June 8, 2026

The Energy Market's Most Dangerous Chokepoint Is Now a Battlefield

Global energy markets have weathered price shocks, sanctions regimes, and supply squeezes across decades of Middle Eastern conflict. But the simultaneous closure of the world's most critical oil transit corridor and an active exchange of ballistic missiles between two of the region's most militarily capable states represents a category of risk that most commodity pricing models were never designed to absorb. What is unfolding in mid-2026 is not a geopolitical flare-up that can be modelled through historical precedent alone. It is a structural rupture.

Understanding why Iran launches missiles at Israel on 7 June 2026 requires looking well beyond the immediate exchange. The event reflects the cumulative pressure of months of military escalation, fractured diplomacy, and the most severe disruption to global oil supply chains since the 1973 Arab oil embargo. Furthermore, crude oil price trends in the lead-up to this moment had already signalled mounting stress across commodity markets.

When big ASX news breaks, our subscribers know first

What Triggered the June 2026 Missile Strike?

The Beirut Strike and the Retaliatory Logic

Israel's military carried out strikes on Beirut targeting what it described as Hezbollah command infrastructure. The justification was Hezbollah's sustained campaign of missile and drone attacks against communities in northern Israel. From Iran's perspective, these strikes crossed a threshold that carried an obligation to respond.

Tehran's foreign ministry framed the missile launch on 7 June not only as a reaction to the Beirut strikes, but also as a response to what it characterised as US violations of existing ceasefire understandings, specifically the interdiction of Iran-bound vessels operating near the Strait of Hormuz. This dual framing is significant: it signals that Iran views both the Israeli and American dimensions of the conflict as inseparable, and that its retaliatory calculus incorporates both simultaneously.

Strategic Insight: Iran's Islamic Revolutionary Guard Corps framed the missile launch as a calibrated warning rather than the opening of a full offensive campaign. This distinction matters considerably for how energy markets and diplomatic actors interpret the event. A warning salvo preserves negotiating space; an all-out offensive eliminates it.

The Hezbollah Variable

Hezbollah functions as Iran's primary forward deterrent in the Levant, providing Tehran with the ability to project military pressure against Israel without committing Iranian forces directly. Lebanon's central government holds limited practical authority over Hezbollah, a structural reality that has repeatedly undermined US-facilitated ceasefire efforts. Each Israeli military incursion into Lebanon generates further retaliatory fire from Hezbollah, which in turn generates Israeli responses, perpetuating a cycle with no internal off-ramp.

The civilian cost in Lebanon has been substantial, complicating international diplomatic positioning and reducing the political feasibility of overt support for Israeli military operations in the region. For further context on the October 2024 Iranian strikes on Israel, which set the precedent for this escalatory pattern, the historical record is instructive.

US-Iran Low-Intensity Combat: Ten Days of Escalation

In the ten days preceding the missile strike, US and Iranian forces had been engaged in repeated military exchanges. American forces targeted Iranian military infrastructure operating near the Strait of Hormuz, while Iran responded with missile and drone attacks against US installations in Kuwait and Bahrain. This layer of direct US-Iranian military contact added significant pressure to an already volatile situation, and Iran explicitly cited these exchanges as part of its justification for the 7 June missile attack on Israel.

Trump's Response and the Nuclear Deal Timeline

Washington Distances Itself from Beirut

President Trump's public response to the escalation broke from conventional US-Israeli alignment optics in notable ways. He stated publicly that the Israeli strikes on Beirut had not been coordinated with Washington, describing his reaction to those strikes as one of dissatisfaction. This was not a formulaic expression of concern; it represented a deliberate effort to separate American diplomatic positioning from Israeli military decisions at a moment when Washington was actively pursuing a deal with Tehran.

Trump's message to Iran following the missile strike was equally direct in tone: he urged Tehran to consider the salvo a sufficient expression of its grievances and return to the negotiating table. The framing treated the missile exchange as a disruption to ongoing diplomacy rather than a justification for American military retaliation.

How Close Was a Deal?

