May 22, 2026

The Strait No One Can Afford to Lose: Reassessing Hormuz in an Era of Transit Risk

Energy markets have spent decades pricing geopolitical risk as an episodic variable, a temporary premium that fades when tensions cool. That assumption is being systematically dismantled by the evolving situation in the Strait of Hormuz. What is now emerging is not simply another cycle of Middle Eastern tension but a structural shift in how the world's most consequential maritime chokepoint must be priced, planned around, and ultimately rerouted.

The Iran Strait of Hormuz toll on oil prices debate has moved from theoretical to operational. Understanding its true market implications requires separating three distinct but frequently conflated scenarios: a modest transit fee that preserves flow, an escalating toll that compresses exporter economics, and a full closure that triggers a global supply crisis. Each carries radically different consequences for Brent crude, Gulf producer revenues, and the broader architecture of global energy security.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Unlike Any Other Chokepoint

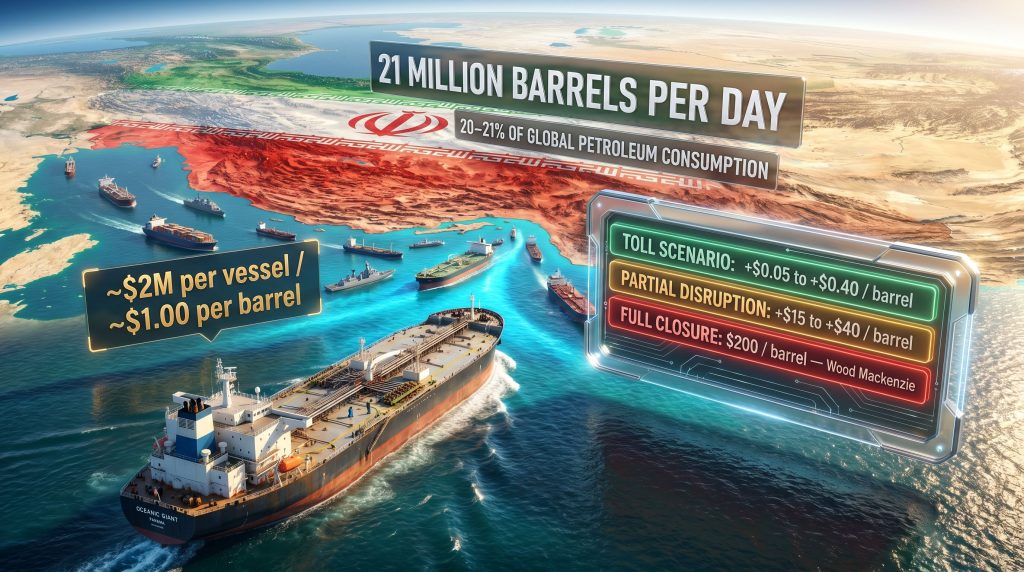

The mathematics of Hormuz dependency are staggering in their concentration. More than 21 million barrels per day of crude oil and petroleum products transit this waterway, representing approximately 20 to 21 percent of total global petroleum liquids consumption. Of that volume, over 11 million barrels per day of Gulf crude and condensate have no viable alternative maritime export route in the near term.

The physical geography compounds the strategic problem. At its narrowest point, the Strait spans just 21 nautical miles, with navigable shipping lanes of only 2 miles in each direction. This creates an extraordinary concentration of economic value through an extraordinarily narrow physical corridor.

"No other single maritime chokepoint concentrates this volume of energy trade. The Panama Canal, Suez Canal, and Strait of Malacca each carry significantly less petroleum traffic, making Hormuz structurally irreplaceable across any realistic short-to-medium term planning horizon."

The major producers dependent on Hormuz as their primary export corridor include Saudi Arabia, the UAE, Kuwait, Iraq, and Qatar, whose liquefied natural gas exports also transit the Strait. Furthermore, the geopolitical tensions reshaping trade around this region make this not a peripheral risk — it is a systemic one embedded at the foundation of global energy supply chains.

Toll vs. Closure: Why the Distinction Defines the Price Outcome

One of the most persistent analytical errors in covering the Hormuz situation is conflating a transit toll with a physical blockade. These are fundamentally different threat mechanisms with vastly different oil price implications.

A toll is a fiscal extraction mechanism. It imposes a cost on transit without restricting the underlying flow of barrels. A closure is a physical supply constraint that eliminates flow entirely. The price consequences of each are not just different in magnitude — they operate through entirely different economic channels.

