May 20, 2026

Iran conflict oil supply disruptions have become a critical concern for global energy markets, as concentrated production facilities and strategic shipping routes create systemic vulnerabilities that can rapidly escalate into worldwide economic crises. The current geopolitical tensions demonstrate how regional conflicts can trigger cascading effects across international energy systems, affecting everything from transportation fuel costs to manufacturing supply chains.

Modern energy infrastructure relies heavily on geographic chokepoints and centralised processing facilities, making them susceptible to both direct attacks and precautionary shutdowns. These vulnerabilities have created a complex web of interdependencies where localised disruptions can cascade through global markets within hours.

Understanding Critical Energy Infrastructure Vulnerabilities

Energy security threats manifest through multiple mechanisms that operate simultaneously during regional conflicts. Direct asset destruction represents the most visible threat, targeting production facilities, refineries, and storage terminals. However, oil price rally analysis suggests that insurance market disruptions often prove more immediately impactful, as coverage withdrawal forces immediate cessation of operations regardless of physical damage.

Operational precautionary shutdowns add another layer of complexity, with facility operators choosing to halt production proactively to protect assets and personnel. This creates supply shortages even when infrastructure remains physically intact.

Current Infrastructure Impact Assessment

Recent disruptions across the Middle East demonstrate these vulnerability patterns in real-time. Qatar's complete halt of LNG production eliminates approximately 19-20% of global LNG supply, given the country's position as the world's largest exporter with 77-80 million tonnes per annum capacity.

Saudi Arabia's shutdown of major refining capacity removes 550,000 barrels per day of processing capability, affecting both domestic refined product availability and export supplies. Furthermore, this represents approximately 8-10% of regional refining capacity, creating immediate bottlenecks in gasoline, diesel, and jet fuel production. Saudi exploration impact analysis indicates these disruptions could have lasting effects on regional production strategies.

Iraqi Kurdistan's production cessation eliminates 400,000 barrels per day from global crude markets, while infrastructure damage at UAE's Fujairah port and the suspension of Iraqi Kirkuk crude loadings at Turkey's Ceyhan port further constrain supply chains.

Supply Chain Vulnerability Vectors

Three distinct threat mechanisms create overlapping risks:

- Physical destruction: Direct attacks on energy infrastructure and transport vessels

- Insurance withdrawal: Coverage cancellation forcing operational shutdowns

- Precautionary closures: Voluntary production halts to protect assets and personnel

These mechanisms often activate simultaneously, amplifying supply disruption impacts beyond what individual threats might cause independently.

When big ASX news breaks, our subscribers know first

Strategic Importance of Maritime Energy Chokepoints

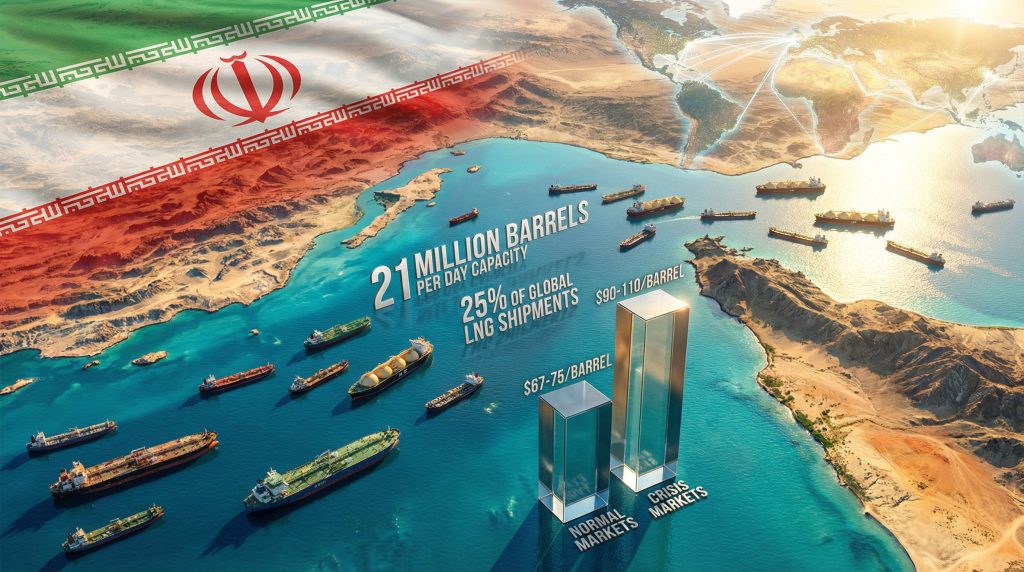

The Strait of Hormuz exemplifies how geographic constraints create systemic vulnerabilities in global energy systems. This narrow waterway, measuring just 21 nautical miles at its narrowest point, handles approximately 21 million barrels per day of petroleum liquids transit alongside 25% of global LNG shipments.

