June 22, 2026

The Energy Chokepoint That Holds the World Hostage

Every decade or so, global energy markets are reminded of a fundamental vulnerability baked into the architecture of petroleum trade: a vast share of the world's oil and gas supply passes through a single 21-mile-wide bottleneck. The Trump Iran peace deal, signed against the backdrop of one of the most consequential maritime crises in modern energy history, directly addresses this chokepoint. The Strait of Hormuz, nestled between Iran and Oman, is not merely a geographic feature — it is a lever, and when that lever moves, the entire global economy feels it.

Under normal operating conditions, roughly one-fifth of all global oil and gas supplies transit the strait. Tankers carrying crude from Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar all funnel through this narrow passage before dispersing to refineries across Asia, Europe, and beyond. No other maritime corridor concentrates so much commodity flow in so confined a space, which is precisely why energy security analysts have identified Hormuz as the single greatest systemic risk to global oil supply continuity for decades.

When hostilities broke out on February 28 and Iran moved to effectively seal the waterway, that theoretical risk became real. The cascading consequences touched every layer of the energy economy: tanker routing was thrown into chaos, marine insurance premiums surged, and import costs spiked across Asia and Europe almost simultaneously.

When big ASX news breaks, our subscribers know first

How the Conflict Escalated Before the Trump-Iran Peace Deal

The path to a Trump-Iran peace deal was not linear. It was a series of escalations, ceasefire attempts, and renewed hostilities that pushed both military and energy markets to their limits, creating what analysts have described as a global oil price shock with far-reaching consequences.

A fragile ceasefire had taken hold in April, only to collapse under renewed pressure in June. On June 10 and 11, U.S. and Iranian forces exchanged strikes on consecutive nights, representing one of the most serious escalation episodes since the war began. The threat to strike Kharg Island, Iran's primary crude oil export terminal, briefly entered the equation, sending crude benchmarks sharply higher as traders priced in potential long-term infrastructure damage.

Iran's naval posture effectively restricted commercial shipping through the strait, with Iranian state media reporting that two vessels had been targeted. U.S. Central Command disputed the characterisation of a full closure, asserting that commercial traffic continued to move through the waterway. This factual disagreement had real market consequences: the ambiguity itself sustained an elevated risk premium in crude pricing.

Simultaneously, a U.S. naval blockade on Iranian ports intensified economic pressure on Tehran, while Iranian retaliatory missile and drone campaigns struck U.S.-linked infrastructure in Bahrain and Kuwait. The broader coalition posture, combining Israeli, Gulf Arab, and U.S. military pressure across multiple fronts, created a strategic environment that ultimately drove both parties toward a negotiating table.

What the Trump-Iran Peace Deal Actually Includes

Breaking Down the Memorandum of Understanding

The preliminary framework signed between U.S. President Donald Trump and Iranian President Masoud Pezeshkian establishes a multi-point structure covering military, nuclear, economic, and energy dimensions. According to reporting from The Guardian, it is explicitly a memorandum of understanding with a 60-day window to finalise a permanent agreement.

| Deal Term | Detail |

|---|---|

| Military Ceasefire | Immediate and permanent cessation of operations on all fronts, including Lebanon |