Reports from maritime intelligence sources indicate that Iran's Islamic Revolutionary Guard Corps has been operating a de facto clearance and documentation system for vessels transiting the Strait. Some vessels have reportedly paid passage fees, with certain transactions conducted in Chinese yuan rather than US dollars. This represents a deliberate signal of dollar-bypass intent that carries its own geopolitical significance. The reported toll rate has been approximately $2 million per vessel.

Translating the Per-Vessel Fee Into a Per-Barrel Cost

The per-vessel toll translates into a per-barrel cost that is far more modest than headline figures suggest:

| Metric | Estimated Figure |

|---|---|

| Reported toll per vessel | ~$2 million USD |

| VLCC cargo capacity | ~2 million barrels |

| Effective cost per barrel | ~$1.00 USD |

| Estimated global oil price impact | ~$0.05 to $0.40/barrel |

| Share of toll burden absorbed by Gulf exporters | ~80 to 95% |

Howard Shatz, Senior Economist at RAND and Professor of Policy Analysis at the RAND School of Public Policy, has assessed that under a permanent Hormuz toll scenario, oil prices would most likely experience only a slight upward adjustment. Alternatively, shipping margins would compress modestly to absorb the additional cost, with the overall price impact remaining contained rather than disruptive, according to comments reported by Rigzone in May 2026.

Critical framing: At roughly $1 per barrel of cargo, independent economic analysis estimates the global oil price impact of a permanent Hormuz toll at only $0.05 to $0.40 per barrel under baseline conditions. This is a modest cost signal, not a market-breaking shock. In addition, crude oil price trends suggest that even modest sustained shifts in supply costs can compound significantly over time.

Who Actually Absorbs the Cost? The Exporter vs. Consumer Equation

Perhaps the most underappreciated dynamic in the Iran Strait of Hormuz toll on oil prices discussion is the question of cost incidence: who actually ends up paying?

Economic modelling consistently points to Gulf oil exporters absorbing the dominant share of the toll burden. Rather than a cost that flows cleanly through to global benchmark prices, the toll functions primarily as a compression of export netbacks — the net revenue Gulf producers receive after deducting freight and related costs from their realised sale price.

- Gulf state exporters including Saudi Arabia, the UAE, Kuwait, and Iraq would absorb an estimated 80 to 95 percent of the toll burden through reduced netbacks

- Global consumers would experience only a marginal price signal under a stable, contained toll scenario

- This cost distribution dynamic makes the toll politically and economically significant for Gulf producers while remaining relatively contained for importing nations in isolation

- The toll therefore functions structurally as a tax on Gulf exporters, not a consumer-facing energy price shock

This distinction matters enormously for how importing nations, their governments, and their central banks should assess and respond to the toll scenario.

The Escalation Pathways: When Modest Becomes Catastrophic

The base case analysis supports a contained oil price outcome under a stable toll. However, energy markets are not static systems, and the escalation pathways from toll to disruption are the scenarios that warrant the most serious attention.

Wood Mackenzie's scenario analysis has identified a prolonged physical closure of the Strait of Hormuz as the single greatest threat to global energy markets in decades. Their worst-case projection is explicit: oil prices could reach $200 per barrel if more than 11 million barrels per day of Gulf crude and condensate supply remain curtailed for a sustained period.

Warning: The $200 per barrel scenario is contingent on a sustained physical closure of the Strait, not the imposition of a transit fee. Conflating these two scenarios produces materially inaccurate price forecasting and policy responses. Analysis of the trade war impact on oil markets similarly demonstrates how conflated risk signals can distort market responses.

Three Distinct Scenarios and Their Price Implications

| Scenario | Oil Price Impact | Key Trigger |

|---|---|---|

| Contained toll, flow preserved | +$0.05 to +$0.40/barrel | ~$1/barrel toll rate maintained |

| Escalating toll, partial supply disruption | +$15 to +$40/barrel | Effective 2 to 5 million bpd reduction |

| Full physical closure, worst case | Up to $200/barrel (Wood Mackenzie) | 11+ million bpd curtailed |

The progression between these scenarios is not linear, and the critical variable at every stage is whether the United States takes diplomatic or military countermeasures to prevent escalation. Simon Henderson, director of the Bernstein Program on Gulf and Energy Policy at the Washington Institute for Near East Policy, has noted that Gulf nations would actively seek US intervention to prevent toll institutionalisation, as reported by Rigzone.

