May 20, 2026

The Architecture of Vulnerability: Understanding the Iran War Impact on Oil Markets

Energy markets have always carried a hidden tension between their apparent global fluidity and their profound geographic fragility. For decades, analysts warned that the concentration of hydrocarbon production in a single geopolitical zone, connected to global consumers through a handful of maritime chokepoints, represented a systemic risk that statistical models consistently underpriced. The Iran war impact on oil markets has transformed that theoretical vulnerability into a live market reality, producing what many commodity analysts now describe as the most consequential oil price shock since the 1973 Arab Oil Embargo.

Understanding why this shock is different from previous Middle East crises requires moving beyond headline price data and examining the structural mechanics of how Gulf oil actually reaches global refiners, and what happens when those mechanics are interrupted.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Truly Irreplaceable

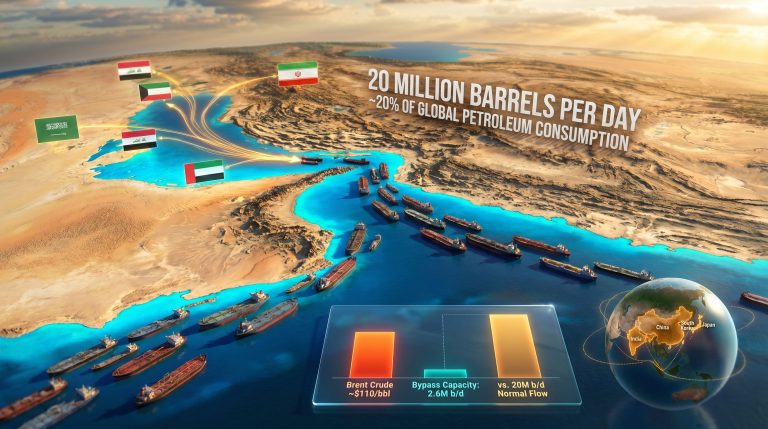

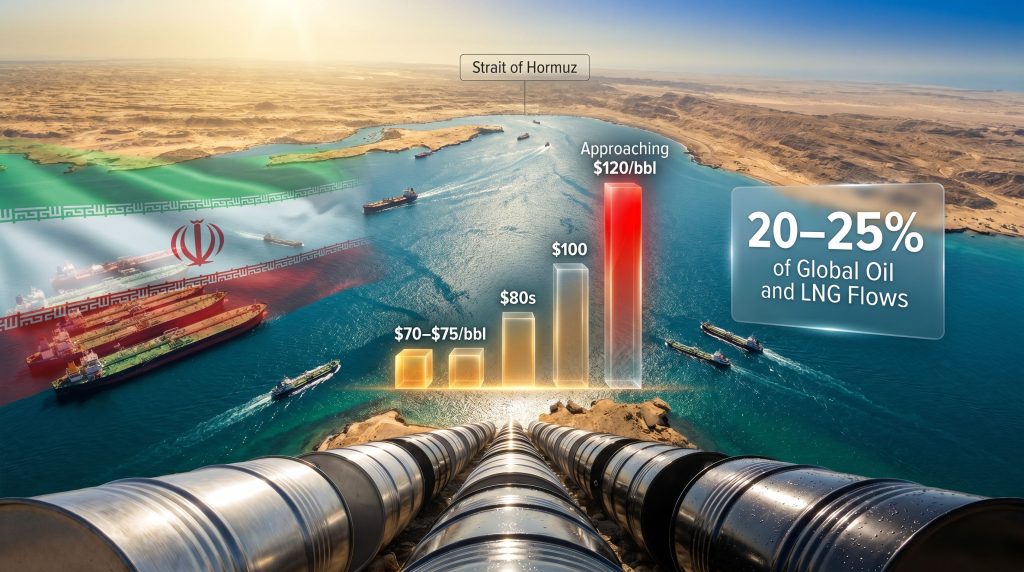

The Strait of Hormuz is a narrow maritime passage, approximately 21 miles wide at its narrowest navigable point, separating Iran from Oman and connecting the Persian Gulf to the Arabian Sea. Roughly 20 to 25 percent of global oil supply and a significant share of LNG shipments pass through this single corridor every day, making it the most concentrated energy chokepoint on earth.

