July 27, 2026

The Quiet Race Beneath the Ice: Why Critical Mineral Supremacy Is Being Decided in the Arctic

Long before the current wave of energy transition policy reshaped commodity markets, industrial nations learned a painful lesson: the countries that control the inputs to technology control the technology itself. Rare earth elements sit at the very foundation of that equation. They are not glamorous commodities traded on visible exchanges. They are embedded silently inside electric motors, radar arrays, semiconductor equipment, and precision-guided systems. For Japan, a nation that manufactures all of the above at scale while producing virtually none of the raw materials required, this structural dependency represents one of the most consequential economic vulnerabilities in its modern industrial history.

It is within this context that Japan's decision to send a formal Japan delegation to Greenland rare earth extraction deserves to be understood. This is not a speculative venture. It is a structured, government-coordinated mission that reflects years of strategic rethinking about where Japan sources the materials that underpin its economic future.

When big ASX news breaks, our subscribers know first

Why Japan's Rare Earth Dependency Is a National Security Issue

Japan imports approximately 99% of its required rare earth elements, with the overwhelming majority historically sourced from China. That statistic alone would be concerning for any industrial economy. For Japan, which operates one of the world's most rare earth-intensive manufacturing bases, it represents a genuine systemic risk.

The country's advanced industries consume an estimated 15,000 metric tons of rare earth elements annually, distributed across several strategically critical sectors:

- Electric vehicles and hybrid powertrains: Neodymium-iron-boron permanent magnets, containing roughly 29-32% neodymium by weight, are essential components in traction motors

- Defence and aerospace electronics: Samarium, europium, and gadolinium are embedded in night-vision systems, laser guidance equipment, and radar technologies, with military-grade applications requiring purity exceeding 99.999%

- Semiconductor manufacturing: High-purity yttrium and gadolinium oxides are required for advanced lithography and wafer processing, enabling sub-5nm semiconductor fabrication

- Industrial robotics and precision systems: High-temperature magnetic applications require dysprosium and terbium to maintain performance at operating temperatures between 150-200°C

Japan's automotive sector alone accounts for approximately 35% of the country's rare earth consumption, while electronics and industrial machinery represent another 40%. These figures are trending upward. Japan's EV strategy projects domestic electric vehicle production reaching 2 million units annually by 2030, which would increase the nation's neodymium requirements by roughly 45% compared to current levels.

The 2010 Senkaku Islands territorial dispute between Japan and China provided a brutal demonstration of what supply disruption looks like in practice. China's unofficial restriction of rare earth exports to Japan during that period caused neodymium oxide prices to surge by approximately 750%, sending shockwaves through Japanese manufacturers of hybrid vehicles and consumer electronics. That episode catalysed Japan's formal Critical Minerals Strategy and permanently altered the country's thinking about procurement. Understanding China's rare earth strategy helps contextualise why Japan is now pursuing Arctic alternatives so deliberately.

Japan's shift from just-in-time procurement toward strategic stockpiling and source diversification is not a policy preference. It is a response to demonstrated economic coercion that showed exactly how a single supplier can inflict severe industrial pain without firing a shot.

Current strategic reserves are estimated to cover approximately 90 days of average consumption, well short of the 180-day buffer that international energy security frameworks recommend. Closing that gap requires new sources, not just deeper stockpiles.

Greenland's Rare Earth Profile: What the Geology Actually Shows

Greenland's geological architecture makes it one of the most geologically compelling rare earth frontiers on the planet. The island's ancient Precambrian bedrock formations, combined with a series of highly unusual alkaline intrusive complexes, have created rare earth concentrations that are globally exceptional in both scale and composition.

Greenland is estimated to hold approximately 38.5 million metric tons of rare earth oxide equivalent resources within identified deposits, representing roughly 15-20% of global rare earth resources outside of China. The Ilímaussaq alkaline complex in southern Greenland is the centrepiece of this geological wealth. This zone hosts one of the most REE-rich peralkaline igneous bodies on Earth, containing unusual mineralogy including steenstrupine, sodalite, and lujavrite-hosted rare earth phases that concentrate both light and heavy rare earth elements.

