July 28, 2026

The Hidden Architecture of the Iranian Oil Sanctions Waiver

Global oil markets have spent decades developing a sophisticated immunity to geopolitical disruption. Supply shocks, sanctions regimes, and diplomatic pivots are absorbed with increasing efficiency as markets evolve better hedging instruments and diversified supply networks. Yet every so often, a policy decision arrives that defies easy categorisation — one that simultaneously functions as a diplomatic instrument, a market stabilisation tool, and a structural inflection point. The Iranian oil sanctions waiver issued in mid-2026 is precisely that kind of event, and understanding what it can realistically deliver requires looking well beyond the headline.

When big ASX news breaks, our subscribers know first

What the Iranian Oil Sanctions Waiver Actually Authorises

The U.S. Treasury's Office of Foreign Assets Control issued a temporary general license on 17 June 2026, authorising the purchase, transport, and importation of Iranian crude oil, petroleum products, and petrochemicals by any buyer globally, including U.S.-domiciled firms, effective through 21 August 2026. The legal architecture of this instrument is distinct from prior relief measures: it is a unilateral executive action rather than a multilateral treaty obligation, operating within the framework of a 60-day Memorandum of Understanding signed between Washington and Tehran following diplomatic engagement in Switzerland.

Critically, the waiver does not represent a blanket normalisation of Iran's sanctions status. Restrictions remain active for transactions involving:

- North Korea

- Cuba

- Russian-occupied Ukrainian territories

- Any entities already in breach of separate U.S. sanctions regimes

This selectivity is deliberate. Washington has calibrated the instrument to release supply pressure without permanently restructuring Iran's geopolitical standing under U.S. foreign policy — a distinction that has profound implications for how much Iranian crude can realistically re-enter the market within the 60-day window. Furthermore, sanctions on oil trading across multiple regimes continue to shape the broader environment in which this waiver operates.

The Strait of Hormuz and the $150 Barrel Scenario That Forced Washington's Hand

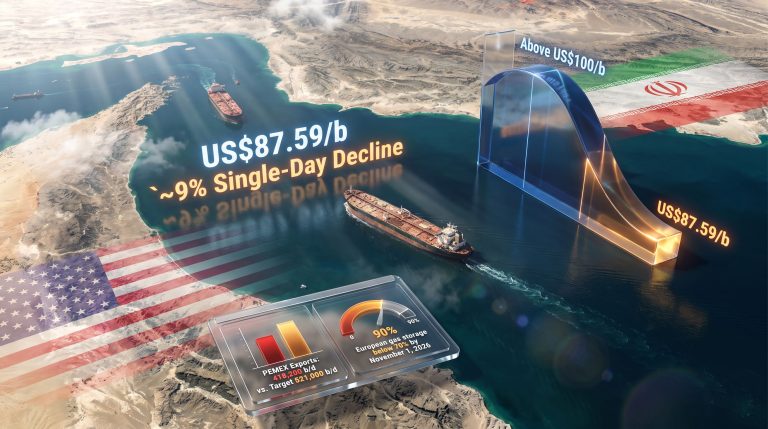

To understand why this waiver exists, it is necessary to trace the supply shock that preceded it. The closure of the Strait of Hormuz — a chokepoint through which roughly 20% of global oil supply transits daily — created an acute vulnerability across import-dependent nations. Finance ministers from approximately 10 countries formally requested sanctions relief, warning that unchecked supply restriction risked pushing prices toward $150 per barrel, a level that would have cascading recessionary effects across multiple economies.

At the time of the waiver announcement, ICE Brent crude was trading in the $77 to $78 per barrel range. Rather than collapsing on the news, prices held relatively firm, suggesting the market was interpreting the waiver not as a supply surge but as a ceiling on upside risk. This is a critical distinction for investors and analysts trying to understand what the waiver actually means for crude pricing dynamics, particularly when viewed alongside broader crude price geopolitics.

The 60-day window was not chosen arbitrarily. It maps directly onto the transitional ceasefire period between the U.S. and Iran, preserving Washington's negotiating leverage while providing short-term supply certainty to allies. The fixed expiry also prevents Iranian crude from being permanently repriced as a freely tradeable commodity, which would have structural implications for OPEC+ discipline.

