July 15, 2026

Japan's rare earth strategy faces an increasingly complex challenge in securing critical mineral supplies as global supply chains become more concentrated. The semiconductor manufacturing, renewable energy, and automotive sectors rely heavily on rare earth elements, yet most production and processing capacity remains concentrated in single geographic regions. This concentration creates systemic vulnerabilities that require strategic responses beyond traditional market mechanisms.

Japan's approach to this challenge offers valuable insights for resource-constrained nations seeking to build resilience without attempting direct competition with established mineral processing powers. Furthermore, through technological innovation, strategic partnerships, and circular economy principles, Japan has developed a multi-faceted strategy that prioritizes adaptability over self-sufficiency.

Understanding Japan's Critical Minerals Vulnerability

Japan's geographic constraints fundamentally shape its approach to critical mineral security. As an island nation with limited domestic mineral resources, Japan must import virtually all rare earth elements required for its advanced manufacturing sectors. The 2010 export restrictions imposed by China exposed the depth of this vulnerability when rare earth prices spiked dramatically and supply chains faced severe disruptions.

Manufacturing Sector Exposure:

• Electronics production requiring high-purity rare earth oxides for display technologies

• Automotive manufacturing dependent on permanent magnets for electric vehicle motors

• Renewable energy infrastructure utilizing rare earth-based wind turbine generators

• Defense systems incorporating rare earth elements in precision guidance systems

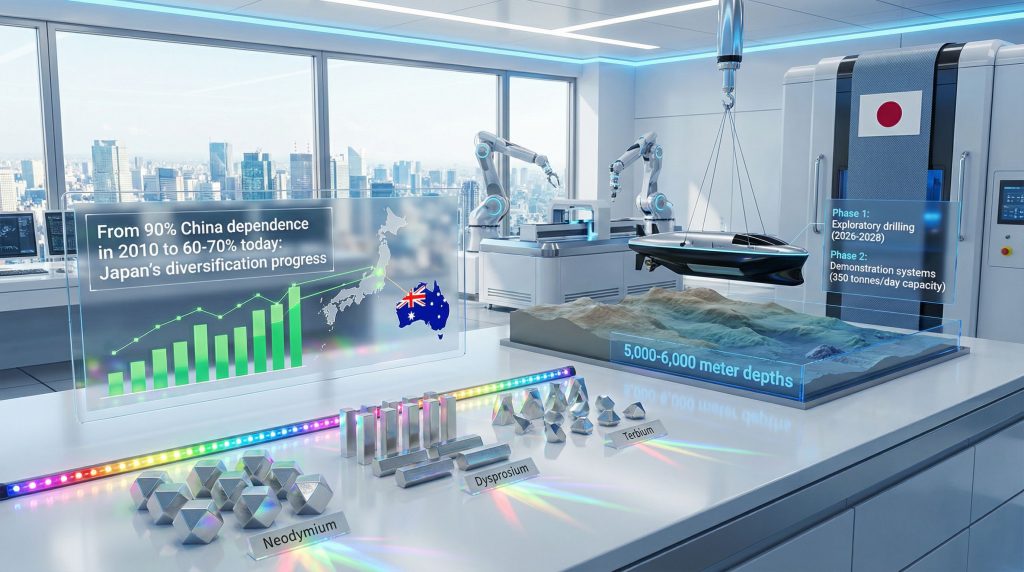

The 2010 crisis demonstrated that Japan's dependence extended beyond simple material availability to encompass processing capabilities, quality standards, and delivery reliability. According to research by Wang from the National Institute for Environmental Studies, Japan reduced its reliance on Chinese sources from approximately 90% in 2010 to 60-70% currently through systematic diversification efforts.

This reduction represents significant progress, yet highlights the persistent challenges facing resource-dependent economies. The remaining dependence reflects both the technical complexity of rare earth processing and the economic realities of competing with established, integrated supply chains.

Economic Impact Assessment:

| Sector | Rare Earth Dependency | Production Value at Risk |

|---|---|---|

| Electronics | High purity oxides | $180-220 billion annually |

| Automotive | Permanent magnets | $95-120 billion annually |

| Renewable Energy | Generator magnets | $45-60 billion annually |

| Defense Systems | Precision components | $15-25 billion annually |

The vulnerability extends beyond immediate supply disruptions to encompass technological competitiveness and industrial capacity. Japanese manufacturers discovered that securing alternative suppliers required substantial investments in quality assurance, logistics infrastructure, and supplier development programs.