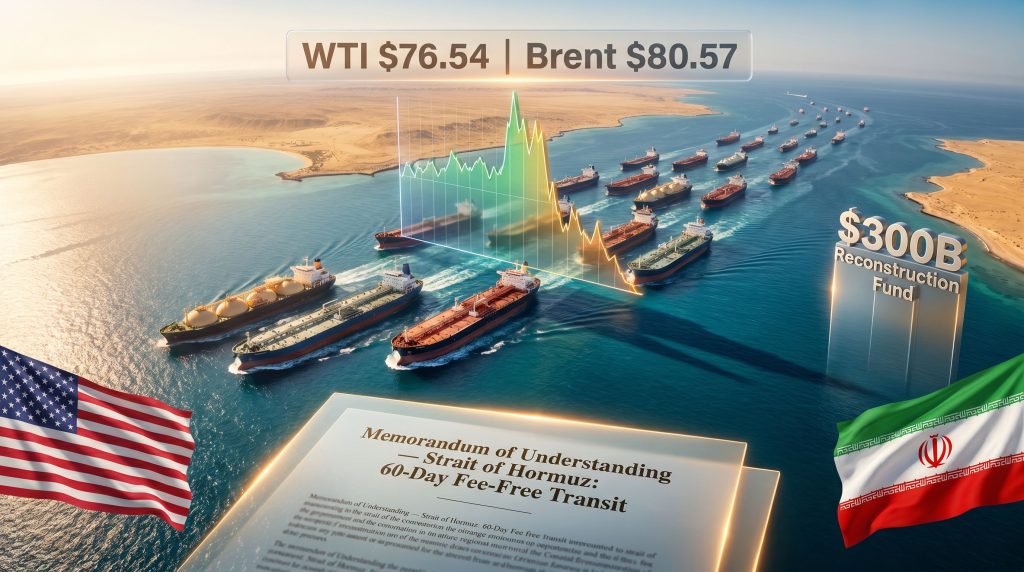

| Strait of Hormuz | Reopened with a 60-day fee-free transit window for all vessels |

| Nuclear Commitments | Iran reaffirms it will not develop or procure nuclear weapons |

| Uranium Enrichment | Downsized on-site under IAEA supervision, not full removal of nuclear material |

| Naval Blockade | U.S. naval blockade on Iranian ports lifted upon signing |

| Reconstruction Fund | Proposed $300 billion fund, primarily sourced from Gulf Arab nations |

| Sanctions | Potential waivers enabling immediate Iranian oil sales; possible full sanctions removal |

| Negotiation Window | 60-day extendable period to finalise a permanent peace agreement |

What the Deal Does Not Resolve

Despite the diplomatic momentum, several critical items remain unresolved:

- The permanent status of Iran's nuclear programme is an open negotiation item within the 60-day window, not a settled outcome

- Israel acknowledged the agreement but confirmed it was not a party to the MOU and has continued military operations against Hezbollah in Lebanon

- Iran's Foreign Ministry signalled that Washington had been shifting positions throughout negotiations, flagging the internal consistency of the framework as a concern

- No binding enforcement mechanism for the MOU's core commitments has been publicly confirmed

The Nuclear Concession Gap

One of the least-discussed but most analytically significant elements of the Trump-Iran peace deal is what the United States did not achieve on the nuclear file. Washington's opening position demanded the complete removal of all nuclear material from Iranian territory. The final MOU settles for on-site downsizing under IAEA supervision — a materially weaker outcome.

This retreat raises legitimate questions about verification architecture. How the IAEA will operationalise supervisory capacity within a 60-day negotiating window, particularly given Iran's historical record of limiting inspector access, remains undefined. For analysts tracking non-proliferation risks, this gap is not a footnote — it is a central variable in assessing the deal's durability.

Key Analytical Point: Trump cited approval from a broad coalition that included Saudi Arabia, UAE, Qatar, Turkey, Pakistan, Bahrain, Kuwait, Jordan, Egypt, and Israel. However, no formal confirmation of Iranian Supreme Leader Khamenei's personal approval has been independently verified, introducing a critical ambiguity about the deal's internal Iranian political legitimacy.

How Oil Markets Responded to the Trump-Iran Peace Deal

The Price Trajectory: From War Premium to Peace Discount

Oil market pricing during this period demonstrated a near-perfect inverse relationship between diplomatic progress and crude benchmarks. Every credible signal of ceasefire progress triggered selling pressure as traders unwound oil price volatility premiums. Every breakdown or postponement triggered sharp recoveries.

In the days surrounding the deal announcement:

- WTI Crude traded at approximately $76.54 per barrel

- Brent Crude settled near $80.57 per barrel

- Iran Heavy crude was priced at approximately $64.96 per barrel, reflecting the market's forward assessment of returning Iranian supply volumes

When U.S.-Iran talks were temporarily postponed, oil prices rebounded sharply, illustrating just how finely calibrated the market's sensitivity to diplomatic signals had become throughout the conflict period. Furthermore, WTI and Brent crude futures markets experienced some of their most volatile trading sessions in years during the peak escalation phases.

The 60-80 Million Barrel Supply Overhang

At the height of the Hormuz disruption, an estimated 60 to 80 million barrels of crude were queued for transit through the strait, waiting for passage to resume. The rapid release of this volume into Asian markets creates a near-term supply overhang that could suppress prices independent of any OPEC+ production decisions.

This backlog dynamic is distinct from conventional supply-demand analysis. Even in a scenario where Iranian export volumes return gradually, the pre-positioned tanker queue alone represents a meaningful one-time injection into Asian spot markets. Traders pricing crude forward need to account for this timing asymmetry.

Goldman Sachs has warned that Strait of Hormuz traffic patterns may never fully recover to pre-conflict norms, even with a signed agreement in place. Infrastructure changes, rerouting decisions, and altered buyer-seller relationships triggered by the disruption period may represent permanent structural shifts rather than temporary adjustments.

