June 24, 2026

The Structural Fault Line in Japan's Automotive Supply Chain

The global aluminium market has long operated on the assumption that geographic concentration in low-cost smelting regions is an acceptable trade-off for procurement efficiency. For decades, that assumption held reasonably well. Today, Japan carmakers aluminium supply risks in the Middle East are being stress-tested in ways that expose deep vulnerabilities within Japan's automotive manufacturing base. The intersection of geopolitical disruption, technical alloy specifications, and rigid qualification timelines has created a procurement crisis with no quick resolution.

Understanding what is unfolding requires more than tracking LME prices. It demands an appreciation of how aluminium supply chains actually function at the physical level, why certain alloy grades cannot simply be replaced, and what the realistic timeline for market normalisation looks like when smelter infrastructure has been damaged beyond rapid repair.

When big ASX news breaks, our subscribers know first

Why Japan Carries More Risk Than Any Other Major Importer

The Mathematics of Concentration Risk

Among the world's five largest aluminium-importing nations, Japan stands apart for a single, defining reason: approximately 30% of its total aluminium and aluminium alloy imports originate from the Gulf region, representing the highest proportional dependency of any major importer according to 2024 UN Comtrade data.

This is not a coincidence or an oversight. It reflects deliberate procurement decisions made over several decades as Japanese manufacturers prioritised cost efficiency and supply stability through long-term offtake agreements with Gulf producers. The Gulf's competitive advantage in aluminium smelting is structurally sound: abundant natural gas provides cheap energy, while proximity to shipping lanes facilitates efficient logistics. Those advantages, however, also concentrated risk in a single geographic corridor.

The dependency structure creates a vulnerability that compounds across several dimensions:

- Japan imports aluminium for a highly diverse range of applications, from beverage packaging to aerospace-grade components, but the automotive sector's alloy-specific requirements mean that commodity-grade substitutes from elsewhere cannot simply fill the gap

- The 18-month average timeline required to qualify and onboard new aluminium suppliers means that diversification decisions made today will not yield procurement flexibility until mid-2026 at the earliest

- Japanese trading houses with established Gulf relationships built their entire logistics and quality assurance infrastructure around those supply chains, creating switching costs that extend beyond price

- The concurrent loss of Russian alloy supply following the Russia-Ukraine conflict had already pushed Japanese buyers further toward Gulf sources between 2021 and 2024, deepening the concentration precisely when geopolitical risk was rising

The Hormuz Dual Chokepoint: A Mechanism Often Misunderstood

Most analysis of Strait of Hormuz disruption focuses on outbound oil and gas flows. For aluminium, the risk geometry is fundamentally different and arguably more acute. Furthermore, understanding the aluminum and alumina markets provides important context for appreciating why this chokepoint matters beyond simple shipping disruption.

Gulf aluminium smelters are net importers of their primary raw material. In 2025, the Middle East produced an estimated 6.15 million tonnes of primary aluminium. Under standard industry conversion ratios, this required approximately 13.08 million tonnes of alumina and between 26.16 and 39.24 million tonnes of bauxite, both of which must be imported, primarily from Australia and Guinea, through the same Strait of Hormuz that exports finished metal to Asian buyers.

This bidirectional dependency is a distinguishing feature of Gulf aluminium risk. A sustained Hormuz disruption does not merely slow outbound metal shipments to Japan. It simultaneously starves smelters of the raw materials needed to maintain production, creating a cascading supply contraction that worsens over time rather than stabilising.

This mechanism means that supply disruption estimates based solely on existing inventory drawdowns systematically understate the true market impact. As raw material pipelines to Gulf smelters thin out, production volumes decline, and the downstream export shortfall accelerates beyond what immediate shipping disruptions alone would suggest.

