June 11, 2026

The Geography of Systemic Fragility: Understanding the Hormuz Chokepoint

Energy markets have long operated on the assumption that the global oil supply chain, however complex, retains enough redundancy to absorb regional shocks. That assumption is being tested in real time. The Iran oil exports blockade in the Strait of Hormuz has always represented the single most consequential vulnerability in the world's energy infrastructure, but it took a full naval blockade beginning April 13, 2026, to expose just how fragile that assumption truly was.

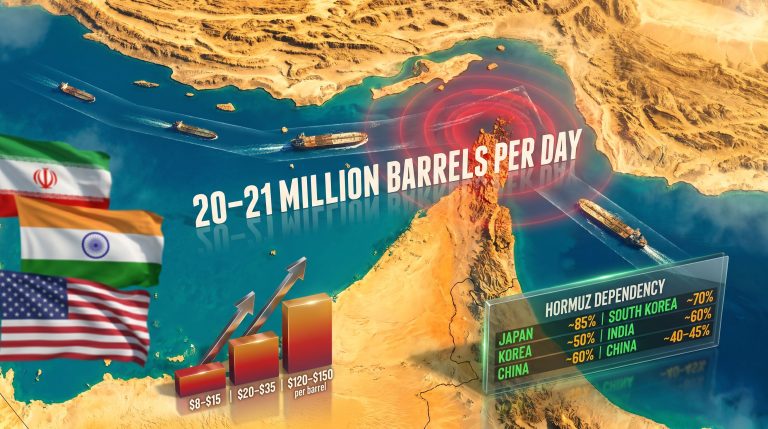

The Strait connects the Persian Gulf to the Gulf of Oman, forming a maritime corridor through which roughly 20% of the world's daily traded oil flows. At its narrowest navigable point, the passage measures approximately 33 kilometres across, yet the actual shipping lanes are far more constrained. The nations most exposed to a prolonged closure read like a who's who of the world's largest energy consumers: China, India, Japan, South Korea, and several major European economies all depend on Persian Gulf crude moving freely through these waters.

What distinguishes the current crisis from previous episodes of regional tension is the mechanism of enforcement. Financial sanctions, however severe, operate at the level of transactions, correspondent banking, and insurance markets. They create friction, but determined state actors with established trading networks can often find workarounds. A physical naval blockade intercepts cargo at sea, stopping vessels from loading, transiting, or discharging. The distinction is operationally profound, and it is one that Iran's energy sector had never been forced to confront before April 2026.

The blockade's collateral effects extend well beyond Iran's own export volumes. Saudi Arabia, the UAE, Kuwait, and Iraq have all experienced curtailed export flows as the enforcement zone disrupts broader Persian Gulf shipping corridors, effectively transforming what began as an Iran-specific pressure campaign into a structural shock affecting the entire region's oil supply architecture. Furthermore, the geopolitical trade tensions underpinning this crisis have been building for years, making the current standoff a culmination rather than a sudden rupture.

When big ASX news breaks, our subscribers know first

From Export Powerhouse to Stranded Barrels: Quantifying the Collapse

The speed and severity of the export volume collapse following April 13 has few modern parallels. Prior to the blockade's imposition, Iran was producing approximately 3.2 million barrels per day in March 2026, with export volumes holding near pre-conflict levels, according to Bloomberg data compiled from ship-tracking information and industry consultant estimates.

Within days of enforcement beginning, that picture changed dramatically.

