June 11, 2026

The World's Most Dangerous 21 Miles: Understanding the Strait of Hormuz

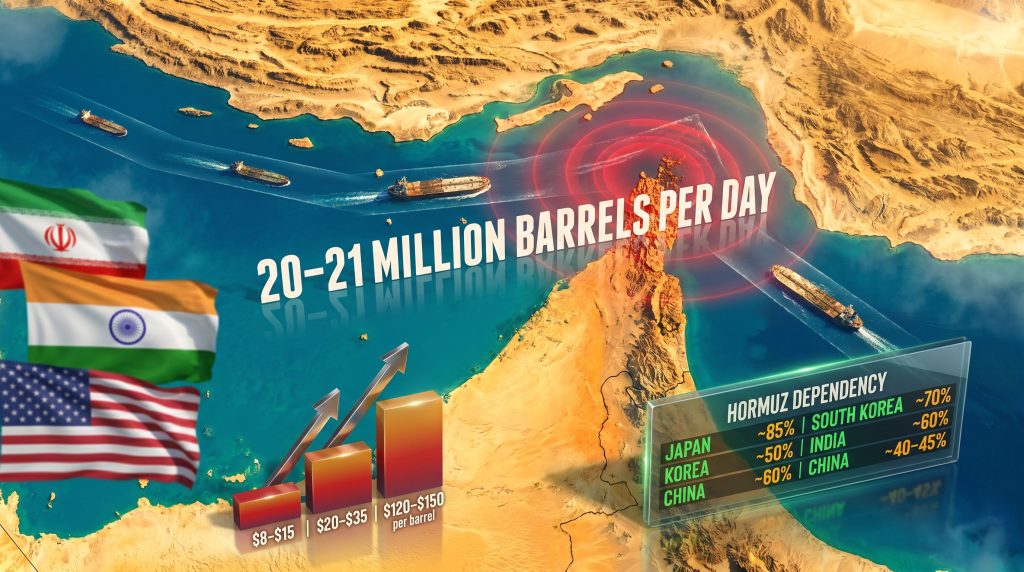

Few geographic features on Earth carry the concentrated economic weight of the Strait of Hormuz. Stretching just 21 nautical miles at its narrowest navigable point, with shipping lanes of only 2 nautical miles in each direction, this sliver of water between Iran and the Oman Peninsula functions as the circulatory system of global energy supply. Approximately 20 to 21 million barrels of crude oil move through this passage every single day, accounting for roughly one-fifth of total global oil consumption. Iran shuts Strait of Hormuz after US strikes represents one of the most significant energy security events in recent history. No other transit route on the planet concentrates so much economic consequence into such a confined space.

Understanding the strategic logic of the Strait of Hormuz is essential context for interpreting what happens when that system is threatened. Unlike pipelines or overland corridors, maritime chokepoints cannot be easily duplicated, rerouted, or scaled. When the strait is disrupted, the entire architecture of global energy pricing shifts almost instantaneously, long before a single barrel goes missing from a refinery's feedstock supply.

Chokepoint Dependency: Which Economies Face the Greatest Exposure?

The risk is not distributed equally across the world. Asian economies sit at the sharp end of any Hormuz disruption scenario, while Western nations maintain comparatively larger buffers through domestic production, diversified import routes, and strategic reserves.

| Country/Region | Estimated Oil Imports via Hormuz | Vulnerability Rating |

|---|---|---|

| Japan | ~85% | Extreme |

| South Korea | ~70% | Extreme |

| India | ~60% | Very High |

| China | ~40-45% | High |

| European Union | ~15-20% | Moderate |

| United States | Less than 5% | Low |

Asian economies bear the structural brunt of any Hormuz disruption. A sustained closure would trigger energy rationing protocols across East and South Asia before Western markets absorb the full impact of reduced supply.

Beyond crude oil, the strait is also the primary export corridor for Qatar's liquefied natural gas operations. Qatar is the world's largest LNG exporter, shipping approximately 77 million tonnes per annum, virtually all of which transits this passage. This creates a secondary vulnerability layer for nations that have diversified away from crude dependency but built growing reliance on gas-fired power generation. For a deeper understanding of these dynamics, the LNG supply outlook for 2025 provides important context on how markets were already positioned before this crisis emerged.