Quantifying the Supply Gap: What the Numbers Actually Reveal

Production Losses at a Scale the Market Has Not Seen Recently

The Middle East accounts for roughly 20% of global aluminium supply outside China, where most domestically produced metal is consumed internally. The scale of potential disruption to this supply base is significant enough to reshape global trade flows rather than merely adjust regional premiums.

| Metric | Estimate |

|---|---|

| Middle East primary aluminium production (2025) | 6.15 million tonnes |

| Middle East share of ex-China global supply | ~20% |

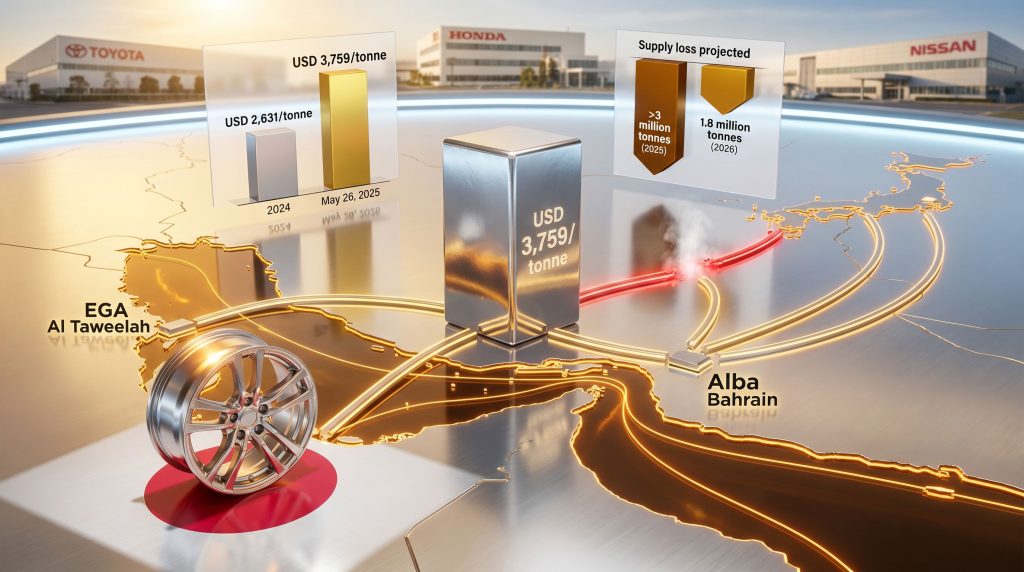

| Estimated 2025 supply loss | >3 million tonnes (~10% of ex-China supply) |

| Projected additional 2026 supply loss | ~1.8 million tonnes |

| Minimum restart timeline for Al Taweelah and Alba | 1 year post-assessment |

| Full regional capacity restoration | Not before 2028 |

Wood Mackenzie analysis indicates that more than 3 million tonnes of aluminium supply could leave the market during 2025 alone. Damaged infrastructure at facilities linked to Emirates Global Aluminium's Al Taweelah plant and Aluminium Bahrain (Alba) creates a technically constrained recovery timeline that commercial urgency cannot accelerate.

Qatar's Qatalum facility added further pressure to regional production volumes after reducing output in early 2025 due to natural gas supply constraints. The convergence of these distinct but simultaneous pressures has produced a supply contraction that analysts at Wood Mackenzie describe as requiring a minimum of one year from the point of damage assessment before Al Taweelah and Alba return to full capacity. According to reporting on Japan's carmakers navigating this supply squeeze, complete Middle Eastern restoration is not expected before 2028.

Why Smelter Restarts Take Longer Than Most Outsiders Expect

A critical piece of technical context is frequently omitted from mainstream coverage of aluminium supply disruptions. When a smelter is shut down, the molten aluminium inside the electrolytic pots solidifies. Before any structural damage assessment can even begin, this solidified metal must be physically removed from the pots, a labour-intensive and time-consuming process with no shortcut.

