June 26, 2026

When Essential Inputs Disappear, the Entire System Breaks Down

Modern industrial agriculture operates on the assumption that inputs will always be available at some price. That assumption has rarely been tested at scale. Yet every few years, a new disruption forces a confrontation with a deeper structural truth: complex production systems are only as capable as their most constrained essential input. This principle, originally identified in the context of plant nutrition by 19th-century chemist Justus von Liebig, now applies with uncomfortable precision to the global food system in 2025 and 2026.

Liebig's Law of the Minimum holds that plant growth is governed not by the total availability of all nutrients, but by whichever essential nutrient is in shortest supply. The practical implication is stark: no amount of additional phosphorus or potassium can compensate for an absence of nitrogen. Growth stops at the limiting factor. This same logic, extended beyond plant biology into supply chain architecture, describes exactly what the Iran war fertilizer shock is doing to global agriculture right now.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz as an Agricultural Artery

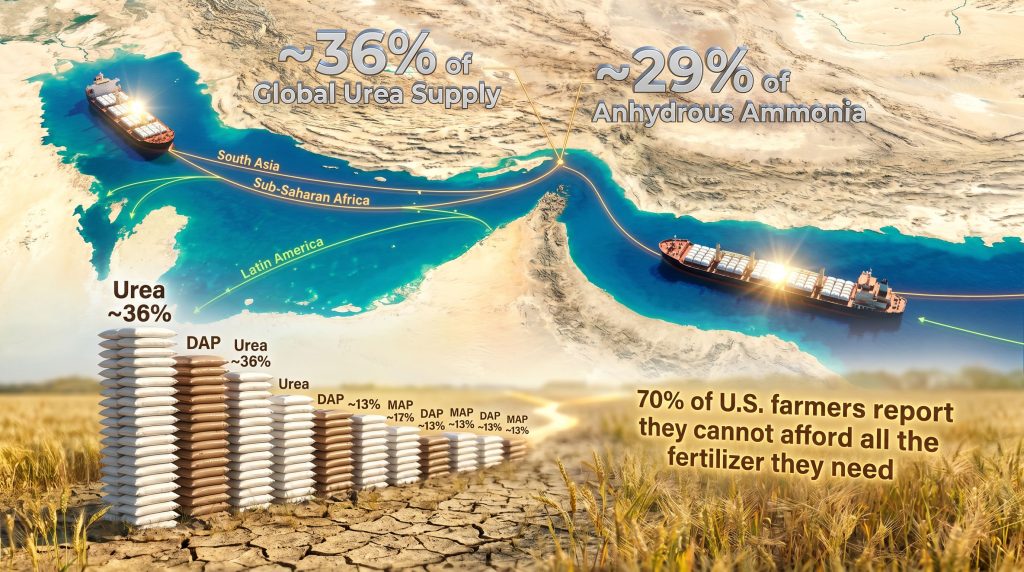

Public discourse about the Strait of Hormuz almost exclusively focuses on crude oil transit. The waterway handles roughly 20% of global oil trade, and any disruption triggers immediate responses in energy markets. What receives far less attention is the strait's equally critical function as an export corridor for agricultural inputs. For context on broader commodity impacts, crude oil price trends have also reflected significant volatility since the conflict began.

The Persian Gulf region is not simply an energy hub. It is one of the world's most concentrated nodes of nitrogen and phosphate fertilizer production, underpinned by cheap and abundant natural gas feedstocks. The numbers are stark:

| Fertilizer Type | Persian Gulf Share of Global Supply |

|---|---|

| Urea (nitrogen fertilizer) | ~36% |

| Anhydrous Ammonia | ~29% |

| Diammonium Phosphate (DAP) | ~26% |

| Monoammonium Phosphate (MAP) | ~13% |

| Liquefied Natural Gas (fertilizer feedstock) | ~20% |

Source: International Food Policy Research Institute (IFPRI)

These figures represent physical product that is no longer moving through global trade channels. Unlike a price spike that can be managed through substitution or efficiency, a physical removal of supply at this scale has no quick remedy. The world cannot conjure nitrogen from alternative sources on a growing-season timeline.

