July 2, 2026

Why Corporate Scale Determines Which Uranium Projects Actually Get Built

The uranium development sector has a well-documented financing problem, and it is not primarily about project quality. Across the past decade, dozens of technically sound uranium deposits have stalled at the feasibility stage, not because the geology failed, but because the corporate structure around them was too thin to absorb the capital requirements of large-scale mine construction. A single-asset developer facing a AUD$300 million capital expenditure requirement is, from a financing institution's perspective, a binary bet. There is no fallback, no offsetting cash flow from a parallel asset, and no portfolio-level narrative to anchor institutional confidence.

This structural ceiling is precisely what makes the IsoEnergy Toro Energy acquisition of Wiluna uranium project strategically significant, not just as a resource addition, but as a reconfiguration of the financing equation for one of Australia's largest undeveloped uranium deposits. Understanding the broader uranium market dynamics helps contextualise why this transaction matters so much for the sector right now.

When big ASX news breaks, our subscribers know first

The Credibility Gap That Trapped Wiluna Under Single-Asset Ownership

Before examining the mechanics of the transaction, it is worth understanding why a project with 87.8 million tonnes of resource at 331 ppm and both federal and state approvals dating back to 2012 and 2013 had not progressed further under its previous owner.

Toro Energy was not a poorly managed company. The Wiluna Uranium Project's regulatory groundwork was genuinely advanced by any standard within Australia's uranium development landscape. Federal and state approvals secured over a decade ago represent a substantial lead over comparable development-stage projects, many of which are still navigating environmental assessment processes. However, the market consistently applied a credibility discount to the project because investors could not construct a plausible financing narrative for a microcap developer facing construction capital of approximately AUD$300 million.

The development capital requirement at Wiluna was not extraordinary by mining industry standards, but it was effectively unmanageable for a standalone microcap operator. That mismatch between project scale and corporate capacity is precisely the structural problem that the IsoEnergy acquisition resolves.

This is a pattern repeating across the uranium development sector. Projects with sound geology, completed approvals, and demonstrable resource bases remain stranded at the development stage because single-asset corporate structures cannot credibly bridge the gap between early-stage technical work and construction financing. The consolidation wave now moving through uranium development is, in large part, a market correction to this structural inefficiency. Furthermore, the uranium supply challenges facing the sector globally make this structural resolution even more pressing.

What the Wiluna Uranium Project Actually Contains

The Wiluna project sits within Western Australia's arid interior, encompassing three distinct deposits: Lake Way, Lake Maitland, and Centipede-Millipede. Each exhibits near-surface mineralisation, with uranium occurring at approximately ten metres depth across much of the resource footprint. This shallow profile is commercially important because it supports conventional open-pit mining methods rather than the more capital-intensive underground approaches required at deeper deposits.

Total Resource Snapshot:

| Category | Tonnes | Grade (ppm U₃O₈) | Contained U₃O₈ (Mlbs) |

|---|---|---|---|

| Measured + Indicated | Majority of 87.8Mt | 331 ppm average | ~69.1 million lbs |

| Inferred | Remaining fraction | 331 ppm average | ~4.5 million lbs |

| Total Resource | 87.8 million tonnes | 331 ppm at 100 ppm cut-off | ~73.6 million lbs |

The near-surface character of Wiluna's mineralisation also has implications for the stripping ratio, the volume of waste material that must be removed per tonne of ore extracted. Lower stripping ratios translate directly into lower operating costs, which matters considerably when evaluating the project's long-term production economics. Combined with the existing approval framework, this geological profile places Wiluna in a relatively favourable position compared to many Australian uranium development assets.

How Wiluna's Geology Compares Globally

Western Australia's Wiluna region is geologically distinct from the high-grade unconformity-hosted uranium deposits that characterise Saskatchewan's Athabasca Basin. Wiluna's resource is a calcrete-hosted uranium deposit, where uranium mineralisation has concentrated through supergene processes in near-surface calcareous sediments. This deposit style is more comparable to the Langer Heinrich mine in Namibia than to the deep, ultra-high-grade systems in Canada.

