June 7, 2026

Global commodity markets face unprecedented transformation as industrial decarbonisation accelerates and supply chain resilience becomes paramount. The iron ore sector exemplifies these macro-economic shifts, where traditional volume-based competition yields to quality differentiation and technological advancement. Regional production hubs must now balance raw material output with sustainable practices while navigating volatile demand patterns from major consuming nations.

What Drives Brazil's Position as the World's Second-Largest Iron Ore Producer?

Global Market Share and Production Volume Analysis

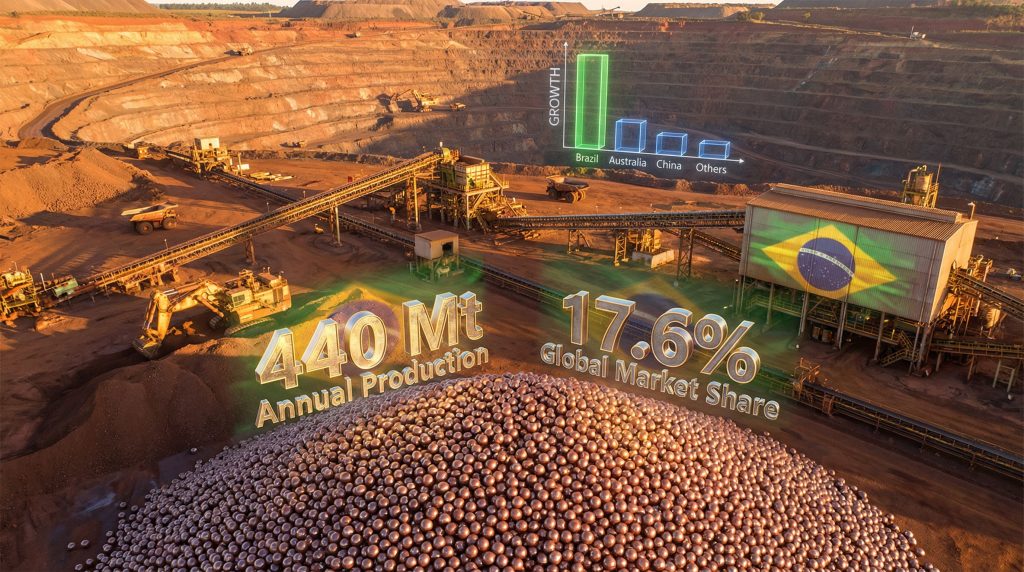

Iron ore production in Brazil commands significant influence within global commodity markets through substantial output volumes and strategic geographic positioning. Current production levels reach 440 million tonnes annually, representing 17.6% of worldwide production from a total global market of 2,500 million tonnes. This positions Brazil as the second-largest producer globally, trailing Australia's dominant 930 million tonnes but maintaining substantial market influence.

Furthermore, understanding these production dynamics becomes crucial when examining iron ore price trends that directly impact Brazilian operations. Regional concentration patterns reveal two primary production centres driving national output:

- Minas Gerais: 222+ million tonnes annually (50.5% of national production)

- Pará: 172 million tonnes annually (39.1% of national production)

This geographic concentration in two states accounts for approximately 394 million tonnes or 89.5% of Brazil's total iron ore output, creating natural infrastructure optimisation opportunities and logistics efficiency advantages. The remaining production disperses across secondary mining regions, though at significantly lower volumes.

Revenue Generation and Economic Impact Assessment

Export performance metrics demonstrate robust international market engagement, with 416.4 million tonnes exported during 2024, achieving year-over-year growth of 7.1%. This export volume generates substantial foreign exchange earnings, with market valuation reaching USD 11.1 billion in 2024.

The revenue generation capacity reflects sustained pricing above critical profitability thresholds. According to industry analysis, iron ore prices have maintained levels above USD 100 per tonne despite market oscillations, contributing to cautious optimism among Brazilian commodity producers. This price stability enables continued investment in production expansion and quality enhancement initiatives.

Brazilian producers maintain strategic conviction in long-term growth despite near-term demand uncertainties, particularly regarding reduced Chinese consumption patterns.

Currency dynamics also influence competitiveness, as Real/USD exchange rate fluctuations directly impact export revenue calculations and relative cost structures compared to Australian and other international competitors.

When big ASX news breaks, our subscribers know first

How Are Brazilian Producers Adapting to Market Volatility?

Quality-Focused Production Strategies

Market volatility has prompted fundamental strategic shifts among iron ore production in Brazil operations, moving beyond traditional volume-based competition toward premium product differentiation. Industry analysis reveals that producers have systematically directed production toward products with higher iron content and lower contamination levels as a primary strategy to maintain competitiveness.