| Metric | Pre-Blockade (March 2026) | Post-Blockade (April 13-25, 2026) |

|---|---|---|

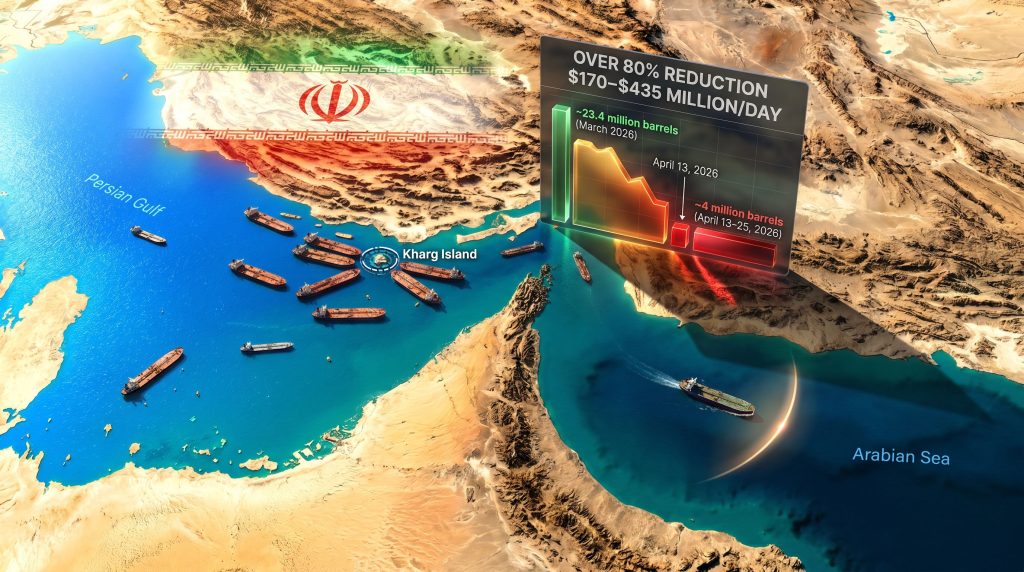

| Monthly export volume | ~23.4 million barrels | ~4 million barrels (Gulf of Oman exits) |

| Export volume decline | Baseline | Over 80% reduction |

| Iranian crude tanker exits | Active and regular | Effectively zero observed |

| Tankers with Iranian oil history in Gulf | Distributed | 18 vessels, up to 35M bbl capacity (Kpler) |

| Floating storage available | ~65-75 million barrels (Vortexa) | Increasingly occupied |

| Daily revenue loss | Baseline | ~$170M/day (US Treasury) |

Sources: Bloomberg ship-tracking data, Kpler, Vortexa, U.S. Treasury Secretary Scott Bessent via X, May 2026

Kharg Island sits at the epicentre of this crisis. The island's terminal complex handles the overwhelming majority of Iran's crude export capacity, making it the single most critical node in the country's energy infrastructure. Satellite imagery has confirmed a growing cluster of tankers anchored offshore, many of them ageing vessels repurposed as floating buffer storage rather than active carriers.

U.S. Treasury Secretary Scott Bessent publicly stated in early May 2026 that Kharg Island was approaching capacity, citing $170 million per day in lost revenue as a lever toward bringing Tehran to the negotiating table. Analysts at both JPMorgan Chase and energy intelligence firm Kpler reached broadly similar conclusions, estimating that Iran had a window of approximately one month from early May 2026 before onshore storage reached exhaustion at then-current production levels.

Antoine Halff, co-founder and chief analyst at data and research firm Kayrros, observed during a conference call that there had been a significant slowdown in production activity and that the system was showing visible signs of stress. His assessment aligned with satellite data reviewed by Bloomberg showing fewer vessel loadings in recent days, though maritime data of this nature often carries interpretation challenges and reporting delays.

The Floating Storage Dilemma

Iran's access to 65 to 75 million barrels of floating storage capacity, according to Vortexa, including vessels operating as so-called dark tankers within the Gulf under restricted tracking conditions, provides a temporary buffer rather than a structural solution. Vessels used as floating storage must eventually cycle back to reload or discharge cargo. As enforcement tightens, that cycling capacity becomes progressively harder to execute.

According to Kpler data, at least 18 tankers with documented histories of loading Iranian crude were identified operating in the Persian Gulf and Gulf of Oman during the week following the blockade's intensification, with collective capacity to hold up to 35 million barrels of crude. Vessels were observed continuing to load as late as the first weekend of May, though at a notably reduced rate compared to pre-blockade activity.

Iran's Strategic Playbook: Four Decades of Adaptation as Operational Capital

What distinguishes Iran's position from that of most nations facing economic siege warfare is the depth of its institutional knowledge about operating under precisely these conditions. Tehran's oil sector has been disrupted, constrained, and partially dismantled multiple times across the past four decades, and each cycle produced hard-won operational expertise.

The key historical inflection points include:

-

The Iran-Iraq War (1980-1988): Systematic infrastructure damage forced Iranian petroleum engineers to develop techniques for managing production under conflict conditions and preserving reservoir integrity during extended disruption periods.

