May 19, 2026

The World's Most Vulnerable Energy Corridor: Why Hormuz Defines Global Oil Security

Every barrel of crude oil is a geopolitical object. It does not simply flow from reservoir to refinery; it moves through infrastructure that is simultaneously a commercial asset and a strategic target. Nowhere is this tension more acute than in the Strait of Hormuz, a narrow channel of water between the Persian Gulf and the Gulf of Oman where the architecture of global energy supply is compressed into a 33-kilometre passage. When naval forces from multiple great powers converge in this space, the consequences extend far beyond the waterway itself, reaching into commodity markets, insurance pricing, diplomatic back-channels, and the long-term investment calculus of energy-importing nations.

The current standoff involving the Iran response to French and British warships in the Strait of Hormuz is not simply a news event. It is a stress test of the entire governance architecture, or more precisely, the absence of one, that currently manages the world's most critical energy chokepoint.

When big ASX news breaks, our subscribers know first

The Physical and Strategic Weight of a 33-Kilometre Passage

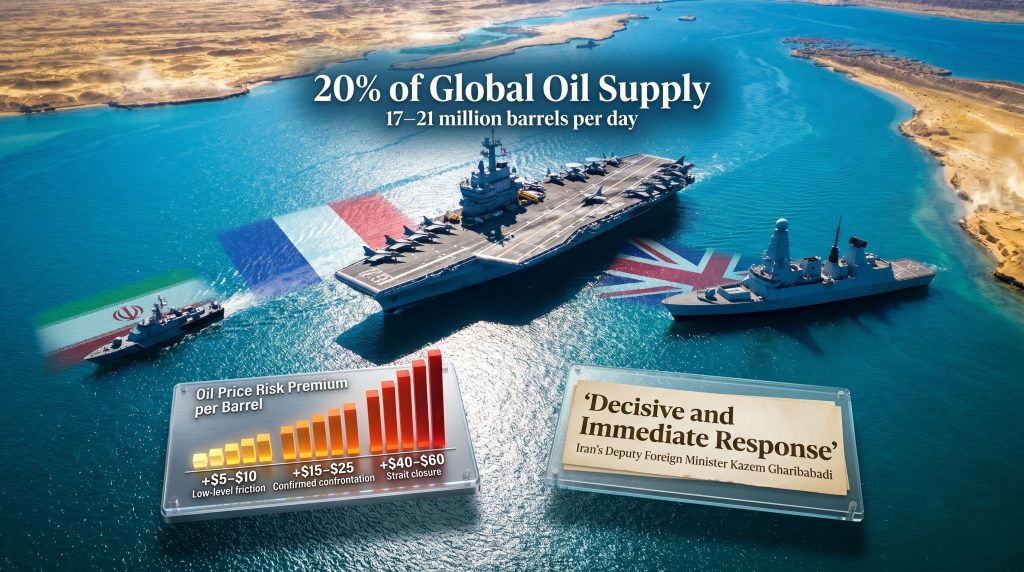

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman and onward to the Arabian Sea, forming the only maritime exit route for crude oil produced by Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, and Iran itself. According to the U.S. Energy Information Administration (EIA), approximately 17 to 21 million barrels of oil per day transit through the strait, representing roughly 20% of global petroleum liquids supply (EIA, World Oil Transit Chokepoints, 2023).

What makes this figure strategically alarming is the absence of a credible alternative. While the Strait of Malacca handles comparably large volumes of energy trade for Asia-Pacific commerce, the Persian Gulf exporters are structurally locked into Hormuz as their primary outlet. The only partial bypass infrastructure is the Abu Dhabi Crude Oil Pipeline, which can divert a portion of UAE exports, and Saudi Arabia's East-West Pipeline to the Red Sea. Neither can absorb a full Hormuz closure at scale, and neither addresses the export needs of Iraq, Kuwait, or Iran at all.

A Corridor With a Long Memory of Conflict

The militarisation of the Strait of Hormuz is not a recent phenomenon. During the 1980s Iran-Iraq War, both nations conducted attacks on commercial tankers in what became known as the Tanker War, a sustained campaign of maritime economic warfare that drew the United States into active naval convoy operations under Operation Earnest Will from 1987 to 1988. That operation, the largest naval convoy operation since World War II, established the precedent of Western military forces actively protecting commercial shipping lanes in the Gulf.

