July 11, 2026

When Energy Dependency Defies Political Logic

Across global energy markets, one pattern repeats itself with remarkable consistency: the deeper the infrastructure tie between two nations, the harder it becomes to sever that relationship, regardless of how turbulent the political climate grows. History offers countless examples of states that maintained fuel and power trade corridors through wars, sanctions, and diplomatic crises because the economic consequences of disconnection proved too severe to accept.

The Israel gas export deal with Egypt is a textbook expression of this principle. On the surface, it is a commercial contract between energy companies. Beneath that surface, it is a load-bearing pillar of Egypt's power grid, industrial economy, and long-term regional ambitions. Understanding why a $35 billion gas agreement survives active political friction requires looking not just at the contract itself, but at the infrastructure, geology, and strategic calculus that make it almost impossible to walk away from.

When big ASX news breaks, our subscribers know first

The Leviathan Field: Geology as Geopolitical Leverage

What Makes Leviathan Structurally Dominant in the Eastern Mediterranean

The Leviathan offshore gas field sits in deep water in the Eastern Mediterranean and represents one of the most significant hydrocarbon discoveries of the past two decades in the region. Its scale is not merely a point of national pride for Israel; it is the geological foundation upon which an entire export architecture has been constructed.

The field is operated by a consortium that includes Chevron (the US supermajor that acquired Noble Energy and inherited the operatorship), NewMed Energy (the Israeli-listed partner), and Ratio Energies. These three entities are co-financing both the production expansion and the export infrastructure needed to move volumes at commercial scale.

Current development trajectories point toward Leviathan reaching approximately 21 billion cubic metres (bcm) of annual production capacity by 2029, a figure that fundamentally reframes Israel's energy identity. A country that spent decades importing energy to meet domestic needs is now constructing a multi-corridor export system designed to serve several regional markets simultaneously. The LNG supply outlook for the region is, consequently, being reshaped around these emerging Eastern Mediterranean volumes.

| Development Phase | Annual Delivery to Egypt | East Med Pipeline Capacity | Approximate Timeline |

|---|---|---|---|

| Pre-expansion baseline | ~4.7 bcm/year | ~6.5 bcm/year | Prior to 2026 |

| Phase 1 post-pipeline | ~6.7 bcm/year | ~8.5 bcm/year | From H1 2026 |

| Phase 2 expansion | ~12-13 bcm/year | Expanded corridor | Post-2028 |

| Peak field capacity target | ~21 bcm/year (total field) | Multiple corridors | By 2029 |

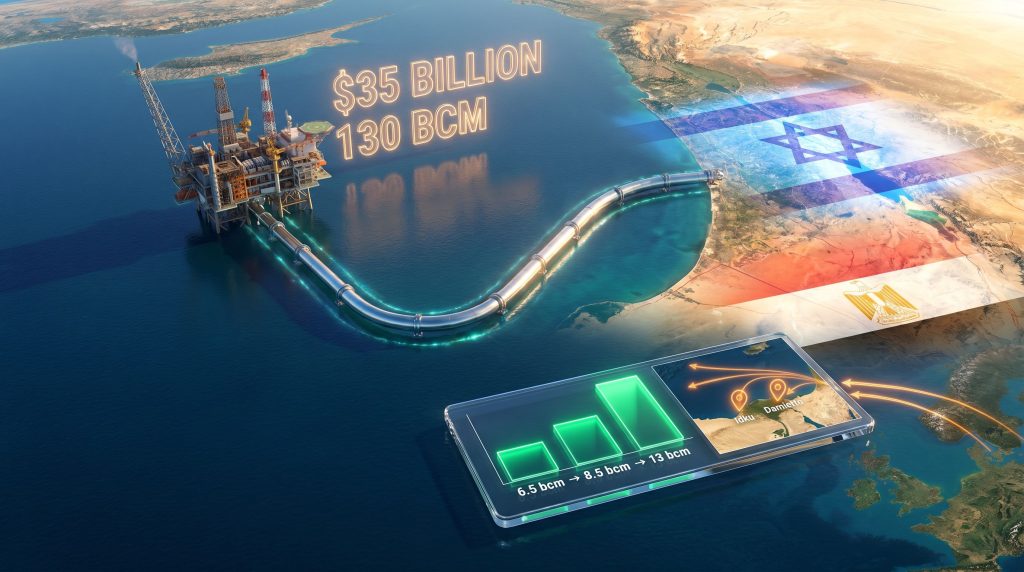

The Contracted Volume: Why 130 bcm Is a Historic Number

The expanded agreement between the Leviathan consortium and Egypt's Blue Ocean Energy covers a total contracted volume of 130 billion cubic metres over the duration of the deal, extending the commercial relationship through approximately 2040. This replaces the prior 2019 export agreement, which had contracted roughly 64 bcm and was scheduled to expire in the early 2030s.