A less-discussed dimension of this disruption is the feedstock problem. Approximately 20% of global LNG exports originate from the Persian Gulf. In import-dependent nations such as India, this LNG is not merely a fuel source; it is the primary raw material for domestic nitrogen fertilizer manufacturing. India's LNG imports have become increasingly strained as the conflict tightens supply, forcing urea production facilities to operate at significantly reduced capacity. The disruption therefore strikes twice: once through the loss of direct fertilizer exports, and again through the destruction of feedstock availability for domestic production elsewhere.

Liebig's Law Applied to Modern Agriculture and Industry

Why No Substitute Exists for Essential Nutrients

Nitrogen, phosphorus, and potassium are the three primary macronutrients required for plant growth. None of them can be sourced from air or water in forms accessible to most crops. Soil reserves are finite. The only meaningful exception is the capacity of leguminous plants such as soybeans to fix atmospheric nitrogen through root-nodule bacteria, a process unavailable to wheat, maize, and rice, which together account for the majority of global caloric production.

This biological reality is what gives Liebig's Law its teeth. When nitrogen supply contracts sharply, farmers growing staple grains face a binary choice: apply less fertilizer and accept lower yields, or abandon planting decisions entirely. Neither outcome is recoverable within a single growing season.

Beyond the Farm Gate: Vaclav Smil's Four Pillars

Energy researcher Vaclav Smil has identified four materials that collectively underpin the physical infrastructure of modern civilisation: cement, steel, plastics, and ammonia. Each of these materials shares a critical characteristic noted by Smil: all four require fossil fuel inputs at considerable scale to produce.

Smil's framework makes visible what commodity price data often obscures: the loss of Persian Gulf oil and gas flows is not merely an energy market event. It is simultaneously a constraint on the physical production capacity of the materials that build, feed, and sustain modern societies.

Ammonia sits at the intersection of this framework and agriculture. It is the foundational chemical precursor for virtually all synthetic nitrogen fertilizers. Its production through the Haber-Bosch process is one of the most energy-intensive industrial activities in the world, consuming approximately 1-2% of total global energy output annually. Disrupting natural gas supply does not simply raise ammonia production costs; it physically limits the scale at which ammonia can be made.

How the Iran War Fertilizer Shock Propagates Through the Food System

Stage One: Physical Supply Removal

The initial disruption operates at the source. Persian Gulf shipping lanes, which carry the urea, ammonia, and phosphate products listed above, have been substantially disrupted by the conflict. This is not a logistics bottleneck resolvable through rerouting. It is a geopolitical closure of a critical export corridor, with no viable maritime alternative of equivalent capacity.

Furthermore, the energy transition demand for alternative inputs has not yet reached a scale that can compensate for these losses, leaving agricultural systems acutely exposed.

Stage Two: Farm-Level Decision Compression

Price signals reach farmers quickly. The documented responses already emerging across key agricultural regions include:

- Reducing fertilizer application rates below agronomically optimal levels, accepting the yield penalty as preferable to the cost

- Switching to lower-input crops that require less nitrogen and fewer petrochemical-based inputs such as herbicides and pesticides

- Reducing total planted area to limit absolute input expenditure

Real-world examples of these responses are already visible. Argentine wheat producers are weighing significant reductions in urea application, with some considering a wholesale crop shift given the economics. In Egypt, at least one documented case involves a farmer cutting planted area to half of normal levels while abandoning wheat entirely in favour of less input-intensive alternatives.

In the United States, a survey conducted by the American Farm Bureau Federation found that approximately 70% of U.S. farmers report being unable to afford all the fertilizer they need during the current season. This is compounded by the country's existing fertilizer import reliance, which leaves domestic producers with limited fallback options when global supply tightens.