Iranian Crude: The Price Mechanics Behind the Discount

Iran Heavy crude was recently benchmarked at approximately $64.96 per barrel, representing a discount of roughly $12 to $13 per barrel relative to Brent. This discount exists because Iranian crude carries a sanctions risk premium that non-Chinese buyers must price into any transaction, covering legal review costs, insurance arrangements, and the reputational exposure of handling sanctioned material even under a temporary general license.

| Metric | Estimated Figure |

|---|---|

| Iran Heavy crude benchmark | ~$64.96/barrel |

| Brent crude at waiver announcement | $77–$78/barrel |

| Approximate discount to Brent | ~$12–$13/barrel |

| Waiver duration | 60 days (to 21 August 2026) |

| Nations requesting sanctions relief | ~10 countries |

| Hormuz daily transit share of global supply | ~20% |

| Oil price risk cited without waiver | Up to $150/barrel |

| Saudi crude exports, April 2026 | 3.99 million b/d (record low) |

| Iraq southern oilfield ramp-up | ~2.1 million b/d |

The discount structure raises a question that market participants are actively debating: if the waiver technically opens Iranian crude to all buyers, does that discount compress as competitive pressure normalises? Historically, the answer depends on how many refiners outside China's independent processing sector — known as teapot refineries — can operationally absorb Iranian barrels within the 60-day constraint.

Why Non-Chinese Buyers Face Structural Barriers

The gap between policy authorisation and operational readiness is arguably the most underappreciated dimension of the current Iranian oil sanctions waiver. Western refiners in Europe, South Asia, and the Americas cannot simply flip a switch and begin importing Iranian crude because a temporary licence permits it. The friction points are numerous and compounding:

- Legal compliance review — Corporations operating within Western financial systems require formal legal sign-off before engaging in transactions that, until days earlier, carried criminal penalties.

- Insurance market limitations — Iranian crude has historically moved via a shadow fleet that operates outside conventional marine insurance markets. Western buyers seeking to operate within the licence's stated boundaries cannot easily access this infrastructure.

- Refinery configuration — Iranian Heavy crude requires specific refinery configurations capable of processing sour, high-sulphur crude. Not all Western refineries are equipped for this without operational adjustment.

- Time constraint — Assembling the compliance infrastructure, insurance arrangements, and logistics for a single Iranian cargo within a 60-day window is operationally unrealistic for most non-Asian buyers.

This structural mismatch explains why Brent has not collapsed following the waiver announcement. Markets correctly understand that the volume of Iranian crude capable of re-entering the market within this timeframe is substantially constrained by operational reality rather than legal permission. Indeed, oil market trade risks arising from geopolitical realignment continue to introduce additional layers of uncertainty that Western buyers must navigate.

Saudi Arabia's Strategic Silence and the OPEC+ Wild Card

A dimension that deserves closer attention is Saudi Arabia's concurrent behaviour. Saudi crude exports fell to a record low of 3.99 million barrels per day in April 2026, down nearly 1 million b/d from the prior month, according to JODI data. This compression of the kingdom's export volumes reduces the supply cushion that would otherwise absorb Iranian re-entry, effectively preventing a price collapse regardless of how much Iranian crude flows.

Whether this is strategic coordination or coincidental production management remains an open question. What is clear is that Iran's participation in the global oil market under this waiver introduces a non-quota supply variable into the OPEC+ framework, since Tehran retains full discretion over its export volumes and pricing strategy during the 60-day period. OPEC's market influence over pricing discipline is consequently more difficult to enforce when a major producer operates outside quota constraints.

Iraq's response adds a further layer of complexity. Southern oilfield output ramped to approximately 2.1 million barrels per day in anticipation of a Hormuz reopening, introducing a competing source of incremental supply that partially offsets whatever Iranian volumes materialise. In addition, OPEC demand forecasts remain a closely watched signal for how the alliance is interpreting near-term consumption trends against this shifting supply backdrop.

The next major ASX story will hit our subscribers first

How Asian Markets Are Responding

China's Structural Advantage

China's position in the Iranian crude market is structurally unique. Throughout the sanctions period, independent Chinese refiners absorbed discounted Iranian barrels outside Western financial systems, giving Beijing a de facto pricing advantage. The waiver theoretically erodes this competitive edge by broadening buyer eligibility, though operational constraints limit real-world competition for Iranian barrels in the near term.

China is simultaneously expanding its LNG import infrastructure, with the PipeChina-operated Longkou LNG terminal in Shandong province preparing to receive Arctic LNG 2 supplies. This signals that Beijing is diversifying its energy import architecture independent of Iranian waiver dynamics.

India's Deliberate Diversification

India's response is instructive in a different way. Despite the partial Hormuz reopening, Indian refiners are not rushing back to Middle Eastern suppliers. India received its first post-deal LNG cargo through Hormuz while simultaneously importing a record 1.1 million tonnes of LPG from the United States in June.

This deliberate diversification reflects a structural shift in Indian energy procurement strategy. The supply crisis appears to have accelerated India's move toward longer-term source diversification rather than reverting to pre-crisis procurement patterns. India has also ordered a major expansion of its strategic petroleum reserves, suggesting policymakers are treating the Hormuz episode as a permanent calibration point rather than a temporary disruption.

