May 21, 2026

Understanding the Iron Ore Market's Structural Transformation

Global commodity markets have entered a period of unprecedented volatility, with traditional demand-supply relationships undergoing fundamental restructuring. Iron ore, the backbone of global steel production, finds itself at the epicentre of this transformation as shifting economic priorities and industrial policies reshape century-old trading patterns.

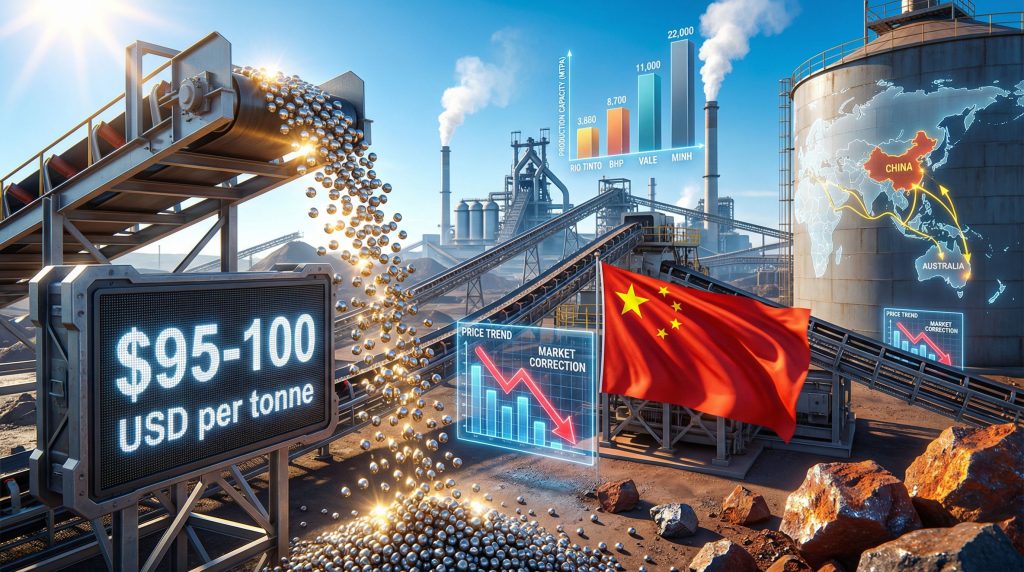

The convergence of multiple macro-economic forces has created a perfect storm for iron ore price trends and China demand prospects, with benchmark rates testing multi-year support levels around $100 per tonne. This represents more than a cyclical adjustment; it signals a structural recalibration of how global steel supply chains operate in an era of changing economic priorities and industrial transformation.

Recent market data confirms this structural shift is accelerating. Iron ore prices fell to US$100 per tonne on December 15, 2025, retreating from strength observed during the previous fortnight, according to Trading Economics iron ore data. This volatility within a relatively narrow trading range suggests underlying demand-supply fundamentals remain under considerable stress.

The iron ore price drop represents more than cyclical commodity weakness; it reflects fundamental changes in global economic structure and industrial priorities that require careful analysis.

When big ASX news breaks, our subscribers know first

China's Economic Pivot and Steel Consumption Patterns

China's transition from infrastructure-heavy growth to technology-focused development has created unprecedented disruption in global iron ore demand patterns. The world's largest steel producer faces a fundamental restructuring of its industrial base, with implications extending far beyond domestic markets.

The property sector crisis represents the most visible manifestation of this transformation. Construction activities, historically consuming approximately 60% of China's steel output, have contracted significantly as developers struggle with debt obligations and changing government priorities.

This contraction has cascaded through the entire steel value chain, reducing hot metal production and creating oversupply conditions in global iron ore markets. However, understanding these patterns provides valuable miners' demand insights for market participants.

