June 22, 2026

The Hidden Architecture of a Tier-One Critical Minerals Empire

Few investment categories reward long-duration thinking more reliably than tier-one mining assets during structural commodity supercycles. The minerals underpinning the global energy transition — copper, zinc, platinum group metals, nickel, and germanium — share a common characteristic: their supply pipelines are measured in decades, not quarters. New mines of genuine scale take ten to twenty years to develop from discovery to full production. This geological and logistical reality means that companies already operating at the intersection of these commodities, with proven reserves, installed infrastructure, and established smelting capacity, occupy a position of structural scarcity that commodity price volatility alone cannot erode.

Against this backdrop, Ivanhoe Mines' Q1 2026 financial results and operational progress represent far more than a single quarter's scorecard. They reveal a company navigating a deliberate and carefully managed transition from disruption back to full operating capacity, across three of the most consequential mineral deposits in the world today.

When big ASX news breaks, our subscribers know first

Understanding What Tier-One Truly Means in Mining

The term tier-one is used loosely across the mining industry, but its technical definition carries specific weight. A tier-one asset must combine four characteristics simultaneously: it must be large in scale (typically capable of producing in the top quartile of its commodity globally), it must demonstrate exceptional ore grade, it must have a mine life extending beyond twenty years, and it must sit in the lower half of the global cost curve.

Very few mines in history satisfy all four criteria. Kamoa-Kakula, the Kipushi zinc complex, and the Platreef PGM project in South Africa collectively represent one of the most concentrated portfolios of tier-one assets under a single corporate umbrella in the contemporary mining sector.

This distinction matters to investors because tier-one assets behave differently from conventional mining operations during both market downturns and commodity rallies. Their low-cost positioning provides downside protection, while their scale and longevity amplify upside leverage when commodity prices strengthen. Furthermore, the growing critical minerals demand driven by the energy transition makes these assets even more strategically significant.

Q1 2026 Financial Performance: Reading Between the Lines

Headline Numbers and Their Context

Ivanhoe Mines financial results and operational progress for Q1 2026 produced an adjusted group EBITDA of approximately $191 million, with the Kamoa-Kakula Copper Complex contributing roughly $158 million of that total on an attributable basis. The company recorded a net loss of approximately $2 million for the quarter.

| Metric | Q1 2026 | FY 2025 Full Year |

|---|---|---|

| Net Result | ~$(2) million | $228 million profit |

| Adjusted EBITDA (Group) | ~$191 million | $578 million |

| Attributable EBITDA (Kamoa-Kakula) | ~$158 million | $569 million |

| Cash and Equivalents (Dec 31, 2025) | — | $885 million |

| Basic EPS (FY 2025) | — | $0.19 |

Disclaimer: Q1 2026 figures reflect transitional operating conditions during an active production ramp-up. Past financial performance is not indicative of future results. This article does not constitute financial advice.

The net loss figure will naturally attract attention, but sophisticated investors in capital-intensive industries understand why adjusted EBITDA is the more instructive metric during ramp-up phases. Non-cash charges including depreciation, amortisation on newly commissioned infrastructure, and costs associated with the ongoing Kakula mine dewatering programme all flow through the net income line without representing actual cash outflows from the business.

Quarterly Earnings Trajectory: The Story the Table Tells

To properly contextualise Q1 2026, the progression of Kamoa-Kakula's quarterly earnings through 2025 is essential reading:

| Quarter | Kamoa-Kakula Revenue ($'000) | Kamoa-Kakula EBITDA ($'000) |

|---|---|---|

| Q1 2025 | 973,397 | 594,337 |

| Q2 2025 | 875,289 | 325,181 |

| Q3 2025 | 566,365 | 195,597 |

| Q4 2025 | 866,044 | 331,121 |

| Q1 2026 | Ramp-up phase | ~158,000 (attributable) |

The Q3 2025 trough is the critical reference point. Revenue fell to $566 million and EBITDA compressed to $195 million, a decline driven primarily by the Kakula mine dewatering disruption. The subsequent recovery through Q4 2025 and into Q1 2026 demonstrates operational momentum, though the attributable EBITDA of $158 million in Q1 2026 reflects the fact that the complex is still rebuilding toward its pre-disruption run rate.

