June 30, 2026

Why Uranium Fundamentals No Longer Guarantee Junior Equity Returns

The uranium market is experiencing one of its most paradoxical periods in recent memory. Understanding the IsoEnergy uranium portfolio strategy requires context about where long-term contract prices stand — approximately $94 per pound as reported by TricUX — a level within striking distance of all-time highs. Spot prices hover around $85 per pound, subject to volatility but structurally elevated relative to the prior decade. Yet across the junior uranium equity landscape, more companies are trading near their 52-week lows than their 52-week highs.

This disconnect is not random. It reflects a deepening divide between two types of uranium developers: those with credible, diversified, execution-ready portfolios attracting institutional capital, and those with concentrated single-asset exposure increasingly being treated as uninvestable by sophisticated allocators.

Understanding how this bifurcation is playing out — and which strategic frameworks are most likely to capture value across the next phase of the uranium cycle — is essential context. Furthermore, examining the uranium market dynamics at play helps clarify why some developers are pulling ahead of others.

When big ASX news breaks, our subscribers know first

The Hidden Risk Inside Single-Asset Uranium Companies

Binary Outcomes and the Cost of Concentration

Single-asset uranium companies carry a structural vulnerability that becomes increasingly visible during periods of market stress. When a company's entire value proposition depends on one deposit in one jurisdiction, any adverse development — a permitting delay, a geopolitical shift, a technical setback, or a wildfire evacuation — produces consequences that are disproportionate to the underlying event.

This is not a theoretical risk. Across the past two to three years, uranium sector restarts have consistently failed to deliver on published timelines. Each failure has eroded investor confidence not just in the individual company, but in the broader sector's capacity to execute. The cumulative effect has been a repricing of execution risk across all junior uranium developers, regardless of asset quality.

Portfolio sequencing — the deliberate staging of multiple assets across different jurisdictions and development timelines — is emerging as the structural answer to this problem. Rather than concentrating risk on a single binary outcome, a sequenced multi-asset portfolio distributes both risk and upside across multiple catalysts, multiple jurisdictions, and multiple market windows.

Why Institutional Capital Is Migrating Up the Quality Curve

The uranium equity market is not simply underperforming due to sentiment. It is undergoing a structural sorting process. Institutional allocators who previously engaged broadly with uranium equities are now applying tighter filters: tier-one jurisdiction only, minimum market capitalisation thresholds, demonstrated management execution, and balance sheet self-sufficiency.

The result is that mid-tier, diversified uranium vehicles with strong funding positions are absorbing a disproportionate share of available institutional capital, while micro-cap single-asset developers face chronic liquidity problems. Scale matters because it determines access to capital, which in turn determines which companies can actually advance their assets when the market eventually rewards execution.

A company with a single asset in a challenging jurisdiction, a modest treasury, and no offtake relationships is structurally disadvantaged regardless of the uranium price. The price environment matters, but the ability to survive long enough to benefit from it matters more.

What Is IsoEnergy's Uranium Portfolio Strategy?