What distinguishes the Strait from other strategic waterways is the absence of any credible alternative at comparable scale. While pipeline routes exist, including the East-West Pipeline across Saudi Arabia terminating at Yanbu on the Red Sea, and the Abu Dhabi Crude Oil Pipeline (ADCOP) to Fujairah, their combined capacity falls far short of replacing full Strait throughput. Saudi Arabia's Yanbu pipeline, for instance, has a rated capacity of around 5 million barrels per day, while total Strait flows have historically exceeded 18 to 21 million barrels per day. The arithmetic gap is decisive.

Geographic concentration compounds this problem. The world's largest oil reservoirs, including those of Saudi Arabia, Kuwait, Iraq, the UAE, and Qatar, all depend on Gulf export terminals that feed into Strait-dependent shipping lanes. When the corridor is disrupted, there is no geographic workaround that preserves volume, cost, and timeline simultaneously. Analysts at the Columbia Center on Global Energy Policy have long noted that the Strait's irreplaceability is precisely what makes it such a focal point of geopolitical risk.

How Oil Prices Have Responded: A Phased Analysis

The Iran war impact on oil markets has unfolded across distinct phases, each driven by different forces:

| Phase | Brent Crude Price Range | Primary Driver |

|---|---|---|

| Pre-conflict baseline | ~$70–$75/bbl | OPEC+ supply management |

| Initial conflict outbreak | $80s/bbl | Risk premium and shipping uncertainty |

| Strait disruption intensifies | Above $100/bbl | Physical supply constraint fears |

| Sustained conflict period | Approaching $120/bbl | Inventory drawdowns and rerouting costs |

The critical distinction in this price sequence is the transition from sentiment-driven to physically-constrained price elevation. Previous Middle East crises, including the 2019 Abqaiq drone attacks on Saudi Aramco infrastructure and the 2019–2020 Gulf tanker incidents, produced sharp but short-lived spikes because physical supply was never sustainably disrupted. This conflict has introduced a fundamentally different dynamic, one that reflects the broader patterns of crude oil geopolitics playing out across global energy markets.

Key Market Insight: When oil price increases reflect genuine volume losses rather than speculative positioning alone, the premium becomes structurally embedded. It cannot unwind until the physical supply pathway is restored. This is the central reason the current shock is more persistent than its predecessors.

Speculative positioning amplified the initial move. Traders rapidly repriced forward curves, options markets saw implied volatility surge, and risk-off hedging by airlines, shipping companies, and industrial consumers added further momentum. However, beneath the sentiment layer, actual volume constraints were simultaneously materialising.

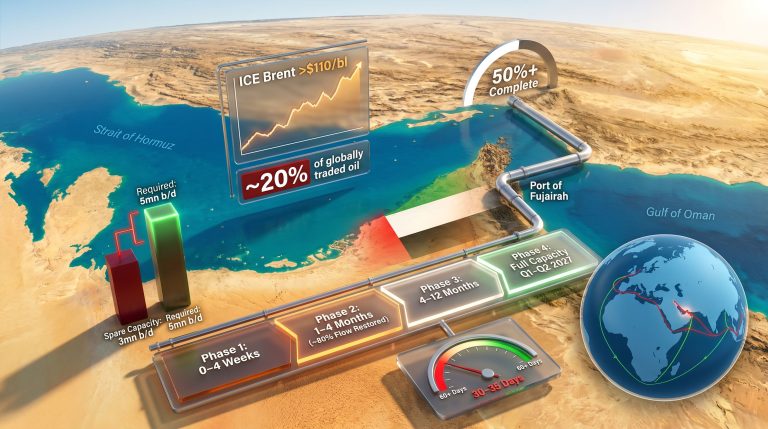

The Shuttle Tanker Workaround: Partial Solution, Real Limits

One of the less widely discussed operational developments emerging from the conflict is the improvised adoption of shuttle tanker systems to extract crude volumes from the Gulf under constrained conditions. Rather than full-size Very Large Crude Carriers (VLCCs) completing point-to-point voyages from Gulf terminals to Asian or European refineries, a staged system has evolved where smaller vessels shuttle crude to transfer points outside the most dangerous zones, where cargoes are then transshipped onto larger vessels for onward delivery.