Trump had been characterising a US-Iran peace framework as effectively finalised since 22 May 2026. His account suggested a formal signing was anticipated within days before the Beirut strike and subsequent Iranian missile attack disrupted the process. The core obstacles preventing agreement closure remain substantial:

| Negotiation Obstacle | Iran's Position | US/Israel Position |

|---|---|---|

| Strait of Hormuz navigation | Sovereign oversight via PGSA permit system | Unconditional freedom of navigation |

| Nuclear enrichment | Retention of civilian enrichment capacity | Significant rollback of enrichment infrastructure |

| Israeli operations in Lebanon | Complete cessation as precondition | Conditional on Hezbollah disarmament |

These are not minor technical disagreements. Each item touches on core national security interests, and movement on any one requires political concessions that carry significant domestic costs for all parties involved.

The Strait of Hormuz: What a Closure Actually Means

Why This Waterway Cannot Be Replicated

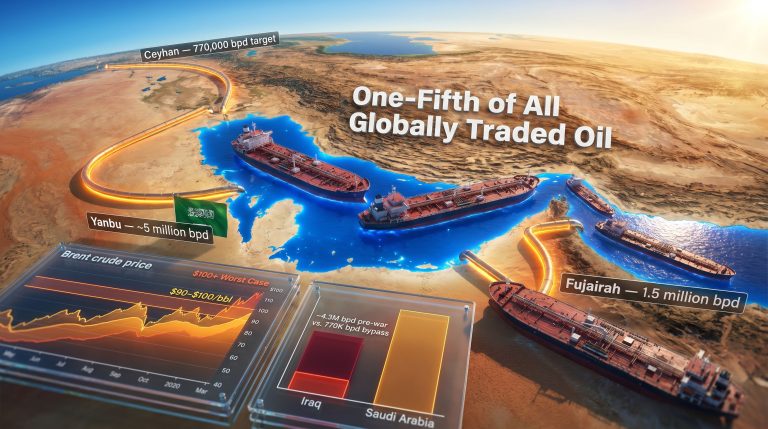

Under normal operating conditions, approximately 20% of global petroleum liquids transit the Strait of Hormuz, a narrow passage between Iran and Oman that serves as the only maritime exit route for crude oil and LNG exports from the Persian Gulf. There is no viable alternative at comparable scale. The Cape of Good Hope rerouting adds thousands of nautical miles to voyage times, dramatically increasing freight costs and delivery windows in ways that compound supply deficits rather than offset them.

Iran's de-facto closure of the strait since late February 2026 has already produced the largest single supply disruption in global energy markets in decades. The Persian Gulf Strait Authority (PGSA), formally launched on 5 May 2026, became Tehran's institutional mechanism for asserting transit control through a permit system.

PGSA Operations: Scale and Composition

Between late April and late May 2026, more than 300 non-Iranian vessels contacted the PGSA seeking safe passage permits. The breakdown of applicants reveals the breadth of commercial activity being filtered through this system:

| Vessel Type | Share of Applications |

|---|---|

| Oil tankers | 42% |

| Bulk carriers | 27% |

| Container ships | 11% |

| LNG carriers | 8% |

| Other vessel types | 12% |

Of the vessels seeking to transit, 77% were attempting to exit the Mideast Gulf rather than enter it, illustrating the severe export constraint bearing down on producing nations. Destination analysis of outbound vessels shows that 28% were bound for China, 19% for India, and 23% for other Asian ports, making Asia's exposure to the Hormuz disruption disproportionate relative to other importing regions.

Risk Indicator: The US Treasury's Office of Foreign Assets Control (OFAC) sanctioned the PGSA, warning that any shipping operator engaging with the authority risks exposure to IRGC-related secondary sanctions. Following that designation, daily vessel transits through the strait fell from approximately seven per day to just over three per day. The sanctions have effectively halved commercial shipping activity through the world's most critical oil transit corridor.

OPEC+ in a War Zone: Targets vs. Reality

The Growing Gap Between Policy and Output

On 7 June, the seven core OPEC+ members, comprising Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman, agreed to a 188,000 b/d production target increase for July 2026. This marked the fourth consecutive monthly increase since the US-Iran war began on 28 February 2026. The target increases are part of a broader process to unwind 1.65 million b/d of production cuts that were originally agreed in April 2023.