A Three-Jurisdiction Architecture Built Around Sequenced Development

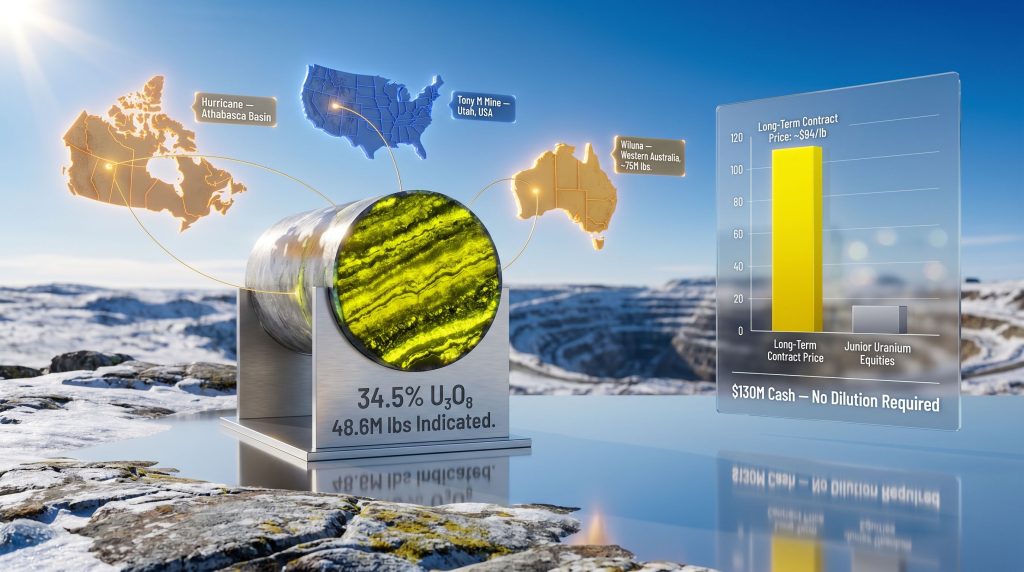

IsoEnergy describes itself as a globally diversified uranium explorer, developer, and near-term producer operating exclusively within what management considers the three strongest uranium jurisdictions in the world: Canada, the United States, and Australia. This is not simply a geographic diversification exercise. The portfolio is deliberately structured so that each jurisdiction represents a different development stage, creating a compounding value architecture across a projected 10-year horizon.

Rather than attempting to simultaneously advance multiple mines — a capital destruction pattern common to junior developers during bull markets — the IsoEnergy uranium portfolio strategy sequences projects into production based on their relative proximity to cash flow generation. This mirrors the capital allocation logic used by major mining companies, applied at a junior-to-mid-tier scale.

Portfolio Asset Summary

| Asset | Jurisdiction | Stage | Strategic Role | Key Metric |

|---|---|---|---|---|

| Hurricane Deposit | Athabasca Basin, Canada | Exploration / Resource Growth | Long-term high-grade value anchor | 48.6M lbs indicated @ 34.5% U₃O₈ |

| Tony M Mine | Utah, USA | Near-Term Production Restart | First cash flow generation | Fully permitted; toll-milling agreement in place |

| Wiluna Uranium Project | Western Australia | Medium-Term Development | Pipeline diversification; jurisdictional optionality | ~75M lbs across three deposits |

The combined global resource base stands at 154.3 million pounds U₃O₈ in the measured and indicated categories, with a further 88.2 million pounds classified as inferred. A treasury position of approximately $130 million provides the financial runway to advance this sequencing plan without dilutive capital raises — a significant competitive advantage in an environment where equity markets are not rewarding uranium developers generously.

Why Tier-One Jurisdiction Selection Functions as a Competitive Moat

Operating exclusively in Canada, the United States, and Australia is not merely a conservative preference. It creates compounding structural advantages:

- Lower sovereign risk reduces the probability of unexpected regulatory or political disruption to project timelines

- Established mining law frameworks provide predictable permitting pathways and legally defensible asset positions

- Infrastructure adjacency in mature mining districts reduces capital intensity for project development

- Institutional investor eligibility expands: many mandates explicitly exclude projects in frontier or high-risk jurisdictions, limiting the capital available to companies operating there

- Lower cost of capital directly improves project economics at every stage of development

The contrast with peers operating in higher-risk jurisdictions is becoming increasingly visible in equity valuations, even adjusting for asset quality differences.

Inside the Hurricane Deposit: The World's Highest-Grade Indicated Uranium Resource

Why Grade Dominates Uranium Project Economics

Uranium mine economics are governed by grade more decisively than almost any other commodity. The reason is that uranium processing is capital-intensive and relatively fixed-cost at the mill level. Higher grades mean more uranium recovered per tonne of ore processed, dramatically improving the economics of each dollar spent on mining and milling.

