July 19, 2026

When the Buyer Becomes the Power: Iron Ore's Shifting Centre of Gravity

The conventional narrative of iron ore markets has long centred on supply-side dominance. A handful of Australian and Brazilian producers control the majority of seaborne volumes, and for decades this concentration gave miners like BHP, Rio Tinto, and Fortescue considerable pricing authority. However, the architecture of that power is being systematically challenged, not through the emergence of new supply, but through the institutional consolidation of demand.

China Mineral Resources Group, the state-backed procurement vehicle established to aggregate buying power across China's fragmented steel sector, is now demonstrating in real time how a sufficiently organised buyer can reshape the terms of even the most entrenched commodity trade relationships. The ongoing China state buyer scrutiny of Fortescue iron ore, centred on a newly developed product called Fortune Fines, offers one of the clearest case studies yet of how this dynamic operates in practice.

When big ASX news breaks, our subscribers know first

Understanding Fortune Fines: Grade, Product Design, and Market Positioning

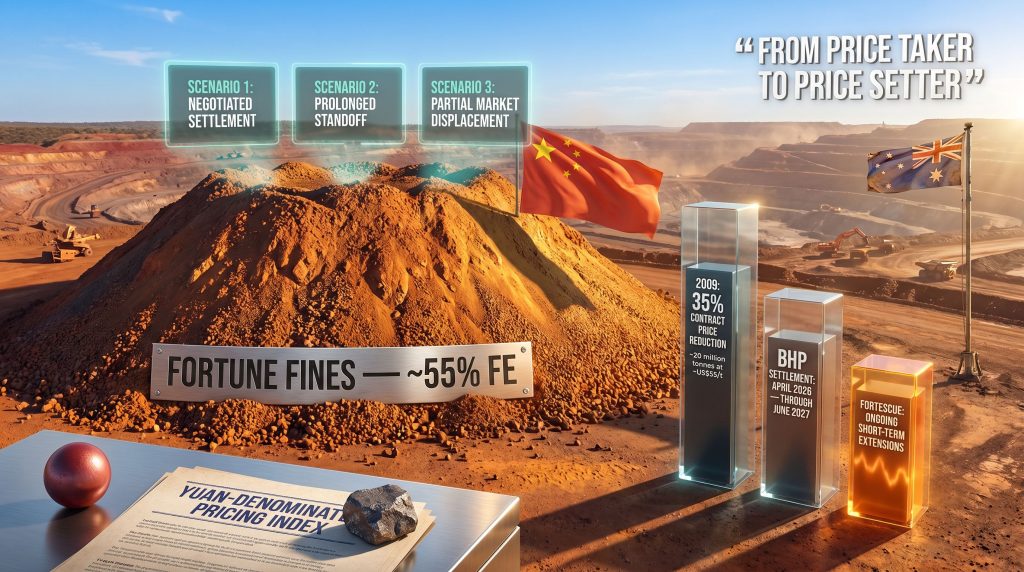

Fortune Fines is Fortescue's newly developed iron ore product carrying approximately 55% iron content, placing it firmly in the lower-grade segment of the seaborne iron ore market. To understand why this matters, some technical context is essential. Iron ore products are broadly categorised by their iron (Fe) content:

- High-grade ore: Typically above 62% Fe, commanding a price premium due to lower slag generation and reduced energy consumption in blast furnaces.

- Mid-grade ore: Generally between 58% and 62% Fe, the most commonly traded range in the seaborne market.

- Low-grade ore: Below 58% Fe, requiring greater processing effort by steel mills and typically sold at a discount to benchmark prices.

At 55% Fe, Fortune Fines falls into the lower end of the low-grade category. For steel mills, this means higher coke consumption per tonne of steel produced, increased slag volumes, and additional burden on furnace productivity. The commercial case for using such products rests on their price discount relative to higher-grade alternatives, and that discount must be sufficient to offset the processing cost differential.

Why Pre-Shipment Scrutiny Raises Strategic Questions

What makes the current scrutiny particularly notable is its timing. Fortune Fines has not yet been shipped. CMRG has directed affiliated steel mills to raise quality-related questions about a product they have not yet physically received or tested under operational conditions. Industry veterans acknowledge that quality due diligence is standard practice when new ore blends are introduced, but pre-shipment interrogation of an unproven product during active contract negotiations carries a distinct strategic dimension.

"The moment quality questions are raised before a single vessel has been loaded, the dispute ceases to be purely technical. It becomes a negotiating instrument."

CMRG's Structural Power: How State Procurement Aggregation Works

China's steel industry comprises hundreds of mills, historically operating as independent buyers competing against one another for ore supply. This fragmentation was, for years, a structural weakness in China's negotiating position. Individual mills lacked the scale to extract meaningful price concessions from major miners operating at the portfolio level.

