July 13, 2026

When a Chokepoint Becomes a Crisis: The Structural Logic Behind Iraq's Export Collapse

Every major oil-producing nation carries some degree of export route risk, but most have quietly diversified their corridors over decades of infrastructure investment. Iraq never did. The country's entire economic architecture was built around a single maritime passage, and when that passage came under sustained pressure following the onset of the U.S./Israel-Iran conflict in February 2026, the consequences were not merely disruptive. They were existential.

Understanding why Iraq finds itself in this position requires looking past the immediate crisis and examining the decades of strategic decisions, political disputes, and infrastructure neglect that made single-corridor dependency not just possible, but seemingly permanent. The current scramble to develop alternative Iraq oil export routes is not simply a logistics problem. It is a reckoning with choices made across multiple governments, superpower relationships, and unresolved internal conflicts.

When big ASX news breaks, our subscribers know first

The Numbers Behind the Collapse

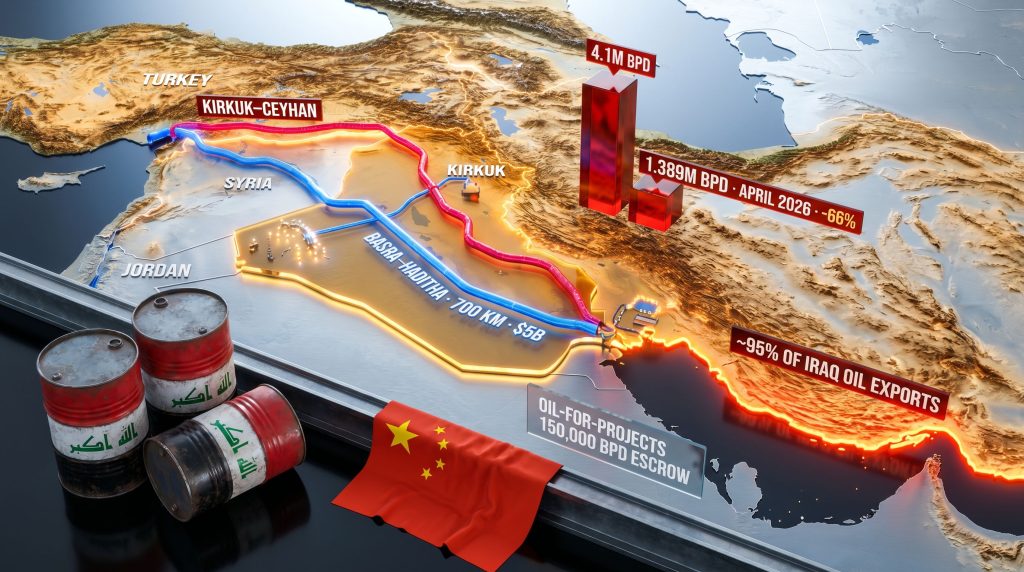

The scale of Iraq's production implosion during April 2026 was unlike anything seen in the country since the chaotic aftermath of the 2003 U.S.-led invasion. Output averaged just 1.389 million barrels per day (bpd) across the month, compared with a long-run monthly average of approximately 3.47 million bpd recorded between January 2002 and March 2026, and a pre-disruption average exceeding 4.1 million bpd in the three months immediately before the conflict began, according to reporting by OilPrice.com.

That represents a production decline of roughly 66% from recent peak levels, compressing Iraq's output to volumes last seen during active wartime. The fiscal implications are severe by any standard, but Iraq's structural dependency on oil revenue makes them catastrophic. Furthermore, these oil price movements have reverberated far beyond Iraq's borders, affecting global markets and trade relationships alike.

| Metric | Value |

|---|---|

| Average monthly production (Jan 2002 to Mar 2026) | ~3.47 million bpd |

| Pre-disruption average (3 months prior) | ~4.1 million bpd |

| April 2026 average production | ~1.389 million bpd |

| Approximate production decline from peak | ~66% |

| Oil's share of annual budget revenue | >90% |

| Share of exports previously routed via Hormuz | ~95% |

| Basra–Haditha pipeline cost estimate | US$5 billion |

| Kirkuk–Nineveh design capacity | 350,000 bpd |

| Oil-for-Projects daily escrow allocation | 150,000 bpd |

When roughly 95% of monetised crude must pass through the Strait of Hormuz before generating any government income, a sustained closure does not create a budget shortfall. It eliminates the budget's operating foundation entirely.

