May 20, 2026

The Strait of Hormuz Crisis: A Framework for Understanding How Long Global Energy Recovery Will Take

The history of global energy markets is punctuated by moments when theoretical risk scenarios become operational realities. For decades, analysts modelled the consequences of a Hormuz closure as a stress-testing exercise, a worst-case scenario kept in the drawer alongside other low-probability, high-impact events. That calculation changed fundamentally when the US-Israel conflict with Iran moved from diplomatic tension to active military engagement. Consequently, ADNOC CEO sees long road back from war disruption as the world's most consequential energy corridor shut down, forcing every importing nation, trading company, and national oil producer to confront a vulnerability that had been quietly accumulating for years.

What makes the current situation categorically different from previous Gulf tensions is not simply the scale of the disruption, but its duration and structural complexity. Understanding the recovery timeline, and what it will actually take to restore full energy flows, requires a framework that goes well beyond counting barrels.

When big ASX news breaks, our subscribers know first

Why Routes Now Matter More Than Reserves

For most of the past century, energy security was measured in production volumes and reserve inventories. That paradigm is being decisively replaced. The defining insight emerging from the current crisis is that a nation's ability to physically move energy to market has become as strategically important as its ability to produce it in the first place.

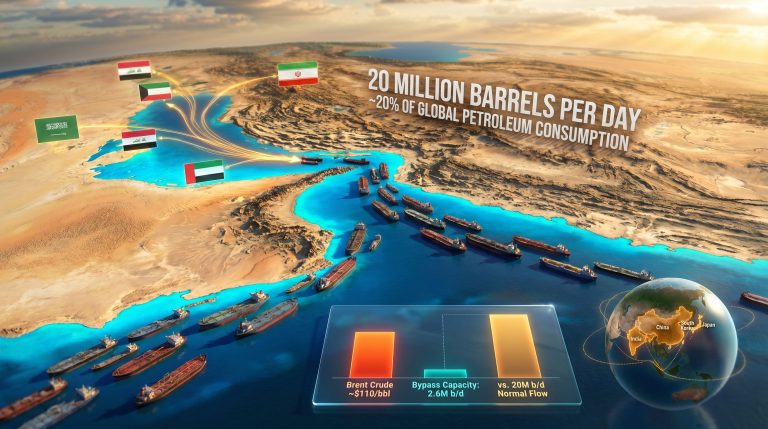

Approximately 20% of the world's traded oil and a substantial share of global LNG supply exports transit through the Strait of Hormuz annually. This single 33-kilometre-wide passage connects the Persian Gulf to the Gulf of Oman, and by extension to the rest of the world. When Iran effectively closed it, the disruption did not reduce the volume of oil sitting beneath Gulf sands by a single barrel. What it eliminated was the mechanism by which those barrels could reach consumers.

This distinction between supply disruption (reduced production volumes) and access disruption (compromised routes, elevated shipping insurance premiums, vessel repositioning delays) is critical because the two types of disruption require entirely different remedies. Production can, in principle, be restored relatively quickly by reopening shut-in wells. Route disruption, however, involves layers of institutional, logistical, and physical complexity that cannot be resolved by any single decision-maker.

Analytical Frame: Energy security in a conflict zone is no longer measured solely by barrels produced. It is now defined by the ability to move those barrels safely to market. This structural shift is fundamentally redefining how national oil companies, traders, and importing nations must plan.