Critical Demand Indicators:

• Chinese steel production stabilising around 1.01 billion tonnes annually

• Property sector steel consumption declining 25-30% from peak levels

• Infrastructure investment growth slowing to sub-3% annually

• Industrial policy emphasis shifting toward high-technology manufacturing

This demand destruction reflects more than temporary economic weakness. Beijing's strategic emphasis on technological advancement and services sector development fundamentally reduces steel intensity per unit of economic growth, creating permanent headwinds for iron ore consumption.

The implications extend beyond raw tonnage reductions. China's evolving industrial structure favours high-value manufacturing over heavy industry, reducing the multiplier effects that historically drove steel demand during economic expansion cycles.

Global Supply Chain Reconfiguration

Despite weakening demand signals, major iron ore producers have maintained aggressive expansion strategies, creating supply-demand imbalances that pressure pricing across all quality grades. Furthermore, this situation is exacerbated by several largest iron ore mines 2025 continuing their expansion plans.

Production Capacity Analysis:

| Producer | 2024 Output (Mt) | 2025 Planned Capacity | Strategic Response |

|---|---|---|---|

| BHP Group | 285 | 290+ | Operational efficiency focus |

| Rio Tinto | 320 | 330+ | Premium grade positioning |

| Fortescue Metals | 190 | 195+ | Green energy diversification |

| Vale | 310 | 320+ | Quality enhancement strategy |

These expansion plans reflect long-term investment commitments made when demand projections appeared more favourable. The inability to quickly adjust production volumes creates structural oversupply that pressures pricing across the entire market spectrum.

Guinea's Simandou project represents a particular challenge to market equilibrium. The development threatens to add 150+ million tonnes of annual capacity by 2027-2028, fundamentally altering global supply balances just as demand growth moderates.

Emerging Market Dynamics

The iron ore market faces additional complexity from new supply sources entering production during a demand downturn. This timing mismatch creates oversupply conditions that may persist for several years, regardless of short-term price volatility.

Production economics favour continued operation even at reduced prices, as most established mines operate well below cash cost thresholds at current levels. This creates price rigidity that prevents rapid market clearing through supply adjustments.

Consequently, the market is experiencing a price decline amid surplus conditions that may persist longer than initially anticipated.

Institutional Price Forecasting and Economic Scenarios

Leading financial institutions have revised their iron ore price projections downward, reflecting structural changes in demand patterns and persistent oversupply conditions. For instance, ING Think analysis suggests iron ore heads for a softer year ahead.

Consensus Forecast Analysis:

| Institution | 2025 Average | 2026 Projection | Analytical Framework |

|---|---|---|---|

| Major Bank A | $95/tonne | $90/tonne | Demand destruction model |

| International Organisation | $95/tonne | $88/tonne | Structural surplus analysis |

| Investment Bank B | $97/tonne | $80/tonne | Long-term equilibrium pricing |

| Swiss Bank | $97.50/tonne | $95/tonne | Supply-demand balance |

These projections incorporate multiple scenario analyses, with base cases assuming continued Chinese demand moderation and gradual supply additions from new projects. Downside scenarios suggest prices could test $75-80 per tonne if demand contraction accelerates beyond current forecasts.

Risk Assessment Framework:

• Upside catalysts: Unexpected Chinese stimulus, supply disruptions, geopolitical tensions

• Downside triggers: Accelerated property sector decline, early Simandou production, global recession

• Probability weighting: Base case scenarios carry 60-70% probability according to institutional analyses

Regional Market Fragmentation and Trade Flow Evolution

The decline in Chinese import requirements has exposed the limitations of alternative demand sources in absorbing global iron ore production volumes. In addition, this highlights the unique Australian industry advantages that remain crucial despite market challenges.

Southeast Asian steel production growth of 3-5% annually represents only 15% of China's consumption scale, insufficient to offset even modest Chinese demand reductions. India's infrastructure development, whilst robust, similarly lacks the scale necessary to rebalance global markets.