At the extreme end of the global grade distribution sits the Hurricane deposit in Saskatchewan's Athabasca Basin. With an indicated resource of 48.6 million pounds at 34.5% U₃O₈, Hurricane holds the highest grade of any indicated uranium resource globally. To contextualise this: the average grade of uranium mines operating globally is typically measured in fractions of a percent. Hurricane's grade is not incrementally better — it is categorically different.

The deposit contains three distinct grade domains:

- Low-grade domain: approximately 1.5% U₃O₈

- Medium-grade domain: intermediate concentrations

- High-grade domain: grades exceeding 50% U₃O₈

The existence of a zone grading above 50% U₃O₈ places portions of this deposit in a category shared by only a handful of known uranium occurrences in recorded geological history.

The South Trend: A Potential Exploration Breakthrough

Hurricane was initially discovered in 2018 and had its first resource published in 2022. In the years following, exploration efforts focused primarily on extending the main zone along strike — a logical but ultimately unrewarding strategy. Results in that direction generated encouraging geochemical signals but no significant new mineralised intercepts.

The winter 2024/25 drilling program marked a strategic pivot. Attention shifted to what the team refers to as the south trend — a corridor that had seen comparatively little systematic drilling historically. The results were immediately significant.

Drill holes targeting the low-grade domain of the south trend, where the resource model predicted grades of approximately 1.5% U₃O₈, returned an intercept of 11.6% U₃O₈ — roughly 7.5 times the modelled grade. This kind of variance between prediction and reality is not routine. It suggests the resource model had materially underestimated the grade tenor of this corridor.

The winter program comprised six holes over 550 metres of strike length, with mineralisation encountered ranging from 0.5% to over 10% U₃O₈. Critically, an intercept grading 2.75% U₃O₈ was returned 550 metres from the nearest known resource boundary, demonstrating that the south trend carries fertile mineralisation over a significant and previously unappreciated strike extent.

When grade materially exceeds the resource model's prediction in an under-drilled corridor, it raises the possibility of an independent high-grade mineralised system rather than a peripheral halo of the main deposit. This distinction carries significant implications for the scale of potential resource additions.

For investors looking to understand what these numbers mean in practice, interpreting drill results within their geological context is essential before drawing conclusions about resource potential.

Summer 2025 Drilling Program: Objectives and Current Status

Building on the winter breakthrough, an expanded 20-hole summer drilling program was designed specifically to follow up on south trend targets. Six holes were completed before the program encountered a temporary interruption: regional wildfires necessitated an evacuation of the exploration camp, with the closest fire located approximately 5 kilometres away on the opposite side of a lake.

Team safety was prioritised, and personnel were returned to Saskatoon. Daily contact with provincial authorities has been maintained, with expectations of a return to site within approximately one week of evacuation — putting the resumption around early July 2025. Given the remaining length of the northern Canadian drilling season, there is considered to be sufficient buffer to complete the 20-hole program and potentially expand it further depending on results from the initial summer holes.

Early results from the first completed summer holes have been described as encouraging, reinforcing confidence in the south trend thesis ahead of formal release to the market.

What Neighbouring Exploration Activity Reveals About Regional Mine Potential

One of the most significant and least widely discussed dimensions of the Hurricane story involves the activity of neighbouring operators on the adjoining Dawn Lake property. While large mining companies operate under high materiality thresholds for public disclosure, certain signals are observable.

In recent management discussion and analysis filings, the neighbouring operator noted that mineralisation being encountered in their exploration work is analogous to that of Cigar Lake and McArthur River — the two highest-grade producing uranium mines in the world. This is a meaningful public disclosure from a company that rarely characterises its exploration results in such direct terms.

Additionally, drill spacing observable from the shared property boundary appears consistent with mine feasibility delineation rather than regional exploration. Tighter drill patterns indicate the neighbouring operator is defining a resource to the standard required for mine planning, not simply characterising a geological trend.