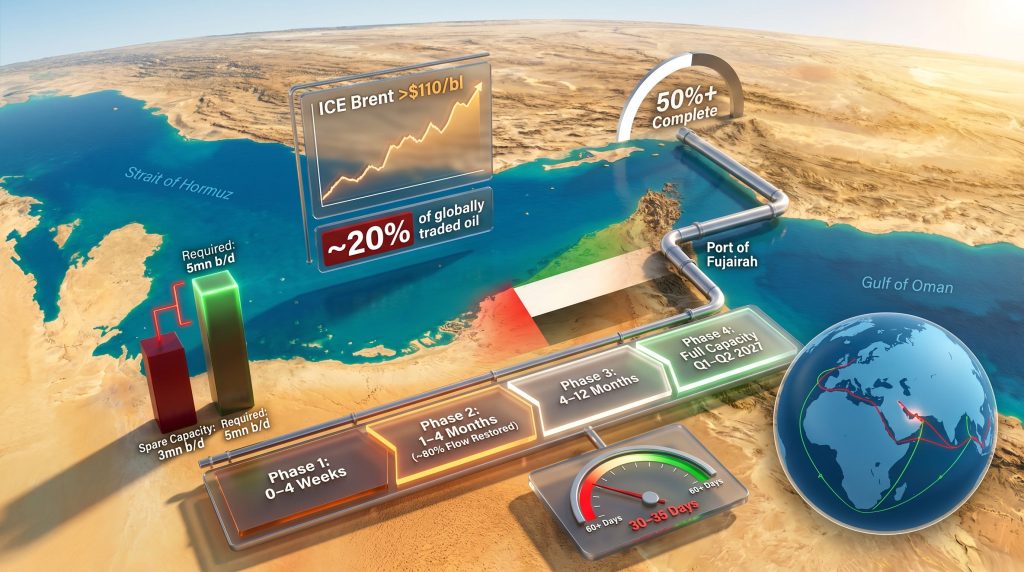

The Four-Phase Recovery Timeline: What Full Flow Restoration Actually Requires

ADNOC's chief executive Sultan al-Jaber, speaking at an Atlantic Council event in May 2026, offered perhaps the most authoritative assessment of the recovery timeline available. His analysis, drawn from direct operational experience managing one of the world's largest state oil companies under active conflict conditions, points to a recovery arc that markets may be significantly underpricing. Indeed, as reported by Arabian Business, al-Jaber explicitly warned that Hormuz disruption represents global economic extortion hitting prices worldwide.

| Recovery Phase | Estimated Timeframe | Key Milestones |

|---|---|---|

| Phase 1: Immediate Stabilisation | 0–4 weeks post-ceasefire | Ceasefire agreement, initial shipping lane assessment |

| Phase 2: Partial Flow Restoration | 1–4 months post-ceasefire | Approximately 80% of pre-conflict flow volumes restored |

| Phase 3: Infrastructure Rehabilitation | 4–12 months | Damaged facilities assessed and repaired on a case-by-case basis |

| Phase 4: Full Operational Capacity | Q1–Q2 2027 | Complete restoration of pre-conflict energy flow levels |

Even under an optimistic scenario where conflict cessation occurs imminently, restoring approximately 80% of pre-conflict flows will take a minimum of four months. Full restoration is not expected before the first or second quarter of 2027.

Why the Timeline Cannot Be Compressed

The four-month minimum for partial recovery is not arbitrary. It reflects the compounding delays inherent in restarting a complex, multi-actor energy system simultaneously:

- Shipping lane clearance and security assessment requires coordination between naval forces, maritime authorities, and commercial operators before tankers can safely transit

- War risk insurance reinstatement is a market-driven process that typically lags diplomatic developments by weeks or months, as underwriters reassess risk premiums and exposure limits

- Vessel repositioning involves redeploying tankers that have been diverted to alternative routes, a logistical exercise that takes time even once routes are confirmed clear

- Upstream restart sequencing cannot be accelerated beyond engineering constraints, with some assets requiring weeks and others requiring months depending on the nature and extent of damage

For context, the 1980s tanker war in the Gulf, which was considerably less intensive than the current conflict in terms of infrastructure targeting, took multiple months to fully unwind even after diplomatic progress. The current disruption involves more extensive damage to physical facilities, making the 2027 full-recovery horizon a realistic, rather than pessimistic, projection.

The UAE's Infrastructure Challenge: Damage Assessment and the Fujairah Bypass

The UAE has absorbed a disproportionate share of Iranian attacks over the approximately two and a half months since the conflict began. ADNOC's leadership has publicly acknowledged damage to infrastructure and facilities, whilst noting that comprehensive damage assessments remain ongoing.

