May 19, 2026

Reading the Signals: What Japan's Aluminium Import Data Reveals About Asia's Industrial Recovery

Industrial commodity flows rarely move in isolation. When a resource-intensive economy like Japan begins pulling more primary aluminium through its ports, the data carries layered meaning beyond simple inventory restocking. Japan primary aluminium imports auto demand recovery reflects procurement decisions made weeks or months earlier, embedded within production schedules, order books, and assembly line forecasts. Understanding why those numbers are moving is far more instructive than simply noting that they are.

When big ASX news breaks, our subscribers know first

Japan's Role as Asia's Most Closely Watched Aluminium Demand Signal

Few markets compress as much analytical information into their aluminium import data as Japan. The country operates without meaningful domestic primary aluminium smelting capacity, making it entirely dependent on offshore supply for automotive-grade alloys, flat-rolled sheet, and extruded profiles. This structural reality transforms every monthly Finance Ministry customs release into a forward-looking indicator for regional demand.

Japan's automotive sector absorbs a disproportionately large share of both flat-rolled and extruded aluminium products. When vehicle output shifts direction, the upstream aluminium supply chain responds with measurable lag effects across import volumes, port inventories, and spot premiums. The country effectively functions as a live readout of how Asia's most technically demanding end-use market is performing at any given point in the cycle.

This dynamic makes the March 2026 import data particularly worth unpacking in detail.

Breaking Down the March 2026 Numbers: More Than a Headline Figure

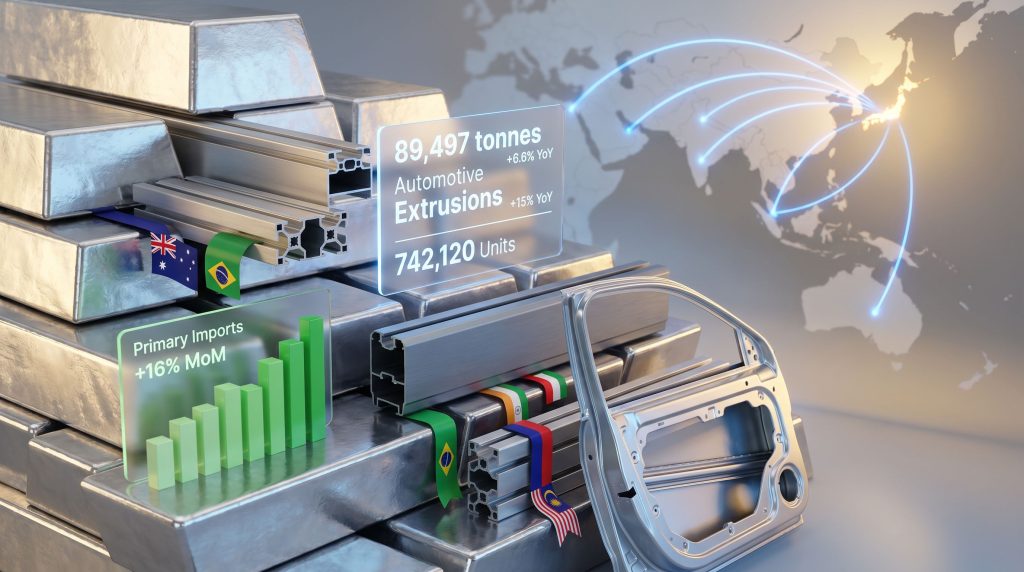

Japan's primary aluminium imports reached 89,497 tonnes in March 2026, representing a 6.6% increase year-on-year and a sharp 16% acceleration month-on-month. While the year-on-year gain is notable, it is the sequential jump that arguably carries more weight, pointing to a concentrated burst of procurement activity rather than a steady incremental recovery.

