June 8, 2026

The Supply-Demand Arithmetic That Makes ISR Uranium's Scaling Logic a National Priority

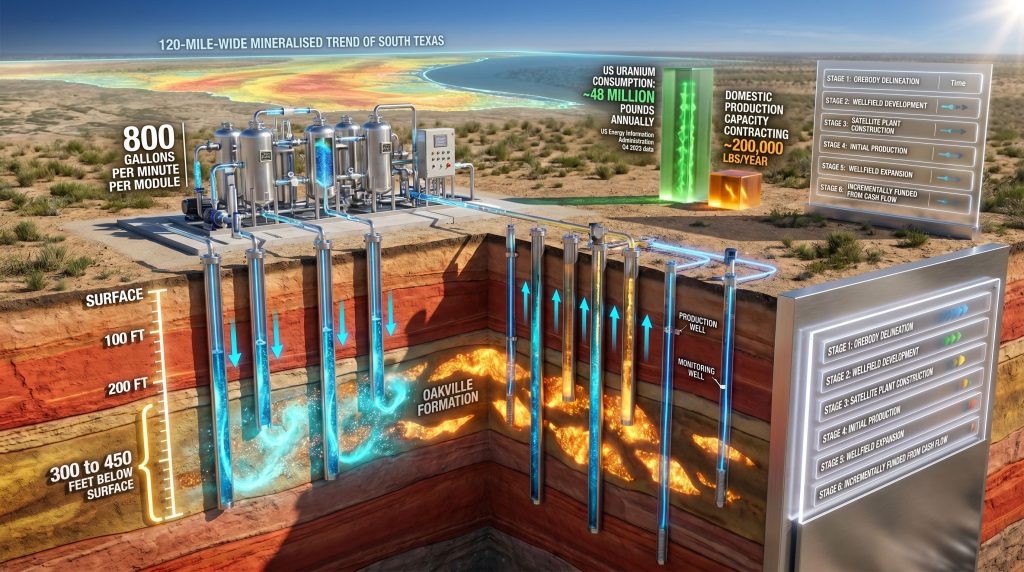

The energy industry rarely faces structural mismatches as clearly quantifiable as the one currently defining the US uranium market. Understanding how ISR uranium projects scale production one wellfield at a time is central to grasping why this production method has become so strategically significant. According to US Energy Information Administration data through the fourth quarter of 2023, domestic uranium consumption is expanding at a rate of approximately 48 million pounds per year, while US uranium production capacity is simultaneously contracting at roughly 200,000 pounds annually. The arithmetic of that divergence is not merely an investor concern or an industry talking point. It is a variable with direct consequences for nuclear reactor fuel supply chains, domestic energy security planning, and the capital allocation decisions of every uranium producer operating in the country.

Understanding why in-situ recovery (ISR) uranium has become the most closely watched domestic production pathway requires understanding something that is not widely appreciated outside the sector: ISR does not scale the way conventional mining does. It scales one wellfield at a time, and that distinction shapes everything from capital structure to regulatory timelines to corporate strategy. Furthermore, the uranium market dynamics underpinning this shift make ISR's modular approach increasingly critical for national energy planning.

When big ASX news breaks, our subscribers know first

What In-Situ Recovery Actually Does Underground

The Chemistry That Replaces Excavation

ISR uranium production begins not with a shovel or a blast, but with chemistry. Operators inject a lixiviant, typically oxygenated groundwater, into uranium-bearing sandstone formations. The oxygenated solution mobilises uranium that is bound to sand grains within the formation, dissolving the mineral in place rather than requiring physical removal of rock. The uranium-bearing solution is then pumped back to the surface through production wells for processing.

This approach works because of the geological characteristics of ISR-amenable deposits. These orebodies tend to be laterally extensive but relatively thin, often measured in tens of feet of thickness across formations that extend for miles. That geometry is precisely what enables sequential segment mining: operators can extract uranium from one part of the deposit while drilling and permitting the next, building output progressively rather than committing to full orebody extraction upfront.