The Kvanefjeld project, located within this complex, contains estimated resources of approximately 11.3 million metric tons of rare earth oxide, with heavy rare earth elements constituting roughly 14% of total rare earth content. That ratio matters enormously. Globally, heavy rare earth elements typically represent only 1-2% of rare earth resources. Greenland's skew toward HREE-rich mineralogy is what makes the deposits strategically disproportionate to their total volume. Furthermore, the broader Greenland critical minerals race is intensifying as multiple nations recognise this geological reality.

| REE Category | Key Elements | Primary Application | Greenland Relevance |

|---|---|---|---|

| Light REEs | Neodymium, Cerium, Lanthanum | EV motors, catalytic converters, glass | Abundant in most deposits |

| Heavy REEs | Dysprosium, Terbium, Yttrium | High-temp magnets, defence, phosphors | Disproportionately concentrated |

| Critical Transition REEs | Praseodymium, Samarium | Wind turbines, precision guidance | Present in identified zones |

A critical distinction that separates geological promise from commercial reality is the difference between total resource estimates and economically recoverable reserves. Greenland's extraction economics remain genuinely uncertain due to the following factors:

- Permafrost and Arctic logistics: Year-round operational access requires significant infrastructure investment in ports, roads, and processing facilities capable of functioning at extreme temperatures

- Ore processing complexity: Many of Greenland's REE minerals occur in association with uranium and thorium, creating radioactive byproduct management challenges that significantly complicate processing and licensing

- Environmental regulatory standards: Greenland's government has implemented increasingly stringent environmental standards, including a 2021 parliamentary vote to halt uranium mining that directly affected several REE projects in the Ilímaussaq region

- Community consent requirements: Inuit community consultation and benefit-sharing frameworks are mandatory components of any extractive development approval

Greenland's rare earth deposits are characterised by average grades of approximately 0.5-0.7% total rare earth oxides at Kvanefjeld, which compares reasonably well to many conventional deposits globally, though well below China's Bayan Obo benchmark mine which runs at approximately 5% REO. Grade alone does not determine viability; mineralogy, separability, and downstream processing infrastructure all factor heavily into feasibility assessments.

Who Is Going to Greenland and What Are They Looking For?

The Delegation's Institutional Composition

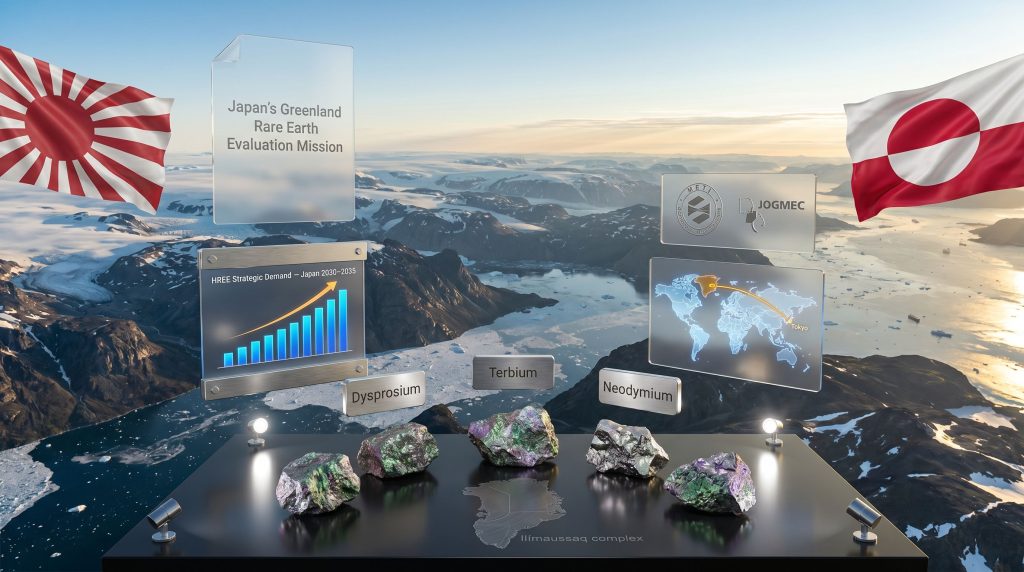

Japan is preparing to send a delegation to Greenland during the northern summer to evaluate possible rare earth extraction, according to reporting by Nikkei as cited by Reuters. The delegation's composition signals that this mission carries institutional weight well beyond a routine commercial scoping trip.