What the table does not show, but what matters enormously for forward valuation, is that the Q1 2025 figure of $594 million in EBITDA was generated before the smelter reached its current level of operational maturity. The acid credit contribution, discussed in detail below, was not at its full run rate during that period.

Balance Sheet as Operational Insurance

With $885 million in cash and equivalents at the close of FY 2025, Ivanhoe carries the liquidity to simultaneously manage dewatering operations at Kamoa-Kakula, complete Phase 2 earthworks at Platreef, sustain exploration drilling across four countries, and service its debt obligations — without being forced into capital markets at an inopportune moment.

In mining, the ability to execute a multi-year capital programme without dilutive equity issuance is a competitive advantage that rarely receives sufficient credit in short-term earnings analysis. However, investors monitoring the broader copper supply crunch will recognise that Ivanhoe's financial flexibility positions it well to capitalise on tightening market conditions.

Kamoa-Kakula: Dewatering, Ramp-Up, and the Sulphuric Acid Edge

The Dewatering Challenge Explained

Underground copper mines in the Central African Copper Belt frequently encounter elevated groundwater inflows, a consequence of the sedimentary geology that also produces the exceptionally high ore grades for which the region is renowned. At Kakula specifically, water inflow rates during 2025 required the diversion of significant underground mining capacity toward rehabilitation and water management rather than ore extraction.

Progress has been methodical rather than rapid. As of Q1 2026:

- 13.4 kilometres of underground workings have been successfully rehabilitated

- Dewatering in the western zone is approximately 70% complete

- Dewatering in the eastern zone stands at approximately 60% complete

- The dewatering timeline directly governs when the mine can return to full ore extraction rates

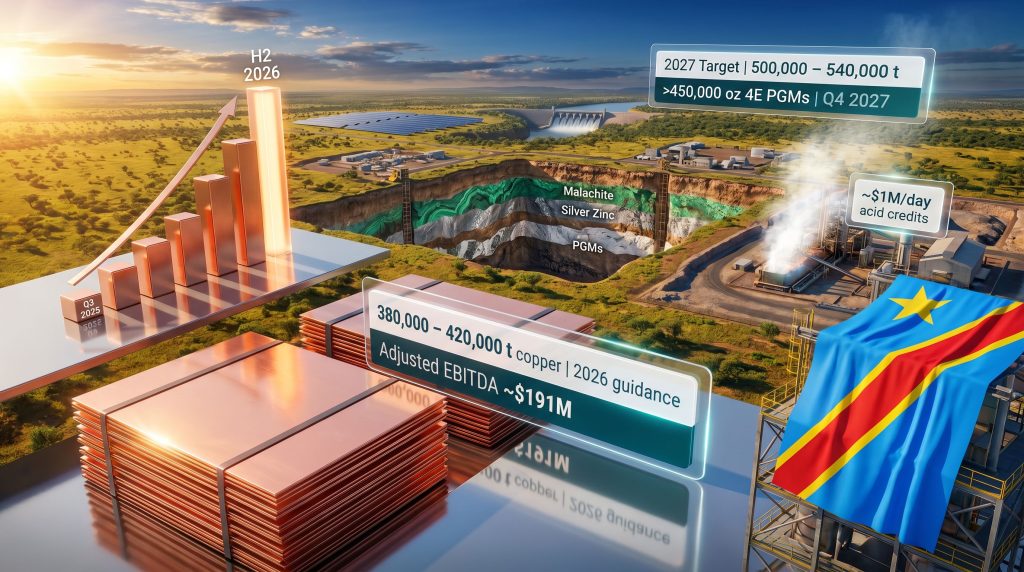

This means the critical path for meeting 2026 production guidance runs directly through the completion of this work. The guidance range of 380,000 to 420,000 tonnes of copper in 2026 accounts for the phased recovery, with the approximately 20,000-tonne smelter destock expected to reduce reportable sales volumes during the year.

2026 to 2028 Production Trajectory

| Production Period | Copper Output Guidance | Key Context |

|---|---|---|

| 2026 | 380,000 to 420,000 tonnes | Ramp-up phase; smelter destock impacts sales |

| 2027 | 500,000 to 540,000 tonnes | Post-dewatering full capacity |

| 2028 onward | >500,000 tonnes per year | 17 Mtpa steady-state, 25+ year mine life |

The jump from 2026 to 2027 guidance is not aspirational; it reflects the mechanical consequence of completing dewatering and restoring full mining rates to all underground panels. A feasibility study for the first five years of the long-term mine plan is currently underway, which will provide additional technical detail on the production profile beyond 2027.