When big ASX news breaks, our subscribers know first

What Makes China's Rare Earth Processing Dominance So Persistent?

The Processing Bottleneck Reality

China's control over global rare earth supply chains extends far beyond mining operations to encompass the more critical processing and refining stages. While China controls approximately 70% of rare earth mining, its dominance reaches 85-90% of refining capacity globally, according to recent analysis from the International Energy Agency.

This processing concentration creates a more significant strategic vulnerability than mining dependence alone. Rare earth elements occur together in mineral deposits and require complex separation processes to isolate individual elements to commercial purity levels. The technical expertise required for these operations developed over decades through accumulated experience, proprietary process improvements, and integrated supply chain optimization.

Technical Complexity Barriers:

• Separation chemistry: Achieving 99.99% purity levels requires sophisticated solvent extraction processes

• Sequential processing: Each rare earth element requires different chemical conditions for optimal separation

• Environmental management: Handling acidic waste streams and radioactive thorium byproducts

• Quality consistency: Maintaining specification compliance across large-scale industrial operations

Establishing competitive rare earth separation facilities requires substantial capital investments, with industry estimates suggesting $300-500 million minimum for commercially viable processing capacity. These costs reflect not only equipment and infrastructure requirements but also the extended development timelines needed to achieve operational efficiency and quality standards.

Environmental regulatory frameworks in developed economies add additional complexity and cost to rare earth processing operations. While these standards provide important environmental protections, they also create competitive disadvantages compared to facilities operating under less stringent regulatory oversight.

Beyond Mining: Why Downstream Control Matters Most

The value distribution across rare earth supply chains reveals why processing control provides more strategic leverage than mining operations. Processing and refining activities command 50-60% of total supply chain value, while mining operations typically capture only 10-15% of the final product value.

Rare Earth Value Chain Analysis:

| Supply Chain Stage | Value Capture % | Strategic Importance | Barrier to Entry |

|---|---|---|---|

| Mining Operations | 10-15% | Medium | Low-Medium |

| Processing/Refining | 50-60% | Very High | Very High |

| Magnet Manufacturing | 20-30% | High | Medium-High |

| End Product Integration | 10-15% | Medium | Low |

Integrated Chinese operations benefit from vertical coordination that reduces supply chain cycle times by 30-40% compared to non-integrated competitors. This integration enables quality control from ore processing through finished magnet production, proprietary process improvements, and optimized inventory management across multiple production stages.

The time-to-market advantages of integrated operations become particularly significant during periods of strong demand growth or supply disruptions. Companies with processing capabilities can respond more rapidly to specification changes, delivery requirements, and quality issues compared to those dependent on external processing services.

China's processing dominance reflects not superior geology but accumulated expertise in complex separation chemistry, integrated supply chains, and decades of operational experience that cannot be rapidly replicated.

This reality shapes strategic responses for consuming countries, as new mining projects without corresponding processing capacity provide limited supply security benefits. However, diversification efforts must therefore address processing capabilities rather than focusing solely on mining operations.

Japan's Multi-Vector Response Strategy: Technology Over Scale

Diversification Through Strategic Partnerships

Japan's response to rare earth vulnerability emphasizes strategic partnerships and equity investments rather than attempting to develop domestic production capacity. This approach recognises the economic realities of competing with established, scale-advantaged operations while building meaningful supply chain alternatives.

Australian mining partnerships represent the cornerstone of Japan's diversification strategy. Lynas Rare Earths, operating the Mount Weld mine in Western Australia, has become a critical supplier through long-term offtake agreements and Japanese equity participation. Mount Weld contains some of the world's highest-grade rare earth deposits, providing both economic viability and strategic supply security.