The Mechanics of a Production Shutdown

Why Can't Iraq Simply Store the Oil?

A detail that often escapes mainstream coverage is precisely why Iraq cannot simply store the oil it cannot export and resume full production once routes reopen. The answer lies in the physical constraints of upstream infrastructure.

Once Iraq's domestic storage facilities reach maximum tank farm capacity, crude production must be halted at the wellhead. There is no economic or physical alternative. The deeper problem is what happens to the wells themselves during extended shut-in periods, particularly in Iraq's mature southern fields.

The damage mechanisms are well understood in petroleum engineering:

- Reservoir pressure depletion: Shut-in wells lose formation pressure over time, reducing the natural drive that brings crude to surface without artificial lift

- Water infiltration: As pressure drops, adjacent aquifer water can migrate into the reservoir, permanently diluting producible oil saturation

- Casing and tubing corrosion: Idle wells exposed to hydrogen sulphide and formation brines experience accelerated metal degradation

- Sand migration and plugging: Low-flow or zero-flow conditions allow fine formation material to settle in perforations, reducing future injectivity and productivity

Iraq's largest southern fields, many of which were developed decades ago under Soviet-era and pre-sanctions engineering practices, are disproportionately vulnerable to these failure modes. A prolonged shutdown does not merely pause production. It may permanently impair the reservoir's long-term deliverability, transforming a temporary geopolitical disruption into a structural production capacity problem with a multi-year recovery timeline.

Iraq's Export Route Map: What Actually Exists

The urgency to identify functional Iraq oil export routes has forced Baghdad to confront an uncomfortable reality: the country's alternative infrastructure is fragmented, politically complicated, and vastly insufficient to compensate for the lost Hormuz corridor. In addition, the geopolitical oil price factors at play here extend well beyond simple supply disruption, touching on regional power dynamics and long-standing territorial disputes.

The Basra Terminal Complex

Iraq's primary export infrastructure centres on the Basra Oil Terminal and the Khor al-Amaya Terminal on the Persian Gulf. These facilities were engineered to handle the bulk of Iraq's 4-plus million bpd output, loading very large crude carriers (VLCCs) destined primarily for Asian markets, with China and India absorbing the dominant share. This corridor has historically carried close to 95% of all monetised Iraqi crude, and its disruption is the direct cause of the current production collapse.

The Iraq-Turkey Pipeline (Kirkuk-Ceyhan System)

The original federal export alternative is the Iraq-Turkey Pipeline, running from the Kirkuk K1 field through the Salahaddin and Nineveh provinces to the Turkish Mediterranean port of Ceyhan. The system comprises two parallel pipes with a combined theoretical nameplate capacity of approximately 1.6 million bpd: a 46-inch line rated at 1.1 million bpd and a 40-inch line rated at 500,000 bpd.

In practice, this nameplate capacity has never been achieved. Functional throughput under normal operating conditions has historically ranged between 250,000 and 400,000 bpd, constrained by decades of militant attacks, maintenance failures, and underinvestment. Recent emergency rehabilitation efforts have restored partial flows at approximately 250,000 bpd, well below even historical norms.

The KRG Sidetrack Pipeline

Running parallel to the federal system, the Kurdistan Regional Government constructed its own pipeline from the Taq Taq field through Khurmala, connecting to the Kirkuk-Ceyhan network at the Fishkhabur border terminal. This KRG-controlled line carries an upgraded nameplate capacity of 1 million bpd and has achieved peak throughput of approximately 900,000 bpd.

The critical distinction is ownership and control. This pipeline answers to Erbil, not Baghdad. For the Federal Government of Iraq, accessing this infrastructure requires negotiating with a semi-autonomous regional authority whose relationship with the federal government has been defined by mutual distrust, accusation, and unresolved financial disputes since at least 2014.

Emergency Trucking and Minor Corridors

In the absence of functioning pipeline alternatives, Baghdad has resorted to overland trucking of crude toward Turkey. However, while this provides some marginal revenue, the volumes achievable by road transport are negligible relative to pipeline scale. Historical overland options to Syria and Jordan via crossings including Rabia-Yarubiyah, Al-Qaim-Al-Bukamal, and Al-Walid-Al-Tanf have remained largely dormant due to political instability and the absence of large-scale pipeline connectivity.