The in-situ leaching benefits over conventional alternatives are significant, as illustrated in the surface footprint comparison below:

| Production Method | Surface Disturbance | Mill Infrastructure Required | Reclamation Complexity |

|---|---|---|---|

| ISR | Minimal (well pads, piping) | No conventional mill needed | Low cost, shorter timeline |

| Open-pit | Extensive (pit, waste dumps) | Full mill required | High cost, extended timeline |

| Underground | Moderate (shafts, portals) | Full mill required | Moderate to high cost |

From Wellfield to Yellowcake: How the Processing Chain Works

Once uranium-bearing solution reaches the surface, it enters an ion exchange (IX) system. Resin beads within the IX plant selectively capture dissolved uranium as the solution passes through. The loaded resin is then transported to a central processing plant (CPP) for final processing into uranium concentrate, the yellowcake that uranium utilities ultimately purchase.

The critical design insight of modern ISR operations is the satellite IX plant model. Rather than constructing a full CPP at every production site, operators position modular satellite IX plants near each active wellfield. Loaded resin is transported from these satellite units to a single licensed CPP that can serve multiple geographically dispersed wellfields across a district. This architecture distributes fixed CPP processing costs across a growing production base, reducing the per-pound capital cost of adding new production capacity.

Structural Insight: A single licensed and operating CPP can receive loaded resin from multiple satellite IX plants spread across an entire district. This design means that fixed processing infrastructure costs are not replicated at every new wellfield, allowing operators to expand output without proportional capital expenditure at each new site.

How ISR Uranium Projects Scale Production One Wellfield at a Time

The Anatomy of a Wellfield Pattern

Each ISR wellfield consists of three distinct well types operating as a coordinated circulation system. According to the World Nuclear Association's overview of in-situ leach mining, these components are fundamental to the contained extraction process:

- Injection wells introduce the oxygenated lixiviant into the ore zone

- Production wells recover the uranium-bearing solution for surface processing

- Monitor wells provide the regulatory compliance mechanism, detecting any solution migration beyond the approved boundary of the licensed ore zone

The geometric arrangement of these wells is engineered to contain the lixiviant within the designated extraction zone. Monitor wells are not an operational afterthought; they are the primary mechanism through which regulatory bodies verify that subsurface chemistry is confined to the permitted area. This is also why each wellfield pattern can be independently permitted and independently operated, functioning as a discrete, self-contained production unit.

The Step-by-Step Expansion Sequence

Understanding how ISR uranium projects scale production one wellfield at a time requires tracing the operational sequence from initial drilling through to active extraction:

| Stage | Activity | Capital Requirement |

|---|---|---|

| 1 | Orebody delineation through drilling and geological mapping | Moderate (exploration-phase) |

| 2 | First wellfield installation within a defined ore zone segment | Moderate (drilling and piping) |

| 3 | Lixiviant circulation initiation and production well activation | Low (operational) |

| 4 | Active extraction phase spanning months to years | Minimal (operating costs) |

| 5 | Adjacent wellfield drilling connected to existing CPP | Low to moderate (incremental) |

| 6 | Sequential pattern repetition across the licensed orebody | Incrementally funded from cash flow |

The financial elegance of this model lies in stage six. Because earlier wellfields are generating cash flow before the full capital commitment of the production system is made, operators can, in principle, fund subsequent wellfield additions from operating revenues rather than requiring repeated equity raises. This is qualitatively different from conventional mine expansion, where additional production capacity typically requires a new capital cycle with all the associated dilution and financing risk.

The Satellite Ion Exchange Model: Engineering for Scalability

Why Modular Flow Capacity Changes the Economics

Satellite IX plants are not simply smaller versions of central processing facilities. They are purpose-designed for relocatability and modular expansion. A plant is typically built in discrete flow-capacity increments, with each increment corresponding to a wellfield module of defined throughput.