Key Partnership Benefits:

• Geographic diversification: Reducing concentration risk through supplier dispersion

• Contract security: Multi-year agreements with predetermined pricing mechanisms

• Quality assurance: Established specifications and delivery reliability

• Strategic alignment: Shared interests in supply chain stability and development

Japanese trading companies and manufacturers have secured equity stakes and long-term supply agreements extending 5-15 years with volume commitments aligned to projected demand growth. These arrangements include force majeure protections, price adjustment mechanisms, and capacity expansion provisions to accommodate future requirements.

From 90% China dependence in 2010 to 60-70% today: Japan's diversification progress demonstrates the potential for systematic supply chain restructuring through strategic partnerships and technological innovation.

Vietnam represents another emerging partnership opportunity for rare earth processing development. Japanese companies have invested in processing infrastructure that leverages Vietnam's industrial capabilities while providing alternative processing capacity outside China's direct control. Japan's rare earth dependency strategy reflects broader trends toward supply chain diversification across advanced economies.

The diversification strategy extends beyond bilateral relationships to encompass multilateral frameworks with the United States, Australia, and other allied nations. These frameworks facilitate coordinated investment, shared technology development, and joint responses to supply disruptions.

Innovation-Driven Efficiency Gains

Japan's technological approach focuses on reducing rare earth consumption per unit of performance rather than competing directly on production volume. This strategy leverages Japan's advanced manufacturing capabilities and research infrastructure to develop more efficient utilisation of available materials.

Advanced Magnet Technology Development:

Japanese manufacturers including Hitachi, TDK, Daido Steel, and Shin-Etsu have developed permanent magnet technologies that reduce heavy rare earth element content by 15-30% compared to earlier generation designs. These improvements target dysprosium and terbium, among the scarcest and most strategically vulnerable rare earth elements.

Technical innovations include:

• Grain boundary diffusion: Optimised crystal structures improving magnetic performance

• Intergranular phase engineering: Enhanced efficiency through controlled microstructure

• Precision separation techniques: Improved processing yields and reduced waste

Urban Mining and Recycling Infrastructure:

Japan has developed sophisticated rare earth recovery systems achieving 85-95% recovery rates from end-of-life magnets and electronic equipment. This urban mining infrastructure provides domestic supply sources while reducing environmental impact compared to primary processing operations.

The recycling approach offers several strategic advantages:

• Domestic supply generation: Reducing dependence on imported materials

• Environmental benefits: Lower energy consumption and waste generation

• Economic viability: Competitive costs when magnet scrap prices exceed primary processing expenses

• Supply chain control: Direct management of processing and quality standards

Japanese rare earth recycling prevents approximately 3,000-5,000 tonnes of annual material disposal while generating usable rare earth oxides for domestic manufacturing. The automotive and electronics industries provide consistent feedstock supply through structured collection and processing programs.

Precision separation technique improvements have enhanced both primary and secondary processing efficiency. Japanese companies have achieved significant yield improvements through process optimisation, quality control systems, and environmental management innovations that exceed international standards.

Deep-Sea Mining: Japan's Long-Term Insurance Policy

Minamitorishima Project Technical Assessment

Japan's exploration of deep-sea rare earth mining near Minamitorishima Island represents a long-term strategic option rather than an immediate supply solution. The deposits, located at depths of 5,000-6,000 meters, contain exceptional concentrations of rare earth elements, particularly heavy rare earths critical for advanced magnet applications.

Project Development Timeline:

| Phase | Duration | Capacity Target | Key Objectives |

|---|---|---|---|

| Phase 1: Exploratory | 2026-2028 | N/A | Geological assessment, technical feasibility |

| Phase 2: Demonstration | 2029-2032 | 350 tonnes/day | Process validation, environmental impact |

| Phase 3: Commercial Assessment | 2033-2035 | TBD | Economic viability, scale-up planning |

The geological potential is substantial, with rare earth-rich mud deposits containing concentrations that could theoretically supply decades of Japan's heavy rare earth requirements. However, the technical challenges are equally significant, requiring specialised equipment, environmental management systems, and operational capabilities that remain largely unproven at commercial scale.