Standard Chartered's Risk Premium Framework: A Permanently Changed Equation

Beyond immediate price impacts, Standard Chartered Bank's Energy Research division has introduced a conceptually important and underappreciated analytical framework. Standard Chartered's Head of Energy Research Emily Ashford stated in a report sent to Rigzone in May 2026 that regardless of whether a formal toll emerges from US-Iran negotiations, the Strait of Hormuz can no longer be treated as a permanently secure route.

This assessment has structural implications that extend well beyond the immediate toll debate:

- All barrels exiting the Gulf via Hormuz now carry a permanent operational risk premium, even during periods of apparent geopolitical calm

- Any alternative routing that bypasses Hormuz receives an implicit economic advantage, improving its competitiveness relative to Hormuz-routed supply

- Energy companies, insurers, and sovereign wealth funds must incorporate this repriced risk into long-duration capital allocation decisions

- The risk premium does not disappear if a toll agreement is reached, because the underlying enforcement capacity and political willingness have already been demonstrated

This framing shifts the conversation from short-term price forecasting to long-term structural repricing of Gulf-origin energy assets — a fundamentally different and more consequential analytical challenge. Consequently, considerations around energy security and critical minerals are becoming increasingly intertwined with Hormuz risk assessments.

The next major ASX story will hit our subscribers first

Pipeline Bypass Infrastructure: The Long-Run Escape Valve

The most economically rational response to a permanent Hormuz toll is not evasion or confrontation but route substitution through alternative infrastructure. Shatz, in comments reported by Rigzone, highlighted that exporters would accelerate construction of pipelines avoiding the Strait, with capacity additions targeting the Red Sea, the Mediterranean via Syria or other Levant-region countries, and the Mediterranean corridor via Iraq and Turkey.

Existing and Potential Bypass Corridors

- Saudi East-West Pipeline (Petroline): Already operational, providing partial Red Sea bypass capacity to Yanbu, but current throughput falls significantly short of replacing Hormuz volumes

- Iraq-Turkey pipeline: Existing infrastructure connecting northern Iraqi fields to the Turkish Mediterranean port of Ceyhan, with expansion potential

- Red Sea routing expansion: New pipeline and terminal investment connecting Gulf fields to Red Sea export points

- Levant corridor pipelines: Potential new construction through Syria or neighbouring countries, subject to geopolitical stabilisation requirements

None of these alternatives currently possesses the capacity to replace Hormuz volumes at scale. The transition period — during which bypass infrastructure is being constructed and commissioned — represents the window of maximum vulnerability and elevated risk premium.

Iran's Revenue Calculus: Fiscal Reality vs. Geopolitical Signalling

A frequently overlooked dimension of the Iran Strait of Hormuz toll on oil prices analysis is whether Tehran would actually benefit financially from a sustained toll mechanism. As analysts at Bruegel have explored, the question of who ultimately pays and who benefits is considerably more complex than it first appears.

| Revenue Variable | Assessment |

|---|---|

| Revenue sensitivity | Directly proportional to toll rate |

| Primary strategic use | Nuclear, missile programs, proxy network funding |

| Population benefit priority | Assessed as low |

| Sanctions access constraint | May significantly limit fund repatriation |

| Net strategic value | High for leverage signalling; uncertain for fiscal benefit |

Shatz assessed, as reported by Rigzone, that any toll revenue would give Iranian leadership greater freedom to fund nuclear and missile programs or support proxy groups, while the prioritisation of population benefits appears low. Henderson noted that whether Iran could actually access collected funds under current sanctions frameworks remains highly uncertain.

This creates a paradox: the toll's greatest value to Tehran may be its demonstration of leverage capacity rather than genuine fiscal extraction. It signals control over a critical global chokepoint while the actual revenue utility remains constrained by the same sanctions architecture that limits Iran's broader economic integration.

Evasion, Armed Escorts, and the Practical Limits of Non-Compliance

For vessel operators and their clients, the question of evasion is operationally critical. The practical conclusion from expert analysis is that meaningful evasion without permanent armed naval escort is highly unlikely.

Shatz highlighted an additional complication, as reported by Rigzone: Iran could maintain retroactive enforcement by tracking non-compliant vessels and pursuing back-payment claims, effectively requiring permanent armed escort commitments rather than isolated interventions. The sustained cost of such escort operations would likely exceed the toll itself in many scenarios.

