August 4, 2026

When Commodity Traders Become Mine Financiers: A Structural Shift in Nuclear Fuel Capital

The uranium sector has spent the better part of a decade rebuilding investor confidence after the post-Fukushima collapse reshaped the nuclear fuel landscape from 2011 onward. What is less discussed, however, is how the financing architecture supporting uranium mine restarts has quietly evolved alongside the commodity's price recovery. Traditional project lenders, constrained by ESG mandates and risk-averse credit committees, have increasingly stepped back from early-stage and restart-phase uranium assets. Into that vacuum, a different class of financier has entered: the global commodity trading house.

The Mercuria uranium financing deal with Lotus Resources is not simply a transaction between two companies. It represents a structural template that could reshape how junior uranium producers access capital during the critical ramp-up phase, and it signals that at least one major trading house views the uranium supply chain as a long-term commercial priority worth financing from the ground up.

When big ASX news breaks, our subscribers know first

Understanding the Mechanics: Why Prepayment Agreements Differ From Conventional Debt

To appreciate why this deal matters, it is worth understanding how prepayment agreements function as a financing instrument, because they operate on fundamentally different logic than a project loan.

In a conventional debt facility, a lender advances capital and expects repayment through cash interest and principal over time. The lender's risk is primarily credit risk: will the borrower generate enough cash flow to service the debt? In a prepayment agreement, the financier advances capital and receives commodity marketing rights in return. The risk profile shifts toward production delivery and commodity price exposure, rather than balance sheet credit metrics.

Comparing the two structures side by side reveals why trading houses prefer prepayment:

| Feature | Prepayment Agreement | Traditional Debt Facility |

|---|---|---|

| Repayment mechanism | Future commodity delivery | Cash interest and principal |

| Financier's primary risk | Production volume and commodity price | Credit and liquidity |

| Borrower retains offtake control | Typically yes, with carve-outs | Usually yes |

| Security required | Production volume commitment | Asset or corporate guarantee |

| Typical application | Working capital and operational ramp-up | Capital expenditure and development |

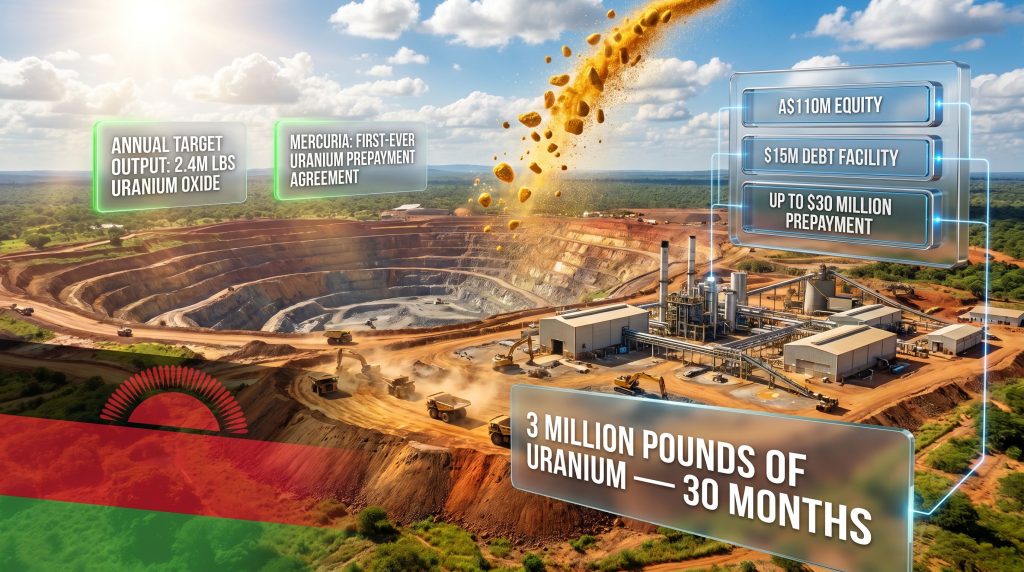

For Mercuria, advancing capital in exchange for the right to market 3 million pounds of uranium over a 30-month period is not a lending exercise. It is a commodity positioning exercise, one that gives the trading house flow access to a producing African uranium asset without bearing the capital intensity of direct mine ownership.

The Kayelekera Mine: Operational History and the Acid Plant Problem

How Did Kayelekera Reach This Point?

The Kayelekera production comeback story is one of uranium market cycles. The mine in Malawi was originally closed in 2014, a direct consequence of the prolonged price depression that followed the Fukushima disaster. For nearly six years, the asset sat idle as uranium prices failed to recover to economically viable levels for the operation.