Technical and Environmental Challenges:

• Operating depth: Extreme conditions requiring specialised equipment and engineering solutions

• Sediment processing: Concentration and separation of rare earths from marine sediments

• Environmental impact: Deep-sea ecosystem effects requiring comprehensive monitoring

• Cost competitiveness: Economic viability compared to land-based processing alternatives

Economic and Environmental Considerations

Deep-sea mining economics remain highly uncertain, with cost estimates varying significantly based on technology assumptions, scale projections, and environmental compliance requirements. The substantial capital investments required for equipment development, environmental management, and processing infrastructure create significant financial risks that may limit commercial viability.

Environmental considerations include potential impacts on deep-sea ecosystems that are poorly understood and difficult to monitor. Additionally, growing deep-sea mining concerns about environmental protection require careful regulatory frameworks for international authorities developing standards for environmental protection, impact assessment, and operational oversight.

Deep-sea mining should be viewed as a long-term strategic buffer rather than a near-term replacement for Chinese supply, with commercial viability remaining uncertain through the mid-2030s.

Even under optimistic scenarios, deep-sea rare earth production would likely meet only 1-5% of Japan's demand by the mid-2030s. The strategic value lies in providing insurance against future supply disruptions rather than achieving supply independence through domestic production.

The project represents Japan's commitment to exploring all potential supply options while acknowledging the technical, economic, and environmental uncertainties involved. This approach reflects the broader strategic philosophy of building resilience through diversified options rather than relying on single solutions.

The Japan-US Alliance Framework: Coordinated Critical Minerals Strategy

Bilateral Cooperation Mechanisms

The Japan-US alliance has evolved to encompass critical mineral security through coordinated investment, technology sharing, and supply chain development initiatives. This cooperation recognises that neither country can achieve supply chain resilience independently given the scale and complexity of global rare earth markets.

Joint Investment Strategies:

• Public-private partnerships: Risk-sharing mechanisms for strategic projects

• Coordinated financing: Multilateral funding for processing capacity development

• Technology transfer: Shared research and development initiatives

• Emergency protocols: Coordinated responses to supply disruptions

The alliance framework facilitates investment mobilisation through transparent pricing mechanisms, rapid permitting processes for strategic projects, and coordinated stockpiling programs. These mechanisms help private investors manage political and commercial risks while supporting supply chain development objectives.

Bilateral cooperation extends to standards development, quality assurance frameworks, and environmental governance systems that provide competitive advantages over less regulated alternatives. This approach leverages shared values and regulatory frameworks to create supply chain differentiation beyond simple cost competition.

Investment Mobilisation Strategies

Japan and the United States have developed coordinated approaches to mobilise private investment in rare earth processing capacity through risk mitigation, policy support, and market development initiatives. These strategies recognise that government funding alone cannot provide sufficient capital for large-scale supply chain transformation.

Policy Support Mechanisms:

• Investment guarantees: Government backing for strategic projects

• Tax incentives: Accelerated depreciation and development credits

• Regulatory streamlining: Expedited permitting for approved initiatives

• Market access: Coordinated procurement from allied suppliers

The framework emphasises technology leadership in processing efficiency, environmental performance, and quality standards rather than direct cost competition. This approach builds on existing technological capabilities while creating sustainable competitive advantages in global markets.

Joint financing structures combine government investment with private capital to reduce individual project risks while maintaining commercial discipline. These hybrid approaches enable larger-scale projects that might otherwise face prohibitive risk profiles for private investors alone.

Global Implications: Lessons for Resource-Poor Industrial Economies

The Resilience-Over-Self-Sufficiency Model

Japan's experience demonstrates that complete independence from global supply chains remains economically unfeasible for most critical minerals. Instead, resilience strategies that combine diversification, technological innovation, and strategic partnerships provide more practical approaches to supply security. The critical minerals energy transition requires coordinated approaches across multiple economies.

The resilience model offers several advantages over self-sufficiency approaches:

• Economic efficiency: Leveraging comparative advantages rather than replicating all capabilities

• Risk distribution: Spreading vulnerability across multiple suppliers and technologies

• Innovation incentives: Driving efficiency improvements through competitive pressure

• Alliance coordination: Building collective capability through shared investments

Competitive Advantages in Standards and Governance:

Resource-poor economies can compete effectively through superior environmental standards, quality assurance systems, and supply chain transparency rather than attempting to match established producers on cost alone. These governance advantages become increasingly valuable as end-users prioritise sustainability and reliability alongside price considerations.