Uday Patel, senior research manager at Wood Mackenzie, has confirmed that once smelters shut down, the solidified aluminium inside smelter pots must be removed before damage assessments can even proceed. His analysis projects that Al Taweelah and Alba would require a minimum of one year to return to full operational capacity after assessments are complete.

This technical reality establishes a hard floor on recovery timelines regardless of financial incentives or political pressure to restore production. The industrial physics of aluminium smelting create an irreducible minimum timeframe that market optimism cannot compress.

LME Pricing: Elevated, Backwardated, and Structurally Significant

| Period | LME Aluminium Price |

|---|---|

| 2024 average (baseline) | USD 2,631/tonne |

| May 26, 2025 cash offer price | USD 3,759/tonne |

| May 26, 2025 three-month offer price | USD 3,682/tonne |

| BMI 2025 full-year forecast average | USD 3,100/tonne |

| BMI 2027 forecast average | USD 2,931/tonne |

Prices reached their highest level since March 2022 as of late May 2025, representing a move of approximately 43% above the 2024 average in spot terms. The market has simultaneously entered backwardation, where immediate delivery prices exceed forward prices, a configuration that signals acute near-term physical tightness rather than speculative activity.

For procurement teams, backwardation creates an uncomfortable reality: forward hedging strategies that normally provide cost certainty do not protect against today's elevated spot costs. Buyers who need physical metal now face the full brunt of the price spike, while those with existing inventory buffers gain only a temporary advantage. Exploring commodity hedging strategies has consequently become a priority for manufacturers seeking to manage this exposure.

It is worth noting that the price elevation did not begin with the 2025 geopolitical disruptions. Energy-related smelter curtailments had already pushed aluminium above its long-term average before Gulf tensions escalated, meaning the market entered this disruption from an already-stressed baseline rather than from equilibrium.

The Earnings Impact on Japan's Automotive Sector

Procurement Cost Escalation: Two Layers of Pressure

Japanese automotive manufacturers are absorbing what can be characterised as a dual cost shock. Rising LME base prices establish a higher floor for all aluminium purchases, while simultaneously surging regional import premiums add a second layer of cost that is independent of the underlying commodity price.

The Japan import premium for the April to June 2025 quarter surged to USD 350 to 353 per tonne, compared with USD 195 per tonne in the previous quarter, representing an increase of approximately 80% quarter-on-quarter. Buyers entering the July to September 2025 negotiation cycle are doing so against a backdrop where European and US premiums remain structurally higher, establishing a challenging benchmark for Asian buyers competing for scarce cargoes.

Procurement teams at Japanese automakers face a compounding problem. It is not merely that aluminium costs more. It is that every component of the total delivered cost, including the LME base price, the regional premium, and the logistics cost associated with longer shipping routes from alternative suppliers, has increased simultaneously.

Automaker Financial Exposure: The Scale of the Problem

| Automaker | Projected Financial Impact | Primary Driver |

|---|---|---|

| Toyota | ¥670 billion (FY ending March 2027) | ¥400 billion from higher material costs |

| Mitsubishi Motors | ¥30 billion (current fiscal year) | Approximately 50% from aluminium and materials |

| Nissan Motor | ¥15 billion (H1) | Weaker sales combined with raw material costs |

The combined projected earnings impact across these three manufacturers alone exceeds ¥715 billion, and this figure does not capture the broader exposure across the hundreds of Tier 1, Tier 2, and Tier 3 suppliers that feed into their production lines. Smaller parts manufacturers, lacking the procurement scale and leverage of Toyota or Nissan, face disproportionately severe exposure because they cannot secure priority allocation in a tightening market.

Koji Sato, chairman of the Japan Automobile Manufacturers Association, communicated at a March 2025 press conference that prolonged disruption would make challenges in material procurement unavoidable. He specifically referenced Japan's combined dependence on Middle Eastern aluminium and naphtha as the source of this structural vulnerability. Nissan and Honda are among the automakers most exposed to these compounding pressures.