The strategic implication is substantial: if Cigar Lake reaches end-of-mine-life around 2035 as anticipated, the Dawn Lake and Hurricane corridor could represent one of the most credible candidates to partially replace that lost production — potentially as a co-development or joint-operation scenario with the neighbouring operator.

Tony M Mine, Utah: Anatomy of a Near-Term Production Restart

Why the United States Represents the First Production Catalyst

Among the three portfolio assets, Tony M in Utah is furthest along the path to cash flow generation. The mine already holds the necessary federal and state permits, has established surface infrastructure in place, and operates under an existing toll-milling agreement that eliminates the need to construct standalone processing facilities.

This combination means the capital expenditure required to restart production is substantially lower than greenfield development. The primary outstanding requirement before a restart decision can be made is the completion of an updated economic study — currently underway with multiple specialist consultants engaged — expected to be delivered before the end of 2025.

The Beneficiation Technology Underpinning the Economics

A 2,000-tonne bulk sample has been extracted from the Tony M mine and is currently being processed through a beneficiation technology that has delivered promising early results. The performance metrics from initial sample runs are notable:

- 75% of total material volume removed during the beneficiation process

- Over 90% of contained uranium preserved after volume reduction

This means that material delivered to the toll mill will carry a head grade dramatically higher than the run-of-mine ore grade, directly improving processing economics and reducing per-pound production costs. The bulk sample program is designed to confirm these results at commercial scale, with the outputs feeding directly into the updated economic study.

Importantly, the company has appointed a Vice President of Commercial who is actively engaging with utility buyers to assess offtake appetite and achievable long-term contract pricing. The commercial strategy prioritises maximising per-pound value extraction over production volume or speed to market.

The Strategic Case for Patience Over Speed

A counterintuitive but strategically sound aspect of the Tony M positioning is the deliberate decision not to rush into production despite having the permits and infrastructure to do so. The reasoning involves understanding how uranium supply dynamics create asymmetric optionality for production-ready operators.

If supply continues to fail to respond to current pricing — and the evidence from global restart programs suggests this is likely — then uranium availability rather than price eventually becomes the binding constraint. In that environment, operators who can bring production online rapidly without the capital destruction of a rushed or failed restart hold asymmetric advantage.

The 2006-2008 uranium bull market offers a historical precedent: the flooding of the Cigar Lake mine triggered an exponential price response precisely because supply was suddenly removed from a market that could not replace it quickly. Operators with functioning infrastructure in that environment captured extraordinary value. Patient positioning now preserves the same type of optionality.

Wiluna Uranium Project, Western Australia: The Medium-Term Development Thesis

Why the Toro Energy Acquisition Represented a Mispriced Asset Opportunity

The acquisition of Toro Energy and its flagship Wiluna Uranium Project illustrates how single-asset micro-cap structures can cause the market to systematically underprice fundamentally sound assets. Toro's management had advanced the project credibly, but the market struggled to reconcile a $300 million capital expenditure requirement with a micro-cap company structure. That capex is manageable within a diversified mid-tier developer's balance sheet, but it represents an existential financing challenge for a standalone small-cap.

By acquiring the asset and placing it within a portfolio context where it can be sequenced behind Tony M's cash flow generation, the valuation disconnect is potentially resolved over time.

Scale, Geometry, and Permitting History

The Wiluna project encompasses approximately 75 million pounds U₃O₈ distributed across three deposits: Centipede-Millipede, Lake Way, and Lake Maitland. The deposit geometry is favourable for open-pit mining, with mineralisation extending from surface to approximately 10 metres depth — a characteristic that reduces mining complexity and pre-strip requirements relative to deeper deposits.

On the permitting front, both federal and state approvals had previously been granted to advance the mine to construction. The current WA uranium mining status indicates the government has signalled its intention to honour those historical permits, providing a defined regulatory pathway forward despite ongoing public debate around uranium development policy in the state.