In practice, this means a satellite IX plant with a total planned capacity of 3,200 gallons per minute (gpm) requires four discrete 800-gpm wellfield modules to be drilled, connected, and permitted before it can operate at nameplate output. Each module represents an independently authorisable production increment, which is a critical distinction for understanding both the production ramp timeline and the regulatory dependencies that govern it.

The staged commissioning sequence typically follows this pattern:

- Phase 1: Plant commissioned at 50% of total planned throughput capacity

- Phase 2: Incremental ramp to 75% capacity as additional wellfield modules are connected

- Full capacity: Achieved only when all four wellfield modules are drilled, connected, and carrying active production authorisations

The absence of major permanent infrastructure at each satellite site is a further advantage. Because satellite IX equipment can be relocated to support uranium recovery at additional wellfields elsewhere within a district once a given segment of the orebody is exhausted, the capital deployed in building the plant retains utility beyond a single production horizon.

The Permitting Architecture That Governs ISR Timelines

Multi-Layer Regulatory Requirements

ISR uranium producers in the United States navigate a layered regulatory environment that operates at both state and federal levels. The foundational requirement for any US ISR project is an aquifer exemption, a designation that authorises the use of a groundwater aquifer for uranium extraction purposes. Without this, no lixiviant injection can legally commence.

Beyond the aquifer exemption, each individual wellfield requires injection permits before it can begin operating. These per-module authorisations are the mechanism that governs precisely when each production unit can transition from infrastructure-complete to production-authorised status. The gap between those two conditions is the most consequential variable in any ISR scaling timeline.

Comparing US ISR Regulatory Environments

Different US jurisdictions have developed ISR regulatory frameworks at very different levels of maturity:

| Jurisdiction | Regulatory Body | ISR Operational History | Permit Framework Maturity |

|---|---|---|---|

| Texas | TCEQ | 50+ years | Highly developed |

| Wyoming | NRC / State | Decades | Established |

| South Dakota | NRC / State | Emerging | Still developing |

| Nebraska | NRC / State | Limited | Early-stage |

Texas, administered by the Texas Commission on Environmental Quality (TCEQ), offers the most developed ISR regulatory reference framework in the country. Its five-decade operational record provides regulators and operators with a shared body of precedent that reduces interpretive uncertainty in the permitting process. Newer ISR jurisdictions are still building that institutional knowledge base, which introduces additional timeline variability for projects in those states.

The Strategic Value of Inherited Permit Foundations

One operational insight that is not widely understood outside the ISR sector is the compounding advantage of acquiring projects with legacy permit structures from prior operators. When uranium prices fell to historic lows in previous cycles, a number of ISR projects with established aquifer exemptions and partially issued wellfield permits were suspended or abandoned.

Companies that subsequently acquired those assets inherited permit foundations that can meaningfully compress the time between construction-ready and production-authorised status. This does not eliminate regulatory risk, however. Final production authorisations remain project-specific determinations that pending acquisitions of legacy permits do not automatically resolve. Nevertheless, the difference between beginning the permitting process from scratch and building upon an existing approved framework can represent years of timeline compression, a significant competitive advantage in a supply-constrained market shaped by uranium supply-demand volatility.

South Texas as the Benchmark for ISR District Development

Geological Foundations of a Multi-Decade Production Region

South Texas has served as the proving ground for commercial ISR uranium production for more than five decades. The uranium mineralisation in the region occurs within the Oakville Formation, with uranium-bearing sands typically located at depths between 300 and 450 feet below the surface. The mineralised trend across the region extends approximately 120 miles long by 20 miles wide, providing the geological runway for multi-wellfield, multi-project district development over extended production horizons.

The legacy of operational activity in South Texas from companies including US Steel, Cameco, Rio Algom, and General Atomics represents a body of institutional knowledge about wellfield construction, lixiviant chemistry management, and plant optimisation. This reduces execution risk for current operators who can access that expertise, and it is a less visible but practically important advantage for companies with technical teams that include veterans of those prior programmes.