-

Post-revolutionary sanctions from 1979 onwards: Decades of restricted access to Western oil field technology pushed the National Iranian Oil Company to develop indigenous reservoir management capabilities and workaround engineering practices.

-

UN and multilateral sanctions (2006-2015): Export volume reductions during this period forced refinement of buyer-relationship maintenance strategies, including maintaining indirect contact with customers who were legally prevented from responding.

-

The first Trump administration (2018-2021): The U.S. withdrawal from the JCPOA and maximum pressure sanctions campaign compressed Iranian exports significantly, but critically, the country was still operating within a financial sanctions framework rather than a physical interdiction regime. The impact of sanctions and oil trading networks during this era offers instructive parallels. As Miad Maleki, a former official at the U.S. Treasury's Office of Foreign Assets Control who now serves as a senior fellow at the Foundation for Defense of Democracies, observed, Iran had never been forced to confront what a genuine forced well shut-in actually looks like. That institutional gap is precisely what the current blockade is designed to exploit.

The Erickson Principle: Brett Erickson, Managing Principal at Obsidian Risk Advisors, has articulated the core strategic miscalculation risk for Washington. His analysis suggests that U.S. policy is operating on a static assumption that Iran will absorb economic pressure along a predictable deterioration curve toward collapse. That framework, he argues, fundamentally misreads how states functioning under sustained economic warfare actually behave. They do not collapse on schedule. They adapt.

Proactive Curtailment: The Engineering Logic

Perhaps the most technically significant aspect of Iran's current response is the decision to proactively reduce output rather than wait for storage capacity to force emergency shut-ins. A senior Iranian official confirmed to Bloomberg that production curtailment had already begun as of early May 2026, though the precise magnitude of reductions was not specified. The controlled reduction is estimated to potentially affect up to 30% of Iran's oil reservoirs, according to the same official.

The distinction between a managed curtailment and a forced shut-in is not merely semantic. It reflects a core principle of petroleum reservoir engineering:

-

Managed reduction: Pressure is reduced gradually and in a controlled manner, preserving formation integrity and allowing rapid restart when market conditions change.

-

Forced shut-in: Sudden cessation of production due to storage overflow can cause reservoir pressure imbalances, formation damage, and in some cases permanent loss of recoverable reserves.

Hamid Hosseini, spokesman for the Iranian Oil, Gas and Petrochemical Products Exporters' Association, captured Iran's confidence in this approach plainly, stating that the country's petroleum engineers understand which wells can be idled without causing damage and how to restart them quickly. This operational knowledge, he emphasised, was acquired through exactly the kind of pressure cycles Iran has endured across decades of conflict and sanctions.

It is worth noting an apparent internal messaging inconsistency: while the unnamed senior official confirmed curtailments had begun, Hosseini himself publicly disputed that production had been reduced when speaking earlier in the same week. This divergence suggests Tehran is managing both domestic and international narratives about the severity of its production response simultaneously.

The Shadow Fleet Problem: Why 2026 Is Structurally Different

A critical and underappreciated distinction separates the current blockade from the 2018-2021 sanctions period in ways that fundamentally alter Iran's tactical options.

| Factor | 2018-2021 Sanctions Period | 2026 Naval Blockade |

|---|---|---|

| Enforcement mechanism | Financial sanctions, secondary sanctions | Physical naval interdiction |

| Shadow fleet effectiveness | High, tankers rerouted freely | Severely constrained by physical presence |

| Chinese buyer access | Maintained via indirect routing | Disrupted at point of loading |

| Floating storage flexibility | Broad, multiple ports accessible | Narrowed, Gulf ports under surveillance |

| Enforcement gaps | Significant and exploitable | Present but progressively narrowing |

| AIS manipulation utility | High | Reduced by satellite monitoring |

Under the prior sanctions regime, Iran operated a sophisticated network of tankers owned by obscure entities beyond international oversight, commonly referred to as the shadow fleet. These vessels moved crude to Chinese buyers through indirect routes without attracting the enforcement actions that conventional carriers would face. That option has been materially constrained by the physical presence of U.S. naval forces controlling the waters through which those tankers must pass to load.

