June 20, 2026

The Architecture of an Oil Market Inflection Point

Energy markets rarely move on fundamentals alone. The interplay between geopolitics, shipping logistics, and diplomatic timelines creates information asymmetries that professional traders exploit and retail participants misread. The moment a geopolitical constraint on crude supply begins to loosen, the market's first instinct is to price in the most optimistic scenario, often before the physical evidence fully supports it. What is unfolding in the Persian Gulf and Gulf of Oman right now is precisely this kind of inflection, one where Iran ships oil after U.S. peace deal negotiations produced a preliminary framework, and where the gap between appearance and reality is wider than headline figures suggest.

Understanding what this moment actually means, and what it does not, requires moving beyond the initial export numbers into the structural mechanics of how Iranian crude reaches global markets, who buys it, and what institutional forces could either accelerate or reverse the current trajectory. Furthermore, a current crude market overview provides essential context for situating these developments within broader price dynamics.

When big ASX news breaks, our subscribers know first

Chabahar First: Why the Initial Export Signal Came From Outside the Gulf

When analysts began detecting the first clear indicators of resumed Iranian crude movement, the data emerged not from the Strait of Hormuz, but from Chabahar, a deep-water port situated on the Gulf of Oman near Iran's border with Pakistan. This geographic detail is not incidental. It carries significant strategic and analytical weight.

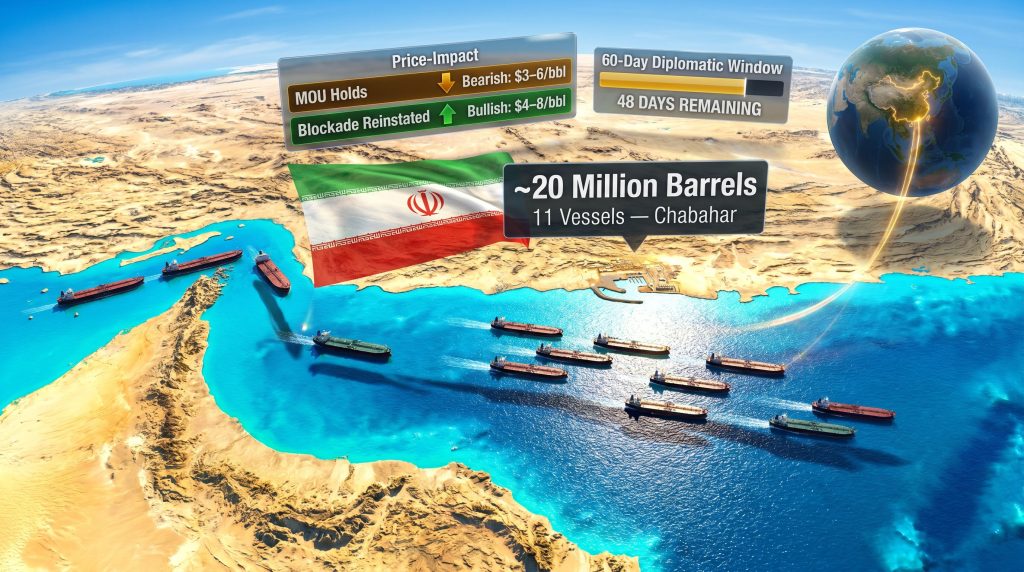

Shipping data compiled by Bloomberg showed 11 tankers carrying a combined volume of approximately 20 million barrels (MMbbl) departing Chabahar in the days following Iran's signing of a memorandum of understanding with Washington on June 18, 2026. The U.S. military had previously prevented these vessels from transiting into the Indian Ocean as part of a sustained effort to constrain Tehran's petroleum revenues.