The Specialised Alloy Problem: A Risk Hiding Inside the Broader Narrative

Why Alloy-Grade Sourcing Is Fundamentally Different from Commodity Procurement

The headline narrative around Japan carmakers aluminium supply risks in the Middle East tends to focus on aggregate tonnage and LME prices. This framing, while accurate, obscures a more acute and arguably more intractable problem: the shortage risk for specialised aluminium alloys used in high-performance automotive components, particularly cast and forged wheels.

Automotive aluminium alloys are defined by precise chemical compositions. Aluminium silicon alloys used in high-pressure die casting processes, and the 6061 and 6082 series alloys used in structural and wheel applications, require extremely tight control over elements including silicon, magnesium, copper, manganese, and chromium, with tolerances often measured in hundredths of a percent. This is categorically different from sourcing commodity-grade aluminium.

The consequence is what industry engineers describe as alloy stickiness: the cost and time required to requalify alternative suppliers for safety-critical automotive components is high enough that procurement teams cannot switch sources opportunistically, even when commodity-grade alternatives are available at competitive prices.

How the Russia-Ukraine Conflict Created the Current Alloy Dependency

The Middle East's emergence as a primary alloy supplier for Japanese automotive manufacturers was itself a response to a previous supply disruption. Before the Russia-Ukraine conflict disrupted trade flows, Russian producers, who account for more than 10% of global aluminium supply outside China according to US Geological Survey data, were significant suppliers of specialised alloy grades to Japanese manufacturers.

As those supply relationships became untenable, Japanese buyers substituted Gulf sources for Russian ones, deepening their dependency on Middle Eastern alloy producers. The current disruption therefore represents the second compounding shock to Japanese automotive alloy supply within a three-year window, arriving before the procurement diversification triggered by the first shock had been completed.

Nobuyuki Takagi, general manager of the light metals section at Marubeni, confirmed that risks of shortages exist for certain aluminium alloys, noting that the Middle East became a critical supply region partially due to the difficulties in sourcing from Russia. Takagi also clarified that a complete aluminium shortage in Japan is considered unlikely because Japanese firms hold equity stakes in overseas smelters in Australia and Canada, providing a partial supply buffer.

The critical distinction here is between commodity aluminium availability and alloy-grade availability. Japan may navigate the crisis without experiencing a broad supply crisis while still confronting targeted shortages in the specific alloy grades that automotive manufacturing requires. That scenario is arguably more dangerous from an operational standpoint because it is harder to communicate and harder for financial markets to price accurately.

Sector Vulnerability: Not All Japanese Aluminium Users Face Equal Risk

Why Automotive Exposure Exceeds the Beverage Sector Despite Lower Volume

| Sector | Aluminium Use Profile | Sourcing Flexibility | Disruption Vulnerability |

|---|---|---|---|

| Beverage and Packaging | High volume, commodity grade | Moderate | Lower |

| Automotive Manufacturing | Moderate volume, alloy-specific | Low | High |

| Construction | Moderate volume, standard grade | Moderate | Medium |

While Japan's beverage and packaging manufacturers consume the largest absolute volume of aluminium domestically, their commodity-grade requirements allow for a broader range of substitute supply sources. Automotive and construction manufacturers face more constrained alternatives due to their dependence on specialised materials and longer qualification timelines.

The vulnerability of smaller automotive parts manufacturers warrants particular attention. Unlike Toyota or Nissan, which have dedicated procurement teams and established relationships with multiple global smelters, smaller Tier 2 and Tier 3 suppliers often operate with thin margins and limited inventory buffers. In a market where physical tightness forces smelters to prioritise their largest customers, smaller buyers are systematically disadvantaged in securing allocation.