Geographic and Economic Constraints

The strait's strategic significance stems from four critical factors that distinguish it from other shipping routes:

| Factor | Normal Operations | Crisis Impact |

|---|---|---|

| Daily Oil Transit | 21 million barrels | Complete halt possible |

| LNG Flow | 25% of global supply | Asian markets most affected |

| Vessel Traffic | 70-80 tankers daily | Insurance withdrawal stops movement |

| Alternative Route Cost | Standard shipping rates | 15-25% premium via Cape route |

Insurance Market Dynamics

Maritime insurance markets demonstrate how financial mechanisms can create harder constraints than physical blockades. When insurers cancel coverage for vessels transiting conflict zones, shipping operations cease immediately regardless of navigational feasibility.

Current insurance withdrawal has created de facto closure even though the waterway remains physically navigable. Historical precedent from 2019 tanker attacks showed insurance premiums spiking to $1.5-2 million per passage, demonstrating the cost sensitivity of risk coverage.

Alternative Route Economics

Bypassing the Strait of Hormuz requires routing around the Cape of Good Hope, adding approximately 3,500 nautical miles and 12-15 additional sailing days. This alternative imposes several cost multipliers:

- Extended transit time: Additional 12-15 days sailing

- Increased fuel consumption: 3,500 nautical miles of additional distance

- Port facility adjustments: Infrastructure optimised for Strait routing requires modification

- Capital cost increases: Longer shipping cycles reduce fleet utilisation efficiency

Regional Production Shutdown Cascading Effects

Production halts across multiple Middle Eastern countries create compounding supply disruptions that affect different energy markets in distinct ways. The interconnected nature of these disruptions amplifies individual impacts through supply chain dependencies.

Qatar LNG Production Impact

Qatar's production halt carries disproportionate weight in global LNG markets due to long-term contract structures and limited short-term substitution options. Unlike crude oil, which trades heavily on spot markets, 80% of LNG moves through long-term contracts compared to 30-40% for crude oil.

Asian importers face the most severe impacts due to dependency ratios:

- Japan: 36% of LNG imports from Qatar, with 99% import dependency

- South Korea: 32-35% from Qatar via Korea Gas Corporation supply chains

- China: 15-18% from Qatar through China National Petroleum Corporation contracts

LNG supply disruptions prove particularly challenging because cryogenic systems require months to restart safely, unlike conventional oil production that can resume operations within days or weeks.

Saudi Refinery Shutdown Consequences

The closure of Saudi Arabia's largest refining facility removes 550,000 barrels per day of processing capacity, affecting multiple refined product streams:

- Gasoline production loss: 192,500 barrels per day (35% of facility output)

- Diesel production loss: 220,000 barrels per day (40% of facility output)

- Jet fuel disruption: Critical for aviation industry supply chains

- Petrochemical feedstock: Impacts plastic and synthetic material production

This single facility shutdown represents approximately $11-16.5 million daily in lost refined product revenue at current market premiums.

Iraqi Kurdistan Output Cessation

The 400,000 barrels per day production halt in Iraqi Kurdistan, combined with suspended Kirkuk crude loadings at Turkey's Ceyhan port, eliminates a significant crude oil source from global markets. This represents approximately 0.4% of global oil production but occurs during a period when multiple supply sources face simultaneous disruption.

Oil Price Volatility and Risk Premium Mechanisms

Energy markets respond to geopolitical tensions through immediate risk premium additions that often exceed actual supply disruption impacts. Current market movements demonstrate this dynamic, with Brent crude reaching $83.44 per barrel and WTI gaining to $76.26, representing 17% and 16% increases respectively over three trading sessions.

Risk Premium Structure Analysis

Iran conflict oil supply disruptions incorporate multiple premium layers during crisis periods:

| Component | Normal Markets | Crisis Markets | Premium Added |

|---|---|---|---|

| Supply/Demand Balance | $65-70/barrel | $65-70/barrel | $0 |

| Geopolitical Risk | $2-5/barrel | $15-25/barrel | $10-20 |

| Supply Disruption | $0/barrel | $10-15/barrel | $10-15 |

| Total Market Price | $67-75/barrel | $90-110/barrel | $20-35 |

Historical Precedent Comparison

The 2022 Russian invasion of Ukraine provides relevant context for current price dynamics. Following February 24, 2022, Brent crude surged from $95 to $123 per barrel within eight days, representing a 29.5% increase driven primarily by risk premiums rather than immediate supply losses.