The Sulphuric Acid Revenue Stream: A Structural Cost Advantage

One of the least-discussed aspects of integrated copper smelting is the commercial potential of sulphuric acid as a by-product. During the smelting process, sulphur dioxide gas is captured and converted into sulphuric acid (H2SO4) through a catalytic conversion process. The acid is then sold commercially, most commonly to the agricultural sector as a fertiliser input, and to industrial chemical processors.

At Kamoa-Kakula, acid credits are approaching approximately $1 million per day in operating cost offsets. To put this figure in perspective, that translates to roughly $365 million per year in potential cost reduction — an amount that fundamentally restructures the mine's effective C1 cash cost per pound of copper produced.

The acid credit mechanism functions as a structural cost hedge that most copper producers outside of integrated smelter operations simply cannot access. As diesel prices rise, they increase smelter operating costs across the industry. At Kamoa-Kakula, the high-grade ore body simultaneously enables the production of more acid per tonne of copper, partially self-insuring the operation against the same inflationary pressures that compress margins at competing mines.

This advantage is further amplified by Kamoa-Kakula's reported status as having the lowest hydrocarbon intensity per tonne of produced copper among major global mines — a function of its ore grade quality and its reliance on hydroelectric and solar power rather than diesel generation.

Why Clean Energy Infrastructure Creates a Durable Competitive Moat

Power sourcing is perhaps the most underappreciated variable in DRC mining economics. The country's electrical grid infrastructure outside of urban centres is fragile, and many mining operations rely heavily on diesel generation, which creates significant cost exposure and scope 1 emissions intensity.

Kamoa-Kakula's integration with hydroelectric power, supplemented by on-site solar capacity, achieves two things simultaneously. First, it materially reduces energy costs per tonne of copper produced. Second, it positions the operation with a carbon intensity profile that satisfies increasingly demanding ESG screens applied by institutional investors and development finance institutions. In an era where access to capital is increasingly conditioned on sustainability credentials, clean power infrastructure is not merely an operational asset — it is a financing advantage.

Platreef PGM Mine: Phase-by-Phase Toward a Giant

Where the Project Stands in Q1 2026

Platreef, located within South Africa's Bushveld Complex, is widely regarded as one of the world's premier undeveloped platinum group metal deposits. What distinguishes it geologically from conventional South African PGM operations is the breadth and consistency of its mineralisation, which allows for wide, mechanised stoping as opposed to the narrow reef mining that characterises older Bushveld operations.

The Phase 1 concentrator was commissioned in Q4 2025 and is currently processing development ore. The first concentrate sale was completed in late 2025, with delivery to Northam Platinum marking a commercial milestone for the project. The completion of Shaft #3 in March 2026 expanded hoisting capacity by approximately five times, to 5 million tonnes per annum, creating the physical infrastructure required for a significant acceleration in ore delivery to surface.

Development Roadmap

| Phase | Key Milestone | Target Timeline |

|---|---|---|

| Phase 1 | Concentrator at 80% capacity | Mid-2026 |

| Phase 1 | Ore hoisting via Shaft #3 | Early Q2 2026 |

| Phase 2 | Concentrator earthworks | On track |

| Phase 2 | >450,000 oz 4E PGMs + Ni/Cu | Q4 2027 target |

| Phase 3 | Shaft #2 widening to 8 Mtpa | 2028 target |

The Phase 2 production target of more than 450,000 ounces of 4E PGMs (platinum, palladium, rhodium, and gold) plus associated nickel and copper is the revenue inflection point for this operation. With a metals basket value exceeding $2,000 per ounce, the economics of Phase 2 production are materially superior to Phase 1, where ore is primarily sourced from development headings rather than long-hole stoping panels.

Long-hole stoping is a bulk underground mining method that becomes available once sufficient development infrastructure is in place. It allows for much higher tonnes-per-day extraction rates compared to development mining, which is why the transition to long-hole stoping at Platreef represents a step-change in production volume, not a linear increase.

