforced closure of the Strait of Hormuz would represent the most severe energy supply shock in over five decades:

- IEA Strategic Petroleum Reserve coordinated release protocols would be activated across member states

- Shipping re-routing via the Cape of Good Hope adds 10 to 15 days to typical voyage times and significantly elevates freight costs across all affected trade lanes

- Global recession risk escalates materially, with estimated economic damage reaching $1 to $2 trillion in global GDP impact per month of sustained closure based on historical modelling frameworks

- The 1973 Arab Oil Embargo remains the closest historical parallel, though the volume of oil at stake today is substantially larger

What Are Iran's Strategic Objectives in Using Hormuz as Leverage?

The Strait as a Negotiating Instrument

Iran's periodic invocation of Hormuz closure serves a multi-layered strategic function that extends well beyond any single diplomatic episode. It is worth examining this pattern as a systematic behaviour rather than an isolated crisis response:

- Economic coercion: Threatening global oil supply creates immediate pressure on major powers to engage diplomatically rather than escalate militarily, effectively raising the cost of inaction for Washington and its allies

- Domestic political signalling: Demonstrates resolve to a domestic audience and to hardline factions within Iran's political structure who would otherwise characterise negotiations as capitulation

- Ceasefire architecture leverage: Positions Iran as a party whose core demands, including asset unfreezing, Lebanon stability, and maritime security guarantees, must be addressed before regional stability can be restored

- Alliance deterrence: Signals to both U.S. and Israeli decision-makers that military escalation carries direct, measurable global economic consequences rather than purely regional ones

Strategic Insight: Iran does not need to physically close the strait to achieve its objectives. The credible threat of closure, repeatedly invoked and occasionally partially enforced across multiple decades, is sufficient to extract diplomatic concessions and maintain negotiating relevance in forums where Iran would otherwise be outmatched.

Iran's Core Ceasefire Demands: A Structured Overview

| Demand Category | Specific Requirement | Likelihood of U.S. Concession |

|---|---|---|

| Regional security | Comprehensive ceasefire including Lebanon | Low to Moderate |

| Financial | Release of frozen Iranian sovereign assets | Moderate |

| Maritime | Guaranteed shipping security in Persian Gulf | Moderate to High |

| Nuclear | Implicit linkage to sanctions relief | Low |

The financial dimension of Iran's demands deserves particular attention. Frozen Iranian assets, estimated at between $6 billion and $10 billion depending on the accounting framework used, represent a concrete deliverable that Washington has previously used as a negotiating chip. Their release would carry meaningful domestic political symbolism for Tehran while remaining technically reversible from Washington's perspective.

How Are Global Energy and Commodity Markets Responding?

Commodity Snapshot: 22 June 2026

| Commodity | Price | Movement |

|---|---|---|

| Brent Crude | $81.55/barrel | +1.0% |

| Gold | $4,164/ounce | Slight decline |

| Iron Ore (Singapore) | $98.85/tonne | Declining |

| U.S. Natural Gas Futures | $3.27/gigajoule | Rising |

| AUD/USD | ~US$0.70 | Stable |

Why Are Energy and Safe-Haven Assets Diverging?

The current divergence between rising oil prices and fading gold is analytically significant. Markets are not pricing a full-scale conflict escalation but rather a period of elevated uncertainty with a meaningful probability of diplomatic resolution. Monitoring crude oil price trends helps contextualise whether this premium is historically consistent with similar threat episodes:

- Brent crude rising reflects direct supply-side Hormuz risk being priced into near-term contracts

- Gold declining indicates that investors are not yet positioning for systemic financial instability or full military conflict, suggesting the ceasefire, however fragile, retains some credibility in market pricing

- Iron ore falling reflects entirely separate demand-side dynamics from China's industrial sector, largely disconnected from Persian Gulf developments

- Natural gas rising captures LNG supply chain sensitivity to Persian Gulf instability, particularly for Asian importers whose dependency on Qatari exports creates direct exposure to Hormuz disruption

This pattern of selective repricing, oil up, gold fading, industrial metals down, is consistent with historical episodes where Hormuz closure threats have been real but ultimately unenforceable.