The 2019 escalation cycle reinforced this precedent with modern urgency. A series of tanker seizures, drone strikes, and limpet mine attacks on vessels near the strait, attributed by Western governments to Iranian forces, prompted the United States and its allies to establish maritime security operations in the region. That period demonstrated a well-documented historical pattern: Hormuz tensions correlate with short-term oil price volatility of roughly 10 to 25%, depending on the severity and duration of the perceived threat.

The current deployment of European naval assets, including the French nuclear-powered aircraft carrier Charles de Gaulle, confirmed by the French Ministry of Armed Forces as travelling toward the region in May 2026, fits within this decades-long pattern of Western intervention. Furthermore, it carries unique political weight given its explicit association with a joint initiative by French President Emmanuel Macron and British Prime Minister Keir Starmer. Understanding the broader crude oil geopolitical factors at play helps contextualise why this deployment carries such significant market implications.

Iran's Legal and Strategic Position on Foreign Warships

Sovereignty, UNCLOS, and the Innocent Passage Dispute

Iran's objections to foreign naval deployments in the Strait of Hormuz are not purely rhetorical. They rest on a specific legal argument rooted in the United Nations Convention on the Law of the Sea (UNCLOS), which governs maritime rights and passage through international straits. Iran and Oman jointly administer the strait under overlapping territorial and contiguous zone claims. Tehran's position has long been that UNCLOS provisions permitting innocent passage do not extend to militarised naval operations or carrier group deployments, which it characterises as coercive power projection rather than neutral transit.

This legal distinction matters because it allows Iran to frame European naval deployments not as legitimate shipping protection exercises but as acts of strategic alignment with what its officials describe as unlawful American maritime conduct. Iran's Deputy Foreign Minister Kazem Gharibabadi made this argument publicly in May 2026, stating that any foreign naval cooperation with current US maritime strategy in the strait would be treated as a direct provocation warranting a decisive and immediate response (IRNA, May 2026, as reported by ANI/ETEnergyworld, 11 May 2026).

"Policy Framing: Tehran's position draws a deliberate distinction between the protection of commercial shipping, which it has not formally opposed as a principle, and the deployment of carrier groups or warships operating in coordination with US forces, which it interprets as hostile military encirclement."

Decoding the Deterrence Language

The phrase "decisive and immediate response" requires careful analytical parsing. In Iranian strategic communication, such language has served different purposes at different moments. Analysts who study Persian Gulf security dynamics identify at least three interpretive frameworks:

- Tactical signalling designed to raise the perceived cost of Western naval operations without committing to a specific military action.

- Domestic political messaging directed at hardline factions within Iran's political establishment who demand visible assertiveness in the face of perceived foreign aggression.

- Genuine rules-of-engagement recalibration, particularly credible when paired with the Revolutionary Guards' separate warning of heavy attacks against American interests following reported strikes on Iranian-flagged vessels.

The simultaneous escalation of language from both the Foreign Ministry and the Revolutionary Guards, which operate with a degree of strategic independence, is a significant signal. When both institutional voices converge on the same threat posture, historical precedent from 2019 suggests a higher probability that at least a limited operational response is being prepared rather than purely managed through rhetoric.

What Prompted the European Naval Deployment

Macron, Starmer, and the Freedom of Navigation Mandate

The Franco-British initiative represents the most significant European military commitment to Gulf shipping security since the 2019 formation of the European-led maritime awareness mission, EMASOH. The explicit framing of the Charles de Gaulle deployment as a mission to restore confidence among commercial shipowners reflects a genuine commercial concern: repeated attacks on tankers near the Strait of Hormuz and the Qatari coastline have substantially elevated shipping insurance costs, disrupted voyage planning, and reduced the number of operators willing to transit the region without military protection.

The political calculus behind the deployment involves at least three intersecting motivations. First, Europe's residual energy import exposure through Hormuz, while partially mitigated by LNG supply outlook improvements post-2022, remains non-trivial. Second, the deployment signals NATO cohesion and European strategic autonomy at a moment when transatlantic burden-sharing is under considerable political strain. Third, France in particular has commercial and diplomatic interests in the Gulf that make visible engagement with maritime security a foreign policy priority.