Chabahar's significance as the initial export signal reflects several operational realities:

- Its position outside the Persian Gulf meant tankers could access open ocean without navigating the politically charged Hormuz corridor

- U.S. naval interdiction pressure was concentrated in the Persian Gulf approaches, making Chabahar the path of least resistance once diplomatic conditions shifted

- Vessel movements from Chabahar are more straightforward to track via Automatic Identification System (AIS) data, providing analysts with cleaner volume estimates than the transponder-blackout environment inside the Gulf

- The port's infrastructure had been maintained through the sanctions period, partly due to its strategic importance to Indian supply chain interests, making it operationally ready for rapid throughput increases

Quantifying the Initial Export Wave

| Metric | Reported Figure |

|---|---|

| Tankers departing Chabahar | 11 vessels |

| Combined cargo volume | ~20 MMbbl |

| NITC-linked vessels transiting Hormuz | ~3 tankers |

| Estimated NITC volume | ~5 MMbbl |

| Supertankers crossing Hormuz | At least 4 |

| MOU negotiation window | 60 days |

The National Iranian Tanker Company (NITC), Iran's state-linked shipping entity, contributed a subset of this total through separate Hormuz transits. However, the reliability of Hormuz-based volume estimates is compromised by a growing practice of navigating the strait with AIS transponders switched off, with vessels hugging Oman's coastline to minimise detection exposure.

What the U.S.-Iran MOU Actually Means for Oil Markets

The diplomatic instrument at the centre of this supply shift is classified as a memorandum of understanding, not a binding treaty, not a sanctions relief framework, and not a permanent peace accord. This distinction matters enormously for how market participants should interpret current export volumes. Consequently, understanding the broader implications of sanctions and oil trading offers a useful parallel for assessing how these diplomatic constraints unwind in practice.

The MOU was designed to function as a 60-day diplomatic bridge, creating space for formal negotiations over Iran's nuclear programme and regional security architecture. Its energy-related provisions were intended to unlock crude, condensate, and broader hydrocarbon flows, but implementation has been uneven from the outset.

The MOU does not constitute a permanent sanctions relief framework. Oil market participants should treat current export volumes as an early-stage indicator, not a baseline for sustained supply growth.

Several critical elements remain unresolved:

- Formal peace negotiations, initially scheduled to convene in Switzerland on June 20, 2026, were postponed following overnight clashes between Israeli forces and Iran-backed Hezbollah fighters in southern Lebanon, demonstrating just how fragile the diplomatic scaffold actually is

- Whether the U.S. naval blockade has been fully lifted or merely suspended remains ambiguous, with different monitoring sources reporting conflicting assessments

- The Iranian government's own Persian Gulf State Authority, an entity established specifically to govern Hormuz maritime transits, has issued directives requiring vessels to follow designated routing corridors and has signalled the potential imposition of passage tolls for international shippers

This toll mechanism represents an underappreciated commercial variable. If formalised, it would introduce a new cost layer into Hormuz transits, affecting freight economics for every non-Iranian operator moving crude through the strait.

The Hormuz Paradox: Control, Transparency, and Market Uncertainty

The Strait of Hormuz is one of the most consequential maritime chokepoints in the global energy system. Approximately 20% of the world's oil supply passes through its 21-mile-wide navigable channel each day, making any disruption to transit conditions a systemic risk event for crude pricing.

What makes the current situation analytically complex is that Iran is simultaneously trying to increase its own export volumes while asserting unprecedented administrative control over who else can use the strait and under what conditions. This dual dynamic creates tension that doesn't resolve neatly into a bullish or bearish narrative.

According to Reuters, the Friday following the MOU signing produced a striking data point: no non-Iranian outbound tankers were observed moving through the Persian Gulf. This stood in sharp contrast to the prior Thursday, when vessels carrying an estimated 10 MMbbl were either crossing or positioned near the Hormuz approach. The supertanker Tenzan offered one of the few identifiable data points from that period, reappearing in the Gulf of Oman after appearing to cross the strait overnight with limited tracking visibility.