Claire Jungman, Director of Maritime Risk and Intelligence at Vortexa, characterises the current situation not as a total disruption but as a constrained and still partially functioning system. Iran retains several operational levers: floating storage cycling, ship-to-ship transfers at sea to obscure cargo origin, AIS transponder deactivation to evade vessel tracking, and the exploration of overland export corridors. The critical variable, she notes, is whether vessels can continue to cycle back into the Gulf to reload, and that window is narrowing as enforcement tightens.

Has Any Iranian Oil Escaped the Blockade?

Enforcement of the blockade is intensive but not absolute. Documented cases of successful cargo transit demonstrate that the system retains gaps, even if those gaps are insufficient to materially offset the overall export volume collapse.

Maritime intelligence platform TankerTrackers.com identified one notable evasion case involving a Very Large Crude Carrier carrying approximately 1.9 million barrels of Iranian crude, valued at roughly $220 million, which successfully reached Asia-Pacific markets by routing through Sri Lanka and the Lombok Strait, the navigable passage between the Indonesian islands of Bali and Lombok. This route circumvents the primary enforcement zone around the Strait of Hormuz entirely, exploiting geographic gaps in interdiction coverage.

Iranian officials have cited such cases in their counter-narrative to U.S. assertions of total interdiction success, using individual transits as evidence that the blockade has not achieved complete closure.

Analytical Perspective: Single-vessel evasion events are financially significant in isolation but statistically immaterial against an export volume decline exceeding 80%. They are more relevant as intelligence about enforcement architecture gaps than as economic relief for Tehran. Their significance lies in demonstrating that alternative routing remains physically possible, which has strategic value for Iran's longer-term negotiating posture.

Iran is simultaneously exploring overland export alternatives. Hosseini confirmed that pipeline and road transport corridors to Turkey, Pakistan, Afghanistan, and Uzbekistan have been identified, with combined capacity estimated at 250,000 to 300,000 barrels per day. While meaningful as a partial offset, this represents less than 10% of pre-blockade export volumes.

Rail transport to China via a Tehran-to-Yiwu/Xi'an corridor also offers an alternative, with faster transit times than sea routes. However, the economics are unfavourable. Chinese teapot refineries, the independent operators that represent the primary market for discounted Iranian crude, operate on narrow margins and depend on pricing advantages that higher-cost overland and rail routes erode substantially. The U.S. Treasury's decision to sanction dozens of individuals linked to Iran's shadow banking network in early May 2026, explicitly targeting teapot refinery operators, compounds this pressure by restricting the financial infrastructure through which these transactions are processed.

Global Oil Market Consequences: The Blockade's Unintended Price Tag

The Iran oil exports blockade in the Strait of Hormuz has generated a market consequence that cuts directly against Washington's domestic political interests. Global oil prices reached a four-year high in the week following the blockade's intensification, a development that creates economic friction not only for U.S. consumers but for allied economies dependent on affordable energy inputs. Indeed, the oil price shock reverberating from this standoff is being felt well beyond the immediate region.

The price signal reflects two compounding supply effects:

-

The direct reduction of Iranian crude from global markets (pre-blockade production was approximately 3.2 million barrels per day)

-

The collateral disruption of exports from Saudi Arabia, the UAE, Kuwait, and Iraq, whose shipping corridors pass through the same enforcement zone

This dual supply shock means the market is absorbing a reduction meaningfully larger than Iran's standalone share of global production. Broader oil price movements tied to trade war dynamics are amplifying these effects further. The downstream consequences radiate across multiple sectors:

Chinese Teapot Refineries: These independent operators, which function as the primary buyers of discounted Iranian crude, face a dual squeeze from supply tightness and the Treasury's targeted sanctions against their financing networks. Their narrow operating margins leave limited capacity to absorb either cost pressure.

Asian Refining Complex: South Korean, Japanese, and Indian refiners with significant dependence on Persian Gulf crude face spot market tightening and logistics cost increases that compress refining margins across the region.

War Risk Insurance: Premiums for vessels operating in or near the Persian Gulf have escalated substantially since April 13, adding a cost layer to all Gulf-origin cargoes regardless of nationality or destination. This premium creep affects the effective cost of oil for every importing nation, not just those with direct exposure to Iranian supply. Shipping firms warned of sanctions over Hormuz toll payments are further complicating the risk calculus for operators in the region.