The next major ASX story will hit our subscribers first

What Historical Precedents Tell Us About Hormuz Closure Scenarios

Previous Hormuz Threat Episodes and Market Outcomes

| Year | Trigger Event | Oil Price Response | Duration of Elevated Risk |

|---|---|---|---|

| 2012 | Iranian nuclear sanctions standoff | Brent peaked ~$128/barrel | 3 to 4 months |

| 2019 | U.S.-Iran tensions post-JCPOA withdrawal | Brent spiked ~15% in 2 weeks | 6 to 8 weeks |

| 2020 | Soleimani assassination | Brent +4% within 48 hours | 2 to 3 weeks |

| 2024 to 2025 | Houthi Red Sea disruption (adjacent risk) | Shipping costs +200 to 300% | 6+ months |

The pattern across these episodes reveals a consistent dynamic: markets price a 3 to 10% Brent premium during active Hormuz threat periods, and that premium compresses rapidly once credible de-escalation signals emerge. The 2024 to 2025 Houthi disruption of Red Sea shipping lanes is particularly instructive, because it demonstrated that even a partial chokepoint disruption, affecting a less critical waterway than Hormuz, can sustain elevated shipping costs and supply chain uncertainty for six months or longer when no clear resolution pathway exists. In addition, OPEC's global influence on production decisions during these episodes often determines whether price spikes are absorbed or amplified.

What Does This Mean for Australian Markets and ASX Energy Investors?

The ASX's Indirect Hormuz Exposure

Australia does not import Persian Gulf crude at meaningful scale, but the ASX carries indirect exposure through several distinct transmission mechanisms that investors should understand clearly:

- Energy sector repricing: ASX-listed energy producers benefit from sustained elevated oil prices. Brent above $80 per barrel supports the economics of domestic LNG projects and increases the valuation multiples applied to energy reserves

- Currency dynamics: A sustained oil price spike typically strengthens commodity-linked currencies, though the AUD/USD sitting at US$0.70 reflects current market ambivalence about whether the Hormuz situation will escalate materially

- BHP (ASX: BHP) and major diversified miners: Elevated energy input costs compress operational margins. BHP's current cost overruns at its Canadian potash project, which has escalated from approximately US$4.9 billion to US$6.9 billion, illustrate how energy cost pressures compound within capital-intensive mining operations

- Investor sentiment transmission: Geopolitical uncertainty introduces a risk-off dynamic that disproportionately affects small-cap and speculative ASX listings, as capital rotates toward perceived safety

The ASX Opening Context: Week 26, 2026

Australian equities entered Week 26 in a cautious posture, with the S&P/ASX 200 having closed the prior Friday at 8,828.7. The index opened approximately 10 points lower on 22 June 2026, with trader hesitation attributed directly to unresolved Hormuz and ceasefire uncertainty. ASX commodity pressure has been building incrementally, and the absence of directional guidance from Wall Street, closed for the Juneteenth public holiday, removed a key reference point that Australian traders typically use to calibrate overnight sentiment.

Investor Consideration: In periods of contested geopolitical risk, where the threat is real but the physical outcome remains uncertain, energy sector volatility typically precedes broader equity market repricing. Monitoring Brent crude as a leading indicator for ASX sentiment is an analytically sound approach during this period.

What Are the Most Likely Scenarios for the Coming Weeks?

Scenario Probability Matrix

| Scenario | Description | Estimated Probability | Oil Price Implication |

|---|---|---|---|

| Diplomatic re-engagement | Switzerland talks rescheduled; ceasefire holds nominally | 45% | Brent stabilises $78 to $84/barrel |

| Prolonged stalemate | No talks; periodic closure threats continue | 35% | Brent $82 to $92/barrel |

| Escalation via Lebanon | Further Israeli strikes trigger Iranian military response | 15% | Brent $90 to $105/barrel |

| Full Hormuz closure | Physical enforcement of strait closure | 5% | Brent $110+/barrel |

The probability-weighted central case points toward a sustained period of elevated but manageable oil prices, with diplomatic re-engagement remaining the modal outcome even if the timeline for resumed Switzerland talks extends beyond initial expectations. The tail risk of full physical closure, while carrying catastrophic economic implications, is constrained by Iran's own economic interest in unimpeded oil export revenue. PBS NewsHour reports that an initial deal to extend the ceasefire and open the strait has been reached, though significant challenges remain on both sides.