The three institutional pillars of the evaluation team are:

- Ministry of Economy, Trade and Industry (METI): Japan's central policy body for industrial and energy strategy. METI's direct participation confirms this is a government-sanctioned initiative with strategic policy dimensions, not merely a private sector exploratory exercise

- Japan Organization for Metals and Energy Security (JOGMEC): A government-affiliated independent administrative body with a specific mandate to secure stable supplies of metallic minerals, coal, oil, and natural gas for Japan. JOGMEC has a well-established track record of financing geological surveys, feasibility studies, and equity participation in overseas mineral projects in partnership with private Japanese companies

- Japanese trading companies (sōgō shōsha): Japan's general trading houses, including major operators such as Mitsubishi Corporation, Mitsui, and Sumitomo, function as the deal-structuring and relationship-building arms of Japan's resource diplomacy. Their role in this delegation likely involves assessing long-term offtake agreement viability and potential joint venture frameworks

The delegation is expected to hold talks with local Greenlandic government officials, the Naalakkersuisut, which governs natural resources under Greenland's home-rule arrangements. Understanding this governance layer is essential to interpreting the mission's scope.

What Stage Is Japan's Engagement At?

The following table clarifies where Japan's current visit sits within the progression of resource engagement:

| Engagement Stage | Purpose | Likely Outcome |

|---|---|---|

| Evaluation / Scoping Mission | Feasibility assessment, stakeholder mapping | No commitment; informs future investment decisions |

| Pre-Feasibility Partnership | Technical studies, resource estimation | Possible MOU or joint venture framework |

| Full Investment Commitment | Capital allocation, extraction agreements | Long-term supply contracts, equity stakes |

Japan's current delegation sits firmly in stage one. No extraction commitment exists, and no investment decision has been made. The outcome of this evaluation will determine whether Japan's engagement progresses to formal technical partnership or redirects capital toward its existing diversification targets in Australia, Canada, and Kazakhstan.

The Geopolitical Layer: Why the Whole World Is Watching Greenland

Greenland does not exist in a geopolitical vacuum. The Arctic island's enormous strategic value, encompassing rare earth resources, shipping lane access, military positioning, and scientific importance, has placed it at the intersection of major power competition in ways that directly affect any nation seeking to engage with its mineral wealth.

In January 2025, the White House indicated that U.S. President Donald Trump was actively considering how to acquire Greenland, a statement that generated significant diplomatic turbulence across NATO's European members. While those discussions have since transitioned to a formal diplomatic track rather than any direct acquisition scenario, the episode permanently elevated Greenland's profile from a regional Arctic policy matter to a globally watched geopolitical contest. In addition, the recent Greenland election and minerals debate has further shaped how the autonomous government approaches external resource interest.

For Japan, this creates a layered diplomatic environment. Japan maintains a close strategic alliance with the United States, which in theory could provide goodwill when engaging in Greenlandic resource discussions. However, Greenland's autonomous government under the Naalakkersuisut ultimately controls resource access decisions, operating within the foreign policy framework of the Kingdom of Denmark. Any resource agreement requires navigating both Greenlandic home-rule institutions and Danish diplomatic considerations, a complexity that favours patient, relationship-oriented actors over those seeking rapid commercial outcomes.

Greenland is not simply Denmark's Arctic territory to negotiate on behalf of. Its autonomous government exercises substantial control over resource licensing, environmental approvals, and community consultation requirements. This jurisdictional layering adds significant process time to any resource development pathway.

The competitive landscape for Greenland's resources includes multiple major economies pursuing different strategic angles:

| Actor | Approach | Strategic Priority |

|---|---|---|

| United States | Direct political interest, infrastructure investment discussions | Military positioning, REE supply security |

| European Union | Bilateral partnerships, critical raw materials frameworks | Regulatory alignment, supply diversification |

| China | Historical commercial engagement, infrastructure investment | Maintaining REE market dominance |

| Japan | Institution-led evaluation, relationship-driven diplomacy | HREE supply security for manufacturing |

| South Korea | Commercial exploration partnerships | Technology sector mineral security |

Japan's non-confrontational, institution-led approach contrasts with more assertive geopolitical positioning from other actors. This methodology has historically proven effective in resource-sensitive jurisdictions where community trust and regulatory compliance are valued alongside commercial terms.