The operational distinction between recoverable damage (pipelines, processing equipment, terminal infrastructure) and structural vulnerabilities (long-term route dependency, workforce disruption, contractor availability) is important here. Recoverable damage has defined timelines, even if those timelines are uncertain. Structural vulnerabilities, however, are more insidious because they reshape the risk calculus for future investment and operational planning.

The Fujairah Pipeline: Bypass Architecture Under Wartime Urgency

One of the most strategically significant developments to emerge from the conflict is the accelerated construction of a crude pipeline connecting UAE production assets to the Port of Fujairah, situated on the Gulf of Oman outside the Strait of Hormuz. As of mid-2026, construction was reported to be more than 50% complete.

The strategic logic is straightforward: Fujairah provides an export pathway that bypasses Hormuz entirely. The Abu Dhabi Crude Oil Pipeline (ADCOP), which has been operational since 2012, already provides a partial bypass route with a capacity of approximately 1.5 million b/d. What the new pipeline represents is a permanent expansion of that bypass architecture, reflecting a fundamental rethinking of Gulf export infrastructure under conditions of wartime urgency.

What distinguishes the current construction push from previous capacity planning is the driver: projects that were theoretically justified for years are now being executed against an active threat environment, compressing timelines and elevating political priority in ways that peacetime project management could not.

Global Energy Buffers Are Dangerously Thin: The Underinvestment Problem by the Numbers

The Hormuz disruption has exposed a structural fragility that predates the current conflict by years. Furthermore, the global energy system has been operating with inadequate buffers across three critical dimensions simultaneously.

| Metric | Current Level | Required Level | Gap |

|---|---|---|---|

| Annual upstream investment | ~$400 billion/year | Sufficient to grow capacity | Barely offsetting natural decline |

| Global spare production capacity | ~3 million b/d | ~5 million b/d | ~2 million b/d shortfall |

| Effective inventory cover | ~30–35 days | 60+ days (minimum) | ~25–30 days |

Al-Jaber's assessment of these figures at the Atlantic Council is notable for its precision and frankness. Annual upstream investment of around $400 billion is barely sufficient to offset natural production decline rates in existing fields, meaning the industry is running on a treadmill — spending heavily just to maintain current output levels, with minimal capacity being added to provide shock absorption.

Global spare production capacity of approximately 3 million b/d is well below the roughly 5 million b/d threshold considered adequate for absorbing a major supply disruption. The current conflict has demonstrated conclusively that this buffer is insufficient for a Hormuz-scale event. In addition, the broader oil price shock dynamics this has unleashed are reshaping producer economics across the entire industry.

The 30–35 days of effective global inventory cover is perhaps the most alarming figure. During the 1990–91 Gulf War, the IEA's strategic petroleum reserve mechanism was activated for the first time, coordinating a release of emergency stocks that helped stabilise markets. That system was designed for a different era of demand levels and supply geography. A prolonged Hormuz closure tests the system in ways it was not originally engineered to handle.

What Restoring Adequate Buffers Would Actually Require

The argument for rebuilding upstream investment, spare capacity, and inventory cover is not simply about the current crisis. It is about the structural resilience of a system that will need to supply more than 100 million barrels per day of demand well into the 2040s, according to ADNOC's own demand forecasting. Achieving adequate buffers would require:

- Sustained upstream investment growth above the current $400 billion baseline to generate genuine capacity additions rather than just decline-rate offsets

- Coordinated OPEC and non-OPEC capacity expansion targeting a minimum spare capacity buffer of 5 million b/d

- A doubling of effective strategic inventory cover from the current 30–35 day level, requiring both physical storage expansion and coordinated release frameworks

These are medium-term imperatives, not aspirational long-term objectives. The current crisis has made that distinction impossible to ignore.

How Major Importers Are Adapting in Real Time

Japan: Alternative Procurement and Operational Resilience

Japan's response to the Hormuz closure offers one of the most instructive case studies in adaptive energy procurement. Despite the effective closure of the strait, Japanese refineries achieved an average run rate of 76% in the week to 16 May 2026, above the monthly average range of 61.7–75.9% recorded across May periods from 2021 to 2025. Crude throughput reached 2.36 million b/d, up 3.8% week-on-week, according to data from the Petroleum Association of Japan.