It is also worth noting that diesel, the fuel that powers farm equipment throughout the production cycle, arrived at elevated prices after many U.S. farmers had already locked in their planting decisions. For the 2025-2026 season, this primarily compresses margins rather than directly reducing output. However, if high diesel costs persist, they will influence planting decisions in subsequent seasons, creating a secondary wave of production constraint.

Stage Three: Consumer Price Transmission

The pathway from farm-gate input costs to retail food prices follows a predictable sequence:

- Fertilizer costs rise at the farm level

- Farmers reduce application rates or planted area

- Crop yields fall or total production volumes decline

- Commodity markets price in reduced supply expectations

- Food manufacturers face higher raw material costs

- Retail food prices increase, with staple grain categories most affected

- Low-income households in import-dependent nations face acute affordability stress

- Livestock feed costs rise in parallel, eventually elevating meat, dairy, and egg prices with a 6-18 month lag

The livestock amplification effect is frequently underappreciated. Because grain crops feed animals as well as people, a production decline in nitrogen-intensive crops such as maize does not confine its inflationary impact to bread and pasta. It flows through to protein foods across a longer timeline, broadening the consumer price impact considerably.

Regional Vulnerability: Who Bears the Greatest Risk?

| Region | Primary Exposure | Key Vulnerability Factor |

|---|---|---|

| South Asia (India, Bangladesh) | Nitrogen fertilizer and LNG feedstock | High import dependence for both energy and fertilizer |

| Sub-Saharan Africa | Urea and DAP imports | Limited domestic production, low buffer stocks |

| Latin America (Argentina, Brazil) | Wheat and soy input costs | Export-oriented production with thin margin tolerance |

| Middle East and North Africa | Food import dependence | Compounded by regional conflict proximity |

| Southeast Asia | Rice production inputs | Nitrogen-intensive smallholder cultivation systems |

Rice deserves particular attention in this analysis. Paddy rice cultivation is among the most nitrogen-intensive agricultural systems in the world when measured at the smallholder level in South and Southeast Asia. Unlike large commercial operations with credit access and diversified input strategies, smallholder farmers in these regions have minimal financial buffers. A doubling of urea prices does not simply reduce their profitability; it may place optimal fertilizer application entirely beyond their means.

According to analysis from IFPRI, the compounding effects of reduced fertilizer availability across these vulnerable regions could result in food production shortfalls that disproportionately affect the world's most food-insecure populations.

Why This Shock Is Structurally Different From Prior Disruptions

Comparing Major Fertilizer Disruption Events

| Disruption Event | Primary Driver | Duration | Key Affected Markets |

|---|---|---|---|

| COVID-19 supply chain disruption (2020-2021) | Logistics collapse | 12-18 months | Global, broad-based |

| Russia-Ukraine war (2022) | Sanctions and export restrictions | Ongoing | Nitrogen, potash, wheat |

| Iran war fertilizer shock (2025-2026) | Strait of Hormuz disruption | Indeterminate | Nitrogen, phosphate, LNG feedstock |

The critical distinction between the current Iran war fertilizer shock and prior events lies in the mechanism and the duration uncertainty. The COVID-era disruption was fundamentally a logistics problem. Supply chains were operating but moving poorly. The Russia-Ukraine shock was a sanctions and export policy problem: supply existed but access was restricted. Both had identifiable resolution pathways.

A military conflict closure of a major international waterway has no equivalent resolution mechanism. Military timelines are not predictable in the way that port strike negotiations or sanctions policy reviews are predictable. Farmers, commodity traders, and food security planners cannot model around an indeterminate duration.

Each successive disruption since 2020 has reduced the buffer capacity of the global fertilizer system. The system's ability to absorb a third major shock within five years is materially lower than it was in 2019.

The cumulative fragility argument deserves serious weight. Fertilizer inventories that might have cushioned a single-event shock have been drawn down. Supplier relationships that might have offered emergency alternatives have been stressed by prior crises. The system entered the Iran war shock already weakened. Meanwhile, natural gas price trends continue to signal volatility that further complicates production cost forecasting for fertilizer manufacturers globally.

The next major ASX story will hit our subscribers first

Alternative Supply Geography: Can Anyone Fill the Gap?