How Long Can the Standoff Hold?

| Scenario | Storage Exhaustion Timeline | Production Impact | Revenue Outlook |

|---|---|---|---|

| Base case (current production, no new outlets) | ~4 weeks from early May 2026 | Forced shut-in of export-equivalent volumes | Continued $170M+/day loss |

| Moderate (overland routes partially activated) | Extended by 2-4 weeks | Partial offset of ~250-300K bbl/day | Marginal improvement |

| Optimistic for Iran (enforcement gaps exploited) | Potentially 6-8 weeks | Reservoir damage risk remains elevated | Slow revenue recovery |

| Negotiated resolution | Not applicable | Gradual controlled ramp-up | Revenue recovery begins |

Note: All scenario projections are speculative estimates based on available data as of early May 2026 and should not be treated as forecasts.

The next major ASX story will hit our subscribers first

The Broader Fault Lines: Currency, Legislation, and the Endurance Test

Iran's economy entered the blockade period already under significant stress. The Iranian rial hit a record low against the U.S. dollar during the blockade's intensification, reflecting the cumulative weight of years of sanctions pressure compounded by the new export collapse. Wartime damage to non-oil industrial sectors, including steel and plastics manufacturing, is generating consumer price inflation that compounds the revenue shock from oil. The government has been forced to restrict some non-oil exports that typically provide supplementary foreign exchange earnings, a decision that further tightens the domestic economic environment.

Iran's governing framework has long incorporated what it calls a resistance economy doctrine: a structural approach premised on managing external pressure through domestic substitution, strategic patience, and institutional resilience rather than conventional market integration. This philosophy has produced genuine operational buffers, but it has limits. The physical nature of naval interdiction creates constraints that no amount of domestic economic restructuring can fully offset.

In a significant escalation signal, Iranian authorities have been drafting legislation to assert formal legal control over Strait of Hormuz passage rights. If enacted, such legislation would represent a direct challenge to the freedom of navigation provisions established under the United Nations Convention on the Law of the Sea (UNCLOS), potentially triggering a multilateral legal and diplomatic response. The legislative posture serves simultaneously as domestic political signalling and as international negotiating leverage, signalling that Iran retains the capacity for further escalation even under severe economic pressure. Consequently, understanding the geopolitical oil price drivers at play here is essential for any serious market analysis.

The Negotiation Calculus

At its core, the standoff is an asymmetric endurance contest. U.S. strategy is premised on accelerating Iran's economic deterioration to a threshold at which negotiation becomes the only viable option. Iran's counter-strategy is premised on demonstrating sufficient institutional resilience to raise the political and economic cost of maintaining the blockade for Washington, particularly as domestic energy price pressures mount.

Several factors introduce genuine uncertainty into the resolution timeline:

- The strictness of enforcement over coming weeks, particularly as U.S. domestic energy price pressures intensify

- The pace of overland route activation and whether Iran can expand non-maritime export capacity faster than storage fills

- The political tolerance in Washington for four-year-high oil prices persisting through domestic economic cycles

- The reservoir integrity question: whether Iran can sustain managed curtailments long enough for diplomatic channels to open, or whether the physical constraints force damaging shut-ins first

Iran's institutional resilience, forged through cycles of war and sanctions that most market observers underestimate in their depth and sophistication, provides genuine short-term buffering capacity. The physical nature of naval interdiction, however, creates constraints that the financial sanctions periods of prior decades simply never imposed. How that asymmetry resolves will determine whether the Iran oil exports blockade in the Strait of Hormuz ends in negotiation or in the kind of forced production collapse that Washington is explicitly seeking and Tehran is racing to prevent.

Disclaimer: This article contains forward-looking analysis, scenario modelling, and speculative projections based on information available as of early May 2026. Energy market conditions, geopolitical developments, and enforcement postures can change rapidly and unpredictably. Nothing in this article constitutes investment advice or a forecast of future outcomes. Readers should consult qualified financial and geopolitical analysts before making decisions based on this content.

Want To Stay Ahead of the Market Disruptions Reshaping Global Commodity Flows?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex market signals into actionable opportunities — explore historic discoveries and their returns to understand how transformative these moments can be, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.