However, these target increases are entirely theoretical for the Hormuz-dependent members of the group. No meaningful output increase can be exported until the strait reopens for unimpeded commercial navigation. In this context, OPEC's market influence over global pricing dynamics has rarely been so constrained by external military factors.

Total OPEC+ production in May 2026 reached 29.53 million b/d, representing a 9.6 million b/d decline from pre-war output levels. The scale of suppression across the most affected members is illustrated below:

| Country | May 2026 Output (mn b/d) | Pre-War Capacity (mn b/d) | Output Gap |

|---|---|---|---|

| Saudi Arabia | 6.57 | 10.478 | -3.91 |

| Iraq | 1.55 | 4.431 | -2.88 |

| Kuwait | 0.58 | 2.676 | -2.10 |

| Iran | 2.65 | ~3.50 (est.) | ~-0.85 |

| Bahrain | 0.03 | 0.20 | -0.17 |

The three most affected Hormuz-dependent OPEC members were running collectively approximately 8.5 million b/d below their cumulative targets in May alone. Saudi Arabia's notable month-on-month output increase of 250,000 b/d in May was driven primarily by domestic power generation requirements rather than export growth, limiting its contribution to global supply.

Iran's Accelerating Output Decline

Iran's production situation is deteriorating in a particularly acute way. Output fell by 300,000 b/d in May to 2.65 million b/d as the US port blockade intensified and Iranian onshore storage capacity approached saturation. When a producing nation's storage fills and export routes are blocked simultaneously, production shutdowns become operationally unavoidable regardless of target-setting decisions made in ministerial meetings. Iran is approaching that threshold. Consequently, OPEC demand revisions for the remainder of 2026 are expected to reflect this deepening shortfall.

The UAE's Exit and Its Structural Impact

The UAE formally departed both OPEC and OPEC+ effective 1 May 2026, reducing the core group's monthly unwind capacity from 206,000 b/d to 188,000 b/d per month. Approximately 564,000 b/d of cuts remain to be unwound as of June 2026. At the current pace, September 2026 represents the projected timeline for full unwind completion, contingent entirely on the strait reopening.

An important internal understanding among OPEC+ members is that no nation will operate above full capacity or exceed its target to compensate for lost output during the conflict period. This represents a form of collective discipline that prevents the group from undermining its own pricing architecture during an already supply-constrained environment.

Kazakhstan's Contrarian Output

One outlier in the production data is Kazakhstan, which produced 1.86 million b/d in May against a target of 1.59 million b/d, exceeding its allocation by 270,000 b/d. This overproduction is one of the few instances of a member actively benefiting from the current supply void, though it represents a fraction of the deficit created by Gulf member shutdowns.

Three Scenarios for What Happens Next

Scenario 1: Diplomatic Re-Engagement and Partial Strait Reopening

If back-channel communication between Washington and Tehran resumes productively, and Iran treats the 7 June missile exchange as having fulfilled its retaliatory obligation, a partial pathway to de-escalation opens. For this scenario to materialise, Israel would need to suspend Lebanon military operations, and Iran would need to stand down further missile activity. A partial reopening of the strait under these conditions could release 4 to 6 million b/d of suppressed Mideast Gulf output within 60 to 90 days.

Scenario 2: Managed Disruption Without Full Escalation

Neither side moves to full-scale confrontation. The PGSA permit system continues operating at reduced capacity under OFAC sanction pressure. US-Iran diplomatic talks stall but do not collapse entirely. This scenario implies chronic supply suppression continuing through Q3 2026, structurally elevated crude prices, and accelerated diversification efforts by Asian importers toward West African, North American, and Russian supply.

Scenario 3: Full Escalation

A second, larger Iranian missile salvo, or an Israeli or American strike on Iranian oil infrastructure or nuclear facilities, triggers near-total Hormuz closure and potential removal of Iran's remaining 2.65 million b/d of export capacity from global markets. This scenario would represent a price shock without historical parallel in the modern crude market.

Strategic Risk Assessment: The June 2026 missile exchange most closely resembles Scenario 2 in its immediate aftermath. Iran's calibrated framing and Trump's preference for a negotiated outcome both suggest the parties retain awareness of the costs of full escalation. However, the proximity of all three scenarios to one another represents the highest geopolitical risk premium embedded in global energy markets since at least 2022.