When big ASX news breaks, our subscribers know first

Iran Shuts Strait of Hormuz: What Is Verified and What Remains Disputed

Following a fresh wave of US military strikes on Iran, conducted under orders from President Donald Trump, Iran's top joint military command issued a formal public announcement declaring the Strait of Hormuz closed to all maritime traffic. The declaration covered oil tankers, commercial vessels, and all other shipping, with explicit warnings that any vessel attempting transit would be targeted and fired upon.

Iranian state media reported explosions, air defence activations, and alleged direct confrontations between US and Iranian forces in the vicinity of the waterway. The announcement represented an immediate and significant escalation in the ongoing US-Iran-Israel conflict dynamic that has been building through successive rounds of proxy warfare, targeted strikes, and sanctions pressure.

What US Central Command Said

US Central Command publicly disputed the characterisation of the strait as physically closed, stating that commercial vessel traffic had not ceased entirely. Independent maritime tracking data during the hours following the announcement reportedly showed some continued vessel movement, adding to the ambiguity of the operational situation on the water.

Separating Confirmed Facts from Contested Claims

The following breakdown distinguishes what has been independently verified from what remains under dispute:

- Confirmed: US military strikes were conducted inside Iran under presidential orders

- Confirmed: Iran's military command issued a formal public closure warning for the strait

- Confirmed: The Palau-flagged MT Settebello was attacked while transiting the Gulf of Oman, resulting in the deaths of 3 Indian nationals

- Confirmed: India's Ministry of External Affairs formally protested and condemned the attacks involving Indian seafarers

- Disputed: Whether all commercial traffic has physically ceased remains contested between Iranian and US sources

The critical distinction here is between a declared closure, which functions as a legal and military warning capable of suppressing voluntary transit, and a physically enforced blockade that stops all vessel movement through direct interdiction. The current situation occupies the dangerous space between these two definitions, and that ambiguity alone is sufficient to reprice global energy markets.

India's MEA spokesperson Randhir Jaiswal confirmed the deaths of three Indian nationals in the MT Settebello attack and stated that New Delhi attaches the highest importance to the welfare of its seafaring community. The ministry also clarified that the three vessels involved in incidents were foreign-flagged and not Indian-owned, though Indian crew members were aboard all of them.

Iran's Hormuz Strategy: A Doctrine Built Over Decades

To understand why the current closure declaration carries genuine market weight, it is necessary to grasp the historical architecture of Iran's Hormuz doctrine. Tehran has wielded the threat of strait closure as its most powerful asymmetric economic lever since the 1980s, treating it as a deterrence instrument rather than a routine operational decision.

During the Iran-Iraq War Tanker War period between 1984 and 1988, Iran demonstrated both the willingness and the capability to conduct kinetic operations against commercial shipping transiting the Gulf. The precedent established during that period created a template that Iranian strategic planners have returned to repeatedly.

Closure threats during the 2011-2012 standoff over Iran's nuclear programme caused Brent crude to spike by approximately 10 to 15 percent within days, purely on the basis of rhetorical escalation without any physical enforcement. The 2019 Gulf of Oman tanker attacks, widely attributed by Western governments to Iranian forces, demonstrated that Tehran was prepared to conduct actual strikes on commercial shipping without issuing a formal closure declaration. Furthermore, understanding crude oil price geopolitics helps explain why these historical patterns consistently translate into immediate market repricing.

Strategic Pattern: Iran has historically deployed Hormuz threats as a pressure valve, escalating rhetoric to extract diplomatic concessions rather than sustaining a full blockade. A sustained physical closure would also harm Iran's own oil export revenues, creating a self-limiting dynamic that has historically constrained follow-through.

What makes the current situation structurally different from previous cycles is that it involves direct US-Iran military exchanges rather than proxy engagement. The escalatory threshold that has been crossed is qualitatively higher than earlier confrontation episodes, which reduces the reliability of historical precedent as a guide to likely outcomes.

Energy Market Scenarios: Modelling the Oil Price Consequences

The range of possible outcomes for global energy markets spans from a short-term price spike that partially retraces, to a sustained supply shock that restructures global economic growth projections. Three core scenarios define the credible probability space. In addition, oil price volatility trends heading into 2025 had already flagged elevated sensitivity to Gulf disruption events.

Scenario 1: Rhetorical Closure with Limited Physical Disruption

Iran's declaration functions primarily as political signalling. Vessel traffic resumes under heightened military escort, and the physical blockade is not enforced. Under this base case, oil prices spike by $8 to $15 per barrel in the short term before partially retracing as the market prices in limited actual supply disruption. War-risk insurance premiums surge by 200 to 400 percent, and some operators voluntarily reroute around the Cape of Good Hope.