The next major ASX story will hit our subscribers first

Supply Recovery Timeline: What the Road to 2028 Actually Looks Like

A Multi-Year Process Governed by Industrial Physics

The recovery timeline for Middle Eastern aluminium capacity is not a function of commercial incentives or political will. It is governed by the technical constraints of the smelting process itself, establishing a sequence of steps that cannot be accelerated regardless of how urgently markets need the supply.

The required sequence runs as follows:

- Solidified aluminium must be fully removed from all affected smelter pots before any structural damage assessment can begin

- Damage assessment must be completed to determine the scope and cost of repairs required

- Procurement of replacement equipment and materials for damaged pot lining and superstructure must occur, often involving long lead times for specialised refractory materials

- Physical reconstruction and relining of damaged pots must be completed

- Controlled restart sequence must be executed, as premature restart of incompletely repaired pots risks further damage and extends the overall timeline

- Ramp-up to full production capacity occurs gradually, typically over several months after restart

Wood Mackenzie projects that this sequence means Middle Eastern smelter capacity will not return to full operational status until 2028, with Indonesia and India expected to begin contributing new capacity during the 2027 to 2028 transition window as partial offsets to regional losses.

The projected 1.8 million tonne additional supply loss in 2026 reflects the lag effect of this process: facilities that curtailed production in 2025 will continue to suppress output throughout the following year as the recovery sequence proceeds.

Price Normalisation Scenarios and Their Assumptions

BMI forecasts aluminium futures averaging USD 3,100 per tonne in 2025, declining to USD 2,931 per tonne by 2027 as new capacity gradually enters the market. This trajectory, however, rests on a key assumption: no further escalation in Strait of Hormuz disruptions beyond current projections.

Disclaimer: Price forecasts are inherently uncertain and subject to revision based on evolving geopolitical, macroeconomic, and operational factors. The figures cited here represent analyst projections at a specific point in time and should not be relied upon as definitive guidance for investment or procurement decisions.

If Hormuz disruptions intensify or extend beyond current projections, the normalisation timeline could be materially delayed. Japanese automakers with limited forward hedging positions face the greatest earnings risk under this scenario, as they would be exposed to spot procurement at elevated prices for an extended period. The backwardation structure currently observed in LME pricing will likely persist as long as physical tightness remains unresolved.

How Japanese Carmakers Are Responding

Strategic Adaptation Under Time Pressure

The 18-month supplier qualification timeline creates a defining urgency for Japanese automotive procurement teams. Diversification strategies initiated today will not yield meaningful flexibility until at least mid-2026, meaning the window for protecting supply chains during the acute phase of the current disruption has effectively already closed for manufacturers that had not begun the process before tensions escalated.

The strategic responses currently under consideration or in early implementation include:

- Evaluating increased offtake volumes from equity-held smelter assets in Australia and Canada, which provide a partial but not fully substitutable buffer against Gulf supply losses

- Accelerating supplier qualification processes for aluminium producers in regions less exposed to current geopolitical risk, including Southeast Asian facilities and expanded capacity in India

- Increasing utilisation of domestic recycled aluminium as a partial substitute for primary metal in applications where secondary aluminium meets specifications

- Negotiating longer-term supply agreements with non-Gulf producers to lock in volume commitments before competing buyers secure available capacity

- Exploring regional premium arbitrage opportunities, though these are constrained by the fact that European and US buyers are simultaneously competing for the same alternative supply cargoes

The Deeper Strategic Lesson

The current disruption is accelerating a strategic conversation within Japan's automotive sector that should have begun earlier. The Russia-Ukraine conflict had already demonstrated that geographic concentration in critical material supply chains represents a systematic risk, yet the adjustment period between that disruption and the current one proved insufficient for Japanese manufacturers to meaningfully diversify their alloy sourcing.

The structural implication is clear: procurement strategies optimised for cost efficiency during stable periods can create earnings vulnerabilities that dwarf the savings accumulated during normal market conditions. A 30% import concentration that delivered marginal cost advantages over a decade can generate billions of yen in earnings impacts over a single fiscal year when that concentration becomes a liability.