This quality-focused approach addresses reduced Chinese demand patterns while capitalising on premium pricing opportunities. China remains the largest consumer of raw material for the steel industry, but declining consumption volumes have forced global producers to compete more aggressively on product specifications rather than simple tonnage delivery.

In addition, producers are increasingly aware of surging iron ore demand patterns emerging from other markets. Premium grade targeting methodology includes:

- Iron content enhancement: Upgraded beneficiation processes increasing Fe% concentration in finished products

- Contaminant reduction: Advanced techniques minimising silica, alumina, and phosphorus levels that reduce steel quality

- Pellet production expansion: Converting fine iron ore into briquetted products preferred by blast furnace operations

The pellet segment currently represents 53.35% of market share in processed iron ore products, with projected demand acceleration at 3.5% compound annual growth rate through 2030. This growth trajectory supports continued investment in pelletisation infrastructure across major Brazilian operations.

Technology Integration and Operational Efficiency

Digital transformation initiatives represent critical adaptation strategies enabling operational optimisation and cost reduction during volatile market conditions. Artificial Intelligence, connected sensors, and remote operation capabilities are redefining operational approaches with measurable improvements in productivity, safety, and sustainability metrics.

Remote Operations Centres (COR) exemplify practical Industry 4.0 implementation, centralising equipment monitoring and operation across extensive mining operations. These facilities enable:

- Real-time equipment performance monitoring across 529-kilometre pipeline systems and mining operations

- Reduced on-site personnel requirements in remote locations

- Enhanced safety protocols through automated hazard detection systems

- Data-driven maintenance scheduling and production optimisation

Sensor-based monitoring systems deploy connected networks enabling predictive maintenance scheduling, reducing unplanned downtime whilst extending asset life cycles. These technological investments demonstrate producer commitment to operational excellence despite challenging market conditions.

Which Companies Are Leading Brazil's Iron Ore Expansion Plans?

Vale's Market Leadership Strategy

Vale maintains its position as Brazil's dominant iron ore producer through strategic expansion and operational optimisation initiatives. First half 2024 production reached 151.4 million tonnes, representing 4.1% year-over-year growth despite broader market challenges. The company targets 340-360 million tonnes annual production capacity by 2026 through continued development of key operations including S11D and Vargem Grande scaling projects.

However, when considering global operations, it's important to examine how Brazil compares to other major producers in the largest iron ore mines worldwide. Vale's expansion strategy emphasises operational efficiency and premium product development rather than pure capacity expansion. The company leverages its substantial reserve base and established infrastructure networks to maintain competitive advantages whilst adapting to evolving market demands.

Mid-Tier Producer Growth Initiatives

ArcelorMittal's Serra Azul expansion represents one of Brazil's most significant capacity enhancement projects. The R$ 2.5 billion investment in the Itatiaiuçu, Minas Gerais operation has tripled annual capacity from 1.6 million tonnes to 4.5 million tonnes, with commissioning completed in 2025. This approximately 181% capacity increase demonstrates confidence in long-term market fundamentals despite near-term volatility.

Bemisa's strategic positioning in Minas Gerais consolidates a robust asset portfolio including the Baratinha, Mongais, and Pedra Branca projects. The company targets 10+ million tonnes annually by 2030, representing approximately 2.3% of Brazil's current national production. This positioning establishes Bemisa amongst significant national producers within the mid-tier segment.

Gerdau's integrated mining platform involves R$ 3.2 billion investment commitments between 2023-2026 focused on long-term steelmaking feedstock security. This sustainable mining platform approach integrates environmental and operational efficiency criteria into expansion strategy, addressing both regulatory requirements and customer ESG expectations.

Advanced technology implementation characterises expansion approaches across multiple producers:

| Company | Investment | Capacity Impact | Timeline | Focus Area |

|---|---|---|---|---|

| ArcelorMittal | R$ 2.5 billion | 1.6 Mt → 4.5 Mt | Completed 2025 | Capacity expansion |

| Bemisa | Undisclosed | Target 10+ Mt/year | By 2030 | Regional consolidation |

| Gerdau | R$ 3.2 billion | Platform development | 2023-2026 | Sustainable mining |

| Cedro Mineração | Technology focus | Mine life extension | Ongoing | Operational optimisation |

These expansion initiatives reflect sustained producer confidence in market resilience and long-term steel demand fundamentals, despite reduced Chinese consumption patterns and price volatility concerns.

What Infrastructure Developments Support Production Growth?

Logistics Network Optimisation

Anglo American's Minas-Rio pipeline system exemplifies critical infrastructure enabling large-scale iron ore production in Brazil. The 529-kilometre pipeline traverses 33 municipalities across Minas Gerais and Rio de Janeiro states, terminating at Porto do Açu in São João da Barra. This integrated system handles transport, filtration, and export of premium-grade iron ore, representing one of the world's longest iron ore slurry pipelines.