Comparing the Two Sides of the Argument

| Factor | Western Position | Iranian Position |

|---|---|---|

| Legal basis | UNCLOS innocent passage rights | Territorial sovereignty and security doctrine |

| Stated objective | Restore shipowner confidence; protect commercial lanes | Perceived as hostile military alignment with US |

| Escalation risk assessment | Deterrence through presence | Provocation requiring decisive response |

| Diplomatic framing | Multilateral shipping security mission | Unilateral foreign military interference |

| Historical precedent cited | 1987–88 Operation Earnest Will | 2019 seizures as defensive responses to foreign pressure |

Iran's Diplomatic Track: The 14-Point Counter-Proposal

A Dual-Track Strategy Running in Parallel

One of the most analytically important features of the current situation is that Iran's military deterrence posturing is occurring simultaneously with substantive diplomatic engagement. Tehran formally submitted its response to the most recent US de-escalation proposal in May 2026, transmitted through Pakistani diplomatic intermediaries, a channel consistent with Iran's historical preference for using trusted third-party nations including Oman, Switzerland, and Qatar in sensitive communications with Washington.

According to Iran's state-run IRNA news agency, Tehran developed a 14-point counter-proposal to the US-backed nine-point peace framework. The plan reportedly structures de-escalation in three stages, with the first phase involving a 30-day transitional period designed to convert a temporary ceasefire into a durable cessation of hostilities.

The key demands embedded within the Iranian framework include:

- Comprehensive sanctions relief targeting Iran's energy and financial sectors.

- Removal of restrictions on Iranian port access, which affects both trade and humanitarian supply chains.

- Withdrawal of US military forces from the broader region.

- A halt to Israeli military operations in Lebanon.

"Analytical Note: The simultaneous submission of a diplomatic proposal and the issuance of military deterrence warnings is consistent with Iran's dual-track foreign policy tradition. It maximises negotiating leverage while signalling that military options remain on the table if talks collapse."

Why Pakistan Matters as an Intermediary

The selection of Pakistan as the transmission channel for Iran's diplomatic response is not incidental. Pakistan maintains functional relationships with both Tehran and Washington while possessing credibility in the Islamic world that Oman or Switzerland may not project equally. The choice signals that the communication being transmitted carries weight and is not a performative gesture.

It also suggests that both parties have agreed to the mediation arrangement, which is itself a form of tacit bilateral engagement, despite the absence of direct US-Iran talks. The risk to this diplomatic track is acute. In the compressed decision-making environment of naval confrontation, a single incident at sea, the disabling of a vessel, a warning shot that escalates, or a miscommunication between commanders, could collapse the diplomatic architecture before a framework agreement is reached.

Oil Market Implications: Pricing the Hormuz Risk Premium

How Geopolitical Risk Embeds Itself in Crude Pricing

Energy traders and commodity analysts model Hormuz disruption risk through what is conventionally called the geopolitical risk premium, the additional cost per barrel that markets assign to crude oil when supply route security is uncertain. This premium is not uniform; it scales with the perceived severity and duration of the threat. Consequently, an oil price shock scenario becomes increasingly plausible as military posturing intensifies.

Based on historical precedent from prior Gulf tension episodes, analysts have modelled the following price impact scenarios:

| Scenario | Price Impact Estimate | Duration |

|---|---|---|

| Low-level friction (vessel harassment, warning shots) | +$5 to $10 per barrel | Short-term spike, typically 1–2 weeks |

| Confirmed naval confrontation (vessel seizure or disabling) | +$15 to $25 per barrel | Sustained premium, weeks to months |

| Strait partial blockade or closure | +$40 to $60 per barrel | Potentially sustained; triggers IEA reserve releases |

The current environment already contains multiple compounding risk signals: reported strikes on commercial shipping near the Strait of Hormuz and the Qatari coastline, reports that a US fighter jet disabled two Iranian-flagged vessels in the Gulf of Oman, and the Revolutionary Guards' explicit warning of heavy attacks against American interests. Each of these individually would be sufficient to generate a modest risk premium. In combination, they represent an unusually dense cluster of escalatory indicators.

Who Bears the Greatest Exposure

The vulnerability to a Hormuz disruption is not evenly distributed. Asia-Pacific importing nations carry the heaviest volumetric exposure because they source the largest share of their crude oil from Persian Gulf producers with no Hormuz bypass capacity.

- India, China, Japan, and South Korea collectively account for the majority of Hormuz-transiting crude oil imports and have limited ability to substitute at scale on short notice.

- European importers face secondary exposure, partially mitigated by expanded LNG infrastructure built since 2022 and overland pipeline alternatives from Russia's former supply network.

- US domestic markets are relatively insulated by shale production volumes, but remain exposed through global benchmark pricing mechanisms that transmit Hormuz risk premiums into domestic fuel costs regardless of import origin.

A less widely understood dimension of disruption cost involves the shipping insurance market. During acute Hormuz tension episodes, war risk premium surcharges on Gulf-routed tankers have historically increased by 300 to 500%, according to Lloyd's of London market data from prior Gulf crises. These surcharges are passed directly into delivered energy costs, meaning that even a non-blocking disruption imposes measurable inflationary pressure on every barrel transiting the strait.

