June 8, 2026

The 100-Day Deadlock: What the U.S.-Iran Standoff Reveals About Modern Energy Geopolitics

When diplomatic frameworks between major powers fracture, they rarely collapse all at once. They erode gradually, through competing demands, hardening domestic political positions, and the slow accumulation of tactical incidents that make compromise structurally harder with each passing week. The U.S.-Iran conflict, now past its 100-day mark with no meaningful breakthrough in sight, is following exactly this pattern, and the consequences for global energy markets are growing more difficult to ignore.

Understanding why the U.S. and Iran peace deal talks remain deadlocked requires moving beyond the surface narrative of political disagreement. The real architecture of this standoff involves layered disputes, each with its own internal logic, each reinforcing the others, and none of them amenable to quick resolution. Furthermore, these dynamics are reshaping how analysts assess oil market geopolitical dynamics across the broader region.

When big ASX news breaks, our subscribers know first

A Conflict Built on Compounding Fault Lines

Hostilities formally began on February 28, and by early April a ceasefire framework had taken shape, though its fragility was evident almost immediately. Rather than serving as a foundation for broader negotiation, the ceasefire became a ceiling, limiting escalation without creating the conditions for genuine diplomatic progress.

By the 100-day milestone reached in early June 2026, formal negotiation structures were functionally absent. Communication between Washington and Tehran was continuing through intermediary channels, with Pakistan playing a notable backchannel role, but the distance between the two parties on core issues had not meaningfully narrowed.

Iranian officials described the state of U.S. and Iran peace deal talks in terms that left little room for optimism, characterising progress as essentially nonexistent. The U.S. side, for its part, had not publicly confirmed any active negotiation framework, reflecting both strategic calculation and the domestic political cost of being seen to engage with Tehran directly.

In international relations, a declared deadlock is rarely the full picture. The persistence of intermediary contacts, even without formal talks, signals that both parties are preserving future optionality rather than definitively closing diplomatic channels.

The Four Pillars of Disagreement Blocking a Deal

Nuclear Enrichment: The Foundational Obstacle

No issue sits closer to the centre of the U.S.-Iran impasse than Iran's nuclear programme. The 2015 Joint Comprehensive Plan of Action (JCPOA) capped Iranian uranium enrichment at 3.67% and established International Atomic Energy Agency (IAEA) inspection access as a verification mechanism. The U.S. withdrawal from that agreement in 2018 and subsequent Iranian enrichment escalation, with Iran enriching uranium to 60% purity by 2023 according to IAEA reporting, means the starting point for any new framework is dramatically further apart than it was a decade ago.

The current U.S. position demands near-zero enrichment levels, a threshold Iran has consistently rejected on sovereign rights grounds. Tehran frames its enrichment programme as a matter of national autonomy rather than a negotiating variable, making this the hardest obstacle to bridge.

| Issue | JCPOA (2015) Framework | Current U.S. Position | Iran's Current Demand |

|---|---|---|---|

| Uranium Enrichment Cap | 3.67% | Near-zero enrichment | Retain enrichment rights |

| Sanctions Relief | Phased removal | No relief without full compliance | Immediate asset unfreezing |

| Verification Regime | IAEA inspections | Enhanced monitoring | Conditional access only |

| Regional Security | Not included | Linked to Hezbollah activity | Must be addressed jointly |

Frozen Assets and the Sanctions Architecture

President Trump has stated publicly that he will not agree to unfreeze Iranian assets or ease sanctions as part of any initial agreement. Iran's position is the direct inverse: the release of frozen assets must come first, before any broader arrangement is possible.

This sequencing dispute is not merely procedural. Billions of dollars in frozen Iranian funds represent both an economic lifeline and a matter of political symbolism for the Iranian government. Granting sanctions relief before receiving verifiable commitments would be politically toxic for the Trump administration domestically. Accepting sanctions as a precondition for compliance would be equally unacceptable in Tehran.

The result is a financial fault line that has paralysed interim deal prospects. Neither side has found a sequencing formula that both governments can defend to their own domestic audiences.