Calcrete deposits typically offer large tonnage at moderate grades, and their shallow geometry makes them amenable to low-cost bulk mining methods. Consequently, Wiluna's open-pit development pathway remains economically plausible despite a grade that would be considered low by Athabasca Basin standards. In addition, Western Australia uranium mining continues to attract significant attention given the region's regulatory maturity relative to other Australian states.

How the IsoEnergy Toro Energy Acquisition Was Structured

Transaction Mechanics and Valuation

The IsoEnergy acquisition of Toro was executed as an all-share transaction via a court-approved scheme of arrangement, a legal mechanism commonly used in Australian public company takeovers that requires shareholder approval and judicial sanction before implementation.

Key Transaction Parameters:

| Parameter | Detail |

|---|---|

| Transaction value | |

| Exchange ratio | 0.036 IsoEnergy shares per Toro share |

| New IsoEnergy shares issued | 4,359,568 common shares |

| Toro ASX suspension | June 16, 2026 |

| ASX delisting date | On or around June 26, 2026 |

| Acquisition completion | June 25, 2026 |

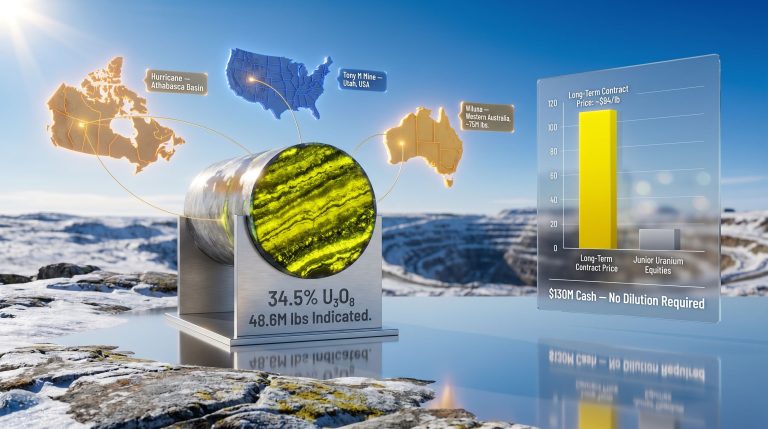

| IsoEnergy cash position (post-deal) | ~C$130.5 million |

The all-share structure is notable for what it reveals about IsoEnergy's capital management priorities. Rather than deploying cash to fund the acquisition, the company preserved its C$130.5 million balance sheet for multi-year technical programmes across all three assets. This approach avoids the dilutive equity raises that would have been necessary to fund the same capital deployment through a cash transaction, and it signals management's intent to use the balance sheet for project advancement rather than corporate transactions.

What the Pro Forma Portfolio Looks Like

Following the acquisition, IsoEnergy's NI 43-101 compliant measured and indicated resources stand at approximately 55.2 million pounds, with the Wiluna addition contributing approximately 75 million pounds in total uranium resources across all classification categories. The company is now listed on both the TSX and NYSE American exchanges, providing access to both Canadian and United States institutional capital markets. The current uranium supply-demand volatility makes this access to capital markets particularly valuable for advancing a portfolio of this scale.

Three Assets, Three Development Philosophies

The Multi-Jurisdiction Architecture

One of the less-discussed dimensions of the IsoEnergy Toro Energy acquisition is how it completes a genuinely diversified jurisdictional footprint. The three core assets now occupy three distinct uranium jurisdictions, each with different risk profiles, regulatory environments, and market dynamics.

Portfolio Overview by Asset:

| Asset | Location | Stage | Primary Near-Term Objective |

|---|---|---|---|

| Hurricane | Saskatchewan, Canada | Exploration and resource growth | Hurricane South Trend drilling; resource expansion |

| Tony M | Utah, United States | Economic validation | Updated PEA from 2,000-tonne bulk sample |

| Wiluna | Western Australia, Australia | Technical studies | JORC-to-NI 43-101 conversion; scoping to PEA upgrade |

Saskatchewan's Athabasca Basin is globally recognised as the premier high-grade uranium district, with average grades at some deposits exceeding 20% uranium, orders of magnitude above the global average. Hurricane's positioning within this geological province provides a high-optionality exploration asset that could generate significant resource growth with relatively modest drilling capital.