The Processing Bottleneck: Why Mining Is Only Half the Problem

One of the most underappreciated dimensions of global rare earth supply chains is that extraction and refining are entirely separate industrial challenges. China's dominance in rare earth supply is not primarily based on having the most resources. It is based on controlling approximately 90% of global rare earth separation and refining capacity, a position built over decades of deliberate industrial investment.

Even if Greenland's rare earth deposits were economically excavated, the resulting ore concentrate would need to be separated into individual rare earth oxides before it could be used by manufacturers. That separation process involves complex hydrometallurgical techniques, solvent extraction cascades, and precipitation chemistry that require highly specialised infrastructure. Building commercial-scale separation facilities typically takes 5-8 years and hundreds of millions of dollars of capital investment.

Japan recognises this bottleneck explicitly. JOGMEC's investment philosophy includes not just geological acquisition but downstream processing capability development. Japan's existing partnership with Lynas Corporation, which processes rare earth concentrates from Mount Weld in Australia through facilities in Malaysia, represents a model for the kind of vertically integrated supply chain Japan seeks to replicate with any Greenland engagement.

Japan has also invested in domestic recycling infrastructure capable of recovering rare earth elements from approximately 3.5 million tons of end-of-life hard disk drives annually. Toyota has independently reduced its dysprosium requirements for electric vehicle motors by approximately 50% through advanced grain boundary diffusion techniques, demonstrating that demand-side substitution can complement supply-side diversification. However, recycling and substitution currently address only a small fraction of Japan's total rare earth consumption. Consequently, the broader rare earth supply chain buildout across allied nations remains a critical policy priority.

The next major ASX story will hit our subscribers first

Three Scenarios for How Japan's Greenland Engagement Could Unfold

Given the early-stage nature of the evaluation mission, the trajectory of Japan's Greenland engagement remains genuinely open. Three structurally distinct outcomes are plausible based on Japan's historical resource diplomacy patterns and Greenland's regulatory environment.

Scenario A: Evaluation Without Progression

The delegation assesses that extraction economics, environmental regulatory barriers, or unfavourable political conditions make Greenland's deposits commercially non-viable within an acceptable risk threshold. Japan redirects capital toward existing partnerships in Australia, Canada, and Kazakhstan, where regulatory environments are more established and processing infrastructure is already partially developed.

Scenario B: Phased Partnership Development

A positive evaluation result leads to JOGMEC-backed feasibility studies conducted in partnership with Greenlandic entities, potentially structured as a joint research agreement or technical cooperation memorandum. This pathway would unfold over a multi-year timeline, potentially resulting in a formal joint venture or long-term offtake agreement, contingent on environmental approvals and community consent processes.

Scenario C: Strategic Anchor Investment

Japan secures a long-term rare earth supply agreement as part of a broader Arctic resource diplomacy framework, positioning Greenland as a cornerstone supply source for heavy rare earth elements specifically. This outcome would require sustained political engagement, substantial infrastructure co-investment, and successful navigation of Greenland's autonomous governance requirements.

Given Japan's historically methodical approach to resource diplomacy, which consistently prioritises long-term relationship building over rapid deal-making, Scenario B represents the most structurally probable outcome if the evaluation visit produces positive initial findings. Scenario C remains a medium-to-long-term aspiration rather than a near-term commercial goal.

What Greenland's Development Could Mean for Global REE Markets

If Greenland were to emerge as a meaningful rare earth producer over the next decade, the implications for global REE markets would be significant, particularly for heavy rare earth elements where supply concentration risk is most acute.

Dysprosium and terbium, the two most strategically sensitive heavy rare earth elements, are currently sourced almost exclusively from China's ionic clay deposits in Jiangxi and Fujian provinces. These deposits are associated with significant environmental degradation and face increasingly strict domestic regulation in China, raising legitimate long-term questions about their production sustainability. A Greenlandic HREE source would represent genuine supply diversification for these elements, not merely an incremental addition to existing light REE supply.

The timeline reality, however, demands measured expectations. Even optimistic development scenarios place meaningful large-scale REE production from Greenland no earlier than the mid-2030s. The multi-stage pathway from positive evaluation through feasibility study, environmental assessment, permitting, infrastructure construction, and operational ramp-up typically spans 10-15 years for projects of this geological and logistical complexity in Arctic environments.