The District CPP Model in Practice

The economic logic of the ISR district model becomes clearest when examining how a single licensed CPP can anchor multiple satellite production units across a region. Fixed processing costs at the CPP are distributed across every satellite wellfield feeding into it. As additional satellite IX plants are commissioned and connected, the per-pound processing cost for the entire system declines, creating a natural economies-of-scale dynamic that improves unit economics as the production base grows.

enCore Energy Corp. (NASDAQ: EU | TSXV: EU) illustrates this model through its Rosita CPP, which is already licensed and operating in South Texas. The Upper Spring Creek satellite IX plant, construction of which was completed on June 4, 2026, feeds uranium-loaded resin to the Rosita CPP. The satellite plant was initially commissioned at 1,600 gpm, representing 50% of its planned total throughput, with a ramp to 75% capacity targeted before the end of June 2026 and full capacity of 3,200 gpm targeted by the end of July 2026.

enCore holds S-K 1300 resources of 30.94 million pounds in the measured and indicated category and 20.54 million pounds in the inferred category across its portfolio, according to its April 2026 corporate presentation. That resource base represents the geological inventory from which sequential wellfield additions can be drawn over a multi-year production horizon.

The next major ASX story will hit our subscribers first

The Scale Threshold Problem for ISR Producers

Why Sub-Million-Pound Producers Face a Structural Ceiling

One of the least publicised dynamics in the ISR uranium sector is the institutional capital threshold problem. The uranium market deficit compounds this challenge, as ISR producers with annual output below approximately 1 million pounds face compounding disadvantages in two critical areas simultaneously:

- Access to institutional capital markets is constrained, with smaller producers receiving less favourable credit ratings and higher financing costs

- Nuclear utility procurement teams negotiate more favourable long-term contract terms with larger, more reliable counterparties, giving sub-scale producers weaker contract leverage

These two disadvantages reinforce each other. Higher capital costs reduce the margin available to fund new wellfield development, slowing the production growth that would eventually resolve the scale problem. Weaker utility contract terms reduce revenue predictability, making the project economics less attractive to debt providers. The result is a structural ceiling that can trap ISR producers in a sub-scale position regardless of the quality of their underlying geology.

Industry Perspective: The economics of the ISR sector increasingly reward operators who achieve sufficient scale to access institutional-grade financing. Producers operating below the critical output threshold face higher borrowing costs and reduced negotiating leverage with utility customers simultaneously, creating a compounding disadvantage relative to larger peers.

Consolidation as Structural Necessity

This dynamic helps explain why M&A activity in the ISR sector should be understood as a structural response to the institutional capital threshold rather than purely opportunistic deal-making. A fragmented supply base of sub-scale ISR producers, each individually capital-efficient at the project level, collectively lacks the balance sheet strength, output reliability, and counterparty credibility required to negotiate the kind of long-term utility contracts and institutional debt packages that underpin sustained production growth.

Corporate consolidation transforms modular project-level capital efficiency into institutional-grade financial architecture. The resource base across a consolidated portfolio, measured in tens of millions of pounds across measured, indicated, and inferred categories, provides both the geologic inventory for sequential wellfield additions and the asset base against which institutional capital can be secured.

Managing Three Parallel Timelines: The Operational Challenge ISR Producers Rarely Discuss

Construction, Permitting, and Production Ramp-Up Rarely Synchronise

The three-timeline management challenge is one of the more technically demanding aspects of ISR production scaling that rarely receives adequate attention in investor communications. These three timelines operate simultaneously but rarely synchronise:

- Construction timeline: Drilling wellfield patterns, installing piping, and commissioning satellite IX plant modules in staged increments

- Regulatory timeline: Pursuing aquifer exemptions, individual wellfield injection permits, and final production authorisations through state and federal agencies on schedules that operators cannot fully control

- Production ramp-up timeline: Activating modules sequentially as each wellfield is drilled, physically connected to the satellite plant, and carrying an active production authorisation

Construction can be completed before permits are received. Permits for one module can be granted while the adjacent module's wellfield is still being drilled. The permit gap, the period during which infrastructure is fully built and operationally ready but legally prohibited from producing, is the primary reason that projected production start dates and realised production start dates diverge in ISR project timelines.