Long-term supply chain resilience will likely require a combination of increased equity participation in non-Gulf smelting assets, greater domestic recycled aluminium utilisation, and a willingness to accept modestly higher average procurement costs in exchange for reduced concentration risk. Examining how top aluminium producers are positioning themselves globally offers useful insight into where alternative supply capacity may emerge. Furthermore, understanding broader China metals market outlook dynamics is also relevant, as Chinese domestic consumption patterns will influence how much ex-China supply is available to redirect toward Japan. The aluminium tariffs impact from US trade policy adds yet another layer of complexity to an already strained global supply picture.

Frequently Asked Questions

Why is Japan more exposed to Middle East aluminium disruptions than other major importers?

Japan sources approximately 30% of its aluminium and alloy imports from the Gulf region, the highest proportional dependence among the world's five largest aluminium importers. Combined with the limited short-term switching flexibility created by the 18-month supplier qualification timeline, this concentration makes Japan structurally more vulnerable than competitors with more diversified supply bases.

Will Japanese automakers face actual aluminium shortages?

A complete aluminium shortage is considered unlikely given Japanese firms' equity stakes in overseas smelters. However, targeted shortages in specialised automotive alloy grades represent a credible near-term risk, particularly given the compounding effect of losing both Russian and Middle Eastern alloy supply within a three-year period.

How long will Middle Eastern aluminium supply disruptions last?

Wood Mackenzie projects that full capacity restoration for affected Gulf smelters will not occur before 2028. New capacity from Indonesian and Indian expansions is expected to begin partially offsetting losses during the 2027 to 2028 period.

What financial impact are Japanese automakers projecting?

Toyota has estimated a ¥670 billion earnings impact for the fiscal year ending March 2027, Mitsubishi Motors projects a ¥30 billion impact for the current fiscal year, and Nissan has flagged a ¥15 billion first-half impact. Combined, these projections exceed ¥715 billion across three manufacturers alone.

What is backwardation and why does it matter for aluminium buyers?

Backwardation occurs when spot prices for immediate delivery exceed futures prices, the inverse of the normal market structure. For aluminium buyers, it signals acute near-term physical scarcity, meaning procurement teams face elevated costs for immediate supply with limited relief from standard forward hedging strategies.

Key Takeaways

- Japan's 30% import dependence on Gulf aluminium makes it the most structurally exposed major importer to current disruptions, a vulnerability compounded by the 18-month supplier qualification timeline

- LME aluminium prices reached USD 3,759 per tonne in late May 2025, the highest since March 2022, while regional import premiums surged approximately 80% quarter-on-quarter to USD 350 to 353 per tonne

- Supply losses exceeding 3 million tonnes in 2025 and a further 1.8 million tonnes in 2026 will keep global markets tight well into the medium term, with full recovery not expected before 2028

- Japanese automakers face a combined projected earnings impact exceeding ¥715 billion across Toyota, Mitsubishi Motors, and Nissan alone

- The specialised alloy shortage risk for automotive applications is more acute than the headline commodity supply narrative suggests, representing a second-order vulnerability that aggregate import statistics do not capture

- The technical constraints of smelter restart, including the mandatory removal of solidified aluminium before damage assessment can begin, establish a hard floor on recovery timelines that commercial urgency cannot compress

- Full Middle Eastern capacity recovery is not expected before 2028, with alternative capacity from India and Indonesia beginning to materialise only during the 2027 to 2028 transition window

This article contains forward-looking statements and analyst forecasts that are subject to material uncertainty. Readers should conduct independent research and seek professional advice before making procurement, investment, or financial planning decisions based on any projections or scenarios described herein.

Want to Know Which ASX Miners Could Benefit From the Global Aluminium Supply Squeeze?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including those in aluminium and related commodities — so subscribers can act on actionable opportunities before the broader market catches on. Explore historic discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major find.