The AIS Transponder Problem

The practice of navigating Hormuz with transponders disabled has become increasingly common and introduces significant lag into real-time market intelligence. For traders and analysts relying on AIS data, this creates a structural blind spot:

- Volume estimates from Hormuz transits carry higher uncertainty margins than those from Chabahar

- Price signals derived from supply estimates may be systematically understating actual flows, or in volatile conditions, overstating them

- Vessels hugging Oman's coastline while dark are exploiting a geographic feature of the strait's geometry to minimise detection while still making passage

This tracking opacity is not new to Iranian crude markets. The so-called shadow fleet, a loosely affiliated network of tankers operating with opaque ownership structures and inconsistent AIS compliance, has been the primary mechanism for moving sanctioned Iranian barrels to Chinese buyers throughout the past several years of maximum pressure policy.

China's Structural Role as Iran's Anchor Customer

The destination for the overwhelming majority of Iranian crude exports is China, and this has been the case consistently throughout the sanctions era. Chinese state-affiliated and independent refineries, particularly teapot refineries in Shandong province, have been the buyers sustaining Iranian export revenues during periods of maximum U.S. enforcement pressure.

The commercial logic is straightforward: Iranian crude typically trades at a significant discount to dated Brent, historically in the range of $5 to $15 per barrel depending on enforcement intensity, grade characteristics, and freight cost adjustments. For price-sensitive Chinese buyers operating on thin refining margins, this arbitrage has been irresistible. In addition, the broader trade war impact on oil markets has further shaped the appetite of Chinese buyers for discounted non-Western crude supplies.

A sustained increase in Iranian export volumes would carry several downstream consequences:

- Reduced Chinese import costs for medium-sour crude grades, potentially freeing budgetary capacity for purchases from other origins

- Compression of Asian refining margins for competing grades, particularly barrels from Saudi Arabia, Iraq, and Russia competing for the same refinery slate

- Potential erosion of the discount premium itself, as increased Iranian availability reduces the scarcity value that underpins the pricing structure

Iranian crude is predominantly medium-sour in quality, with major grades including Iranian Heavy (approximately 30° API, 1.7% sulphur) and Iranian Light (around 33° API, 1.4% sulphur). These grades slot directly into the refinery configurations of complex Chinese plants optimised for middle-distillate yields, making them genuinely competitive on a quality-adjusted basis once the sanctions discount is factored in.

Oil Price Scenarios: Mapping the Range of Outcomes

The current situation does not resolve into a single price direction. Instead, it presents a scenario matrix where outcomes depend heavily on diplomatic variables that remain genuinely uncertain. For further geopolitical oil price analysis, the interplay between regional tensions and crude benchmarks has rarely been more pronounced.

| Scenario | Probability Assessment | Estimated Price Impact |

|---|---|---|

| MOU holds, full 60-day negotiation proceeds | Moderate-High | Bearish: potential $3-6/bbl downward pressure |

| Negotiations collapse, blockade reinstated | Moderate | Bullish: sharp reversal, $4-8/bbl upside |

| Hormuz toll regime formalised | Low-Moderate | Neutral-to-bearish with volatility spike |

| Israel-Hezbollah escalation disrupts deal | Low-Moderate | Strongly bullish, supply disruption premium |

The bearish case rests on Iran adding meaningful incremental supply to a global market that was already contending with OPEC+ production increases earlier in 2026. If Iranian exports climb toward pre-sanctions levels of 2.5 to 3.0 million barrels per day from an estimated current baseline of roughly 1.5 million barrels per day, the supply addition would be substantial enough to materially affect the supply-demand balance.

The bullish reversal case is equally plausible. If the Israel-Hezbollah ceasefire collapses, or if U.S. domestic political dynamics shift toward reinstating naval enforcement, the rapid contraction in Iranian volumes would remove a supply source that markets had begun pricing in, triggering a sharp upward correction.