Logistics infrastructure continues as a fundamental constraint on production scaling. The Minas-Rio system demonstrates how major producers address transportation bottlenecks through dedicated infrastructure investment rather than relying on shared rail or trucking networks. This approach provides operational control and capacity certainty essential for large-volume mining operations.

Port capacity optimisation at the Açu terminal enables efficient export processing with reduced handling costs compared to traditional rail-to-port transportation methods. The filtration and export facility specifically handles Anglo American's premium iron ore products, supporting quality-focused market positioning strategies.

Sustainable Mining Technology Implementation

Digital transformation initiatives integrate across infrastructure development, creating smart mining ecosystems rather than traditional mechanical operations. Industry analysis confirms that digital transformation plays a central role in strategic development, incorporating solutions such as:

- Artificial Intelligence applications for operational optimisation

- Connected sensor networks enabling real-time monitoring

- Remote operations capabilities reducing on-site personnel requirements

The Remote Operations Centre inaugurated in 2025 centralises monitoring and operation of mining equipment across the extensive Minas-Rio system. This represents practical implementation of Industry 4.0 technologies enabling:

- Centralised equipment monitoring: Real-time oversight of distributed mining and pipeline assets

- Predictive maintenance: Data-driven scheduling reducing unplanned downtime

- Safety enhancement: Automated hazard detection and response systems

- Operational optimisation: Performance analytics driving efficiency improvements

Brazil Iron's pioneering "Green Iron" initiative promises revolutionary technology implementation with the Hot Briquetted Iron (HBI) project targeting 2030 production launch. This initiative requires R$ 1.7 billion research investment to develop zero net greenhouse gas emission production methods, positioning Brazil as a leader in decarbonised iron ore processing.

Furthermore, this initiative aligns with growing mine reclamation innovation practices across the industry. The project represents the first domestic facility producing HBI with carbon-neutral credentials, addressing international steel industry decarbonisation requirements whilst creating premium product differentiation opportunities.

How Do Market Fundamentals Support Continued Investment?

Price Resilience Analysis

Market stability above critical profitability thresholds enables sustained investment in iron ore production in Brazil despite global demand uncertainties. Industry analysis confirms that iron ore prices have remained above USD 100 per tonne on average, maintaining cautious optimism among commodity producers throughout market oscillations.

This price resilience stems from several fundamental factors:

- Supply discipline: Global producers maintaining capacity utilisation rates aligned with demand patterns

- Quality premiums: Higher-grade Brazilian ore commanding price premiums over lower-quality alternatives

- Infrastructure constraints: Limited ability for rapid capacity expansion creating supply stability

- China adaptation: Gradual demand adjustment rather than precipitous decline enabling market adaptation

Nevertheless, producers must remain vigilant regarding potential iron ore price decline scenarios as global markets evolve. Chinese demand patterns remain the dominant influence on global iron ore pricing, though reduced consumption levels have stabilised rather than collapsed. China continues as the largest consumer of raw material for the steel industry, meaning Brazilian producers must adapt to modified demand characteristics whilst maintaining production efficiency.

Reserve Base and Long-Term Viability

Brazil's iron ore reserve foundation supports sustained production expansion with 29 billion tonnes of proven reserves globally ranked. This substantial reserve base enables mine life extension projects across multiple operations, supporting long-term investment confidence amongst producers and financial institutions.

Resource incorporation studies are advancing at Serra da Serpentina and Serra do Sapo locations, where Anglo American's Minas-Rio operation currently extracts premium-grade ore. These viability studies will define optimal strategies for incorporating additional mineral resources, potentially extending operational lifespans significantly beyond current mine plans.

Mine life extension initiatives across the industry typically target 10+ year extensions through advanced geological modelling, improved extraction techniques, and resource optimisation studies. Cedro Mineração exemplifies this approach through technology intensification at Nova Lima and Mariana operations, aiming to amplify mine life significantly whilst reducing environmental impacts.

The combination of substantial reserves and technological advancement creates favourable conditions for continued investment despite market volatility. Producers can plan long-term development projects with confidence in feedstock availability and operational viability.

What Growth Projections Define Brazil's Iron Ore Future?

Production Capacity Forecasting

Iron ore production in Brazil faces robust growth trajectory projections despite current market uncertainties. According to GlobalData analysis, industry forecasts anticipate 544.6 million tonnes projected output by 2030, representing a 3.8% compound annual growth rate from current production levels of approximately 440 million tonnes.