Current price movements follow similar patterns, with Bernstein Research raising 2026 Brent assumptions from $65 to $80 per barrel while acknowledging potential spikes to $120-150 in extreme conflict scenarios. Moreover, trade war oil markets analysis suggests additional complexity from international trade tensions.

Country-Specific Energy Security Vulnerabilities

Different nations face varying degrees of energy security risk based on import dependencies, strategic reserve capacity, and alternative supply access. Asian economies demonstrate particular vulnerability due to geographic distance from alternative suppliers and high import ratios.

Asian Market Exposure Assessment

China's energy security profile reveals significant exposure through multiple channels:

- Oil import dependency: 70% of domestic consumption

- Iranian oil imports: 1.38 million barrels per day (2025 data)

- Strategic reserve capacity: 4-5 month supply buffer

- Alternative supply constraints: Limited pipeline access to non-Middle Eastern sources

Japan and South Korea face even more severe vulnerabilities:

- Import dependency: 99% for both countries

- Strategic reserves: 90-day government-mandated minimum

- Supply concentration: Heavy reliance on Middle Eastern sources

- LNG dependency: Critical for power generation and industrial processes

European Market Adaptations

European markets demonstrate greater resilience due to 2022 energy crisis adaptations, but still face significant LNG supply chain disruptions. Gas markets experience immediate price volatility, with Dutch TTF contracts, British gas prices, and European LNG prices all jumping during current disruptions.

Supply Disruption Duration Tolerance

Global energy markets can withstand short-term supply disruptions through strategic reserve deployment, but extended outages create severe shortages. Critical timeline analysis reveals escalating risk profiles:

Strategic Reserve Deployment Timeline

Week 1-2: Strategic petroleum reserves provide market stability with coordinated releases from major consuming nations

Week 3-5: Price volatility increases as reserve drawdowns accelerate and replacement supply uncertainty grows

Week 6+: Severe supply shortages emerge without alternative sources, forcing demand destruction and economic recession risks

Alternative Supply Activation Requirements

Different supply sources require varying timeframes for activation:

- OPEC spare capacity: 30-90 days for full deployment of 2-3 million barrels per day

- US shale production: 3-6 months for significant output increases

- Alternative shipping routes: Immediate availability but with 15-25% cost premiums

- Emergency reserve releases: 1-2 weeks for coordination between International Energy Agency members

Consequently, the US oil production decline further complicates alternative supply scenarios during crisis periods.

The next major ASX story will hit our subscribers first

Sectoral Economic Disruption Patterns

Energy supply disruptions propagate through the economy via multiple transmission mechanisms, with some sectors experiencing disproportionate impacts due to energy intensity or substitution limitations.

Transportation and Logistics Impacts

The transportation sector faces immediate and severe disruptions across multiple modes:

Aviation Industry:

- Jet fuel shortages: International flight cancellations and route modifications

- Cost increases: Fuel surcharges passed to consumers

- Operational adjustments: Airlines reduce capacity and frequency

Maritime Shipping:

- Container rate escalation: 20-40% increases due to route diversions

- Delivery delays: Extended transit times via alternative routes

- Insurance cost spikes: Risk premiums add substantial operational costs

Ground Transportation:

- Diesel price volatility: Trucking and rail operations face cost uncertainty

- Supply chain delays: Delivery schedules disrupted by fuel cost planning

- Consumer price transmission: Transport costs passed through to final goods

Manufacturing Supply Chain Vulnerabilities

Energy-intensive industries experience cascading disruptions beyond direct fuel costs:

- Petrochemical sector: Feedstock shortages affect plastic and synthetic material production

- Aluminium and steel: Energy costs represent 20-40% of production expenses

- Cement manufacturing: Natural gas disruptions halt production processes

- Agricultural inputs: Fertiliser price increases impact global food production costs

Refined Product Market Dynamics

Refined petroleum products often experience more severe price volatility than crude oil during supply disruptions due to lower inventory levels and reduced refining flexibility.

Diesel Market Stress Indicators

US ultra-low-sulfur diesel futures surged 15% to $3.32 per gallon, reaching two-year highs due to several factors:

- Lower refinery capacity: Global diesel production constraints

- Commercial transportation demand: Limited substitution options for heavy-duty applications

- Inventory limitations: Diesel stocks typically lower than gasoline

- Regional supply imbalances: Refinery shutdowns create geographic shortages

Gasoline and European Products

Gasoline futures increased 6% to $2.50 per gallon, while European gasoil futures gained 16% to $1,025 per metric ton following previous 18% increases. This demonstrates how Middle Eastern refinery disruptions affect global refined product availability regardless of crude oil substitute availability.