The full picture across key metrics is summarised below:

| Metric | Value | Change |

|---|---|---|

| Total primary aluminium imports | 89,497 tonnes | +6.6% YoY / +16% MoM |

| Flat-rolled products (can stock) | 33,639 tonnes | +3.6% YoY |

| Flat-rolled deliveries to automotive | 16,105 tonnes | +1.2% YoY |

| Extruded aluminium (automotive) | 13,149 tonnes | +15% YoY |

| Aluminium alloy ingots (ADC12) | 79,137 tonnes | -3% YoY |

| ADC12 average import value | USD 2,969/tonne | +5.6% YoY |

| Domestic vehicle production | 742,120 units | +8.8% YoY |

Data from Japan's Finance Ministry and the Japan Aluminium Association confirms that flat-rolled product shipments for can stock rose 3.6% year-on-year to 33,639 tonnes, supported in part by seasonal beverage production cycles. Automotive flat-rolled deliveries edged up 1.2% to 16,105 tonnes, consistent with the broader recovery in domestic vehicle assembly.

The Extrusion Recovery: A Six-Month Contraction Finally Breaks

Of all the individual data points in the March release, the performance of extruded aluminium destined for the automotive sector carries the sharpest analytical significance. Shipments in this category climbed 15% year-on-year to 13,149 tonnes, marking the first positive monthly reading after six consecutive months of contraction.

This is not a minor technical detail. Extended extrusion drawdowns typically indicate that assemblers are working through pre-existing inventory rather than ordering fresh material. A return to positive territory suggests that buffer stocks have been sufficiently depleted and that procurement teams are beginning to rebuild upstream inputs in anticipation of sustained production commitments. In short, it implies confidence in forward demand rather than defensive caution.

Domestic vehicle production data from eight major Japanese automakers, compiled by Argus, corroborates this interpretation. Output reached 742,120 units in March 2026, up 8.8% year-on-year, providing the demand foundation that justifies the restocking behaviour observed in aluminium procurement patterns.

The Recovery in Historical Context: 2023 to 2026

The current upturn needs to be read against a difficult two-year backdrop to be properly assessed. Japanese automotive aluminium demand was already showing momentum in the January to October 2023 period, with transportation applications accounting for 43.4% of total demand and rising approximately 9.9% year-on-year. That momentum then stalled. Furthermore, energy transition demand across Asia was simultaneously reshaping how industrial buyers were prioritising supply contracts during this period.

| Period | Automotive Aluminium Demand | Total Demand Trend |

|---|---|---|

| Jan-Oct 2023 | 43.4% of total demand | Transportation up 9.9% YoY |

| Jan-Nov 2024 | Fell 4.1% to 1.45M tonnes | Total demand down 3.3% |

| Full Year 2024 | Primary imports up 1.9% to 1.05M tonnes | Driven by supply diversification |

| March 2026 | Automotive extrusions +15% YoY | Vehicle output +8.8% YoY |

The 2024 contraction in automotive aluminium demand is a critical reference point. Total demand fell 3.3% over that period, with the automotive subsegment declining 4.1% to approximately 1.45 million tonnes. That dip makes the March 2026 reading look more like a genuine inflection rather than a continuation of existing momentum. The recovery is emerging from a trough, which adds credibility to the directional signal.

Sector Divergence: Which Applications Are Recovering and Which Are Not?

The March 2026 data does not present a uniform recovery narrative. Beneath the headline import growth lies a meaningful divergence between performing and underperforming end-use segments.

Performing sectors:

- Automotive extruded aluminium: +15% YoY to 13,149 tonnes

- Automotive flat-rolled sheet: +1.2% YoY to 16,105 tonnes

- Can stock flat-rolled products: +3.6% YoY to 33,639 tonnes

Underperforming sectors:

- Extruded aluminium for construction: -5.3% YoY to 27,221 tonnes

- Japan housing starts: -29% YoY to just 63,495 units in March 2026

- Aluminium foil production: declined to 7,608 tonnes

- Aluminium foil shipments: declined to 8,060 tonnes

The construction sector contraction deserves particular attention. A 29% collapse in housing starts is not a cyclical wobble. It represents a structural demand gap that directly suppresses extruded aluminium consumption in window frames, curtain walling, structural profiles, and architectural cladding. This segment has historically been one of the most volume-intensive aluminium end markets in Japan, and its ongoing weakness acts as a meaningful counterweight to automotive strength.