Japan's procurement diversification has been rapid and pragmatic:

- US crude has become one of the primary alternative supply sources, reflecting the growing role of American production in Asian energy markets

- Latin American sources including Mexico, Ecuador, and Venezuela are under active consideration, with at least one Japanese refiner pursuing Alaskan crude procurement

- Sanctions-exempt Russian crude imports continue to provide a partial supply buffer for some Japanese buyers

- National strategic petroleum reserves are being actively deployed to bridge supply gaps whilst alternative procurement routes are established

The Japanese government has also implemented a retail fuel subsidy programme targeting a nationwide average gasoline price cap of approximately ¥170/litre (around $1.06/litre). As of 18 May 2026, subsidised retail gasoline prices averaged ¥169.2/litre. The gasoline subsidy for the week of 21–27 May was set at ¥41.80/litre, with equivalent subsidies applied to gasoil, kerosine, and fuel oil, and a 40% equivalent applied to jet fuel.

Norway: The Strategic Reserve Anomaly

A less-discussed but strategically significant development is Norway's parliamentary debate over fuel stockholding policy. Norway's parliament, the Storting, was scheduled to debate in May 2026 a proposal to expand the country's diesel and jet fuel strategic reserves from 20 days to 90 days of consumption coverage.

Norway occupies an unusual position in global energy security architecture: as Europe's largest oil exporter, it has no IEA stockholding obligation under its membership terms, making it the only country outside North America without one. This anomaly, previously of academic interest, has become a live policy vulnerability as the Hormuz disruption amplifies European energy security concerns.

The country's sole domestic refining asset, the 203,000 b/d Mongstad refinery operated by Equinor, provides limited domestic processing capacity relative to national consumption requirements. A March 2026 report from the Norwegian Defence Research Institute flagged strategic fuel stocks as a national security priority, directly informing the parliamentary debate. The energy and environment committee's recommendation specifically noted logistics concerns in Norway's northern regions, where military activity would be most intensive in a high-tension scenario.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways for Hormuz and Global Energy Markets

Scenario 1: Diplomatic Resolution Within 3–6 Months

This scenario requires a durable ceasefire, credible US-Iran negotiations, and shipping lane security guarantees acceptable to commercial operators and their insurers. Under this pathway, partial flow recovery is achievable by late 2026, with price normalisation beginning as market confidence in route security is restored. Residual risks include infrastructure repair backlogs, insurance market recalibration delays, and a persistent trust deficit among vessel operators and cargo owners.

Scenario 2: Prolonged Stalemate (6–18 Months)

The consequences of extended disruption are already visible in commodity markets. Ice Brent front-month futures were trading above $110/barrel as of May 2026, more than 50% above pre-conflict levels from before the initial strikes on 28 February. The resulting commodity market volatility has created cascading challenges for hedging strategies across multiple asset classes. A prolonged stalemate would likely sustain this price environment whilst:

- Accelerating investment in alternative routing infrastructure across the Gulf region

- Triggering meaningful demand destruction in price-sensitive emerging market economies, particularly in South and Southeast Asia

- Permanently shifting crude procurement strategies for major Asian importers toward Atlantic Basin and Pacific Rim supply sources

- Increasing the strategic market share of US, Latin American, and Alaskan crude in Asian refinery slates

Scenario 3: Permanent Loss of Free Navigation Through Hormuz

This represents the catastrophic tail risk that market pricing has not yet fully internalised. A world in which freedom of navigation through Hormuz is not restored would require a fundamental restructuring of global energy trade architecture at enormous cost. Furthermore, it would set a precedent that would have cascading implications for other strategically critical waterways globally.

Critical Warning: The principle of freedom of navigation through international straits is foundational to the global trading system. A precedent-setting failure to defend this principle in Hormuz would create a decade-long strategic liability for the global energy system and invite similar coercive behaviour at other chokepoints.