This approach carries significant operational constraints:

- Shuttle tanker capacity is inherently lower than direct VLCC deployment, capping achievable throughput well below pre-conflict levels

- Transfer operations introduce additional time, cost, and logistical complexity at transshipment hubs

- Marine insurance underwriters have dramatically increased war risk premiums for Gulf-adjacent voyages, with some specialist insurers withdrawing coverage entirely for certain route segments

- The additional voyage legs extend delivery timelines, effectively reducing the number of cargo cycles achievable per vessel per quarter

The net effect is that while shuttle systems are providing genuine partial mitigation, they cannot replicate the volume efficiency of unimpeded Strait navigation. The workaround buys time; it does not solve the underlying supply equation.

Refiner Behaviour: Saudi Crude Falls Out of Favour

A revealing downstream consequence of the disruption has been the systematic reduction of Saudi crude intake by both Chinese and European refiners. This development reflects a convergence of factors beyond simple availability concerns.

Saudi crude exports, while not entirely halted, have become subject to elevated uncertainty around delivery reliability, voyage insurance costs, and scheduling predictability. Refiners operating complex facilities with tightly optimised feedstock schedules are acutely sensitive to supply unpredictability. When the cost and reliability calculus shifts, sophisticated refinery operators substitute away from uncertain supply sources even when those sources are not completely unavailable.

The competitive beneficiaries of this substitution include:

- U.S. WTI crude exported via Atlantic Basin routes, which faces no Strait of Hormuz exposure

- West African grades including Nigerian Bonny Light and Angolan Cabinda, which route via the Atlantic and Indian Oceans without Gulf transit dependency

- North Sea blends including Brent and Johan Sverdrup, which have seen renewed buying interest from European refiners seeking supply chain simplicity

- Russian crude continues to reach certain Asian buyers, particularly India, through alternative routing, though sanctions frameworks complicate this channel

This refiner substitution dynamic is accelerating a structural shift in crude trade flow architecture that analysts had previously expected to unfold over years, not months. Furthermore, the scale of this oil market disruption is prompting a fundamental reassessment of long-term supply strategies across the refining sector.

Asia-Pacific Exposure: The Highest-Stakes Import Region

The Iran war impact on oil markets falls most heavily on Asia-Pacific economies, which collectively represent the world's largest concentration of crude oil import demand and the greatest structural dependence on Gulf supply.

China's Complex Import Challenge

China presents the most complex case. As the world's largest crude importer, China sources a substantial share of its total import volumes from Gulf producers. Chinese refiners have demonstrated flexibility in diversifying supply, and China's strategic petroleum reserve (SPR) provides a meaningful buffer, but the scale of Chinese demand means that even partial Gulf disruption creates meaningful volume challenges that SPR deployment can only partially bridge.

Japan, South Korea, and India

Japan and South Korea face structural constraints that make rapid substitution more difficult. Both nations operate highly complex refinery systems optimised for specific crude grades, and their limited domestic production means all supply must be imported. Rerouting to Atlantic Basin crude involves longer voyage times and higher freight costs that directly erode refinery margin economics.

India occupies an interesting strategic position, balancing reduced Gulf crude availability against its continued access to discounted Russian crude through the shadow tanker fleet, though this channel carries its own reliability and sanctions-compliance risks.

Southeast Asia's Acute Vulnerability

Southeast Asian importers, including the Philippines, Thailand, and Vietnam, face the most acute consumer price pressure. These economies hold thinner strategic reserves, operate less complex import diversification networks, and have populations with higher energy cost sensitivity relative to income levels.