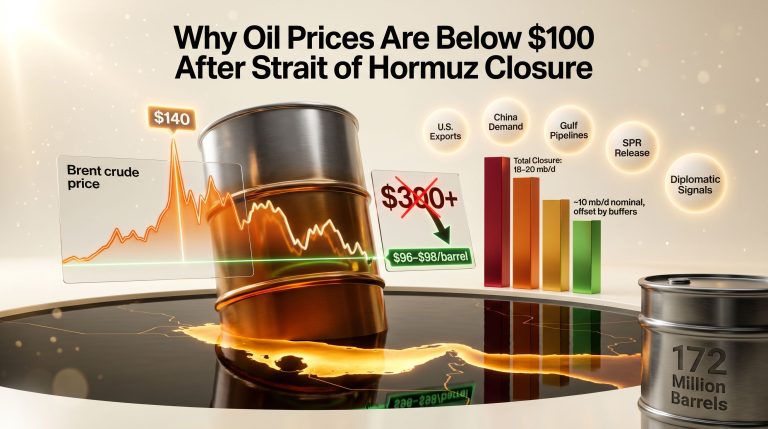

The Strait of Hormuz: Geography as Leverage

Under normal conditions, the Strait of Hormuz handles a substantial share of the world's seaborne crude oil and LNG exports. The precise figure varies by source and year, but the U.S. Energy Information Administration has historically cited approximately 20% of global petroleum liquids transiting the strait annually, making it the single most critical maritime energy chokepoint on the planet.

Since February 28, traffic through the waterway has remained materially below pre-conflict levels. U.S. Central Command has reported intercepting Iranian drones threatening commercial shipping in the strait, and missile and drone incidents across the broader Gulf region have sustained elevated war-risk insurance premiums for vessels operating in the area.

Iran's ability to threaten or restrict Hormuz access gives it leverage that does not depend on nuclear capability. It is an immediately deployable economic instrument, which is precisely why any interim agreement that fails to address strait navigation rights explicitly would be structurally incomplete. Consequently, this reality has contributed directly to the oil price shock reverberating across energy-producing nations.

Regional Security Linkage: The Hezbollah Complication

Tehran has consistently argued that any durable resolution must account for the broader regional conflict architecture, including the situation in Lebanon and the role of Hezbollah. The U.S. position has similarly sought to link nuclear and regional security issues, though from the opposite direction, demanding that Iran's support for proxy networks be curtailed as part of any deal.

This mutual linkage strategy, while logical from each party's perspective, dramatically expands the scope of what a deal must accomplish. Rather than narrowing the negotiating agenda, both sides have widened it, making a comprehensive agreement even less accessible in the near term.

How Energy Markets Are Processing the Deadlock

As of early June 2026, WTI crude is trading above $90 per barrel and Brent crude has settled near $93 per barrel. These figures represent a partial retreat from the sharp spikes recorded in the early weeks of the conflict, but they remain significantly elevated relative to pre-war benchmarks.

What market pricing at these levels actually signals is worth unpacking. A return to pre-conflict price ranges would require markets to price in a rapid resolution. The fact that prices have stabilised at elevated levels rather than collapsing back toward the mid-$70s range suggests that traders and institutions have effectively concluded that the conflict will persist for an extended period without either full escalation or comprehensive resolution.

The scenario table below illustrates how different diplomatic outcomes translate into energy market implications:

| Scenario | Estimated Oil Price Range | Global GDP Impact | Duration Risk |

|---|---|---|---|

| Current Partial Disruption | $88-$95/bbl | Moderate inflationary drag | Ongoing |

| Negotiated Partial Reopening | $75-$82/bbl | Stabilising effect | 3-6 months |

| Full Hormuz Closure (escalation) | $120-$150/bbl | Severe global recession risk | Unpredictable |

| Comprehensive Peace Agreement | $65-$72/bbl | Deflationary relief | Long-term |

LNG Market Vulnerabilities

Qatar's LNG export infrastructure relies heavily on Hormuz access, and the ripple effects of reduced traffic through the strait extend far beyond crude oil. Asian buyers, particularly Japan, South Korea, and China, are among the most exposed to supply security disruption given their dependence on Gulf LNG imports. The LNG supply outlook for the region has consequently become a focal point for procurement planners across Asia.

European buyers, already accelerating LNG import diversification following the 2022 Russian gas disruption, are now reassessing long-term contract structures in light of Hormuz vulnerability. The dual experience of Russian supply disruption and Gulf instability within a four-year window is fundamentally reshaping how energy-importing nations think about supply chain architecture and the risk premium embedded in single-corridor dependency.