Battery Foil Weakness: A Counterintuitive EV Signal

The decline in aluminium foil demand presents an analytically interesting wrinkle. The Japan Aluminium Association has attributed part of this decline to softer demand from lithium-ion battery applications within the automotive supply chain. This creates an apparent paradox: traditional vehicle assembly aluminium is recovering strongly, while EV-specific aluminium components are weakening simultaneously.

The explanation likely lies in the uneven pace of Japan's EV transition. Traditional vehicle assembly, which relies heavily on structural extrusions and sheet products, is recovering faster than the EV-specific component manufacturing base. Battery cell and pack manufacturers appear to be operating through existing foil inventories rather than rebuilding positions. This bifurcation within the automotive supply chain is a genuinely important distinction that aggregate import figures can obscure. However, Asian aluminium demand across the broader region is anticipated to gradually recover as EV adoption accelerates in neighbouring markets.

How Japan's Aluminium Sourcing Geography Is Being Permanently Redrawn

The composition of Japan's primary aluminium supply has undergone a structural realignment since 2022, driven by a deliberate strategy of geographic diversification away from sanctioned Russian material. The March 2026 country-level data captures where this realignment currently stands. In addition, top aluminium producers globally have been repositioning their long-term supply agreements to accommodate this shift in Japanese procurement strategy.

| Supplier Country | March 2026 Volume | YoY Change | Q1 2026 Volume | Q1 YoY Change |

|---|---|---|---|---|

| Australia | 22,756 tonnes | -9.1% YoY / -14% MoM | 75,260 tonnes | +1.1% |

| Brazil | 19,504 tonnes | +7.4% YoY | 50,698 tonnes | +45.1% |

| India | 13,619 tonnes | >+100% YoY | 25,941 tonnes | +19.1% |

| UAE | 8,710 tonnes | +9.9% YoY | 28,534 tonnes | +9.4% |

| Malaysia | 7,545 tonnes | +836.9% YoY | 13,570 tonnes | +108.3% |

Australia retains the top position by volume at 22,756 tonnes in March, but the 9.1% year-on-year and 14% month-on-month decline indicates it is losing relative share to more aggressively growing alternatives. Brazil's first-quarter surge of 45.1% to 50,698 tonnes is particularly significant in absolute terms, reflecting deliberate contract reallocation toward South American smelters that can supply high-quality primary ingot at competitive premiums.

India's emergence is arguably the most structurally interesting development. Imports more than doubled year-on-year to 13,619 tonnes in March, with the first quarter up 19.1% to 25,941 tonnes. Indian smelting capacity has been expanding steadily, supported by domestic bauxite and coal resources, and Japanese buyers appear to be treating Indian supply as a credible long-term alternative to traditional Western Pacific sources.

Malaysia's 836.9% surge demands context. The absolute volume of 7,545 tonnes remains modest relative to Australia's position, and the extraordinary percentage reflects a low comparison base from 2025. However, the directional consistency across India, Brazil, UAE, and Malaysia collectively confirms a sustained procurement strategy rather than opportunistic spot buying. Consequently, aluminium sector investment is increasingly flowing toward supply chains that serve Japan's diversification priorities.

The next major ASX story will hit our subscribers first

Pricing Dynamics: The ADC12 Divergence

One of the more technically interesting signals embedded in the March data is the simultaneous decline in ADC12 alloy ingot import volumes alongside rising per-tonne values. Volumes fell 3% year-on-year to 79,137 tonnes, yet the average import value climbed 5.6% to USD 2,969 per tonne.