Scenario 2: Partial Enforcement Through Selective Vessel Targeting

Iranian forces selectively engage vessels transiting without US military escort, creating a de facto risk zone that deters commercial shipping without constituting a complete blockade. Oil prices climb $20 to $35 per barrel above pre-crisis levels. LNG spot prices in Asia surge sharply as Japan, South Korea, and India activate strategic petroleum reserve protocols. Global shipping insurance markets enter crisis mode as war-risk exclusion clauses are invoked across major underwriters.

Scenario 3: Full Physical Blockade with Active Naval Confrontation

A sustained physical closure enforced by Iranian naval and air assets, met with active US military counter-operations. Under this tail-risk scenario, oil prices potentially breach $120 to $150 per barrel, depending on the duration of the closure. Global GDP growth projections are revised downward by 0.5 to 1.5 percentage points, and the International Energy Agency coordinates an emergency strategic reserve release among member nations.

Even a credible threat of closure, without physical enforcement, is sufficient to reprice global energy markets. Declared closures have historically moved Brent crude by double digits within 24 to 72 hours purely on the basis of market uncertainty and insurance risk repricing.

Disclaimer: The scenario projections above represent analytical modelling based on historical precedent and current market dynamics. They do not constitute investment advice. Energy market outcomes in geopolitical crisis scenarios carry extreme uncertainty and actual price movements may differ materially from modelled ranges.

India's Strategic Exposure: Energy, Seafarers, and Diplomatic Pressure

India finds itself caught in multiple dimensions of this crisis simultaneously. As both a significant energy importer and a major supplier of maritime labour to the global shipping industry, New Delhi faces vulnerabilities that extend beyond the price of crude.

India imports approximately 85 to 90 percent of its crude oil requirements, with a substantial portion sourced from Middle Eastern producers including Saudi Arabia, Iraq, and the UAE, whose export routes all pass through the Strait of Hormuz. A prolonged closure would force India to activate its Strategic Petroleum Reserve, which holds approximately 5.33 million metric tonnes across underground storage caverns at Visakhapatnam, Mangaluru, and Padur.

India's refining sector, dominated by IOC, BPCL, and HPCL, would begin facing feedstock disruption within an estimated 2 to 3 weeks of a sustained physical closure. Alternative supply routes, including US crude delivered via longer Atlantic tanker passages and Russian Urals via non-Hormuz routing, would add an estimated $4 to $8 per barrel in additional freight costs on top of any underlying price shock.

The human dimension of India's exposure is equally significant. Indian seafarers represent one of the largest national labour pools in global commercial shipping, and the MT Settebello attack that killed three Indian nationals is not an isolated data point but a signal of systemic risk to a workforce that operates across the Gulf on a daily basis.

The Alternative Route Problem: Why Bypass Infrastructure Cannot Fill the Gap

A common misconception in public discourse around Hormuz disruptions is that existing pipeline and maritime bypass infrastructure can adequately compensate for a closure. However, the data does not support this assumption.

| Alternative Route | Capacity | Current Utilisation | Coverage of Hormuz Volume |

|---|---|---|---|

| Saudi Arabia East-West Pipeline (Petroline) | ~5 million bpd | ~50% utilised | ~25% |

| UAE Abu Dhabi Crude Oil Pipeline (ADCOP) | ~1.5 million bpd | Partial | ~7% |

| Cape of Good Hope tanker rerouting | Theoretically unlimited | Adds 10-15 days transit | Cost and time prohibitive |

| Iraq-Turkey Kirkuk-Ceyhan Pipeline | ~0.35 million bpd | Intermittently operational | Minimal |

Even if all alternative infrastructure operated simultaneously at maximum rated capacity, the global market could replace only approximately 30 to 35 percent of normal Hormuz throughput. The remaining 65 to 70 percent would require emergency strategic reserve releases, coordinated demand destruction, or diplomatic resolution to prevent a structural supply shock from materialising.

A less commonly discussed constraint is the practical ceiling on Cape of Good Hope rerouting. While theoretically scalable, the additional 10 to 15 days of transit time per voyage effectively reduces global tanker fleet capacity when a significant proportion of voyages simultaneously adopt the longer route. This creates a secondary capacity crunch in the tanker market that amplifies the supply shock beyond what simple volume calculations suggest. Consequently, downstream industrial demand across steel, chemicals, and manufacturing would face compounding pressure as feedstock costs escalate alongside freight disruption.