Utah's uranium sector benefits from proximity to established toll milling infrastructure, making Tony M one of the few development-stage uranium assets in the United States with a defined, near-term pathway to production without requiring greenfield processing construction. Australia sits in a different category entirely. Western Australia's uranium regulatory framework is mature, and Wiluna's pre-secured approvals represent a meaningful barrier to entry that competing projects in earlier stages cannot easily replicate.

The Tony M Bulk Sample Programme: Why the Numbers Matter

Beneficiation and What It Means for Project Economics

The 2,000-tonne bulk sample programme at Tony M is generating data that goes well beyond confirming grade continuity. The programme is specifically testing beneficiation, a process that uses physical separation techniques to concentrate uranium into a smaller volume of material before it is transported to a toll mill for processing.

The result from initial test work is striking: beneficiation removed 75% of the total mined material volume while retaining more than 90% of the contained uranium. To understand why this metric is transformative for Tony M's economics, it is necessary to understand how toll milling costs are typically structured.

Why the Beneficiation Result Changes the Cost Model:

- Toll milling fees are generally charged on a per-tonne-of-material-processed basis

- Haulage to the mill is a significant operating cost for Utah uranium projects, given the remote locations of many ore bodies

- Reducing transport volume by 75% while preserving 90% of uranium content compresses the cost per pound of uranium produced

- A lower cost per pound improves the project's margin at any given uranium spot price, widening the range of market conditions under which restart becomes economically viable

The critical question is whether laboratory-scale beneficiation results translate to bulk operating conditions. The 2,000-tonne bulk sample is designed specifically to answer this question at a scale that more closely mirrors commercial production. This is precisely why management has chosen to complete this programme before committing to a restart decision, rather than relying on smaller-scale test data.

The Sequenced Restart Logic

IsoEnergy's management has articulated a deliberate philosophy around Tony M's restart timing. The company holds existing permits, infrastructure, and a toll milling agreement, meaning the mechanical prerequisites for production are largely satisfied. Despite this, management has indicated that patience takes precedence over speed to first production, with the goal of maximising per-pound value rather than optimising for earliest possible output.

This approach is consistent with a broader truth about uranium project economics that is sometimes overlooked in retail investor analysis. The timing of first production determines the contracting environment available for future uranium sales. A company that rushes into production during a period of spot price softness may lock in offtake agreements at lower prices, while a developer that completes technical validation during the same period retains the flexibility to contract when conditions are more favourable.

Preserving optionality around production timing is not a passive strategy. It is an active decision to treat the uranium sales contracting process as a variable to be optimised, not a fixed constraint to be accepted.

The next major ASX story will hit our subscribers first

Wiluna's Technical Path to a Development Decision

The JORC-to-NI 43-101 Conversion: More Than Paperwork

The conversion of Wiluna's existing JORC-compliant resources to NI 43-101 standard is frequently described in corporate communications as a technical or administrative exercise. In practice, it is considerably more consequential than that framing suggests.

NI 43-101, administered by the Canadian Securities Administrators, requires that all resource estimates be prepared by or under the supervision of an independent Qualified Person who meets specific professional registration criteria. The standard imposes strict requirements on data verification, sampling methodology documentation, geological modelling transparency, and resource classification criteria. When converting a JORC resource to NI 43-101 compliance, the independent QP must independently verify all underlying data rather than simply accepting the prior resource estimate at face value.

Why NI 43-101 Compliance Matters for Capital Access:

- North American institutional investors and lenders typically require NI 43-101 compliance before committing capital

- TSX listing rules mandate NI 43-101 disclosure for material mineral properties

- The conversion process can result in resource reclassification if the QP identifies data gaps or methodology differences between JORC and NI 43-101 standards

- Successful conversion establishes a credible, independently verified baseline for subsequent economic studies

Beyond resource conversion, the planned technical programme at Wiluna includes additional infill and extensional drilling to support resource category upgrades, followed by advancement of the existing scoping study to a full Preliminary Economic Assessment. The scoping study already exists, which means the PEA work builds on a foundation rather than starting from zero, consequently compressing the timeline to a credible technical and economic baseline.