Integration and Value Creation Roadmap

Canadian technical teams have already been deployed to Western Australia for asset integration work. The priority workstreams over the next 6 to 12 months include:

- Resource update to NI 43-101 standards, bringing the existing resource estimate into compliance with Canadian reporting requirements and improving its credibility with institutional investors

- Updated economic study incorporating current cost assumptions, equipment pricing, and uranium market conditions

- Infill drilling program to upgrade resource confidence classifications and reduce technical uncertainty

The strategic development timeline positions Wiluna as a 3 to 5 year pathway to production, sequenced behind the Tony M restart and ahead of the longer-term Hurricane co-development scenario.

The next major ASX story will hit our subscribers first

Capital Allocation Across the Portfolio: Thinking Like a Major at Junior Scale

Stage-Gated Investment Framework

The capital allocation model applied across the three-asset portfolio follows a stage-gated logic that prioritises resources based on proximity to production rather than spreading capital equally across all assets:

- United States (near-term): Complete economic study, assess market conditions, make production restart decision

- Australia (medium-term): Upgrade resource to NI 43-101, update economic study, advance through permitting and construction

- Canada (long-term): Explore south trend, expand resource, evaluate co-development pathway with neighbouring operators

Comparison of Portfolio Approaches in the Junior Uranium Sector

| Strategic Model | Risk Profile | Capital Efficiency | Institutional Appeal | Execution Risk |

|---|---|---|---|---|

| Single-asset, single-jurisdiction | High (binary) | Low | Limited | High |

| Multi-asset, single-jurisdiction | Moderate | Moderate | Moderate | Moderate |

| Multi-asset, multi-jurisdiction (tier-one only) | Low-Moderate | High | High | Low-Moderate |

| Multi-asset, mixed-jurisdiction (includes frontier) | High | Variable | Low-Moderate | Very High |

Strategic Equity Positions: Portfolio-Within-a-Portfolio

Beyond the three core assets, IsoEnergy maintains equity positions in approximately 6 to 7 uranium junior companies with an aggregate value of around $40 million. Structures such as the Pure Point joint venture provide discovery upside without direct operational management burden. This approach functions as a portfolio-within-a-portfolio, offering optionality across the broader uranium exploration universe while keeping core capital focused on the primary development sequence.

NextGen Energy continues to hold a meaningful equity position, having been diluted to approximately 28% through the Toro transaction. The institutional shareholder base more broadly is characterised as strong, with additional investors described as waiting for clearer market directional signals before increasing their positions.

The Structural Uranium Deficit: Why This Cycle Differs

Supply Failure as a Persistent Structural Condition

The uranium supply and demand imbalance is not a temporary dislocation awaiting correction. No significant new mines have been commissioned during the current price cycle, and restart programs across the industry have repeatedly underdelivered against published guidance. This persistent supply-side failure, occurring at $85 to $94 per pound pricing, suggests the structural barriers to bringing new production online are higher than the market currently appreciates.

Demand, meanwhile, is being supported by multiple independent structural drivers:

- Decarbonisation commitments driving nuclear energy re-evaluation across developed economies

- AI data centre power demand creating electricity load growth that grid-scale renewables cannot easily address

- Energy security imperatives following geopolitical disruptions pushing governments toward domestic and allied-nation energy supply chains

The combination of persistent supply failure with independently accelerating demand creates the conditions for a supply availability crisis, not merely a price cycle. Consequently, when supply cannot physically meet demand at any price, the operational status of individual assets becomes more strategically significant than their valuation multiples.

In a scenario where spot uranium approaches $200 or higher due to physical scarcity rather than speculative demand, the distinguishing factor between uranium developers will not be their resource size or grade alone — it will be whether they can actually deliver pounds to market without encountering the same execution failures that have characterised the restart generation.