The 4E PGM Basket and Why It Matters

The platinum and palladium dynamics at play in global markets make the 4E designation particularly important. It refers to the four platinum group metals most commonly found together in the Bushveld Complex: platinum, palladium, rhodium, and gold. Each has distinct supply-demand characteristics:

- Platinum faces structural demand from hydrogen fuel cell and autocatalyst applications

- Palladium remains in deficit due to its critical role in gasoline vehicle catalytic converters

- Rhodium commands extraordinarily high pricing due to its scarcity and use in emissions control

- Gold provides pricing stability as a monetary metal within the basket

The combination of these four metals, along with nickel and copper co-production, gives Platreef a revenue diversification profile that most single-commodity mines cannot match.

Kipushi: High-Grade Zinc and the Germanium Opportunity

Performance and Margin Recovery

Kipushi's Q3 2025 results demonstrated the margin expansion potential at a recently restarted operation as it moves along its production learning curve. Revenue of $129 million and EBITDA of $27 million represented a margin improvement from 10% in Q2 2025 to 21% in Q3 2025 — a near-doubling of profitability on similar revenue.

Kipushi produces zinc, copper, lead, and germanium. The ore grades are considered exceptionally high by global zinc mining standards, which directly translates to lower processing costs per unit of metal recovered and stronger margins across the commodity price cycle.

Germanium: The Critical Mineral Nobody is Talking About

Germanium occupies an unusual position in the critical minerals landscape. It is produced in relatively small volumes globally, with production historically concentrated in China. Its primary applications span:

- Fibre optic cables (germanium dioxide as a core dopant)

- Infrared optical systems used in military and aerospace applications

- Semiconductor substrates for advanced electronics

- Solar cells in high-efficiency photovoltaic applications

The concentration of global germanium supply in China, compounded by China export controls on strategic minerals, has driven Western governments to classify the metal as critical, with supply security measures being discussed across multiple jurisdictions. Kipushi's germanium by-product stream positions Ivanhoe as one of very few non-Chinese producers capable of contributing to this supply chain — a strategic reality that may attract industrial offtake interest beyond conventional commodity marketing channels.

For investors evaluating Kipushi's long-term value, the germanium contribution may be disproportionately significant relative to its current revenue share. As Western industrial policy continues to prioritise supply chain diversification for critical minerals, the premium attached to non-Chinese germanium production could increase materially over the next decade.

Note: Germanium pricing and demand projections involve significant uncertainty. Investors should not treat speculative upside scenarios as a base case.

The next major ASX story will hit our subscribers first

Western Forelands: Where the Next Giant May Be Found

The Makoko District Discovery

Exploration activity across Ivanhoe's Western Forelands licence package in the DRC has generated what company leadership describes as an emerging major copper system in the Makoko District. The geological setting is characterised as sedimentary-hosted copper mineralisation — a deposit type that has historically produced some of the world's largest copper endowments in the Central African Copper Belt.

The announcement of formal development plans for the Western Forelands is described as imminent. This represents a potential catalyst that the market may not have fully priced into Ivanhoe's current valuation, given that new tier-one copper discoveries of meaningful scale have become exceptionally rare globally.

| Jurisdiction | Exploration Focus | Strategic Rationale |

|---|---|---|

| DRC (Western Forelands) | Sedimentary-hosted copper | Tier-one scale potential |

| Angola | Copper exploration | Copper Belt extension geology |

| Zambia | Copper exploration | Established mining jurisdiction |

| Kazakhstan | Copper exploration | Geographic diversification |

The sedimentary-hosted copper discovery model used across these licence packages is geologically analogous to the processes that formed Kamoa-Kakula itself, providing confidence that the methodology has a proven track record in generating giant copper systems from this type of exploration targeting.