Frequently Asked Questions: Iran Ceasefire and Strait of Hormuz

Has Iran Actually Closed the Strait of Hormuz?

As of late June 2026, the Iran war ceasefire and Strait of Hormuz closure announcement remains disputed. Iran has declared a closure in response to alleged ceasefire violations, but U.S. officials have stated that commercial vessels continue to transit the waterway. The situation is best characterised as a contested closure announcement rather than a verified physical blockade, with the gap between claim and physical reality itself functioning as a strategic ambiguity that Iran has an interest in maintaining.

Why Did the U.S.-Iran Switzerland Peace Talks Collapse?

The scheduled diplomatic meeting in Switzerland was cancelled following Israeli military strikes in Lebanon. Tehran characterised these strikes as a violation of the existing ceasefire framework and withdrew from the scheduled talks as a direct consequence, signalling that its participation in any peace process is conditional on Israel's behaviour in adjacent theatres of conflict.

What Would a Real Hormuz Closure Mean for Oil Prices?

A sustained, physically enforced closure of the Strait of Hormuz would likely push Brent crude above $100 per barrel within weeks, trigger coordinated IEA strategic reserve releases, and significantly elevate global inflation and recession risk. The economic damage from a prolonged closure would extend well beyond energy markets into every sector with meaningful energy input costs.

How Does the Hormuz Situation Affect Australian Investors?

Australian markets face indirect exposure through elevated energy input costs for industrial and mining operations, commodity currency dynamics affecting the AUD/USD exchange rate, and broader risk-off sentiment that reduces appetite for speculative equity exposure. ASX energy producers may benefit from higher oil prices, while capital-intensive sectors face meaningful margin pressure.

What Are Iran's Conditions for a Permanent Ceasefire?

Iran's reported demands include a comprehensive regional ceasefire encompassing Lebanon, the release of frozen Iranian sovereign assets, and guaranteed maritime security arrangements for Persian Gulf shipping lanes. These preconditions reflect Iran's intent to use the current moment to resolve a broader set of grievances rather than simply return to the pre-conflict status quo.

Key Takeaways: Navigating the Hormuz Risk Premium

-

The Strait of Hormuz remains the single most consequential energy chokepoint in the global economy, with approximately 20% of traded oil dependent on unimpeded transit through a corridor barely 33 kilometres wide at its narrowest point

-

Iran's ceasefire announcement and Strait of Hormuz closure claim represent a strategic negotiating posture as much as a military action, with the credible threat carrying market impact independent of physical execution

-

The current situation is characterised by competing claims, a fragile truce, and unresolved diplomatic prerequisites, not a stable peace settlement

-

Commodity markets are pricing a moderate risk premium with Brent at approximately $81.55 per barrel, suggesting markets view escalation as possible but not yet probable

-

The most likely near-term path involves rescheduled diplomatic engagement and a continuation of the contested truce, with oil prices remaining elevated but below crisis thresholds

-

Investors should monitor Brent crude, U.S. natural gas futures, and Persian Gulf shipping insurance rates as the most sensitive leading indicators of escalation or de-escalation in the weeks ahead

The material in this article is provided for informational purposes only and should not be treated as investment advice. Forecasts, scenario probabilities, and price projections are analytical frameworks subject to significant uncertainty and should not be relied upon as predictions of actual outcomes. Readers are encouraged to conduct independent research and consult with a certified financial adviser before making any investment decisions.

Want to Stay Ahead of ASX Energy Opportunities Driven by Global Geopolitical Shifts?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral and energy discoveries so investors can act before the broader market catches up — explore historic discovery returns on the dedicated discoveries page to understand the magnitude of opportunities these moments can generate, then begin a 14-day free trial of Discovery Alert to position yourself ahead of the next major market-moving event.