Additional dormant corridors include the Kirkuk-Baniyas pipeline to Syria, inactive due to the Syrian conflict, and the IPSA pipeline toward Saudi Arabia, politically dormant since the Gulf War era.

The Baghdad-Erbil Fault Line and Its Infrastructure Consequences

No analysis of Iraq oil export routes can ignore the political dimension that has arguably done more damage to Iraq's export resilience than any physical attack on its infrastructure.

The 2014 revenue-sharing agreement between Baghdad and Erbil created a framework under which the KRG would deliver approximately 550,000 bpd of regional production to the Federal Government in exchange for a 17% allocation from Iraq's central budget. The arrangement has never functioned as designed. Each party has persistently accused the other of non-compliance, with Baghdad alleging underdelivery of oil volumes and Erbil alleging irregular budget disbursements.

What makes this dispute strategically significant is the timing of its consequences. Baghdad's long-term objective has been to consolidate federal control over northern oil revenues and eliminate the KRG's capacity for independent export financing. The KRG pipeline to Ceyhan represented precisely the kind of independent revenue stream Baghdad sought to terminate.

The unintended outcome of this decade-long campaign is that the Federal Government now finds itself without reliable access to the only fully operational northern pipeline at the precise moment it faces an existential export crisis. Strategic pressure exerted against a rival's infrastructure can become strategic self-harm when circumstances shift rapidly.

This dynamic has broader implications for how Baghdad approaches the current crisis. Negotiating genuine pipeline access with the KRG requires conceding ground in a political dispute that successive federal governments have publicly committed to winning. The alternative — building entirely new federal pipeline infrastructure around KRG territory — is technically possible but expensive and time-consuming. Consequently, OPEC's market influence over how this situation develops remains a critical variable, given Iraq's obligations as a member state.

The Kirkuk-Nineveh Segment: Baghdad's Federal Pipeline Gambit

The new Kirkuk-to-Nineveh pipeline segment represents Baghdad's attempt to resolve this political constraint through infrastructure. Rather than negotiating access to KRG-controlled corridors, the federal government is constructing a pipeline route that bypasses KRG territory entirely, connecting Kirkuk directly to the Fishkhabur border terminal via Nineveh province.

The segment carries a design capacity of 350,000 bpd, which Baghdad's Oil Ministry has deliberately sized to match an initial trial throughput target of 150,000 to 250,000 bpd of Kirkuk crude. This phased approach reflects genuine technical caution. The old Iraq-Turkey Pipeline system has not operated at anything approaching its 1.6 million bpd nameplate capacity in years, and stress-testing that entire network simultaneously would risk catastrophic infrastructure failure.

The flow logic for the broader federal network is as follows:

Southern Basra Fields

↓

Basra–Haditha Pipeline (700 km, 2.5 million bpd capacity)

↓

Haditha Junction

↓

Kirkuk–Nineveh Segment (350,000 bpd design capacity)

↓

Fishkhabur Border Terminal

↓

Iraq-Turkey Pipeline

↓

Ceyhan Mediterranean Port (Turkey)

Once the Basra-Haditha corridor is operational, this architecture theoretically allows Iraq to move crude from the Persian Gulf coast to the Turkish Mediterranean without passing through the Strait of Hormuz or relying on any KRG-controlled infrastructure. Analysts tracking commodity market volatility will note that progress on this corridor represents one of the most significant structural shifts in global oil logistics in decades.

The next major ASX story will hit our subscribers first

The $5 Billion China Question

The construction of the Basra-to-Haditha pipeline — the southern connector that gives the entire northern network strategic relevance — has thrust Beijing back to the centre of Iraq's energy story at a moment when Western governments had hoped the conflict might pull Baghdad toward Western alignment.

The pipeline stretches 700 kilometres at a projected cost of US$5 billion and is designed to carry up to 2.5 million bpd from Iraq's southern production heartland northward to the federal network junction. Baghdad bypassed standard competitive public procurement processes to directly engage Chinese state-owned engineering firms for accelerated construction.

