July 24, 2026

Global commodity markets operate through complex supply-demand equilibriums that can shift dramatically when new production capacity enters established trading patterns. The iron ore market oversupply phenomenon exemplifies how structural economic transitions in major consuming nations can create persistent imbalances even during periods of robust pricing activity. Furthermore, iron ore price trends demonstrate characteristics that distinguish temporary cyclical adjustments from longer-term structural oversupply conditions.

Understanding market oversupply requires analysis of production capacity utilisation rates, inventory accumulation patterns at major port terminals, and the disconnect between pricing mechanisms and underlying physical demand fundamentals. When port stockpiles reach multi-year highs while steel production declines to seven-year lows, markets signal structural rather than cyclical imbalance.

Defining Iron Ore Market Oversupply Conditions

Iron ore market oversupply manifests through specific measurable indicators that distinguish it from normal market volatility. Singapore iron ore futures reaching $109 per tonne during January 2026 represented a 15-month high, yet this pricing strength occurred alongside Chinese port stockpiles ballooning to near four-year highs. This fundamental disconnect illustrates how financial market positioning can drive pricing independent of physical market conditions.

Key Oversupply Indicators:

• Port inventory accumulation exceeding normal seasonal patterns

• Steel production declining while ore imports reach record levels

• Pricing driven by hedge fund positioning rather than physical tightening

• Production capacity additions outpacing consumption growth trajectories

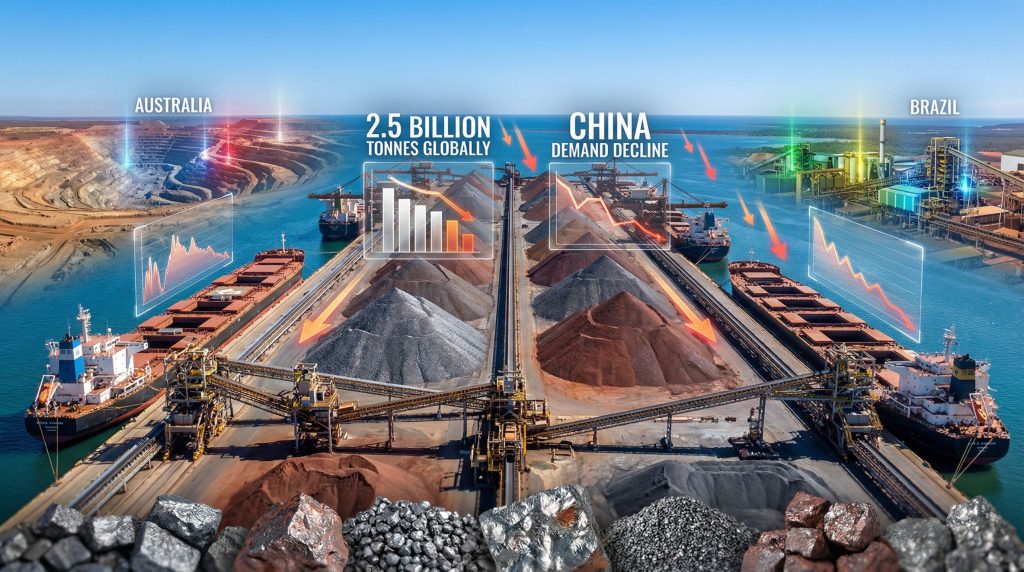

The seaborne iron ore market operates on approximately 2.5 billion tonnes of annual global production capacity, with australia's iron ore leadership commanding roughly 55% of global market share and Brazil controlling approximately 25%. Capacity utilisation rates vary significantly across different ore grades, with premium 65%+ iron content deposits maintaining higher operational rates due to quality premiums and blast furnace efficiency advantages.

Structural oversupply emerges when fundamental demand patterns shift independently of supply adjustments. China's steel production trajectory toward a seven-year low despite record 2025 iron ore imports exemplifies this dynamic, where strategic stockpiling and quality preferences drive import volumes beyond immediate consumption requirements.

When big ASX news breaks, our subscribers know first

New Mining Projects Reshaping Global Supply Dynamics

The Simandou project in Guinea represents the most significant new iron ore supply addition in recent years, with its $23 billion investment creating production capacity equal to approximately 5% of global output. The project's first commercial shipment arrived in China during January 2026, marking the beginning of a gradual supply expansion that analysts expect will pressure pricing through 2027.

Simandou's high-grade ore specifications, containing 65%+ iron content, position it advantageously within global cost curves whilst providing blast furnace efficiency benefits that command quality premiums. However, the project's production ramp-up timeline extends over multiple years, requiring time to achieve economies of scale that will maximise its market impact.

Simandou Project Timeline and Impact:

• Initial production: 20 million tonnes annually in 2026

• Full capacity target: 120 million tonnes per annum by 2030

• Infrastructure requirements: Port development and shipping logistics

• Market positioning: Premium grade ore commanding quality pricing

Shanghai Metals Market analysis indicates that supply surplus pressures will develop gradually rather than through sharp adjustments, as new production requires time to establish operational efficiency and market penetration. This timeline provides existing producers with adjustment periods whilst creating long-term pricing pressure expectations.