Scenario Analysis: What Could Drive Outperformance or Underperformance in 2026

Bull Case

- Kakula dewatering completes ahead of schedule, pushing production toward the upper bound of 420,000 tonnes guidance

- Copper prices sustain constructive levels, amplifying EBITDA margin recovery through H2 2026

- Western Forelands development announcement acts as an exploration re-rating catalyst

- Platreef Phase 1 reaches 80% concentrator capacity by mid-2026 as targeted

Base Case

- Dewatering progresses on the current timeline, with production landing in the middle of the guidance range

- Acid credits continue building toward the $1 million per day operating offset level

- Platreef Phase 2 earthworks stay on schedule, maintaining the Q4 2027 production target

- Kipushi continues its margin improvement trajectory through 2026

Bear Case

- Dewatering delays extend into H2 2026, skewing production toward the lower end of guidance

- Copper price correction compresses EBITDA margins despite the structural acid credit hedge

- Platreef ramp slower than anticipated, deferring PGM revenue contribution

- Geopolitical or regulatory developments in the DRC affect operational continuity

Key Risks Investors Should Understand

Jurisdictional and Geopolitical Exposure

Operating at scale in the DRC carries inherent risks that are distinct from those faced by mining companies in more stable jurisdictions. Regulatory frameworks, royalty structures, community relations, and infrastructure reliability all require continuous management. Ivanhoe's investment in energy self-sufficiency through hydroelectric and solar power partially mitigates infrastructure risk, but it does not eliminate broader country risk.

South Africa's mining policy landscape similarly requires ongoing monitoring, particularly regarding the Mineral Resources Development Act amendments that have been debated within the sector.

Capital Allocation Complexity

Running three simultaneous major operations in active ramp-up or expansion phases, alongside multi-country exploration programmes, creates significant demands on management bandwidth and capital allocation discipline. The $885 million cash position provides a meaningful buffer, but investors should track capital expenditure burn rates across all three operations as H2 2026 progresses.

Frequently Asked Questions

What were Ivanhoe Mines' key financial results for Q1 2026?

The full Q1 2026 results overview details adjusted group EBITDA of approximately $191 million, with Kamoa-Kakula contributing around $158 million on an attributable basis. A net loss of approximately $2 million was recorded, reflecting non-cash charges and transitional ramp-up costs rather than underlying operational deterioration.

Why does Kamoa-Kakula have an acid credit advantage?

The on-site copper smelter captures sulphur dioxide gas released during concentrate smelting and converts it into sulphuric acid. This acid is sold commercially, generating credits that approach $1 million per day in operating cost offsets, effectively functioning as a natural hedge against diesel price inflation in the DRC.

What is germanium and why does Kipushi's production matter?

Germanium is a semiconductor and optical material classified as a critical mineral due to its applications in fibre optics, military infrared systems, and advanced electronics. Global supply is historically concentrated in China, making non-Chinese production sources strategically important for Western supply chain security.

What is the Makoko District discovery?

Makoko is an emerging copper discovery within Ivanhoe's Western Forelands exploration licence area in the DRC. It is being characterised as a potentially giant sedimentary-hosted copper system, with development plans expected to be announced in the near term.

What is Platreef's Phase 2 production target?

Phase 2 targets production of more than 450,000 ounces of 4E platinum group metals, alongside nickel and copper, by Q4 2027.

The Long-Duration Investment Case

Q1 2026 is a transitional quarter. That framing is not an excuse for underperformance; it is the accurate description of where multiple simultaneous ramp-up processes sit on their respective operational curves. The dewatering at Kakula, the shaft commissioning at Platreef, and the margin recovery at Kipushi are all progressing as planned.

The more important question for long-duration investors is not whether Ivanhoe Mines financial results and operational progress in Q1 2026 matched Q1 2025 levels, but whether the infrastructure, ore bodies, and operational capabilities being built today will generate superior returns over the five, ten, and twenty-year horizons that tier-one assets are designed to serve.

A 25-plus-year mine life at Kamoa-Kakula operating at 17 million tonnes per annum steady-state, a multi-decade PGM operation at Platreef, a world-class zinc and germanium producer at Kipushi, and an exploration pipeline that may contain the next giant copper discovery collectively represent a critical minerals portfolio of genuine generational significance. Consequently, the Ivanhoe Mines financial results and operational progress narrative in 2026 is ultimately a story about long-term structural value, not short-term quarterly fluctuations.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. All forecasts and production guidance referenced represent company estimates and are subject to material risks and uncertainties. Investors should conduct independent due diligence before making any investment decisions.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across copper, zinc, PGMs, and other critical minerals — turning complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore Discovery Alert's discoveries page to see how historic finds have generated extraordinary returns, then start your 14-day free trial to position yourself ahead of the next major announcement.