The next major ASX story will hit our subscribers first

Scenario Modelling: Four Pathways Forward

Geopolitical risk analysis requires scenario framing rather than point predictions. The following four pathways represent structurally distinct outcomes, each with different implications for energy markets, diplomatic engagement, and regional stability.

Scenario 1: Diplomatic Resolution (Low Probability, Near-Term)

Iran's 14-point framework is accepted in modified form, naval deployments are scaled back by mutual agreement, and a ceasefire framework enters its transitional phase. The risk premium fades over weeks, shipping confidence recovers, and insurance premiums normalise.

Scenario 2: Frozen Standoff (Moderate Probability)

Diplomatic talks continue without breakthrough. Naval presence is maintained by all parties. No direct confrontation occurs, but the persistent threat keeps a meaningful risk premium embedded in crude pricing and sustains elevated insurance costs indefinitely.

Scenario 3: Controlled Escalation (Moderate-High Probability)

A vessel seizure or disabling incident triggers a limited military exchange. Both sides exercise restraint and pull back from full confrontation. A short-term oil price spike of $15 to $25 per barrel accelerates diplomatic engagement and potentially produces a ceasefire framework under international pressure.

Scenario 4: Uncontrolled Escalation (Lower Probability, Highest Impact)

A miscalculation, the 1988 USS Vincennes incident remains the historical case study in how quickly Gulf naval confrontations can escalate beyond intent, triggers a broader exchange. The IEA activates coordinated strategic petroleum reserve releases. A $40 to $60 per barrel price shock disrupts global energy supply chains and compresses the near-term feasibility of energy transition investments.

The Governance Vacuum at the Heart of the Hormuz Problem

Why No Framework Currently Governs the Strait

Perhaps the most underappreciated structural factor in the current crisis is the complete absence of a multilateral maritime security framework specific to the Strait of Hormuz. Unlike the Black Sea, where Turkey's Montreux Convention provides a legal architecture for managing competing naval interests, or even the South China Sea, where UNCLOS arbitration panels have issued binding rulings, the Hormuz corridor operates under competing and irreconcilable legal interpretations with no dispute resolution mechanism.

This governance vacuum is not accidental. It reflects decades of US-Iran antagonism that has made bilateral treaty negotiation impossible, combined with a broader Western preference for operational maritime security missions over formal legal frameworks. The result is a situation where every naval deployment, every vessel seizure, and every deterrence statement is interpreted through incompatible legal frameworks by the parties involved, maximising the risk of miscalculation.

Long-Term Structural Implications for Energy Supply Chains

The current standoff reinforces several long-term structural trends that have independent momentum regardless of how the immediate crisis resolves. The investment case for LNG infrastructure as a Hormuz hedge has strengthened meaningfully across European and Asian markets since 2022. Strategic petroleum reserve capacity, while a viable short-term buffer, is explicitly not designed to absorb a prolonged Hormuz disruption; the IEA's coordinated reserve releases in 2022 following the Ukraine conflict demonstrated both the utility and the limits of this instrument.

Furthermore, the Iran response to French and British warships in the Strait of Hormuz cannot be fully assessed without acknowledging broader market forces. OPEC's market influence and the ongoing effects of trade war oil prices together create a compounding set of pressures that amplify the economic consequences of any Hormuz disruption.

Perhaps most consequentially for energy transition timelines, a sustained Hormuz risk premium raises the delivered cost of fossil fuels globally, which has a paradoxical dual effect: it accelerates the commercial case for renewable energy investment while simultaneously constraining the fiscal capacity of energy-importing economies to fund that transition. The strait's instability, in other words, has consequences that extend well beyond the commodity markets where its effects are most immediately visible.

Disclaimer: This article contains scenario projections and market impact estimates based on historical precedent and publicly available analytical frameworks. These projections do not constitute financial advice. Geopolitical developments are inherently unpredictable, and actual outcomes may differ materially from any scenario described. Readers should conduct independent analysis before making any investment or commercial decisions based on the information presented.

Want To Stay Ahead of the Market Moves Triggered by Geopolitical Shocks Like Hormuz?

When energy corridors come under threat and commodity markets reprice risk overnight, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex market signals into actionable opportunities before the broader market catches up. Explore historic discovery returns that demonstrate what early positioning can achieve, and begin your 14-day free trial at Discovery Alert to secure your market-leading edge.