Brazilian and Australian production expansions complement Simandou's supply additions through operational efficiency improvements and capacity optimisation programmes. Vale's EBITDA declined 22% to $15.4 billion in 2024, reflecting margin pressures from competitive dynamics and operational challenges following post-dam incident recovery programmes.

Weather-related supply disruptions continue affecting largest iron ore mines during cyclone seasons (November-April) and Brazilian mines during rainfall periods, creating seasonal volatility that temporarily masks underlying oversupply trends. Major producers coordinate maintenance scheduling during lower-demand periods, typically around Lunar New Year production shutdowns.

Chinese Steel Demand Transformation and Import Patterns

China's steel demand trajectory reflects broader economic transformation from infrastructure-intensive growth toward services and consumption-oriented development. Real estate sector downturns, characterised by 30% reductions in new construction starts, directly impact steel consumption through reduced structural steel requirements and deferred infrastructure projects.

Despite declining steel production, China's iron ore imports reached record levels in 2025, creating a fundamental disconnect between import volumes and domestic consumption patterns. This phenomenon reflects multiple factors including strategic stockpiling, quality specification preferences, and financial market positioning independent of immediate production needs.

Chinese Market Dynamics:

• Steel production on course for seven-year low in 2025

• Infrastructure investment plateauing after decades of expansion

• Government policies targeting steel sector overcapacity reduction

• Steel intensity per GDP declining as economy matures

Port inventory accumulation to four-year highs demonstrates strategic stockpiling ahead of Lunar New Year shutdowns and anticipation of potential government policy support. HSBC Holdings analysis suggests short-term pricing may benefit from front-loaded fiscal spending in early 2026 as China implements its latest five-year plan. Consequently, this could provide temporary commodities demand support through infrastructure investment.

Chinese steelmakers increasingly prioritise high-grade ore imports to meet environmental regulations and blast furnace efficiency requirements, driving premium ore demand regardless of overall steel production volumes. This quality-focused import strategy sustains import volumes whilst domestic consumption patterns weaken.

Price Dynamics and Market Volatility Drivers

Iron ore pricing volatility reflects the intersection of financial market positioning, government policy expectations, and underlying physical market fundamentals. Current Singapore futures benchmark pricing at $107-109 per tonne during January 2026 represents levels last reached approximately 15 months earlier during Chinese government stimulus implementation periods.

ING Groep analysis characterises the early 2026 rally as increasingly disconnected from underlying fundamentals, driven by improved hedge fund risk appetite and policy support expectations rather than sustained physical market tightening. This positioning-driven price strength creates vulnerability to sentiment shifts or policy disappointments.

Price Forecasting Consensus:

| Institution | 2026 Average Forecast | 2027 Outlook | Primary Assumptions |

|---|---|---|---|

| Investment Banks Consensus | $94-96/tonne | $85-90/tonne | China demand decline, supply growth |

| ING Groep | $95/tonne | $88/tonne | Property sector weakness impact |

| Market Analysts | $96/tonne | $90/tonne | Steel production capacity cuts |

| Trading Platforms | $112/tonne | $105/tonne | Short-term technical factors |

Bloomberg analyst surveys forecast steady price declines from median $100 per tonne in Q1 2026 to $90 per tonne in Q2 2027. These forecasts incorporate Simandou ramp-up projections and structural Chinese demand stabilisation assumptions, proving highly sensitive to China policy implementation timing and infrastructure spending acceleration.

Premium grade economics maintain 15-25% pricing advantages over standard 60-62% iron content ore. This reflects blast furnace efficiency gains and reduced beneficiation requirements that justify quality premiums despite the iron ore market oversupply conditions.

Geopolitical Factors and Supply Chain Dynamics

China-Australia trade relations continue influencing market liquidity through bhp strategic pivot pricing disputes that restrict cargo volumes and create alternative sourcing pressures. Resolution of these disputes would unlock previously restricted ore supplies, potentially adding 50-100 million tonnes annually to available market supply and creating additional pricing pressure.

Guinea's emergence as a major iron ore exporter through Simandou development represents significant geopolitical shifts in African mining investment and infrastructure development. Chinese investment interests in West African mining corridors create new supplier relationships that compete with established Australian and Brazilian producers.

Geopolitical Supply Considerations:

• BHP-China pricing dispute resolution timeline uncertainty

• West African infrastructure development and political stability

• Supplier diversification strategies amongst major steel producers

• Regulatory environment impacts on mining project development

African mining development faces infrastructure completion challenges, political stability considerations, and market absorption capacity questions for additional global production volumes. However, successful project implementation creates long-term supply diversity that reduces dependence on traditional producing regions.

Investment Implications and Company Performance Analysis

Major mining companies face profitability pressures under oversupply conditions as margin compression occurs across different price scenarios. Vale's 22% EBITDA decline to $15.4 billion in 2024 exemplifies how competitive dynamics and operational challenges affect financial performance during market transitions.