The near-doubling of contracted volume is significant for several reasons beyond the headline revenue figure of $35 billion:

- It locks Egypt into a long-term upstream dependency on a single bilateral supplier for the majority of its gas imports

- It provides the Leviathan partners with revenue certainty that justifies continued capital expenditure on production expansion

- It commits Israeli export infrastructure to Egypt for a period extending well beyond any conceivable near-term political resolution in the broader region

- Approximately 50% of total export revenues flow into Israeli government funds under the fiscal terms governing Leviathan's commercial operations

Infrastructure as the Physical Enabler of a $35 Billion Relationship

The 45-Kilometre Subsea Pipeline: Engineering the Bottleneck Away

No amount of contractual ambition translates into delivered gas without physical infrastructure to carry it. For years, the primary constraint on Israel's gas export volumes to Egypt was not the Leviathan field's productive capacity, but the limited throughput of the existing transit route.

Israel Natural Gas Lines resolved this constraint by completing a 45-kilometre subsea pipeline connecting the Leviathan onshore gas reception facility in Ashdod to the East Mediterranean Gas pipeline near Ashkelon. From Ashkelon, gas travels through the East Mediterranean Gas pipeline to processing facilities at El-Arish in Egypt's Sinai Peninsula, where it enters Egypt's domestic distribution network.

This single infrastructure project raised the East Mediterranean Gas route's annual throughput capacity from approximately 6.5 bcm to 8.5 bcm. The installation also followed the completion of a third pipeline between the Leviathan offshore reservoir and its production platform, enabling higher field-level extraction rates without creating a new surface bottleneck.

Infrastructure Note: The multi-corridor export system being assembled through the Arish-Ashkelon route, combined with the planned Nitzana onshore pipeline expected to become operational around 2028, substantially reduces single-point-of-failure risk for both parties. Redundancy in transit infrastructure is not incidental; it is a deliberate risk-management strategy for a commercial relationship operating in a geopolitically sensitive environment.

The Nitzana Pipeline: Adding a Secondary Transit Corridor

The Nitzana onshore pipeline, approved in 2023 and anticipated to be operational by approximately 2028, will provide a complementary land-based route for Israeli gas entering Egypt. Its completion would give both parties a fallback transit option in the event of technical failure or physical damage to the primary subsea route, further embedding the supply relationship into durable physical infrastructure that cannot be unwound quickly.

Egypt's Structural Energy Problem: The Demand-Supply Gap Driving the Deal

Declining Domestic Production Meets Rising Industrial Demand

Egypt's domestic natural gas output has entered a structural decline phase driven by the maturation of its existing producing fields. At the same time, demand from the power generation sector, industrial consumers, and residential users has continued to expand. The resulting supply-demand gap is not a temporary cyclical phenomenon; it reflects the geology of Egypt's maturing hydrocarbon base colliding with a growing economy's energy appetite.

The practical consequences of this imbalance have been economically painful:

- Cairo was forced to resume liquefied natural gas imports, which carry significant cost premiums compared to pipeline supply due to the energy and capital required for liquefaction, shipping, and regasification

- Electricity shortfall risks intensified, threatening both household power security and industrial production continuity

- Emergency procurement at spot LNG prices exposed Egypt to international market volatility with minimal hedging capacity

Pipeline Gas vs. LNG: Why the Cost Differential Matters

The economic logic underpinning Egypt's commitment to the Israel gas export deal becomes clear when comparing the landed cost and logistics profile of pipeline gas against LNG imports. Furthermore, broader natural gas price trends in 2025 have amplified the cost advantage of locked-in pipeline supply over spot LNG procurement.

| Supply Option | Cost Profile | Delivery Speed | Geopolitical Risk |

|---|---|---|---|

| Israeli pipeline gas (Leviathan) | Lower, no liquefaction or shipping premium | Immediate via pipeline | Moderate, bilateral dependency concentration |

| Spot LNG imports | Higher, includes full supply chain premium | Weeks of shipping lead time | Lower, diversified global suppliers |

| Domestic Egyptian production | Lowest, no import cost | Immediate | None |

With domestic production declining and LNG imports proving expensive and logistically slow, Israeli pipeline gas offers Egypt the most competitive available alternative on a cost-per-unit and delivery-speed basis.

Egypt's Dual Commercial Role: Consumer and Re-Exporter

A dimension of this deal that receives insufficient attention is Egypt's ambition to function not merely as a gas consumer but as a regional energy hub. Egypt operates two major LNG liquefaction facilities:

- Idku LNG terminal: A two-train facility capable of processing significant volumes of pipeline gas for export

- Damietta LNG terminal: A single-train facility that was inactive for years before returning to operation and is now central to Cairo's re-export strategy

When Israeli gas volumes exceed Egyptian domestic demand, the surplus can be directed to these terminals, liquefied, and exported to European or Asian buyers as LNG. This transforms the Israel gas export deal into a supply chain enabler for Egypt's commercial ambitions, giving Cairo a financial interest in maximising rather than merely stabilising Israeli gas imports.