Risk Management and Hedging Strategies

Energy companies and large consumers employ multiple financial and operational strategies to manage supply disruption risks during geopolitical crises.

Financial Risk Mitigation

Futures Contract Strategies:

- Fixed price contracts: Lock current prices for future delivery periods

- Volume hedging: Secure specific quantities regardless of spot market availability

- Basis risk management: Hedge price differences between different crude types or delivery locations

Options and Derivatives:

- Call option purchases: Protect against upward price movements while maintaining downside exposure

- Collar strategies: Combine options to create price bands for budget certainty

- Swap agreements: Exchange floating market prices for fixed-rate certainty

Operational Contingency Development

Companies implement multiple operational safeguards:

- Supply diversification: Develop relationships with suppliers across different geographic regions

- Inventory optimisation: Increase strategic stock levels during periods of market stability

- Alternative logistics: Pre-negotiate backup transportation, storage, and processing arrangements

- Flexible supply contracts: Include force majeure and alternative delivery terms

Long-Term Energy Infrastructure Investment Implications

Current supply disruptions may accelerate investment in energy infrastructure designed to reduce vulnerability to geopolitical chokepoints and enhance supply security.

Strategic Reserve Expansion Programs

Countries may extend emergency supply capabilities beyond current standards:

- Current capacity: 90-day strategic reserves standard among developed nations

- Proposed expansion: 120-180 day supply duration targets

- Infrastructure investment: Additional storage terminals and distribution networks

- Coordination mechanisms: Enhanced international reserve sharing agreements

Chokepoint Bypass Infrastructure

Investment priorities may shift toward projects that circumvent critical maritime passages:

- Pipeline capacity expansion: Trans-Arabian and East-West crude systems

- Alternative export terminals: LNG facilities outside Persian Gulf

- Overland transport networks: Rail and pipeline connections to non-maritime routes

- Storage hub development: Strategic positioning outside vulnerable regions

Energy Transition Acceleration

Iran conflict oil supply disruptions provide additional impetus for renewable energy deployment and grid modernisation investments. Countries seeking to reduce import dependencies may accelerate timelines for:

- Solar and wind capacity: Domestic energy production expansion

- Battery storage systems: Grid stability during supply transitions

- Electric vehicle infrastructure: Reduced transportation fuel dependencies

- Green hydrogen development: Industrial process fuel substitution

In addition, energy security transition planning becomes increasingly critical for long-term national security strategies.

Market Psychology and Investor Behaviour

Financial markets demonstrate distinct behavioural patterns during energy supply crises, with risk perception often driving price movements independent of actual supply balance fundamentals.

Volatility Amplification Mechanisms

Several psychological factors amplify market movements:

- Herding behaviour: Traders follow momentum rather than fundamentals

- Loss aversion: Overreaction to potential supply losses versus actual disruptions

- Availability bias: Recent events receive disproportionate weight in decision-making

- Anchoring effects: Previous crisis prices become reference points for current valuations

Long-Term Investment Implications

Institutional investors may reassess energy sector allocation based on:

- Geopolitical risk premiums: Higher required returns for Middle Eastern exposure

- Supply chain diversification: Investment in alternative energy sources and routes

- Strategic asset valuation: Premium pricing for assets outside vulnerable regions

- ESG considerations: Environmental, social, and governance factors in energy transition

Current energy supply disruptions demonstrate the complex interdependencies within global energy systems and highlight the cascading effects that regional conflicts can trigger across worldwide markets. Understanding these vulnerability patterns enables better preparation through diversified supply chains, enhanced strategic reserves, and accelerated investment in energy infrastructure that reduces dependence on geopolitically sensitive chokepoints.

Organisations that develop comprehensive energy security frameworks today will be better positioned to navigate future uncertainties while maintaining operational stability and economic resilience during periods of international tension.

Disclaimer: This analysis contains forward-looking statements and market speculation. Energy markets involve significant volatility and risk. Past performance does not guarantee future results. Readers should conduct independent research and consult qualified professionals before making investment or operational decisions based on geopolitical energy market analysis.

Concerned About Energy Market Volatility's Impact on Your Investments?

Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, including energy and critical mineral opportunities that can benefit from supply chain disruptions and commodity price volatility. Stay ahead of market movements by exploring Discovery Alert's dedicated discoveries page to understand how major mineral discoveries have generated substantial returns during periods of geopolitical uncertainty, then begin your 14-day free trial today.