No single supplier or region can replicate the product volume and diversity currently disrupted. Partial substitution options exist but carry significant constraints:

- Russia and Belarus hold substantial potash and nitrogen production capacity but remain subject to Western sanctions that limit market access, particularly for European and North American buyers

- Canada has significant potash reserves concentrated in Saskatchewan, but production scale-up timelines are measured in years, not growing seasons

- Morocco and OCP Group represent a meaningful phosphate alternative, with OCP being one of the world's largest phosphate exporters, capable of partially offsetting Gulf phosphate shortfalls

- China operates as a major urea producer but has a well-documented pattern of restricting exports when domestic supply concerns arise, making it an unreliable emergency supplier

A multi-source substitution strategy, even if aggressively pursued, would require an estimated 12-24 months to meaningfully offset current shortfalls. That timeline spans multiple growing seasons, meaning at least one and potentially two annual crop cycles will face materially constrained nitrogen and phosphate availability.

Scenario Modelling: The Range of Outcomes

| Scenario | Duration | Estimated Yield Impact | Food Inflation Trajectory |

|---|---|---|---|

| Base Case (3-6 month disruption) | Short-term | 2-5% reduction in nitrogen-intensive crops | Moderate price spike, recovery within 12-18 months |

| Extended Disruption (6-18 months) | Medium-term | 5-12% yield reduction in vulnerable regions | Sustained food inflation, particularly in import-dependent markets |

| Structural Shift (more than 18 months) | Long-term | Systemic reduction in global crop output | Potential food security crisis in low-income import-dependent nations |

Disclaimer: Scenario projections involve inherent uncertainty. These ranges are illustrative frameworks for risk assessment, not forecasts. Actual outcomes will depend on conflict duration, diplomatic developments, farmer adaptation, and policy responses across multiple jurisdictions.

As experts have warned, the extended disruption and structural shift scenarios carry consequences that extend well beyond commodity markets, potentially reshaping agricultural investment decisions and government food security strategies for years to come.

The Long-Term Reckoning: Energy, Fertilizer, and Food as One Policy Domain

Petroleum consultant Art Berman has raised the possibility that world oil production may not return to pre-conflict levels following the Iran war. If this scenario proves accurate, the implications extend far beyond energy markets. Smil's four foundational materials, all fossil-fuel-dependent, would face structurally higher production costs on a permanent basis. In that world, the economics of synthetic nitrogen fertilizer production shift not temporarily but persistently.

This longer-term scenario underscores a strategic gap in how governments have historically designed food security policy. Energy security, fertilizer security, and agricultural resilience have been treated as separate domains with separate ministries, separate budgets, and separate frameworks. The Iran war fertilizer shock demonstrates that they are, in physical terms, a single integrated system. A disruption at the energy node propagates through the fertilizer node and emerges as a food security crisis within one or two growing seasons.

Longer-term structural responses, including precision agriculture technologies that reduce per-hectare fertilizer requirements, biological nitrogen fixation research for non-legume crops, and soil health programmes that rebuild natural nutrient cycling capacity, all represent genuine pathways to reduced vulnerability. However, these are multi-year to multi-decade transitions.

Farmers currently facing unaffordable input costs cannot simultaneously invest in long-term resilience strategies. The policy design challenge is to address the immediate crisis without entrenching the dependency that makes future crises inevitable. The belief that essential input constraints were a solved problem of industrial modernity is being revised in real time. Liebig understood in the 1800s that a single missing nutrient could limit the productivity of an entire system. The global food economy is now learning the same lesson at civilisational scale.

Want to Stay Ahead of Commodity Disruptions Reshaping Global Markets?

When supply chain shocks like the Iran war fertiliser crisis expose deep vulnerabilities across agricultural and commodity markets, identifying the next major investment opportunity requires real-time intelligence. Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to surface significant mineral discoveries, delivering actionable alerts to subscribers before the broader market reacts — explore historic discovery returns or begin a 14-day free trial to position yourself ahead of the next major market move.