Alternative Market Limitations:

• Southeast Asian capacity additions insufficient for global rebalancing

• Indian demand growth positive but inadequate scale

• European steel production declining due to decarbonisation pressures

• North American demand stable but not growth-oriented

Shipping and Logistics Implications

Traditional Australia-to-China shipping routes face reduced utilisation rates, creating knock-on effects for maritime freight markets and port infrastructure economics. This reconfiguration affects:

• Freight rate structures for bulk carriers

• Port capacity utilisation in Western Australia

• Regional economic multiplier effects in mining communities

ASX-Listed Mining Companies: Strategic Responses

Australian iron ore producers have adopted divergent strategies to navigate the challenging price environment, reflecting different operational capabilities and strategic priorities.

BHP Group (ASX: BHP)

BHP maintains iron ore as a core portfolio asset despite price volatility, emphasising operational efficiency and cost curve positioning. The company's integrated approach includes:

• Cost optimisation: Focus on maintaining industry-leading cost structures

• Quality positioning: Emphasis on premium grade products for specialised applications

• Operational excellence: Continued investment in automation and digital technologies

Recent market developments suggest materials sector weakness affects broader mining valuations, with iron ore price fluctuations creating earnings volatility across the sector.

Rio Tinto (ASX: RIO)

Rio Tinto's strategy emphasises high-grade ore premium pricing whilst diversifying into growth commodities. However, recent strategic shifts suggest capital allocation priorities are evolving rapidly.

Market intelligence indicates Rio Tinto is scaling back lithium investments in Australia, with reports describing a downsizing of previously ambitious battery metals plans. This suggests the company is prioritising traditional iron ore operations whilst selectively pursuing diversification opportunities.

Strategic Focus Areas:

• Premium iron ore grade positioning for specialised steel applications

• Automation and digitalisation investments to reduce operational costs

• Selective diversification into copper and critical minerals with established demand profiles

Fortescue Metals (ASX: FMG)

Fortescue has pursued the most aggressive diversification strategy, moving beyond traditional iron ore operations into renewable energy and battery metals.

• Green energy initiatives: Substantial investments in hydrogen and renewable energy projects

• Operational efficiency: Maintaining low-cost production philosophy across all operations

• Technology development: Exploring green steel production technologies for future market positioning

This diversification reflects management's view that traditional iron ore demand may face long-term structural challenges requiring alternative revenue sources.

The next major ASX story will hit our subscribers first

Technological Disruption and Steel Industry Evolution

The global steel industry's decarbonisation journey creates both challenges and opportunities for iron ore producers, with quality specifications becoming increasingly important.

Green Steel Technology Impact

Hydrogen-based direct reduction processes favour high-grade iron ore feedstock, creating potential quality premiums that may partially offset volume declines. This technological shift affects:

• Grade requirements: Higher iron content needed for efficient hydrogen reduction

• Impurity sensitivity: Reduced tolerance for phosphorus and sulphur content

• Supply chain integration: Closer producer-consumer relationships for specialised products

Electric Arc Furnace Growth

Increased steel recycling through electric arc furnaces reduces virgin iron ore requirements, representing a structural headwind for traditional blast furnace feedstock demand.

Technology Transition Metrics:

• Electric arc furnace share of global steel production: 30% and growing

• Scrap steel availability increasing with infrastructure replacement cycles

• Energy cost advantages in regions with renewable electricity access

Geopolitical Risk Factors and Trade Policy Evolution

International trade tensions add complexity to iron ore market dynamics, potentially redirecting established trade flows and affecting pricing mechanisms.

US-China trade relationships continue influencing steel market structures, with potential tariffs on Chinese steel exports capable of redirecting global trade patterns. However, domestic Chinese oversupply remains the primary driver of international price pressure.

Resource Security Considerations

Governments increasingly view iron ore as strategically important, potentially leading to:

• Export licensing requirements in major producing countries

• State intervention in pricing mechanisms during supply disruptions

• Stockpiling programmes to ensure supply security

• Investment restrictions affecting foreign ownership of mining assets

These developments could create price volatility separate from fundamental supply-demand dynamics.