Furthermore, uranium market trends for 2025 suggest that the companies best positioned are those with demonstrated execution capability across multiple jurisdictions rather than speculative single-asset plays. For a broader analysis, IsoEnergy's building approach to constructing a diversified uranium portfolio across tier-one jurisdictions has been widely examined by industry analysts.

Frequently Asked Questions: IsoEnergy Uranium Portfolio Strategy

What makes the Hurricane deposit globally significant?

Hurricane holds the world's highest-grade indicated uranium resource at 48.6 million pounds grading 34.5% U₃O₈. Its location in Saskatchewan's Athabasca Basin — the world's premier uranium district — combined with neighbouring operators pursuing mine-oriented exploration delineation, positions it as a potential long-duration, high-margin production asset with significant resource expansion potential through the south trend.

When could Tony M begin producing uranium?

Subject to the completion of the economic study expected before end of 2025 and prevailing market conditions at the time of the decision, a production restart could be initiated with production potentially commencing in 2026. The asset is fully permitted and infrastructure-ready, meaning restart timelines are governed by economics and market conditions rather than regulatory or construction constraints.

How does the Wiluna acquisition change IsoEnergy's strategic profile?

Wiluna transforms the portfolio from a Canada-U.S. binary into a genuine three-continent, tier-one uranium platform. Adding approximately 75 million pounds of near-surface uranium in Western Australia materially reduces single-jurisdiction concentration risk while extending the production pipeline across a 10-year sequencing horizon.

What is the significance of the south trend drilling results at Hurricane?

Encountering 11.6% U₃O₈ in areas modelled at approximately 1.5% grade, and identifying 2.75% U₃O₈ mineralisation 550 metres from the known resource boundary, indicates the south trend may host an independent high-grade mineralised system. This raises the prospect of material resource additions outside the current estimate in a corridor that has historically received very limited drilling attention.

How is IsoEnergy funded relative to its development pipeline?

With approximately $130 million in cash, a strong institutional shareholder base led by NextGen Energy at approximately 28%, and no near-term production capital commitments of a scale that threatens the treasury position, the company maintains financial flexibility to advance its sequencing plan without forced equity dilution.

Key Takeaways: What IsoEnergy's Strategy Reveals About Uranium Development

- The uranium equity market is bifurcating: diversified, well-funded, tier-one developers are accumulating institutional relevance while undiversified micro-caps face structural capital access problems regardless of asset quality

- Portfolio sequencing — not simultaneous multi-project development — is the capital-efficient model for advancing multiple uranium assets without destroying value

- High-grade resource anchors like Hurricane provide long-duration optionality that appreciates disproportionately in supply-constrained markets, particularly as Cigar Lake approaches end-of-mine-life around 2035

- Patient positioning on production-ready assets like Tony M preserves asymmetric upside in a scenario where supply failure drives uranium prices to levels that would reward rapid, reliable production restarts

- The south trend breakthrough at Hurricane represents potentially the most significant unreported exploration development in the Athabasca Basin this cycle — a corridor grading 7.5 times above model expectations across 550 metres of previously under-drilled strike

- Australia's Wiluna project provides a 75-million-pound near-surface development pipeline that was systematically undervalued due to single-asset corporate structure, not because of any fundamental deficiency in the asset itself

Disclaimer: This article contains forward-looking statements and speculative analysis based on publicly available information and management commentary. It does not constitute financial advice. Uranium prices, project timelines, and resource estimates are subject to change. Readers should conduct their own independent research before making any investment decisions. Past performance in the uranium sector is not indicative of future results.

Want to Position Yourself Ahead of the Next Major Uranium Discovery?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to deliver real-time alerts on significant mineral discoveries — including high-grade uranium finds like those reshaping the Athabasca Basin — turning complex exploration data into actionable investment insights for both short-term traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page to see what's possible, and begin your 14-day free trial today to ensure you're never the last to know when the next major find is announced.