The 2025 Supply Disruption: A Real-World Stress Test

What Happened When Exports Were Reduced

During a period of intensified regional conflict in 2025, Israel temporarily curtailed natural gas exports to Egypt. The effects were immediate and spread across multiple sectors of the Egyptian economy:

- Fertiliser manufacturing plants suspended operations due to insufficient gas feedstock

- The government increased consumption of fuel oil as a backup energy source across power stations, adding cost and carbon intensity to the power generation mix

- Cairo was forced to arrange emergency LNG purchases worth billions of dollars to partially replace the lost pipeline volumes

Quantifying Egypt's Exposure to Supply Concentration Risk

| Metric | Value |

|---|---|

| Israeli gas as share of Egypt's total energy consumption | ~20% |

| Israeli gas as share of Egypt's total gas imports | ~60% |

| Emergency LNG procurement triggered during 2025 disruption | Billions of dollars |

The 2025 episode functioned as an involuntary stress test that quantified Egypt's vulnerability in concrete economic terms. It also illustrates the central paradox of the deal: the same import concentration that creates acute disruption risk when supplies are curtailed is the mechanism that makes the deal commercially attractive for Egypt under normal operating conditions.

Risk Note: Analysts and investors monitoring Eastern Mediterranean energy dynamics should treat Egypt's supply concentration exposure as the deal's primary structural vulnerability. Future conflict escalation, infrastructure damage, or political breakdown each carry the potential to trigger supply gaps that would cost Egypt far more to replace via LNG markets than the import cost savings justify on an annualised basis.

The Geopolitical Architecture Enabling Energy Cooperation Amid Conflict

The 1979 Peace Treaty as the Legal Scaffold

Egypt and Israel formalised diplomatic relations under their 1979 peace treaty, a framework that has endured for over four decades through multiple rounds of regional violence, leadership changes, and shifting alliances. Energy trade has gradually evolved into one of the most commercially substantial expressions of that relationship, creating interdependencies that give both governments a continuous economic incentive to preserve the bilateral framework even when political rhetoric moves in the opposite direction.

The Commercial Firewall: How Egypt Separates Trade From Politics

Egypt's official position frames the $35 billion agreement as a purely commercial transaction negotiated by private energy companies under prevailing market conditions. This institutional framing serves a specific political function: it allows Cairo to maintain vocal public criticism of Israeli military operations in Gaza and to serve as a key diplomatic mediator in Israeli-Palestinian negotiations while simultaneously sustaining energy imports that underpin its power grid and industrial base.

This approach is not unique to Egypt. Several states throughout modern energy history have maintained active trade relationships with geopolitical rivals by creating institutional boundaries between commercial frameworks and diplomatic postures. The distinction is often criticised as artificial, but it has proven functionally durable in numerous bilateral contexts.

The Three Simultaneous Roles Egypt Occupies

Egypt currently navigates three distinct and partially contradictory geopolitical positions. These energy trade tensions playing out globally provide useful context for understanding how bilateral energy dependencies can persist under diplomatic strain:

- Energy importer: Structurally dependent on Israeli gas to prevent domestic power shortages and avoid expensive LNG substitution

- Political critic: Publicly opposing Israeli military actions in Gaza and serving as one of the most active diplomatic mediators between Israeli and Palestinian parties

- Regional hub aspirant: Seeking to leverage Israeli gas volumes through its LNG terminals to access European and Asian buyer markets

Managing these three roles simultaneously requires a level of institutional compartmentalisation that becomes increasingly difficult to sustain as conflict intensity escalates, as the 2025 supply curtailment demonstrated.

The next major ASX story will hit our subscribers first

Washington's Role and Israel's Four-Month Export Licence Delay

The Invisible Architect Behind the Final Approval

Israel delayed issuing the final export permit for the expanded agreement for approximately four months, with Prime Minister Netanyahu citing undisclosed security and national interest considerations as justification for the postponement. The delay created commercial uncertainty for the Leviathan partners and prompted diplomatic engagement from the United States.

Washington reportedly played a material behind-the-scenes role in facilitating the eventual licence approval, framing the deal's completion as consistent with broader American strategic objectives of deepening economic interdependencies among Middle Eastern states. The US interest was not purely commercial; a functioning Israel-Egypt energy relationship that creates mutual dependency is consistent with American preferences for regional economic integration as a stabilising mechanism.

No formal trilateral diplomatic process was publicly convened, but the timeline of the licence approval and the acknowledged US engagement suggest that Washington's influence extended meaningfully into the approval process.