Economic Multiplier Effects Across Sectors

Iron ore price weakness creates ripple effects throughout commodity-dependent economies, particularly affecting regions with concentrated mining exposure.

Australian Economic Implications

Western Australia's fiscal position depends heavily on iron ore royalty revenues, creating budget pressures as commodity prices decline. This affects:

• State government infrastructure investment capacity

• Regional employment in mining-dependent communities

• Currency implications for the Australian dollar

• Broader economic multiplier effects in service sectors supporting mining operations

Global Steel Industry Consolidation

Sustained low iron ore prices may accelerate steel industry consolidation as marginal producers face profitability pressures. This could ultimately support iron ore demand through:

• Elimination of inefficient steel production capacity

• Investment in more efficient production technologies

• Geographic rebalancing toward lower-cost production regions

Investment Risk Management Strategies

Investors with iron ore exposure face a complex risk environment requiring sophisticated hedging and portfolio management approaches.

Portfolio Diversification Approaches

Risk Mitigation Strategies:

• Commodity diversification: Exposure to metals with stronger demand fundamentals (copper, lithium, rare earths)

• Currency hedging: Managing AUD exposure given commodity price correlation

• Sector rotation: Rebalancing toward technology and services sectors less dependent on Chinese infrastructure

• Geographic diversification: Reducing concentration in single-commodity dependent regions

Market Timing Considerations

Technical analysis suggests iron ore prices may find support around $85-90 per tonne levels, though fundamental recovery requires Chinese demand stabilisation or supply discipline from producers.

Investment Timeline Framework:

• Short-term (6-12 months): Continued volatility within $85-105/tonne range

• Medium-term (1-3 years): Gradual rebalancing as Chinese property sector stabilises

• Long-term (3-5+ years): New equilibrium dependent on alternative demand sources and supply discipline

Long-term Structural Market Outlook

The iron ore market's future trajectory depends on multiple variables, with recovery scenarios requiring either demand stabilisation or supply curtailment to restore pricing power.

Demand Recovery Pathways

Iron ore prices will likely remain subdued until Chinese property markets stabilise and alternative demand sources reach sufficient scale. Key recovery catalysts include:

• Chinese economic stabilisation: Property sector debt resolution and policy support

• Indian infrastructure acceleration: Sustained GDP growth driving steel consumption

• Southeast Asian industrialisation: Manufacturing capacity expansion requiring steel inputs

• Green steel transition: Quality premium development for specialised applications

Supply Discipline Requirements

Market rebalancing ultimately requires either demand recovery or supply curtailment from high-cost producers. Current price levels test operational breakeven points across the industry cost curve.

Critical Thresholds:

• Cash cost support: Most operations remain profitable at current prices

• Capital discipline: New project approvals increasingly unlikely below $120/tonne long-term prices

• Mine life optimisation: Existing operations may defer expansion or accelerate depletion

The iron ore price drop represents more than cyclical commodity weakness; it reflects fundamental changes in global economic structure and industrial priorities. Investors and industry participants must prepare for an extended period of price volatility as markets adjust to new demand patterns and supply realities.

Disclaimer: This analysis contains forward-looking statements and market projections that involve uncertainty and risk. Commodity prices are inherently volatile and subject to numerous economic, political, and technical factors beyond prediction. Investors should conduct independent research and consider professional advice before making investment decisions. Past performance does not guarantee future results.

Looking to Identify the Next Iron Ore Discovery Opportunity?

While iron ore markets navigate structural challenges, Discovery Alert's proprietary Discovery IQ model instantly identifies significant mineral discoveries across the ASX, including iron ore prospects that could benefit from quality premiums in the evolving green steel market. Explore why major mineral discoveries have historically generated substantial returns by visiting Discovery Alert's discoveries page, and begin your 30-day free trial today to position yourself ahead of market opportunities.