The IEA's 2027 Surplus Projection

The International Energy Agency has flagged the potential for a substantial oil surplus by 2027 as Middle Eastern supply progressively returns to global markets. This projection is contingent on successful implementation of the peace framework and gradual normalisation of Iranian export volumes under sanction waivers or full sanctions removal.

The surplus scenario carries significant implications for OPEC+ cohesion. Gulf producer states operate fiscal budgets calibrated around specific oil price break-even levels. A sustained price decline driven by returning Iranian volumes would test the cartel's internal discipline at a moment when several members are already managing output cut obligations. In this context, OPEC market influence will be a critical factor in whether prices stabilise or spiral further downward.

Scenario Analysis: Is the Trump-Iran Deal Durable?

Scenario 1: Full Implementation

Both parties ratify a permanent agreement within the 60-day window. Iranian oil exports resume under sanction waivers, adding meaningful volume to global supply. The $300 billion reconstruction fund is operationalised with Gulf Arab contributions. IAEA verification architecture is established and accepted by Tehran.

Market outcome: Sustained downward pressure on crude benchmarks through 2026 and 2027. The IEA surplus scenario materialises. OPEC+ faces mounting pressure to implement deeper production cuts to defend price floors.

Scenario 2: Partial Implementation

The MOU holds on military terms but permanent negotiations stall over the nuclear programme status. Iranian oil sales resume under temporary waivers but full sanctions relief is withheld. Israel continues operations in Lebanon, creating a parallel conflict thread that periodically destabilises the broader framework.

Market outcome: Moderate price normalisation with a persistent geopolitical risk premium baked in. Hormuz traffic recovers but tanker insurance costs remain elevated. Crude benchmarks settle in a range above pre-conflict levels but below peak war-premium highs.

Scenario 3: Deal Collapse

Negotiations break down within the 60-day window. The naval blockade is reimposed and Iranian enrichment activities resume without IAEA oversight. U.S. military strikes on Iranian infrastructure return to the table.

Market outcome: A sharp crude price spike. Hormuz closure risk premium re-enters market pricing. Tanker rates surge. The 60-80 million barrel queue that has already begun moving through the strait reverses course.

Historical Pattern Warning: Trump's track record during this conflict involved multiple announcements of imminent settlements that subsequently collapsed before reaching final agreement. Analysts weighting scenario probabilities should assign meaningful probability to both Scenario 2 and Scenario 3 outcomes rather than treating full implementation as the base case.

The Broader Geopolitical Fault Lines

Israel's Parallel Calculus

Israel's position within the Trump-Iran peace deal framework is structurally ambiguous. The Israeli government acknowledged the agreement and expressed appreciation for Trump's diplomatic efforts whilst simultaneously confirming it was not a party to the MOU. More significantly, Israeli forces have indicated they will not withdraw from Lebanon and have continued strikes on Hezbollah positions.

This creates a direct tension within the ceasefire's geographic scope. The MOU calls for a halt to operations on all fronts including Lebanon, yet Israel's active military presence in that theatre represents the most immediate near-term threat to the agreement's integrity. The Netanyahu government appears to be pursuing a dual-track strategy: nominally supporting the broader diplomatic framework whilst preserving operational freedom against Hezbollah.

Iran's Internal Fracture Lines

On the same day Trump announced the deal, Iran's parliamentary speaker and chief negotiator Mohammad Baqer Qalibaf issued a public warning to Washington against pursuing strategies that could, in his framing, reset the entire negotiating board and destabilise energy infrastructure and markets. This statement, issued from within Iran's own political establishment on the day of the announcement, signals that domestic consensus around the MOU is not uniform.

The gap between Trump's characterisation of Khamenei's approval and Iran's Foreign Ministry's considerably more cautious public framing represents a material risk factor that markets have not fully priced. In Iranian political architecture, the Supreme Leader's position is not equivalent to a head of state's signature on a treaty — and the distinction matters enormously for implementation timelines.

The next major ASX story will hit our subscribers first

How Global Energy Markets Are Structurally Changing

Infrastructure and Routing: Permanent Shifts

The Hormuz crisis has accelerated infrastructure investment across the Middle East as producers sought bypass routing to reduce strait dependency. Iraq has confirmed it will retain its Syria oil route even after Hormuz fully reopens, signalling that the infrastructure diversification triggered by the conflict is not temporary. A thorough geopolitical oil price analysis reveals that this is a strategically significant data point: even producers who benefited from the conflict's resolution are hedging against future strait vulnerability.