The next major ASX story will hit our subscribers first

OPEC+ and the Internal Alliance Stress Test

Iranian export growth occurring outside the OPEC+ quota framework creates a structural problem for the cartel's internal cohesion. Saudi Arabia and the UAE, both of whom have been managing their own production adjustments to support price levels, face a direct market share challenge if Iranian volumes expand without coordination. OPEC's global oil influence remains a central force shaping how member states respond to this kind of unsanctioned supply growth.

The arithmetic is uncomfortable for Riyadh. Every additional barrel Iran places into Chinese refineries is a barrel potentially displaced from Saudi Aramco's contract book. At pre-sanctions production levels, Iran was a top-five global producer. A return toward that output level would require either:

- A compensating OPEC+ production cut by other members to absorb the additional supply

- An acceptance of lower price levels across the Gulf producer bloc

- A formal reintegration of Iran into the OPEC+ quota framework, which would require extensive diplomatic negotiation

None of these outcomes is straightforward. The cartel's next production policy decision will almost certainly treat Iranian export trajectory as a pivotal input variable, regardless of whether Tehran is formally at the table.

Risk Factors That Could Reverse Current Momentum

Energy market participants should assess the following risk factors when evaluating the durability of Iran's resumed export volumes:

- Israel-Hezbollah conflict spillover: The postponement of Switzerland talks following overnight clashes demonstrates that regional proxy dynamics can derail diplomatic progress with minimal warning

- Iranian domestic political resistance: Hardline factions within Iran's political establishment have historically resisted transparency commitments on nuclear-related matters, and compliance with MOU terms is not guaranteed

- U.S. policy reversal risk: Washington's strategic posture on Iran enforcement is sensitive to Israeli security considerations, and political pressure to reinstate interdiction measures could intensify depending on how regional events evolve

- Transponder evasion normalisation: If AIS blackout navigation becomes standard Hormuz practice, it undermines the data transparency that supports market confidence in Iranian supply estimates

Prerequisites for a Stable Hormuz Corridor

- Formal, codified lifting of U.S. naval interdiction orders through written diplomatic instruments

- International shipping operators accepting Iran's Persian Gulf State Authority routing and toll requirements

- Sustained de-escalation between Israel and Iran-aligned forces across Lebanon, Syria, and Gaza

- Verified and independently confirmed progress on nuclear transparency within the 60-day MOU window

What to Watch: A Forward-Looking Monitoring Framework

For energy analysts, traders, and investors tracking this situation, the following indicators provide the most actionable intelligence:

- Chabahar departure data remains the most reliable leading indicator of Iranian export momentum, given its cleaner AIS compliance environment compared to Hormuz transits

- AIS transponder compliance rates through the Strait of Hormuz function as a proxy for shipping operator confidence and overall geopolitical stability in the corridor

- The 60-day MOU negotiation clock is the single most important structural variable: whether formal talks resume and produce substantive progress will determine whether current volumes represent a durable shift or a transient window

- OPEC+ response signals from Saudi Arabia and the UAE will indicate how seriously Gulf producers are treating the Iranian supply threat to their market share and fiscal breakeven calculations

- Israel-Hezbollah ceasefire durability remains the primary near-term wildcard capable of unravelling the entire diplomatic framework within days

As reported by the BBC, Iran ships oil after U.S. peace deal conditions began to take shape, but the durability of those conditions remains far from settled. The weeks ahead will test whether this represents a genuine structural shift in global supply or a temporary diplomatic window that closes as quickly as it opened.

Disclaimer: This article contains forward-looking analysis and scenario-based projections relating to geopolitical events, oil market conditions, and diplomatic outcomes. These projections involve significant uncertainty and should not be construed as financial advice. Readers should conduct independent research and consult qualified financial advisers before making investment decisions based on geopolitical developments in global energy markets.

Want to Stay Ahead of Major Commodity Discoveries Driving the Next Market Move?

While geopolitical forces reshape global energy supply chains, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across 30+ commodities — turning complex market signals into clear, actionable opportunities. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.