CMRG was established precisely to address this imbalance. By consolidating procurement decisions across multiple steel mills, the entity creates a single demand-side counterparty capable of matching the scale of the world's largest iron ore exporters. Furthermore, the mechanics of this model are significant:

- Demand aggregation: Multiple mills' requirements are pooled, creating volume leverage that no individual buyer could achieve independently.

- Coordinated market signalling: Directing mills to simultaneously raise concerns about a specific product creates a unified demand-side response that amplifies commercial pressure.

- Pricing architecture control: By negotiating the structure of price indices, including the push toward yuan-denominated benchmarks, CMRG reshapes the reference framework within which iron ore transactions are denominated.

- Temporal leverage: Maintaining short-term supply extensions rather than finalising long-term agreements sustains negotiating uncertainty, which typically benefits the party with greater patience and alternative options.

This model is, in economic terms, an exercise in monopsony power. A monopsony occurs when a single buyer, or a coordinated group of buyers operating as one, gains sufficient market influence to affect the price and terms under which sellers must transact. When that buyer is state-backed and operating within a domestic regulatory jurisdiction that limits external legal recourse, the structural pressure it can exert is substantial. Consequently, China iron ore demand dynamics are shifting in ways that extend well beyond routine commercial negotiation.

The BHP Settlement as a Negotiating Benchmark

To contextualise where Fortescue currently stands, the BHP-CMRG agreement reached in April 2026 provides an instructive reference point. According to recent reporting, BHP ended its dispute with the powerful Chinese iron ore buyer after months of standoff, offering a telling precedent for what Fortescue may face.

| Feature | BHP Agreement | Fortescue Status (June 2026) |

|---|---|---|

| Contract Duration | Through June 2027 | Ongoing short-term extensions |

| Pricing Mechanism | Includes yuan-denominated indexes | Under active negotiation |

| Settlement Timeline | Months-long standoff before resolution | Negotiations remain stalled |

| Product Under Scrutiny | Established high-grade products | Fortune Fines (new, unshipped) |

| Grade Profile | High-grade, established market acceptance | Lower-grade, commercially unproven in China |

The BHP outcome is significant in two respects. First, it demonstrates that CMRG is willing to sustain prolonged negotiating standoffs, suggesting its tolerance for unresolved tension is higher than that of individual mining companies managing quarterly earnings cycles. Second, the inclusion of yuan-denominated pricing indexes in the BHP agreement represents a structural departure from the dollar-denominated benchmark system that has governed seaborne iron ore pricing for decades.

For Fortescue, the BHP settlement is simultaneously a roadmap and a warning. It shows that resolution is achievable, but it also reveals the concessions that may be required to reach it, including pricing mechanism compromises and an extended period of commercial uncertainty.

Historical Precedent: China's 2009 Iron Ore Playbook

The institutional sophistication CMRG displays in 2026 did not emerge in isolation. It reflects a strategic evolution that traces directly to China's 2009 iron ore price dispute, one of the most consequential episodes in the history of commodity trade negotiations.

In 2009, Chinese negotiators secured a 35% reduction in iron ore contract prices, covering approximately 20 million tonnes at around US$55 per tonne. That negotiating campaign deployed tools that extended well beyond commercial argument, including the detention of representatives from foreign mining companies. The Stern Hu and Rio Tinto case from this era illustrates the full strategic weight China was prepared to apply to procurement disputes.

The progression from 2009 to 2026 reflects a deliberate institutional evolution:

- 2009: Ad hoc price protests backed by political pressure and detention of individuals.

- 2015–2020: Gradual consolidation of steel industry governance and early exploration of centralised procurement structures.

- 2021–2023: CMRG formally established with a mandate to aggregate demand-side leverage.

- 2024–2026: CMRG executing multi-supplier negotiating campaigns simultaneously, incorporating currency denomination as a structural objective.

This trajectory suggests that what Fortescue is experiencing is not an isolated commercial dispute, but a phase in a longer-running strategic project to restructure the terms of China steel and iron ore market engagement.

The Cartel Question: Rhetoric, Reality, and Trade Law Limits

Fortescue's executive chairperson Andrew Forrest has publicly characterised CMRG's coordinated procurement approach as an attempt to establish a cartel-like structure in iron ore purchasing. This framing deserves careful analysis because it sits at the intersection of commercial rhetoric, trade law, and geopolitical signalling.

In economic theory, cartel behaviour typically describes supply-side coordination among producers to restrict output and maintain elevated prices. The demand-side equivalent, where buyers coordinate to suppress prices paid to suppliers, is termed a monopsony or, when involving coordinated buyer groups, a buyers' cartel. Trade economists note that the legal frameworks governing anti-competitive behaviour were largely designed with supply-side cartels in mind.

Demand-side equivalents, particularly those organised through state-backed entities operating within sovereign jurisdictions, present substantially more complex enforcement challenges.

"Existing international trade frameworks provide limited practical recourse against state-sponsored buyer coordination, particularly when that coordination occurs within the buyer's own domestic regulatory environment."