The next major ASX story will hit our subscribers first

The US-China Trade Dimension and Its Energy Implications

The Hormuz crisis has introduced an unexpected dynamic into the US-China trade relationship. Following the Trump-Xi Beijing summit, both governments committed to establishing a joint Board of Trade framework targeting approximately $30 billion in bilateral tariff reductions across priority product categories, with US crude and LNG explicitly identified as candidates. The broader trade war oil impact on global supply chains has made this diplomatic opening considerably more consequential than it might otherwise have been.

China had imposed a 20% surcharge on US crude in 2025, layered on top of an existing 2.5% tariff, effectively pricing American barrels out of the Chinese import market. With Persian Gulf supply now severely constrained, Chinese buyers face a structural incentive to reconsider alternative sourcing. The US-China trade war dynamic, in this sense, is being reshaped in real time by the Hormuz closure, as market forces override some of the tariff-driven separation that defined bilateral energy trade through 2025.

If tariff reductions on US crude proceed through the Board of Trade mechanism, the Hormuz crisis paradoxically creates a commercial opening for American exporters to re-enter one of the world's largest crude import markets. Whether Chinese buyers will act on this incentive before a political resolution materialises remains one of the more consequential unanswered questions in global commodity markets.

Frequently Asked Questions

When did Iran launch missiles at Israel in 2026?

Iran's armed forces launched ballistic missiles targeting northern Israel on Sunday, 7 June 2026. This was the first direct instance of Iran launching missiles at Israel since April 2026.

Were there confirmed casualties from the missile attack?

At the time of initial reporting, Israel's Defense Forces confirmed active interception operations were underway. No confirmed casualty figures were available in the immediate aftermath of the strike.

Why did Iran attack Israel with ballistic missiles in June 2026?

Iran stated the attack was a retaliatory response to Israeli strikes on Beirut targeting Hezbollah infrastructure, and also cited what Tehran characterised as US violations of ceasefire terms, including the interdiction of Iran-bound vessels.

How does the escalation affect crude oil supply?

The attack compounds an already severe supply disruption caused by the effective closure of the Strait of Hormuz since late February 2026. OPEC+ production is running approximately 9.6 million b/d below pre-war levels, and further escalation risks deepening that deficit.

Is a US-Iran nuclear deal still possible?

The Trump administration has continued to publicly advocate for a negotiated resolution. The three primary structural obstacles remain: Hormuz navigation rights, Iran's nuclear enrichment programme, and the cessation of Israeli military operations in Lebanon. A deal remains within the realm of possibility but faces significant political and logistical barriers.

The Minimum Conditions for Strait Reopening

Restoring normal commercial transit through the Strait of Hormuz would require the alignment of multiple diplomatic and security conditions simultaneously. Any credible resolution framework would need to address the following in sequence:

- A formal US-Iran ceasefire agreement with verifiable compliance mechanisms in place.

- Israeli suspension of Lebanon military operations, removing Iran's stated precondition for standing down.

- Hezbollah cessation of cross-border attacks on northern Israel.

- Dismantling or formal suspension of the PGSA permit system.

- Lifting of OFAC sanctions against PGSA-affiliated entities to restore commercial confidence in strait transits.

Each of these conditions carries its own political complexity, and none can be resolved unilaterally. The interdependency of the list is itself a measure of how deeply entangled the military, diplomatic, and economic dimensions of this crisis have become.

The broader question for commodity markets is how long non-Hormuz producers can absorb the structural demand shift being directed toward their supply. US shale, West African producers, and non-sanctioned Russian volumes are all operating under increased pressure to fill a gap that, at its current magnitude, cannot be fully offset from outside the Persian Gulf.

Readers seeking ongoing commodity market analysis covering crude oil supply dynamics, Strait of Hormuz developments, and OPEC+ production data can access regularly updated market intelligence through Argus Media's latest market news portal.

This article contains forward-looking analysis and scenario projections based on available information as of the date of publication. Geopolitical developments are inherently uncertain, and actual outcomes may differ materially from scenarios described. Nothing in this article constitutes financial or investment advice.

Want to Capitalise on Commodity Market Shifts Driven by Major Geopolitical Events?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data into actionable investment insights — explore historic discoveries and their market returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.