A compounding secondary shock has emerged from crude export restrictions imposed by select Asian producers, which has further tightened available supply for regional importers already facing reduced Gulf access. This cascading effect was not widely anticipated in pre-conflict supply security assessments.

The next major ASX story will hit our subscribers first

How Governments Are Responding

The IEA Strategic Reserve Release

The International Energy Agency coordinated a large-scale strategic petroleum reserve release among member nations, representing one of the most significant collective interventions in global oil markets since the 2022 response to Russia's invasion of Ukraine. Historical analysis of IEA reserve releases suggests they are effective at dampening price velocity rather than price level, providing a buffer that gives markets time to adjust without preventing the fundamental repricing that physical supply constraints ultimately impose.

The finite nature of strategic reserves introduces a critical time dependency. Most IEA member nations hold reserves calibrated to bridge disruptions measured in weeks to a few months. If the conflict extends into a multi-quarter disruption, reserve depletion becomes a secondary vulnerability rather than a solved problem.

U.S. Policy Considerations

The Trump administration has been evaluating several policy levers to address rising domestic gasoline prices, recognising the direct political sensitivity of pump price levels for American consumers. Options under consideration include accelerating domestic production incentives, examining export policy adjustments, and additional Strategic Petroleum Reserve deployment.

The administration's policy calculus is complicated by the fact that U.S. energy independence does not insulate domestic consumers from global Brent crude benchmark pricing, which feeds through to U.S. pump prices regardless of where the underlying oil was produced.

OPEC+ Strategic Positioning

OPEC's market influence has never been more closely scrutinised than during this conflict period. OPEC+ members outside the direct conflict zone, including Nigeria, the UAE, and to some extent Iraq, face an internal tension between capitalising on elevated prices through sustained production and risking demand destruction that ultimately reduces their long-term revenue.

Saudi Arabia's unique dual role, as both a partially disrupted exporter and a holder of meaningful spare production capacity, positions it as a critical swing variable in how this market shock ultimately resolves. Consequently, OPEC demand forecasts are being revised with considerably greater frequency than in previous disruption cycles.

Economic Contagion: Beyond the Oil Price Headline

| Sector | Transmission Mechanism | Severity of Impact |

|---|---|---|

| Consumer fuel costs | Direct pass-through at the pump | High and immediately visible |

| Aviation | Jet fuel cost surge and route economics | High and structurally damaging |

| Petrochemicals and fertilisers | Feedstock cost inflation into food prices | High with cascading effects |

| Shipping and freight | Bunker surcharges and rerouting costs | Medium-High embedded in goods prices |

| Emerging market currencies | Current account deterioration | High for energy importers |

| Advanced economy inflation | CPI energy component uplift | Medium partially offset by hedging |

The IMF's analytical framework for asymmetric commodity shocks highlights that sustained oil price elevation above $100 per barrel creates fundamentally different economic outcomes for energy exporters versus importers. For developing economies with limited hedging capacity and thin fiscal buffers, the second-round inflation effects, flowing through food prices, transport costs, and manufactured goods, can persist long after the initial price shock moderates. The IMF's energy trade analysis provides a detailed breakdown of these transmission mechanisms across affected regions.

Analytical Note: Demand destruction functions as an imperfect natural price ceiling. Historical elasticity data suggests meaningful demand response begins to emerge when prices sustain above $100 per barrel for multiple quarters, but this response arrives with a significant lag and causes economic damage in the process. It is a correction mechanism, not a protection mechanism.

Three Scenarios for Resolution

Scenario 1: Partial Normalisation (Base Case)

Shuttle tanker systems stabilise partial Strait flows. IEA reserve releases and OPEC+ spare capacity deployment prevent a full supply crisis. Brent consolidates in the $90 to $100 per barrel range. Global growth slows but avoids recession, and inflation remains elevated but manageable within central bank frameworks.