The Eastern Mediterranean Gas Competition: A Multi-Player Strategic Landscape

How the Israel-Egypt Deal Fits Into a Larger Regional Contest

The Israel gas export deal with Egypt does not exist in isolation. The Eastern Mediterranean has become one of the world's most strategically contested gas regions, with multiple producers and transit states competing for European market access. Consequently, broader oil price movements and commodity market volatility continue to influence how buyers and sellers in this region evaluate long-term supply contracts.

| Supplier | Target Market | Annual Volume | Key Infrastructure |

|---|---|---|---|

| Israel (Leviathan to Egypt for LNG re-export) | Europe via Egypt's LNG terminals | Up to ~13 bcm (Phase 2) | Arish-Ashkelon pipeline plus Nitzana route |

| African consortium (three nations) | Europe directly | ~30 bcm (planned) | Trans-African pipeline corridors |

| Eastern Mediterranean (Cyprus, Greece) | Europe | Under development | EastMed pipeline (proposed, feasibility contested) |

Three African nations have separately announced coordinated plans to deliver approximately 30 bcm of gas annually to Europe as part of European efforts to reduce dependency on Russian pipeline supply. Additionally, Europe's search for alternatives to both Russian and Middle Eastern gas has revived interest in two African pipeline projects collectively valued at approximately $38 billion.

These competing supply corridors create genuine commercial pressure on the Israel-Egypt pathway, particularly as European buyers evaluate long-term supply diversification strategies. Egypt's competitive advantage as a re-export hub depends on its ability to offer liquefied volumes from Israeli gas at prices that remain competitive against African pipeline alternatives. Furthermore, the crude oil market dynamics shaping energy investment decisions globally will influence which of these competing projects attract final investment decisions through the late 2020s.

Frequently Asked Questions: Israel Gas Export Deal With Egypt

What is the total value of the Israel-Egypt gas export deal?

The agreement is valued at approximately $35 billion, covering the supply of 130 billion cubic metres of natural gas from Israel's Leviathan offshore field to Egypt's Blue Ocean Energy over a period extending to approximately 2040.

Which companies are involved in the Leviathan gas deal with Egypt?

The primary stakeholders on the Israeli production side are Chevron (US operator), NewMed Energy (Israeli-listed partner), and Ratio Energies. Egypt's receiving counterparty is Blue Ocean Energy.

How much has Israel's gas export capacity to Egypt increased?

Completion of the new 45-kilometre subsea pipeline has raised the East Mediterranean Gas route's annual throughput from approximately 6.5 bcm to 8.5 bcm, with Phase 2 expansions targeting deliveries of nearly 13 bcm annually to Egypt.

Why did Israel delay the gas export licence for the expanded deal?

Israel postponed issuing the final export permit for approximately four months, citing security and national interest considerations. The United States reportedly engaged diplomatically to facilitate the eventual approval.

How does Egypt justify the deal despite political tensions with Israel?

Cairo formally classifies the agreement as a commercial transaction negotiated by private energy companies under market conditions, institutionally separating energy cooperation from its political criticism of Israeli actions in Gaza.

What are the risks if Israeli gas exports to Egypt are disrupted again?

As demonstrated during the 2025 supply curtailment, disruption triggers fertiliser plant shutdowns, increased fuel oil consumption, and costly emergency LNG procurement. With Israeli gas representing approximately 20% of Egypt's total energy consumption and 60% of its gas imports, the substitution cost is substantial.

What This Deal Signals for Regional Energy Markets

The Israel gas export deal with Egypt encodes several broader lessons that extend well beyond the bilateral relationship:

- Structural infrastructure dependency creates durable commercial ties that survive political disruption: The depth of Egypt's reliance on Leviathan gas makes unilateral contract termination economically prohibitive, regardless of diplomatic conditions

- The 45-kilometre subsea pipeline is the physical fulcrum of a $35 billion relationship: Capital investment in transit infrastructure is not peripheral to energy deals of this scale; it is the decisive enabling variable

- Egypt's LNG hub ambition depends on sustained Israeli upstream supply: Cairo's re-export strategy through Idku and Damietta is structurally contingent on continued Israeli gas import volumes exceeding domestic Egyptian consumption

- Supply concentration at 60% of imports creates systemic vulnerability: The 2025 disruption demonstrated that there is no short-term substitute for pipeline gas at equivalent cost and speed, making concentration risk the deal's primary unresolved structural weakness

- Israel's fiscal transformation from energy importer to exporter is now locked in: With approximately 50% of Leviathan export revenues flowing to government funds and contracts extending to 2040, the fiscal and geopolitical identity shift is effectively irreversible under current frameworks

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. All forecasts, projections, and scenario analyses are illustrative and subject to material uncertainty. Readers should conduct independent research and consult qualified advisers before making investment decisions.

Want to Track the Next Major Energy or Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and commodity data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.