Lotus Resources acquired Kayelekera in 2020, positioning the company ahead of what it believed would be a structural demand recovery in nuclear fuel markets. That thesis proved well-timed: uranium prices have recovered substantially from their post-Fukushima lows, driven by tightening mine supply and accelerating reactor construction globally. Furthermore, uranium market dynamics have continued to evolve in ways that reinforce the commercial logic of the restart.

The mine was restarted in 2024, targeting annual production of 2.4 million pounds of uranium oxide. However, a specific operational challenge interrupted that ramp-up: disruptions to sulfuric acid supply chains, triggered by geopolitical instability following the Iran conflict.

Sulfuric acid is not a peripheral input in uranium processing. In heap leach and acid leach extraction methods, it is the primary reagent that dissolves uranium from crushed ore, making it as essential to the operation as the ore itself.

Without reliable acid supply, Kayelekera cannot process ore at scale. The damage to the mine's acid plant infrastructure, combined with supply chain disruptions, created the specific operational gap that the Mercuria prepayment facility is designed to address. A portion of the up to $30 million facility is earmarked specifically for acid plant repair and restoration, making this a targeted capital injection rather than general corporate funding.

Kayelekera Production and Deal Snapshot:

| Metric | Detail |

|---|---|

| Annual production target | 2.4 million pounds uranium oxide |

| Prepayment volume commitment | 3 million pounds over 30 months |

| Facility size | Up to $30 million |

| Funding availability | September 2025 at earliest |

| Mine location | Kayelekera, Malawi |

| Mine status | Restarted 2024, temporarily paused |

The Mercuria Uranium Financing Deal With Lotus Resources: What the Term Sheet Says

Lotus Resources has confirmed signing a non-binding term sheet with Mercuria Energy Group for a prepayment facility linked to Kayelekera production. The deal, if finalised, would see Mercuria advance up to $30 million in exchange for the right to market 3 million pounds of uranium across a 30-month window.

Critically, Lotus has made clear that it retains full control over customer selection under this arrangement. Existing utility offtake partners are not displaced by Mercuria's marketing rights. The trading house gains commodity flow access, but the final buyer relationships remain with Lotus. This dual-layer design is deliberate and commercially sophisticated:

- It preserves Lotus's long-term relationships with power utilities, which are typically built over years and are not easily reconstructed.

- It gives Mercuria the commodity volume it needs to justify advancing capital, without requiring control over the utility supply chain.

- It protects Lotus from being perceived as having surrendered strategic control over its own production.

The non-binding nature of the current term sheet is a material consideration. The $30 million is not yet guaranteed, and the funding timeline extending to September at the earliest means Lotus must manage near-term working capital requirements through its existing facilities in the interim.

Lotus Resources' Multi-Layer Capital Stack: A Financing Blueprint Worth Studying

What makes the Lotus Resources approach particularly instructive for the junior uranium sector is the deliberate construction of a diversified capital stack rather than dependence on any single financing source.

The company's financing architecture for the Kayelekera restart programme comprises four distinct layers:

- Equity: An A$110 million placement to fund the core mine restart capital programme.

- Debt: A $15 million unsecured loan facility secured from Curzon Uranium to bridge liquidity gaps.

- Offtake monetisation: Two uranium offtake agreements totalling 1.5 million pounds for the 2026 to 2029 delivery period, de-risking the revenue profile.

- Prepayment: The Mercuria facility adding a commodity-linked working capital layer for operational continuity.

Each instrument addresses a different part of the project risk profile. Equity funds capital expenditure without creating debt service obligations. The Curzon loan bridges near-term liquidity. Offtake agreements provide revenue certainty to underpin the business case. The Mercuria prepayment facility specifically addresses the operational working capital needs of the production ramp-up phase.

This financing approach mirrors strategies employed by mid-tier gold producers during expansion phases, where stacking complementary instruments reduces the single-point-of-failure risk that has historically plagued single-debt-facility junior miners.

Why Mercuria Is Making Its First Uranium Financing Move Now

Mercuria's decision to enter uranium project financing at this point in the cycle is not coincidental. Several converging market dynamics have made uranium project finance attractive to trading houses that previously focused exclusively on price arbitrage and physical commodity flows. In addition, the interplay between spot versus term prices has created structural incentives for trading houses to secure long-term commodity flow access.

The macro demand drivers attracting institutional attention to uranium supply:

- China's nuclear reactor build programme represents the world's largest single demand growth pipeline for uranium, with dozens of units under construction and more in planning.

- European utilities are reassessing long-term nuclear fuel supply security following the disruption to Russian supply chains, creating demand for non-Russian uranium sources.

- The Russian uranium import ban has accelerated Western utility demand for alternative supply sources, further tightening the available production pool.