Scenario 2: Prolonged Blockade (Adverse Case)

The Strait remains effectively closed for six or more months. Global inventory drawdowns accelerate beyond strategic reserve capacity to compensate. Prices sustain above $120 per barrel, demand destruction becomes economically significant, and emerging market debt pressures intensify. Global recession probability rises materially.

Scenario 3: Rapid De-escalation (Optimistic Case)

Diplomatic resolution or ceasefire restores shipping confidence within 60 to 90 days. The risk premium rapidly unwinds, with Brent retracing toward $75 to $80 per barrel. Short-term economic damage is absorbed without lasting structural shifts in trade flow architecture.

The probability distribution across these scenarios is most sensitive to a single variable: whether the conflict escalates to include systematic attacks on tanker traffic or Gulf port infrastructure. Either development would sharply shift outcomes toward the adverse scenario regardless of reserve release or workaround efforts.

Long-Term Structural Consequences: A Rewired Global Oil Market

Perhaps the most underappreciated dimension of the Iran war impact on oil markets is the degree to which this crisis is accelerating structural changes that will persist well beyond any eventual ceasefire.

The tanker market is undergoing a rapid bifurcation into vessels willing to transit Gulf-adjacent waters at elevated war-risk insurance premiums, and those being permanently redeployed on alternative routes. This two-tier market structure, once established through commercial contracts and insurance frameworks, is slow to reverse even when geopolitical conditions improve.

Supply diversification strategies that major importers had planned to implement gradually over a decade are being compressed into emergency timelines. Investment in U.S. LNG export infrastructure has gained renewed urgency as a strategic hedge for Asian buyers seeking to reduce Gulf dependence. In addition, African and South American crude development projects are attracting accelerated financing interest from sovereign importers previously content with Gulf supply reliability.

The tension between short-term fossil fuel security investment and long-term decarbonisation commitments is being stress-tested in real time. Japan and South Korea, both signatories to ambitious net-zero frameworks, are simultaneously extending fossil fuel supply contracts and accelerating liquefied natural gas terminal investment, a pragmatic acknowledgment that energy security and energy transition are not always compatible on the same timeline.

Frequently Asked Questions

What makes the Strait of Hormuz so critical to global oil prices?

The Strait serves as the exit point for the majority of Gulf oil production, with approximately 20 to 25 percent of global oil and LNG flows transiting this single corridor. No alternative routing exists at comparable scale, making any sustained disruption immediately visible in global supply availability and pricing benchmarks.

Which economies face the greatest risk from the current disruption?

Asia-Pacific nations, particularly China, Japan, South Korea, India, and Southeast Asian importers, face the most acute exposure due to their high structural dependence on Gulf crude. Emerging market economies with limited hedging capacity and thin fiscal reserves face the most severe second-round economic impacts.

Can strategic petroleum reserves solve the supply problem?

Reserve releases are effective at moderating price velocity and providing short-term market stability, but they cannot permanently substitute for disrupted physical supply volumes. Their utility is time-limited by reserve capacity, which is typically calibrated for disruptions measured in weeks to a few months rather than multi-quarter conflicts.

How are U.S. consumers affected despite domestic energy production?

U.S. domestic crude production does not insulate American consumers from global oil price benchmarks. Brent crude pricing feeds directly into domestic refinery economics and retail gasoline pricing regardless of where the underlying oil was extracted, meaning global supply disruptions translate into U.S. pump price increases even when domestic production is at high levels.

Disclaimer: This article contains forward-looking scenario analysis and market commentary based on publicly available information as of the publication date. It does not constitute financial, investment, or trading advice. Oil market conditions are subject to rapid change, and readers should conduct independent research and seek professional guidance before making investment or commercial decisions based on energy market conditions.

Want to Stay Ahead of the Next Major Resource Discovery?

While oil market disruptions reshape global energy investment strategies, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries so subscribers can identify actionable opportunities before the broader market reacts — explore historic discoveries and their returns, or start your 14-day free trial today to gain a decisive market edge.