As al-Jaber stated plainly at the Atlantic Council: if Iran retains effective control of Hormuz, freedom of navigation as a principle is finished. The geopolitical stakes extend well beyond crude oil pricing.

ADNOC's OPEC Exit: Reading the Signal Correctly

The UAE's decision to exit OPEC should be interpreted in the context of everything described above. The departure was framed not as a rejection of the cartel's principles but as a forward-looking repositioning toward supply flexibility in a world that will require substantially more energy, not less.

ADNOC's leadership has been explicit that global oil demand is expected to remain well above 100 million barrels per day into the 2040s. In that context, operating under production quota constraints during a period of wartime supply disruption and structural underinvestment would represent a strategic misalignment. The exit positions the UAE to serve as a genuine swing supplier in a post-conflict recovery scenario, contributing to the spare capacity rebuild that al-Jaber himself has identified as a global priority.

For OPEC oil market influence more broadly, the UAE's departure raises serious questions about the cartel's ability to manage markets through geopolitical disruptions when member incentives diverge significantly from collective quota targets.

The Chokepoint Coercion Problem and What It Means for Energy Security Doctrine

One of the less-discussed but most consequential dimensions of the current crisis is the concept of energy infrastructure attacks as instruments of strategic coercion rather than purely military objectives. When energy chokepoints are targeted in ways that inflict economic harm on nations far removed from the immediate conflict, the legal and strategic frameworks governing state responses require urgent recalibration.

The United Nations Convention on the Law of the Sea (UNCLOS) establishes the right of transit passage through international straits. The practical question of how that right is enforced when a state actor chooses to contest it militarily remains unresolved in international law and policy. The Hormuz precedent will shape how the international community responds to future chokepoint coercion events, whether in the Strait of Malacca, the Bab-el-Mandeb, or the Turkish Straits.

For investors, however, the implications are structural rather than cyclical. A world in which chokepoint coercion is a viable geopolitical tool permanently reprices energy security risk, elevates the value of bypass infrastructure and domestic refining capacity, and strengthens the investment case for supply diversification across every dimension of the global energy system. The broader geopolitical risk landscape for resource investment has consequently been fundamentally altered by these developments.

Key Takeaways: What the Hormuz Crisis Reveals About Global Energy Vulnerability

- Recovery timelines are longer than markets typically price in, with full flow restoration to pre-conflict levels requiring infrastructure repair, route rehabilitation, and diplomatic normalisation working in parallel — pointing to a Q1–Q2 2027 horizon at the earliest

- The world's energy buffer systems are structurally inadequate, with 30–35 days of inventory cover and 3 million b/d of spare capacity proving insufficient for a disruption of this scale and duration

- Bypass infrastructure investment is accelerating, with the Fujairah pipeline and similar projects representing a permanent architectural shift in Gulf export strategy rather than a temporary wartime measure

- Energy security is now defined by routes, not just reserves, with the ability to move energy safely to market now as strategically important as the ability to produce it

- The underinvestment problem requires urgent attention, as restoring global spare capacity to 5 million b/d and doubling effective inventory cover are medium-term operational requirements

- Freedom of navigation is a global economic interest, with the Hormuz precedent carrying implications for international maritime security doctrine that extend far beyond crude oil pricing. In this context, ADNOC CEO sees long road back from war disruption as a defining challenge for the entire global energy architecture in the years ahead

Disclaimer: This article contains forward-looking statements, scenario projections, and analysis based on publicly available information current as of May 2026. Energy market conditions, geopolitical developments, and recovery timelines are subject to rapid change. Nothing in this article constitutes financial or investment advice. Readers should conduct their own independent research and consult qualified advisers before making any investment decisions.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Energy Disruptions?

The Hormuz crisis is reshaping commodity markets, accelerating bypass infrastructure investment, and permanently repricing energy security risk — creating significant opportunities for investors who can identify high-potential resource discoveries quickly. Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex commodity data into actionable insights, so subscribers can capitalise on emerging opportunities before the broader market reacts — start your 14-day free trial today, or explore historic discovery returns to understand just how transformative early-mover positioning can be.