Infrastructure Damage and Investment Deterrence

Since the conflict began, Iranian-allied forces have launched attacks targeting oil infrastructure, industrial facilities, and military installations across multiple Gulf states. The cumulative effect of this damage extends beyond immediate production losses. War-risk insurance premiums for Gulf-region energy projects have escalated sharply, and upstream investment decisions for new Gulf development are being reconsidered in light of sustained security uncertainty.

This investment deterrence dynamic is one of the less-discussed consequences of prolonged Gulf instability. The damage is not only physical and immediate. It erodes the long-term capital formation that underpins future production capacity across one of the world's most productive hydrocarbon basins. In addition, oil markets under pressure from multiple directions are making investment decisions increasingly complex for producers and buyers alike.

The Role of Indirect Diplomacy in a Functional Deadlock

Pakistan's positioning as a diplomatic intermediary between Washington and Tehran reflects a structural reality of U.S.-Iran relations: direct, official engagement carries prohibitive political costs for both governments. Third-party mediation allows message testing and signal exchange without the domestic political exposure of formal talks.

This approach has historical precedent. Switzerland has served as the U.S. protecting power in Iran since 1980, facilitating consular and diplomatic communications in the absence of formal relations. The use of multiple intermediaries simultaneously, however, introduces risks of message distortion and misinterpretation that can compound rather than reduce miscalculation risk. Al Jazeera's reporting on the Pakistan marathon talks illustrates precisely how challenging even facilitated dialogue can be when core positions remain immovable.

The public posturing from both governments, hardline statements from Tehran paired with Trump administration rhetoric rejecting preconditions, masks what is almost certainly a more nuanced private exchange. This dual-track dynamic is standard diplomatic practice, but it makes external assessment of actual progress extremely difficult.

Six-to-Twelve Month Outlook: Four Scenarios Worth Monitoring

-

Fragile Interim Agreement: A limited deal addressing partial Hormuz reopening and a nuclear enrichment freeze in exchange for modest sanctions adjustments. This scenario would require significant domestic political management from both sides and remains challenging but not impossible if economic pressure on Iran intensifies.

-

Prolonged Stalemate: The most probable near-term trajectory. Sustained elevated oil prices, continued shipping disruptions, and incremental military incidents without full escalation characterise this scenario. The humanitarian and infrastructure costs accumulate steadily without triggering a decisive political response.

-

Escalation Beyond Current Parameters: A major infrastructure strike, a Hormuz closure event, or a ceasefire breakdown could push oil prices into the $120-$150/bbl range with cascading effects on global inflation, central bank policy, and allied security commitments.

-

Comprehensive Diplomatic Breakthrough: Historically unprecedented in the bilateral context without a multilateral framework. Would require simultaneous resolution of nuclear, sanctions, Hormuz, and regional security issues. Long-term normalisation of Gulf energy flows and significant oil price relief would follow, but the structural preconditions for this outcome are not currently present.

The next major ASX story will hit our subscribers first

What the Geopolitical Periphery Tells Us

China and Russia both provide Iran with meaningful economic and diplomatic insulation, limiting the effectiveness of Western sanctions pressure. China's continued purchase of Iranian crude at discounted rates reduces Tehran's economic pain below what a fully enforced sanctions regime would produce. Russia's diplomatic alignment at the UN Security Council provides Iran with veto protection against multilateral intervention.

This external support architecture means that economic pressure alone is unlikely to force Iran into concessions it views as structurally unacceptable. Any pathway to a durable resolution must account for this geopolitical reality, which further complicates the broader geopolitical risk landscape for commodities and capital markets globally.

For energy markets, the clearest near-term signal to monitor is the status of Hormuz navigation. A partial reopening of the strait, even without a comprehensive peace agreement, would represent the single most actionable lever for delivering immediate oil price relief and restoring some degree of shipping confidence across the Gulf corridor.

Until that variable shifts materially, the market's working assumption remains what 100 days of deadlock has already demonstrated: the U.S. and Iran peace deal talks are neither ending quickly nor escalating catastrophically, and the elevated price environment that reflects that expectation is likely to persist.

Disclaimer: This article contains forward-looking analysis and scenario projections based on publicly available information as of June 2026. Energy price ranges and geopolitical outcome scenarios are illustrative and do not constitute investment or trading advice. Actual outcomes may differ materially from projections presented here.

Want to Stay Ahead of the Market Opportunities Emerging From Global Energy Disruption?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across oil, gas, and 30-plus commodities — turning complex market signals into actionable investment insights at a time when geopolitical disruption is reshaping global energy flows. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial to position yourself ahead of the broader market.