Cost curve positioning becomes critical during extended oversupply periods, with high-cost producers facing operational sustainability challenges whilst low-cost operators maintain competitive advantages. BHP and Rio Tinto operational efficiency programmes target cost reductions that preserve market share during pricing pressure periods.

Investment Strategy Considerations:

• Dividend sustainability analysis under lower price scenarios

• Capital allocation strategies during down cycles

• Mid-tier producer consolidation opportunities

• Technology investments improving operational efficiency

Mid-tier producer consolidation opportunities emerge as smaller operators face financial pressure from sustained iron ore market oversupply conditions. Companies with strong balance sheets and operational efficiency capabilities may acquire distressed assets at favourable valuations during market stress periods.

The next major ASX story will hit our subscribers first

Technology and Grade Quality Market Competition

High-grade ore premium dynamics reflect environmental regulations driving quality preferences and blast furnace efficiency improvements with premium ores. Transportation cost advantages of concentrated products justify quality premiums that persist despite overall market oversupply conditions.

Processing technology advances through beneficiation improvements for lower-grade deposits and direct reduction iron (DRI) technology adoption create competitive dynamics between different ore quality specifications. Furthermore, iron ore demand insights reveal that green steel production requirements increasingly favour high-grade ores that reduce environmental impacts during steelmaking processes.

Technology Impact Factors:

• Beneficiation improvements reducing processing requirements

• Environmental regulations favouring high-grade specifications

• Green steel production technology preferences

• Transportation efficiency gains from ore concentration

Blast furnace efficiency improvements with premium ores create sustainable demand segments for high-quality products even during oversupply conditions. This supports quality premium structures that differentiate producers by ore grade capabilities.

What Are the Seasonal Patterns and Market Timing Factors?

Chinese demand seasonality creates predictable inventory management cycles around Lunar New Year production shutdowns and construction season demand patterns. Strategic buffer inventory requirements ahead of typical 1-2 week production shutdowns drive temporary stockpiling that can mask underlying demand trends.

Supply-side seasonal factors include weather disruptions in Australia and Brazil, shipping logistics variations, and coordinated maintenance scheduling at major mining operations. These seasonal patterns create short-term volatility that overlays longer-term structural supply-demand imbalances.

Seasonal Market Influences:

• Lunar New Year shutdown inventory requirements

• Construction season demand patterns in major markets

• Weather disruption probabilities in producing regions

• Maintenance scheduling coordination amongst producers

Government stimulus timing and infrastructure spending programmes create additional seasonal demand variations that interact with natural market cycles. Policy announcement timing and implementation schedules influence commodity demand expectations independently of underlying economic fundamentals.

Macroeconomic Conditions and Long-Term Demand Outlook

Global steel production trends reflect emerging market infrastructure development needs balanced against developed market steel recycling rate improvements and electric vehicle impact on steel demand composition. These macro trends influence long-term iron ore consumption patterns beyond immediate Chinese market dynamics.

China's carbon neutrality targets create steel sector transformation pressures that affect iron ore demand through production efficiency requirements, recycling rate improvements, and alternative steelmaking technology adoption. Government policies targeting emission reductions modify traditional steel production processes and raw material requirements.

Long-Term Demand Drivers:

• Infrastructure development in emerging markets

• Steel recycling technology advancement in developed economies

• Electric vehicle manufacturing steel intensity requirements

• Carbon neutrality policy implementation in major consuming nations

Infrastructure spending programmes in major economies and trade policy impacts on global steel flows create additional demand variability that interacts with supply expansion from new mining projects. Consequently, market outlook forecasts suggest policy coordination between producing and consuming nations influences market stability during transition periods.

How Can Market Participants Manage Risk?

Producer response mechanisms during oversupply scenarios include production curtailment decision frameworks, inventory management optimisation, and hedging approaches for price risk mitigation. Major producers develop operational flexibility that enables rapid production adjustments when market conditions deteriorate.

Buyer strategy adaptations balance long-term contract commitments against spot market opportunities, quality specification optimisation, and alternative supplier development programmes. Strategic inventory positioning enables buyers to optimise purchasing timing whilst managing supply security requirements.

Risk Mitigation Approaches:

• Production flexibility enabling rapid capacity adjustments

• Strategic inventory management optimising storage costs

• Financial hedging instruments managing price volatility exposure

• Supplier diversification reducing concentration risks

Market participants increasingly employ sophisticated risk management frameworks that incorporate multiple scenario planning approaches. This recognises that iron ore market oversupply conditions may persist longer than traditional cyclical adjustments suggest.

Disclaimer: This analysis contains forward-looking statements and market forecasts based on current information and analyst projections. Iron ore market conditions involve significant volatility and uncertainty. Readers should conduct independent research and consider professional advice before making investment decisions. Market forecasts may not reflect actual future performance due to changing economic conditions, geopolitical developments, and unforeseen supply-demand dynamics.

Want to Stay Ahead of Mining Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, providing investors with actionable insights during volatile market conditions like the current iron ore oversupply. Begin your 30-day free trial today and position yourself to capitalise on emerging opportunities before they reach mainstream market attention.