This expansion trajectory exceeds global market growth expectations, suggesting Brazilian producers will capture increased market share through competitive positioning and quality differentiation strategies. The growth projection incorporates both capacity expansion projects and operational efficiency improvements across major producers.

Regional expansion patterns indicate diversification beyond traditional Minas Gerais and Pará concentration. While these states will maintain dominant production positions, secondary regions may contribute incremental capacity as geological exploration identifies viable deposits and infrastructure development enables economic extraction.

Production capacity breakdown by timeline:

| Period | Projected Output (Mt) | Growth Rate | Key Drivers |

|---|---|---|---|

| 2024 | 440 | Baseline | Current capacity utilisation |

| 2026 | 480-500 | 4.5-6.8% | Major expansion completions |

| 2028 | 510-530 | 3.1-3.9% | Technology optimisation |

| 2030 | 544.6 | 3.3% | Full capacity realisation |

Market Segment Evolution

Pellet feed demand acceleration represents a critical growth driver, with projections indicating 3.5% compound annual growth rate through 2030. This segment evolution reflects steel industry preferences for processed iron ore products enabling improved blast furnace efficiency and reduced emissions.

Brazilian producers are positioning for this market shift through pelletisation infrastructure investment and quality enhancement programmes. Companies like Herculano are directing investments toward high-quality pellet feed production expansion at Itabirito operations, adding portfolio value whilst contributing to steel chain decarbonisation objectives.

Market value projections anticipate growth to USD 12.76 billion by 2030 based on combined volume expansion and premium pricing for higher-grade products. This represents substantial increase from current USD 11.1 billion market value achieved in 2024.

Product mix evolution expectations:

- Premium pellet feed: Increasing share as steel industry prioritises efficiency

- High-grade fines: Continued demand from integrated steel producers

- Direct reduction grade: Growing segment for HBI and DRI production

- Lump ore: Specialised applications maintaining niche market presence

The market segment evolution supports producer strategies emphasising quality over quantity, enabling sustainable profitability despite potential volume competition from other global producers.

The next major ASX story will hit our subscribers first

Which Challenges Could Impact Production Scaling?

Environmental and Regulatory Considerations

Iron ore production in Brazil confronts increasingly stringent environmental compliance requirements that could constrain expansion timelines and increase development costs. Regulatory frameworks now mandate comprehensive environmental impact assessments, community engagement protocols, and long-term restoration planning for all major mining projects.

Deforestation mitigation requirements present particular challenges for operations in sensitive ecosystems. Mining companies must demonstrate net-positive environmental impact through restoration initiatives, biodiversity protection measures, and carbon offset programmes. These requirements add significant complexity and cost to project development.

Water resource management protocols require sophisticated monitoring and treatment systems, particularly for operations utilising water-intensive processing techniques. The slurry pipeline transport method employed by the Minas-Rio system exemplifies water-efficient alternatives to traditional transportation methods.

Indigenous rights compliance frameworks necessitate extensive consultation processes and benefit-sharing agreements with traditional communities. These requirements can extend project development timelines whilst creating ongoing operational obligations throughout mine life cycles.

Infrastructure and Social Factors

Transportation bottleneck resolution remains critical for scaling production beyond current levels. While major producers like Anglo American have invested in dedicated pipeline systems, many smaller operations rely on shared rail and highway networks with limited capacity expansion potential.

Community engagement and land dispute management present ongoing challenges requiring sustained investment in social programmes and stakeholder relations. Mining operations must maintain positive relationships with 33+ municipalities across operational footprints whilst managing competing interests amongst various stakeholder groups.

Workforce development for technology integration becomes increasingly important as digital transformation accelerates. Operations requiring remote monitoring capabilities, AI-assisted decision making, and predictive maintenance systems demand skilled technicians and engineers with specialised training.

Critical challenge categories requiring strategic management:

- Regulatory compliance: Environmental permits, monitoring requirements, restoration obligations

- Social licence: Community relations, benefit sharing, dispute resolution

- Technical capability: Skilled workforce, technology integration, innovation capacity

- Infrastructure adequacy: Transportation networks, utility access, communication systems

Investment disclaimer: This analysis contains forward-looking projections and market assessments that involve inherent risks and uncertainties. Actual production volumes, pricing levels, and market developments may differ materially from projections presented. Investors should conduct independent due diligence and consider professional advice before making investment decisions related to Brazilian iron ore producers or related commodities.

The successful navigation of these challenges will determine which producers achieve projected growth targets whilst maintaining sustainable operations aligned with evolving regulatory and social expectations. Companies demonstrating proactive approach to challenge management may capture disproportionate market opportunities as the industry consolidates around best-practice operators.

Looking to Capitalise on Brazil's Iron Ore Expansion?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the market.