When import values rise while volumes fall, the most likely explanation is tighter supply conditions at origin rather than demand-led price pressure at destination. Buyers are paying more precisely because availability has tightened, not because domestic consumption has accelerated beyond supply capacity.

ADC12 is the workhorse die-casting alloy used extensively in automotive powertrain and structural casting applications. Its pricing trajectory therefore functions as a proxy for how tightly the automotive casting supply chain is stretched globally. Rising values alongside volume declines suggest that upstream alloy producers, particularly in Southeast Asia and South Asia where much of Japan's ADC12 originates, are operating closer to capacity constraints than the headline import volumes would suggest.

Structural Risks That Could Interrupt the Recovery Trajectory

Several material risks complicate any straightforward optimistic reading of the March 2026 data:

-

Construction sector weakness remains severe. A near-30% decline in housing starts is not a demand softening that typically self-corrects within a single quarter. If residential construction activity remains depressed through 2026, the suppression of extruded aluminium demand in this segment will continue to offset automotive gains.

-

Global trade disruption risks represent a meaningful premium uncertainty. The aluminium tariff impacts flowing from recent US trade policy have added complexity to global supply flows, and Japan's import costs remain sensitive to freight rate volatility, currency movements, and any renewed disruptions to key Pacific and Indian Ocean trade lanes.

-

EV transition timing uncertainty could weigh on battery foil and associated aluminium demand. If Japan's EV ramp accelerates faster than expected, aluminium foil demand could recover sharply. If the transition remains slower than anticipated, the weakness in this segment could persist longer than consensus currently assumes.

-

Port inventory management remains a live variable. Japanese buyers have historically managed port stocks carefully, and any accumulation of excess inventory at major ports could suppress the import pull in subsequent months even if underlying demand remains healthy.

Japan's Long-Term Aluminium Vision and What It Means for Import Dependency

Japan's national aluminium industry roadmap, commonly referenced as Aluminium VISION 2050, envisions a significant expansion of domestic recycling capacity alongside sustained demand growth concentrated in transportation applications. The ambition is to reduce the economy's dependence on primary aluminium imports by increasing the recovery and reuse of post-consumer and post-industrial scrap.

However, the structural reality of automotive-grade alloy requirements creates a ceiling on how far recycled content can displace primary metal in the near term. High-performance automotive extrusion alloys and body sheet products carry strict chemical composition tolerances that recycled streams often cannot meet without dilution with primary material. Japan's automotive assemblers, who compete in global markets on the basis of precision engineering and material consistency, are unlikely to compromise on alloy quality in pursuit of recycled content targets.

The practical implication is that Japan primary aluminium imports auto demand recovery will remain a critical indicator of Japanese industrial health well into the 2030s, regardless of how aggressively recycling capacity is expanded. The VISION 2050 framework is better understood as a demand modifier than a demand displacer. Furthermore, China industrial demand trends will continue to influence the broader pricing environment within which Japan's import premiums are negotiated.

Key Takeaways for Market Participants

- The extrusion recovery is the most significant structural signal in the March 2026 dataset, ending six months of contraction and pointing to genuine restocking behaviour in the automotive supply chain

- India and Brazil are emerging as the primary beneficiaries of Japan's geographic diversification strategy, with both recording strong absolute and percentage volume growth in Q1 2026

- Construction weakness and battery foil declines are material demand offsets that prevent March's figures from being interpreted as a broad-based industrial boom

- Rising ADC12 values alongside falling volumes points to upstream supply tightness rather than a softening of downstream automotive demand

- Malaysia's percentage surge should be read cautiously given its low absolute base, but the directional trend across multiple emerging suppliers confirms a structural shift in procurement strategy

- Primary import dependency is structurally embedded in Japan's industrial model and will remain so regardless of recycling ambitions, making monthly import data a reliable leading indicator through at least the next decade

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Historical data and forward-looking statements about aluminium market trends involve inherent uncertainty. Readers should conduct independent research before making investment or procurement decisions based on commodity market data.

Want to Capitalise on the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity data into actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.