- New greenfield uranium mine development timelines typically span one to two decades, meaning supply additions cannot easily respond to demand increases in the near term.

- Kazakhstan, the world's largest uranium producer, has faced its own production challenges, contributing to near-term supply tightness.

For a trading house like Mercuria, which has historically dominated oil, gas, and metals markets, uranium represents a new commodity vertical with growing strategic importance. Prepayment agreements specifically offer first-mover marketing access to production streams before competition for uranium supply intensifies further.

By financing Kayelekera's restart, Mercuria effectively buys its way into a producing African uranium asset's supply chain at a fraction of the cost of direct mine ownership, while securing the commodity flow that matters most for a trading operation.

The next major ASX story will hit our subscribers first

African Uranium and the Global Supply Diversification Imperative

Why Does Malawi Matter to Western Utilities?

Kayelekera's position in Malawi carries significance beyond the individual transaction. Western utilities and their regulators have become acutely focused on uranium supply chain diversification, seeking alternatives to the Kazakhstan-Russia supply axis that has historically dominated global uranium production.

African uranium assets, including those in Niger, Namibia, and now increasingly Malawi, are attracting renewed interest as part of a broader supply resilience strategy. Kayelekera's restart, commercially validated by the Mercuria financing arrangement, positions Malawi as a meaningful contributor to this diversification effort.

The deal also functions as a form of third-party commercial validation: when a major commodity trading house is willing to advance $30 million against future Kayelekera production, it signals to the broader market that the asset is operationally credible and commercially financeable.

Risks That Junior Miners and Investors Should Not Overlook

The Mercuria uranium financing deal with Lotus Resources carries genuine strategic significance, but a balanced assessment requires acknowledging the risks embedded in this structure. Consequently, understanding the broader context of uranium supply volatility is essential before drawing conclusions about the deal's near-term impact.

Key risk considerations for the Kayelekera restart programme:

- The current term sheet is non-binding, meaning the $30 million facility is not yet contractually secured and could change in terms or fail to finalise.

- The September funding timeline creates a working capital gap that must be managed through existing facilities, including the Curzon loan, in the interim.

- Acid plant repair timelines introduce operational uncertainty. If restoration takes longer than anticipated, the production ramp-up could be delayed, creating volume shortfall risk under the prepayment commitment.

- Sulfuric acid supply chain vulnerability has a geopolitical dimension that is not fully resolved by the financing arrangement itself.

- Prepayment volume commitments create delivery obligations. If Kayelekera underperforms against its 2.4 million pound annual production target, Lotus may face renegotiation pressure on the marketing volume commitment.

Investors and market observers should treat the deal announcement as a positive structural development while recognising that the non-binding term sheet represents intent rather than certainty. The finalisation of the facility, and the operational resolution of the acid plant issue, are the milestones that will determine whether this financing template delivers its projected value.

What This Transaction Signals for the Broader Junior Uranium Financing Market

The Mercuria uranium financing deal with Lotus Resources is widely viewed as a proof-of-concept transaction for trading house involvement in uranium project finance. Other trading houses that have watched uranium's structural recovery but hesitated to commit capital will observe this deal closely.

Junior miners with the following characteristics are likely to be most attractive for similar prepayment structures going forward:

- A defined and credible production profile, ideally from an asset already in production or with demonstrated restart capability.

- Established offtake relationships with creditworthy utilities, which provide the marketing counterparty certainty that trading houses require.

- A commodity with liquid spot and forward markets, allowing trading houses to hedge their commodity price exposure.

- Operational assets in politically stable jurisdictions with clear regulatory frameworks, reducing execution risk.

The emergence of prepayment finance as a mainstream capital instrument for uranium producers represents a maturation of the sector's financing ecosystem. For years, junior uranium miners faced a binary choice between equity dilution and limited debt options. The trading house prepayment model introduces a third pathway: commodity-linked working capital that aligns the interests of the miner and the financier around production success rather than debt service mechanics.

However, as Canaccord Genuity's involvement in the broader Lotus Resources capital raise demonstrates, institutional appetite for well-structured uranium project finance is not limited to commodity traders alone. As global uranium demand accelerates through the late 2020s and supply additions remain structurally constrained, the Mercuria-Lotus transaction may ultimately be remembered as the deal that opened the door to a new era of commodity trader participation in nuclear fuel supply chain finance.

This article is intended for informational purposes only and does not constitute financial or investment advice. References to forward-looking statements, production targets, and financing timelines involve uncertainty and may not be achieved. Readers should conduct independent due diligence before making any investment decisions related to uranium mining companies or commodity markets.

Want to Catch the Next Major Uranium Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the next significant find.