The August 21 Cliff and Its Implications for Crude Volatility

Markets typically begin pricing policy expiry events approximately two to three weeks in advance of the actual date. With the Iranian oil sanctions waiver set to expire on 21 August 2026, crude markets face an embedded volatility trigger in the final weeks of July and early August.

According to reporting by S&P Global, the U.S. simultaneously allowed the Russian oil sanctions waiver to lapse, adding further complexity to the global supply picture as the August deadline approaches.

The scenario tree from here branches in three principal directions:

- Diplomatic extension — U.S.-Iran talks produce a durable framework, the waiver is extended or replaced by a more permanent arrangement, and Iranian crude remains accessible to global buyers.

- Managed expiry — Talks conclude without a permanent deal but both parties allow the waiver to lapse quietly, reverting to prior sanctions enforcement without a dramatic market event.

- Abrupt termination — Diplomatic talks collapse, the waiver expires with Iranian supply abruptly removed from the market, potentially triggering a rapid upward price correction, particularly if Hormuz transit remains constrained.

The Trump administration has previously demonstrated capacity for rapid policy reversal on sanctions matters, having signalled opposition to renewal before reversing that position under international pressure. This creates a binary risk structure that sophisticated energy traders are already managing through options positioning.

A Compound Risk Environment: El Niño and Concurrent Commodity Pressures

The Iranian waiver does not operate in isolation. Equatorial Pacific Ocean temperatures are currently running 1.7 degrees Celsius above the 30-year average for June, representing the largest temperature deviation for the month since 1981 according to Bloomberg reporting. This configuration is consistent with the development of a severe El Niño event, potentially exceeding the 2023–2024 cycle that caused cocoa prices to triple and drove 10 to 15 per cent increases across wheat, corn, sugar, rice, and coffee markets.

A concurrent commodity shock environment would dramatically amplify the consequences of any Iranian waiver termination. Energy markets absorbing a sudden supply removal would simultaneously face food commodity inflation pressures, creating a multi-vector inflation scenario that central banks are poorly positioned to address through conventional rate policy.

Other live risk factors compounding the waiver's fragility include:

- Qatar's Ras Laffan gas facility blaze, which has debilitated approximately 1.4 BCf/d of capacity, equivalent to roughly 8% of Qatar's total gas supply

- Ongoing Israeli-Hezbollah ceasefire fragility, which introduces Middle Eastern geopolitical volatility independent of U.S.-Iran dynamics

- Ukraine's drone strikes on Russian fuel infrastructure, contributing to Crimean fuel shortages and retail sale restrictions across multiple Russian regions

- European Rhine water levels expected to fall to approximately 33 inches due to heatwave conditions, impeding intra-continental fuel logistics

Sanctions Waiver vs. Permanent Removal: The Policy Spectrum

Understanding the current instrument requires placing it within the broader spectrum of available policy tools.

| Policy Instrument | Duration | Buyer Eligibility | Volume Impact | Price Effect |

|---|---|---|---|---|

| Temporary General Licence (current) | 60 days | All buyers including U.S. firms | Constrained by logistics | Moderate downward pressure |

| Targeted Humanitarian Waiver | Ongoing | Food/medicine only | Negligible | Minimal |

| Full Sanctions Removal | Permanent | Universal | Potentially 1–2 million b/d incremental | Significant downward pressure |

| Snapback Sanctions | Immediate | Prohibited entirely | Zero | Sharp upward spike |

Full sanctions removal would require Congressional engagement and treaty architecture comparable to the original JCPOA framework, which remains politically contentious regardless of executive branch posture. However, the current instrument sits deliberately between humanitarian carve-outs and full normalisation, providing market relief without crossing the political threshold that formal removal would require.

What This Means for Energy Market Positioning

For investors and market participants, the Iranian oil sanctions waiver presents a specific risk-reward calculus. The waiver has functioned primarily as a risk ceiling on crude prices rather than a downward price catalyst, given the structural barriers preventing meaningful volume increases from non-Chinese buyers. Consequently, the key variables to monitor as 21 August approaches include:

- Progression of U.S.-Iran diplomatic talks in Switzerland

- Saudi Arabia's export volume decisions in July and August

- Iranian crude export data as a proxy for actual waiver utilisation

- Asian refinery procurement patterns as indicators of real buying interest

- El Niño development data from NOAA for concurrent commodity risk calibration

This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. Energy market forecasts involve inherent uncertainty and should not be relied upon as the sole basis for investment decisions. Past price behaviour is not indicative of future results.

Want to Stay Ahead of Major ASX Resource Discoveries Shaping Energy Markets?

As geopolitical events like Iranian oil sanctions waivers reshape commodity markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex market signals into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.