The public labelling of CMRG's conduct as cartel behaviour by a senior executive of a major mining company is therefore significant not primarily as a legal claim, but as a diplomatic and reputational signal. It draws international attention to the structural nature of CMRG's procurement model and positions Australia's resources sector as a party with legitimate grievances in what might otherwise be characterised as routine commercial negotiations.

The next major ASX story will hit our subscribers first

Fortescue's Competitive Exposure: Grade, Scale, and Strategic Positioning

As the world's fourth-largest iron ore producer, Fortescue occupies a specific and somewhat exposed position in the current negotiating environment. Its historical ore grade profile, while competitive on a cost basis, has consistently sat below the benchmark grades offered by BHP and Rio Tinto. This creates a compounding vulnerability in the current dispute.

Furthermore, iron ore surplus concerns add additional downward pressure on lower-grade producers, reinforcing CMRG's negotiating leverage. Fortescue's response has focused on deepening its strategic presence within China itself, expanding its senior leadership team in-country and emphasising the scale of its existing investments there. This approach reflects an understanding that in commodity trade relationships of this magnitude, commercial and diplomatic dimensions are inseparable.

Scenario Mapping: Three Possible Paths Forward

Scenario 1: Negotiated Settlement with Yuan Pricing Component

Fortescue agrees to a partial yuan-denominated pricing mechanism mirroring the BHP framework. Fortune Fines receives conditional approval following a technical review process, and a long-term agreement is finalised with pricing benchmarks aligned to Chinese domestic steel market indices. This outcome resolves short-term uncertainty but establishes structural precedents for future contract cycles.

Scenario 2: Prolonged Standoff with Incremental Concessions

Quality scrutiny of Fortune Fines remains unresolved through the remainder of 2026. Fortescue retains market access through successive short-term extensions but faces compounding pricing uncertainty. CMRG extracts incremental commercial concessions across each renewal cycle, achieving through attrition what it could not achieve in a single negotiation.

Scenario 3: Partial Market Displacement

CMRG redirects a portion of contracted volumes toward alternative suppliers, potentially including Brazilian producers or emerging African exporters. Fortune Fines faces a delayed or scaled-back commercial launch in the Chinese market. Fortescue accelerates efforts to diversify its customer base beyond CMRG-affiliated steel mills, accepting near-term revenue exposure in exchange for longer-term relationship diversification.

Key Risk Indicators Investors Should Monitor

For investors tracking the China state buyer scrutiny of Fortescue iron ore, several specific indicators carry forward-looking significance:

- Fortune Fines shipment timeline: Any formal delay to the product's first commercial shipment would signal an escalation in the quality dispute beyond routine due diligence.

- Contract structure updates: Movement from short-term extensions toward a multi-year framework would indicate negotiating progress, while continued rolling renewals suggest ongoing impasse.

- Yuan pricing adoption: Any confirmation that Fortescue has accepted yuan-denominated pricing indexes would represent a significant structural concession, with implications for revenue currency exposure.

- CMRG's simultaneous negotiations with Rio Tinto: Progress or stagnation in parallel negotiations would reveal whether CMRG is pursuing a sequenced or simultaneous multi-supplier strategy.

- Australian government commentary: Any formal diplomatic response to state-backed buyer coordination affecting a major export sector would escalate the dispute beyond a purely commercial frame.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Scenarios and projections discussed are speculative and involve significant uncertainty. Past negotiating outcomes do not guarantee future results. Investors should conduct independent due diligence before making any investment decisions.

The Deeper Implication: Iron Ore Pricing Is Becoming a Geopolitical Variable

The Fortune Fines dispute is, on its surface, a disagreement about product quality and contract terms. However, the structural forces driving it operate at a considerably higher level of strategic ambition. China's systematic push to introduce yuan-denominated pricing indexes into iron ore contracts serves dual purposes: it reduces China's exposure to dollar-denominated commodity benchmarks, and it advances the broader internationalisation of the renminbi in global commodity markets.

Australia's iron ore dominance remains structurally significant, yet the precedent established by the BHP agreement, and the terms that will eventually govern any Fortescue settlement, will shape the contracting environment for Rio Tinto, Vale, and every subsequent entrant to the Chinese market. In addition, global iron ore trade pressures from shifting tariff regimes add further complexity to an already strained bilateral trading relationship.

What is being negotiated is not simply the price of one product from one supplier. It is the institutional architecture within which the world's most significant bilateral commodity trade relationship will operate for the next decade. For Australian iron ore exporters, the lesson being written in real time is that product quality, ore grade, and contract structure are no longer purely commercial decisions made in boardrooms and trading desks. They are variables in a geopolitical equation — one where the buyer has spent fifteen years building the institutional capacity to write the terms. Indeed, China state buyer scrutiny of Fortescue iron ore may well be remembered as the inflection point at which that shift became undeniable.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While iron ore's geopolitical landscape shifts beneath the feet of major producers, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries so subscribers can act before the broader market catches on — explore historic discovery returns or start your 14-day free trial today.