The implication is clear. Commodity exporters, whether of oil, gas, or other Gulf-origin goods, would rationally pursue route substitution as the dominant long-run response rather than confrontational non-compliance. Furthermore, legal experts have argued that Iran's toll mechanism defies international maritime law, adding another layer of complexity to enforcement and compliance decisions. This dynamic creates a gradual but structural erosion of Hormuz's strategic leverage as bypass infrastructure matures over time.

Long-Term Market Implications for Global Energy Security

The Iran Strait of Hormuz toll on oil prices question sits within a larger structural story about the long-term repricing of Gulf energy risk. Several macro-level implications deserve attention from investors, policymakers, and energy planners:

- Accelerated exploration outside the Gulf: A sustained toll or elevated risk premium creates positive economic incentives for oil and gas development in non-Hormuz-exposed regions including West Africa, North America, Latin America, and the North Sea

- Strategic reserve expansion: Importing nations face renewed economic justification for expanding strategic petroleum reserves as insurance against escalation scenarios

- Energy transition acceleration: A persistent Gulf risk premium strengthens the economic case for renewable energy investment and demand-side efficiency improvements in oil-importing economies

- Insurance and shipping market repricing: Marine war risk premiums on Hormuz-transiting vessels will structurally increase, creating cascading cost effects across global commodity supply chains

"The Strait of Hormuz has undergone a fundamental repricing of its risk profile. Energy markets that continue to treat Hormuz as a stable, permanently secure corridor will systematically misprice Gulf-origin barrels and underestimate the long-run strategic value of alternative supply development."

Moreover, OPEC's market influence becomes increasingly complex to model when a significant proportion of member state exports face structural transit risk of this magnitude.

Frequently Asked Questions: Iran's Strait of Hormuz Toll and Oil Prices

How much would oil prices rise if Iran permanently tolled the Strait of Hormuz?

At a toll equivalent to approximately $1 per barrel of cargo, economic analysis estimates global oil prices would increase by only $0.05 to $0.40 per barrel under a stable, contained toll scenario.

Who pays the Hormuz toll, oil exporters or consumers?

Economic modelling indicates Gulf oil exporters would absorb approximately 80 to 95 percent of the toll cost through reduced export netbacks, with only a marginal portion passed through to global consumers via higher benchmark prices.

Could the Hormuz toll trigger $200 oil?

The $200 per barrel scenario projected by Wood Mackenzie is associated with a full physical closure of the Strait, not a transit toll. A toll that preserves oil flow would produce a far more contained price response.

Can shipping companies evade the Hormuz toll?

Practical evasion without permanent armed naval escort is considered highly unlikely. The more economically viable response is alternative routing through Red Sea or Mediterranean pipeline corridors, though significant infrastructure investment is required.

How does the Hormuz toll affect Iran financially?

The financial benefit to Iran depends on both the toll rate and whether Tehran can actually access collected revenues under existing international sanctions frameworks — a constraint that may significantly limit the fiscal utility of the mechanism.

What alternative routes exist if Hormuz becomes too costly?

Key alternatives include the Saudi East-West Pipeline to the Red Sea, expanded Iraq-Turkey pipeline capacity to the Mediterranean, and potential new Levant-region routing, though none currently have sufficient capacity to fully replace Hormuz volumes at scale.

Key Takeaways

- A transit toll on Hormuz shipping, at reported rates, would produce a modest global oil price increase of $0.05 to $0.40 per barrel, not a market-breaking shock

- The toll functions primarily as a fiscal mechanism targeting Gulf exporters, with global consumers experiencing only marginal direct cost pass-through

- The real price risk lies in escalation from toll to disruption — any scenario reducing physical oil flow through the Strait carries exponentially larger price consequences, up to $200 per barrel in Wood Mackenzie's worst-case analysis

- Standard Chartered's framing is strategically critical: Hormuz now carries a permanent operational risk premium regardless of formal toll outcomes

- Long-run market responses will include accelerated pipeline bypass investment, increased exploration outside the Gulf, and structural repricing of Gulf-origin energy assets across insurance, shipping, and capital markets

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking price projections and scenario analyses involve significant uncertainty and should not be relied upon as predictions of actual market outcomes.

Want To Stay Ahead of the Next Major Resource Discovery Driving These Market Shifts?

As geopolitical risk reshapes global energy supply chains and accelerates exploration outside the Gulf, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data into actionable opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on the Discovery Alert discoveries page, and start your 14-day free trial today to position yourself ahead of the market.