Portfolio Construction as a Financing Strategy

Why Multi-Asset Scale Changes the Institutional Conversation

The financing challenge for uranium developers is not simply about having enough cash on hand. Institutional lenders and project finance providers assess risk at the corporate level, not just the project level. A single-asset developer with a technically superior project may still struggle to access project finance if the corporate structure lacks the resilience to absorb unexpected delays, cost overruns, or temporary market dislocations.

Single-Asset vs. Multi-Asset Developer Comparison:

| Risk Dimension | Single-Asset Developer | IsoEnergy Post-Acquisition |

|---|---|---|

| Project risk concentration | Entire corporate value in one asset | Distributed across three assets |

| Capital deployment flexibility | Binary: advance or suspend | Staged allocation by project maturity |

| Balance sheet resilience | Dependent on single project milestones | C$130.5 million across multi-year programme |

| Jurisdictional exposure | Single country risk | Canada, USA, Australia |

| Institutional financing appeal | Constrained without project de-risking | Portfolio narrative supports broader access |

| Execution risk profile | Single construction cycle risk | Staggered development reduces peak exposure |

The approximately C$130.5 million cash position is particularly significant in the context of uranium development timelines. A typical uranium development programme from scoping study to production decision spans five to ten years, and a company that enters this process without sufficient capital depth is forced into repeat equity raises. Each of these dilutes existing shareholders and signals financial fragility to potential lenders. IsoEnergy's balance sheet depth provides the runway to advance all three assets through their respective technical programmes without immediate dilution pressure.

Forward Catalysts Across All Three Assets

Near-Term Milestones for Investors to Monitor

The IsoEnergy Toro Energy acquisition of Wiluna uranium project sets up a period of concurrent technical activity across all three development assets. Each catalyst carries different implications for the investment thesis, and evolving uranium market trends will influence how the market values each milestone as it is delivered.

Tony M (Utah):

- Updated PEA incorporating beneficiation results targeted for 2026

- The PEA outcome will test whether laboratory-scale beneficiation efficiency translates to commercial assumptions

- A favourable PEA could accelerate the restart decision framework and influence uranium contracting strategy

Wiluna (Western Australia):

- NI 43-101 resource conversion completion across Lake Way, Lake Maitland, and Centipede-Millipede

- Additional drilling results targeting resource category upgrades and potential resource extensions

- Advancement of the existing scoping study to PEA standard, establishing the first NI 43-101 compliant economic study for the project

Hurricane (Saskatchewan):

- Ongoing drilling at the Hurricane South Trend, where recent programmes have encountered mineralisation beyond the current resource boundary

- Results will clarify the potential scale of resource growth at one of Canada's most geologically prospective uranium districts

- Resource expansion at Hurricane would add high-grade optionality to a portfolio that currently skews toward larger, lower-grade bulk-mineable assets

Uranium Market Context

Global nuclear capacity additions, utility restocking activity, and the long lead times inherent in uranium mine development are all contributing to a market environment where development-stage assets are attracting renewed institutional interest. IsoEnergy's completed acquisition of Toro Energy positions the company to capitalise on this environment with a genuinely diversified portfolio spanning three credible uranium jurisdictions.

Western Australia's Wiluna region benefits from an established federal and state regulatory framework, with the project's existing approvals representing a head start that would take years and considerable capital to replicate from a greenfield position. The Athabasca Basin continues to host some of the world's most economically significant uranium deposits, and IsoEnergy's Hurricane asset provides direct exposure to further exploration upside in this premier district. Meanwhile, the United States domestic uranium landscape adds a strategic dimension to Tony M's positioning, given ongoing discussions around domestic nuclear fuel supply security.

This article is for informational purposes only and does not constitute financial or investment advice. Forward-looking statements involve risks and uncertainties, and actual outcomes may differ materially from those projected. Readers should conduct their own due diligence before making investment decisions.

Want to Track the Next Major Uranium Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex mineral data into actionable insights for both short-term traders and long-term investors. Explore how historic discoveries have generated exceptional returns on the Discovery Alert discoveries page, then begin your 14-day free trial to position yourself ahead of the market.