At Upper Spring Creek, drilling for the first 800-gpm module was complete and wellfield infrastructure was nearly finished as of early June 2026, with drilling for Module 2 approximately 90% complete and activities underway for two additional 800-gpm modules. Production start remains targeted for late 2026, contingent on receipt of final regulatory clearances. The project benefits from permit foundations originally established by a prior operator, Signal Equities LLC, before low uranium prices forced a suspension of activity. enCore acquired the project in December 2020 and has developed those permit foundations further, but final production authorisations remain the controlling variable on the timeline.

ISR vs. Conventional Uranium Mining: The Full Structural Comparison

Capital, Environmental Profile, and Expansion Mechanics

| Dimension | ISR Uranium | Conventional Open-Pit or Underground |

|---|---|---|

| Initial capital requirement | Lower (no mill, no pit development) | Higher (mill construction and mine development) |

| Production capacity determination | Incremental wellfield-by-wellfield | Fixed at construction by mill throughput |

| Surface disturbance | Minimal | Significant |

| Reclamation timeline | Short, lower cost | Extended, higher cost |

| Expansion capital cycle | Fundable from operating cash flow | Typically requires new capital raise |

| Environmental regulatory perception | Substantially improved vs. legacy uranium | Carries legacy mining associations |

| Jurisdictional flexibility | Dependent on sandstone aquifer geology | Applicable to hard-rock deposits |

A less widely appreciated dimension of ISR's environmental profile is the reclamation dynamic. Because ISR does not create waste rock dumps, tailings facilities, or open pits, the reclamation process after wellfield exhaustion involves primarily groundwater restoration within the exempted aquifer zone and the removal of relatively modest surface infrastructure. This produces a reclamation cost and timeline profile that is categorically different from conventional uranium mining, a distinction that shapes both regulatory attitudes and community acceptance in ISR-friendly jurisdictions.

Furthermore, as the IAEA's technical guidance on uranium in-situ recovery confirms, modern ISR uranium extraction represents a genuinely different environmental paradigm compared to the open-pit and underground operations that shaped public perception of uranium mining in earlier decades. The contained underground chemistry, minimal surface footprint, and comparatively straightforward reclamation process position ISR as the production method best aligned with contemporary environmental standards and regulatory expectations.

What Sustained ISR Sector Growth Actually Requires

Beyond Individual Project Mechanics

The modular architecture of ISR production is capital-efficient at the project level but carries a fragmentation risk at the national supply level. The US supply-demand gap, growing by tens of millions of pounds annually, requires not just one additional wellfield but many wellfields added rapidly across multiple operators and districts. The ISR sector's collective ability to respond to that demand depends on resolving several interconnected challenges simultaneously:

- Regulatory process improvements that reduce the permit gap without compromising aquifer protection standards or reducing the rigour of monitoring requirements

- Corporate consolidation that creates ISR producers of sufficient scale to access tier-one institutional capital and negotiate competitive utility supply contracts

- District-scale land positions that provide the geological runway for sequential wellfield additions over multi-year production horizons without requiring repeated exploration programmes

- Utility offtake agreements that provide sufficient revenue visibility to support incremental capital deployment into each successive wellfield module

The ISR sector's structural challenge is ultimately this: the same modular architecture that makes individual project expansion so capital-efficient can, at the sector level, produce a fragmented collection of sub-scale producers that collectively fall short of the output volumes required to materially close the supply-demand gap. Resolving that paradox requires both operational excellence at the wellfield level and strategic thinking at the corporate and sector level.

Readers seeking additional context on ISR uranium production mechanics and US domestic uranium supply dynamics can explore further analysis published at Crux Investor, which covers uranium sector developments including ISR project progress and operator strategy.

This article contains forward-looking statements and projections based on information available at the time of writing. Production timelines, resource estimates, and regulatory outcomes are subject to change. This content is for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence before making investment decisions.

Want To Stay Ahead of the Next Major Uranium Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to ensure you're positioned ahead of the broader market.