Japan's strategic interest, if it progresses beyond evaluation, would position it as an early-mover in establishing the commercial and diplomatic frameworks that govern Greenland's eventual REE production. Early-mover advantage in resource diplomacy is not merely commercial; it shapes the terms of access, the structure of revenue-sharing arrangements, and the long-term supply agreements that could define Japan's REE security architecture well into the 2040s. Analysts tracking the mission note that Japan's timing is deliberate, arriving early in Greenland's resource development cycle rather than competing in a crowded later-stage field.

Frequently Asked Questions

What Is the Purpose of Japan's Delegation to Greenland?

Japan is sending a multi-institutional team, including METI officials, trading companies, and JOGMEC, to conduct a ground-level evaluation of Greenland's rare earth extraction potential. This is an assessment mission focused on feasibility and stakeholder engagement, not an extraction or investment commitment.

Why Does Japan Need to Secure Rare Earth Supplies From Greenland Specifically?

Japan imports approximately 99% of its rare earth elements and has been actively diversifying its source nations since China's 2010 export restrictions. Greenland's deposits are particularly interesting because they are disproportionately rich in heavy rare earth elements, which are Japan's highest-priority supply vulnerability given their critical role in electric vehicle motors and defence systems.

What Makes Greenland's Rare Earth Deposits Geologically Distinctive?

Greenland's Ilímaussaq alkaline complex hosts rare earth concentrations with unusually high proportions of heavy REEs, which typically represent only 1-2% of global rare earth resources but account for roughly 14% of Greenland's identified deposit content. This heavy REE skew is what elevates Greenland's strategic relevance beyond its total resource volume.

How Does U.S. Interest in Greenland Affect Japan's Resource Diplomacy There?

The U.S. government's expressed interest in Greenland's strategic value has elevated the territory's geopolitical profile globally. Japan's close alliance with the U.S. may create diplomatic goodwill, but Greenland's autonomous government ultimately controls resource access decisions through its home-rule institutions, independent of both Danish and American influence.

When Could Greenland Realistically Produce Rare Earths at Scale?

Even under optimistic development pathways, large-scale REE production from Greenland is unlikely before the mid-2030s. The sequential requirements of environmental assessment, community consultation, permitting, infrastructure development, and operational ramp-up in an Arctic environment mean that Japan's current evaluation mission represents the beginning of a decade-long process rather than a near-term supply solution.

What Is JOGMEC's Role in Japan's Resource Diplomacy?

JOGMEC is Japan's government-affiliated body mandated to secure stable mineral and energy supplies for the nation. It provides financing for overseas geological surveys, feasibility studies, and risk capital for equity participation in projects alongside private Japanese companies, functioning as the institutional backbone of Japan's resource diversification strategy.

Key Takeaways

- Japan's Japan delegation to Greenland rare earth extraction represents a government-coordinated, institution-led assessment mission involving METI, JOGMEC, and major trading companies, confirming this is a strategic initiative rather than a purely commercial exploration exercise

- Greenland's deposits are geologically distinctive for their disproportionate heavy rare earth content, directly addressing Japan's most acute supply chain vulnerabilities in electric vehicles, defence electronics, and high-temperature magnetic applications

- The mission occurs within a highly contested geopolitical environment, with the United States, European Union, China, and South Korea all pursuing varying levels of engagement with Greenland's strategic resource base

- Japan's approach, methodical, patient, and relationship-driven, reflects its established model of resource diplomacy that prioritises long-term supply security over short-term commercial speed

- No mining commitment exists; the evaluation outcome will determine whether Japan escalates its engagement toward feasibility studies and potential joint ventures, or redirects capital toward existing diversification partnerships in Australia and Canada

- The processing bottleneck is as strategically important as the extraction question; securing ore access without refining capability does not resolve Japan's supply chain vulnerability

- For global REE markets, Japan securing early-mover positioning in Greenland could have long-term implications for heavy rare earth element pricing and supply concentration, particularly if Greenland emerges as a meaningful HREE producer in the 2030s

This article is intended for informational purposes only and does not constitute financial or investment advice. Statements regarding future timelines, resource estimates, market projections, and geopolitical scenarios involve inherent uncertainty and should not be relied upon as predictions of specific outcomes. Readers should conduct independent research and consult qualified advisors before making investment decisions.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including critical minerals like rare earths that are reshaping global supply chains — so subscribers can identify actionable opportunities before the broader market reacts. Explore Discovery Alert's discoveries page to see the historic returns that major ASX mineral discoveries have generated, and begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.