This decision connects directly to the 2019 Oil-for-Projects framework negotiated between Baghdad and Beijing, under which Iraq allocates 150,000 bpd into an escrow account as collateral for infrastructure work performed by Chinese entities. The US$1.5 billion emergency infrastructure budget approved under the framework draws on this mechanism, with Chinese state contractors now serving as the primary builders of Iraq's most strategically significant pipeline project.

The geopolitical signal embedded in this procurement decision is difficult to overstate. Under emergency conditions, without competitive bidding, and at a moment of maximum strategic vulnerability, Baghdad chose Chinese contractors over Western alternatives. This deepens Beijing's structural footprint in Iraqi energy infrastructure at precisely the moment its leverage is most valuable. Furthermore, the trade war impact on oil globally means that China's growing role in Iraqi infrastructure carries implications well beyond the Middle East.

Long-Term Scenarios: Four Pathways for Iraq's Export Geography

The trajectory of Iraq's infrastructure development depends heavily on how the broader regional conflict resolves. Four distinct scenarios are plausible, each carrying different implications for Iraq's export resilience, geopolitical alignment, and long-term production capacity. As analysts at the Foundation for Defence of Democracies have noted, many of these pipeline ambitions face significant structural obstacles that make timely delivery far from guaranteed.

Scenario A: Hormuz Reopens, Northern Routes Stall

The removal of immediate pressure reduces urgency for northern corridor investment. Infrastructure projects proceed slowly or stall, structural vulnerability to future closures remains unaddressed, and China retains its infrastructure leverage with no countervailing Western investment.

Scenario B: Hormuz Remains Disrupted, Northern Acceleration

Baghdad fast-tracks the Basra-Haditha corridor under sustained fiscal pressure. European refiners desperate for replacement barrels provide indirect incentives for Turkish transit expansion. Turkey's strategic importance rises significantly, and China's engineering footprint deepens further.

Scenario C: Partial Reopening, Hybrid Export Model

Iraq operates a dual-corridor system with southern tanker routes serving Asian markets and northern pipeline routes serving European refiners. The Kirkuk-Ceyhan system undergoes permanent rehabilitation as a strategic hedge. Baghdad negotiates a revised revenue-sharing arrangement with the KRG to access existing KRG pipeline capacity.

Scenario D: Prolonged Shutdown, Permanent Reservoir Damage

Extended well shut-ins in mature southern fields cause irreversible pressure depletion and water infiltration. Iraq's long-term production capacity is structurally impaired, with recovery to pre-crisis levels taking years rather than months. Fiscal deterioration accelerates political instability and compounds foreign infrastructure dependency.

Disclaimer: The scenarios presented above are analytical frameworks intended for informational purposes only. They do not constitute investment advice. Geopolitical and energy market developments involve significant uncertainty, and actual outcomes may differ materially from any scenario modelled here.

Infrastructure Milestones That Will Define Iraq's Export Future

For analysts and observers tracking Iraq's export capacity recovery, the following developments represent the key indicators to monitor:

- Commissioning progress and initial flow volumes on the Kirkuk-Nineveh pipeline segment

- Any formal agreement between Baghdad and Erbil on federal access to KRG pipeline infrastructure

- Construction timeline updates and contractor performance benchmarks for the Basra-Haditha corridor

- Utilisation rates at the Ceyhan terminal as northern flows gradually increase

- Any renegotiation of terms within the 2019 Oil-for-Projects framework that alters Beijing's infrastructure role

- Evidence of reservoir damage in southern fields as shut-in durations extend

The crisis facing Iraq's oil sector is not simply a product of an external conflict. It is the culmination of structural choices, political rivalries, and infrastructure underinvestment that left one of the world's largest oil producers almost entirely dependent on a single corridor that was always, under the right circumstances, closeable. Whether the current emergency catalyses genuine diversification or simply defers it depends on decisions being made in Baghdad, Erbil, Ankara, and Beijing right now. For a deeper understanding of the petroleum industry in Iraq and its long historical development, the structural vulnerabilities exposed by this crisis were, in many respects, decades in the making.

Want to Stay Ahead of the Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex commodity data into actionable investment insights — because when global supply chains fracture, the opportunities created in resource markets move fast. Start your 14-day free trial today and explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial returns for investors who positioned themselves early.