India's Repositioning

India's energy import bill surged 82% during the peak conflict period as elevated oil prices hit the country's import-dependent economy. Despite Hormuz reopening and the receipt of India's first post-deal LNG cargo through the strait, India has signalled it is not rushing back to Middle Eastern crude procurement. Indian energy buyers are actively diversifying sourcing toward non-Gulf suppliers, a strategic reorientation with long-term implications for OPEC+'s demand base.

India's government has also ordered a major strategic oil reserve expansion in direct response to the supply disruption, signalling a fundamental reassessment of energy security buffers at the policy level.

The ECB's Warning and European Structural Damage

The European Central Bank has noted that the Iran peace deal will not erase the energy price shock already absorbed by European economies. Structural inflation from the conflict period has a long tail. European industrial competitiveness, which was already under pressure from elevated energy costs prior to the conflict, has absorbed another layer of permanent cost escalation that monetary policy alone cannot reverse.

OPEC+ Under Pressure

OPEC oil production fell to its lowest level since 2000 during the conflict period. Kuwait has indicated output could reach 2 million barrels per day within a week of full normalisation, illustrating the rapid supply response capacity waiting to be unlocked across Gulf producers. Furthermore, OPEC's demand growth strategy is now explicitly focused on India rather than Europe — a strategic reorientation that reflects both the demand geography shift and the long-term structural decline of European oil consumption driven by accelerating EV adoption.

Key Variables to Watch

For investors and energy analysts tracking the implications of the Trump-Iran peace deal, the following variables represent the highest-information monitoring points:

- The 60-day negotiating window is the single most important variable determining whether the peace dividend is durable or transitory

- Iranian oil supply re-entry under sanction waivers represents the most immediate downside price risk for crude benchmarks

- The 60-80 million barrel tanker backlog currently exiting the strait creates a near-term supply overhang that is independent of longer-term deal outcomes

- Israel's Lebanon operations remain the most credible near-term geographic threat to the ceasefire framework

- Goldman Sachs's Hormuz traffic warning suggests that routing and infrastructure changes may have permanently altered global tanker economics regardless of diplomatic outcomes

- India's procurement diversification signals that even a successful deal will not fully restore pre-conflict Middle Eastern oil trade flows

- Iran's internal political dynamics and the unconfirmed status of Khamenei's approval introduce a verification risk that markets have not fully discounted

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Oil market forecasts, geopolitical scenario projections, and price references are inherently uncertain and subject to rapid change. Readers should conduct independent research before making any investment decisions.

FAQ: Trump-Iran Peace Deal and Oil Market Impact

Has the Trump-Iran Peace Deal Been Officially Signed?

A preliminary memorandum of understanding has been agreed between U.S. President Donald Trump and Iranian President Masoud Pezeshkian. It is a framework agreement with a 60-day window to negotiate a permanent deal. Core issues including the full status of Iran's nuclear programme remain unresolved. NPR's coverage of the agreement provides further detail on the specific terms disclosed at the time of signing.

Will the Strait of Hormuz Fully Reopen Under the Deal?

The MOU includes a commitment to reopen the strait with a 60-day fee-free transit window for vessels. Goldman Sachs has warned that traffic may never fully return to pre-conflict levels even with a signed agreement in place, citing permanent routing and infrastructure changes.

What Happens to Iranian Oil Sanctions Under the Deal?

The agreement includes potential sanction waivers to allow Iran to sell oil immediately, with the possibility of full sanctions removal subject to ongoing negotiations. However, no permanent sanctions relief has been confirmed as of the time of writing.

What Is the $300 Billion Reconstruction Fund?

The deal proposes a $300 billion reconstruction fund for Iran sourced primarily from Gulf Arab nations. The United States has indicated it will not contribute directly to the fund financially.

How Did Oil Prices React to the Peace Deal?

WTI traded near $76.54 and Brent near $80.57 in the period surrounding the announcement, reflecting a partial unwinding of the conflict-era war premium. Prices rebounded when talks were temporarily postponed, demonstrating the market's acute sensitivity to diplomatic signals.

Want to Know Which ASX Mineral Discoveries Could Deliver the Next Major Return?

The geopolitical shifts reshaping global energy markets are a reminder that commodity-driven opportunities can emerge rapidly — and that being positioned ahead of the market is everything. Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and translating complex data into actionable insights for both traders and long-term investors. Explore historic discovery returns on Discovery Alert's discoveries page to see what early positioning has meant for investors in the past, then begin your 14-day free trial at Discovery Alert to ensure you never miss the next major opportunity.