The next major ASX story will hit our subscribers first

The Geopolitical Triangle: US, China, and Russia in the Hormuz Crisis

The US Military Calculus

The US Fifth Fleet, headquartered in Bahrain, is the designated force for maintaining freedom of navigation in the Persian Gulf. Historical precedent exists for direct US tanker escort operations under fire: Operation Earnest Will, conducted between 1987 and 1988, involved the US military reflagging and escorting Kuwaiti tankers through contested Gulf waters during the Iran-Iraq War Tanker War. The current situation, however, involves direct US-Iran military exchanges rather than third-party escort duties, fundamentally altering the risk calculus.

China's Dual Interest Position

China's strategic position in this crisis is uniquely complicated. Importing approximately 40 to 45 percent of its crude through the Strait of Hormuz, Beijing has substantial economic reasons to want the waterway open. Its deepening diplomatic relationships with both Iran through the 25-year Comprehensive Cooperation Agreement and with Saudi Arabia through its brokered normalisation role position China as a potential back-channel mediator. However, Beijing's unwillingness to directly challenge US military operations in the region limits its practical intervention capacity to diplomatic pressure rather than deterrence. The broader context of oil markets and geopolitics illustrates how US-China tensions were already reshaping energy trade flows before this crisis emerged.

Russia's Energy Arbitrage Opportunity

A sustained Hormuz disruption would dramatically increase the market value of Russian pipeline gas supplies and Arctic LNG routes to both Europe and Asia. Moscow has both the strategic incentive and the supply infrastructure to position itself as an emergency alternative supplier to India and China, both of which have maintained energy trading relationships with Russia despite Western sanctions pressure following the 2022 Ukraine invasion. The crisis creates an inadvertent strengthening of Russia's energy leverage at a moment of existing geopolitical tension.

Frequently Asked Questions: Iran Shuts Strait of Hormuz After US Strikes

Has Iran Ever Physically Closed the Strait Before?

Iran has never sustained a complete physical closure of the Strait of Hormuz in the modern era. All previous closure declarations, including those during the 1980s Tanker War and the 2011-2012 nuclear sanctions crisis, functioned as strategic pressure instruments rather than enforced blockades. The 2026 Strait of Hormuz crisis represents the most operationally serious iteration of this threat in recent decades, distinguished by the fact that it follows direct US military strikes on Iranian territory rather than sanctions or proxy confrontations.

What Would a 30-Day Closure Do to Oil Prices?

Energy security analysts generally model a sustained 30-day physical closure as producing an upward shock of $30 to $60 per barrel to Brent crude, depending on the speed and coordination of strategic reserve releases by IEA member nations. Tail-risk models that incorporate broader regional conflict escalation place potential price levels above $150 per barrel under extended closure scenarios.

Is the Strait Actually Closed Right Now?

The current situation is best characterised as a declared but not fully enforced closure. Iran's military command has issued formal warnings that vessels attempting transit will be fired upon. US Central Command has disputed that all commercial traffic has ceased. The declared closure alone, regardless of physical enforcement, is sufficient to deter voluntary commercial transit and trigger war-risk insurance repricing across the global shipping market. Iran shuts Strait of Hormuz after US strikes remains the defining geopolitical energy event of the current period.

What Are the Immediate Consequences for LNG Markets?

Qatar's LNG exports of approximately 77 million tonnes per annum route almost entirely through the strait, creating acute exposure for Japan and South Korea, which rely on LNG for 30 to 40 percent of their electricity generation. European nations that have been diversifying into Qatari LNG since reducing Russian gas dependence in 2022 now face an unexpected Hormuz exposure vector. This was not part of their original energy security calculus when those diversification strategies were designed, and consequently the crisis has introduced considerable uncertainty across multiple regional energy systems simultaneously.

Want to Stay Ahead of the Next Major Market-Moving Discovery?

When geopolitical shocks like the Strait of Hormuz closure send energy markets into turmoil, the investors best positioned are those already holding the right assets — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they hit the market, turning complex data across 30+ commodities into clear, actionable opportunities. Explore historic discoveries and the returns they generated, then begin your 14-day free trial at Discovery Alert to ensure you're positioned before the broader market catches on.