Alliance-Based Supply Chain Architecture

Moving beyond bilateral dependencies toward multilateral frameworks provides enhanced resilience through diversified partnerships, shared technology development, and coordinated crisis response capabilities. This approach distributes risks while maintaining access to global markets and innovation.

Key Framework Components:

• Technology sharing: Joint research and development initiatives

• Coordinated investment: Multilateral funding for strategic projects

• Emergency protocols: Shared stockpiles and crisis response mechanisms

• Standards harmonisation: Compatible quality and environmental requirements

Alliance-based architectures enable smaller economies to participate in large-scale supply chain development while maintaining independence and flexibility. This approach provides alternatives to both complete dependence and prohibitively expensive self-sufficiency strategies.

The European Union and South Korea represent potential candidates for adapting Japan's approach through regional cooperation, technological innovation, and strategic partnerships. Moreover, the European CRM facility development reflects similar strategic thinking about supply chain diversification. These economies face similar vulnerabilities while possessing complementary capabilities that could support coordinated responses.

The next major ASX story will hit our subscribers first

Market Dynamics and Investment Implications

Sector Transformation Indicators

The global rare earth sector is experiencing gradual transformation as consuming countries implement diversification strategies and new processing capacity comes online outside China. However, this transformation will likely extend through the 2030s given the technical complexity and capital requirements involved.

Rare Earth Processing Capacity Projections 2025-2035:

| Scenario | Chinese Market Share 2025 | Chinese Market Share 2035 | Non-Chinese Capacity Growth |

|---|---|---|---|

| Conservative | 85-90% | 75-80% | Limited progress |

| Central | 85-90% | 65-70% | Moderate expansion |

| Ambitious | 85-90% | 50-55% | Substantial diversification |

Investment requirements for meaningful diversification range from $15-25 billion globally across all processing stages. These investments must overcome significant barriers including technical expertise development, environmental compliance, and competition from established integrated operations.

Strategic Metals Investment Themes

Investment opportunities arising from supply chain diversification efforts include companies developing non-Chinese processing capacity, technologies improving separation efficiency and recycling capabilities, and infrastructure supporting alternative supply chains.

Key Investment Categories:

• Processing technology: Advanced separation and purification systems

• Recycling infrastructure: Urban mining and circular economy solutions

• Alternative suppliers: Mining and processing operations outside China

• Efficiency technologies: Magnet design reducing rare earth consumption

Technology leaders in separation and recycling may benefit from increasing demand for alternative processing capabilities. Consequently, companies with expertise in high-purity processing, environmental management, and quality assurance systems are particularly well-positioned as diversification efforts accelerate.

Infrastructure developers for alternative processing hubs face both significant opportunities and substantial risks. Success will likely depend on access to capital, technical expertise, regulatory support, and long-term off-take agreements with major consumers.

What Are the Key Risks to Japan's Rare Earth Strategy?

Economic Viability Challenges

Japan's rare earth strategy faces persistent economic challenges as non-Chinese alternatives typically command premium pricing compared to Chinese sources. These premiums reflect higher processing costs, smaller scale operations, and additional quality assurance requirements that may limit adoption without policy support.

Cost Structure Analysis:

• Premium pricing: Non-Chinese suppliers often charge 15-30% higher prices

• Scale disadvantages: Smaller operations face higher per-unit costs

• Quality assurance: Additional testing and certification requirements

• Logistics complexity: Multiple suppliers increase coordination costs

Industrial resistance to premium pricing remains significant without policy mechanisms supporting diversification costs. Japanese manufacturers must balance supply security objectives against competitive pressures from global markets where cost optimisation drives procurement decisions.

Scale disadvantages in global cost competition may persist as Chinese integrated operations maintain efficiency advantages through vertical coordination, established expertise, and favourable regulatory environments. These structural advantages are difficult to overcome through policy support alone.

Geopolitical Response Scenarios

Japan's diversification efforts may trigger responsive measures from China including processing restrictions, technology transfer limitations, or preferential pricing for non-diversifying customers. These responses could accelerate diversification incentives while increasing transition costs for Japanese manufacturers.

Potential Response Mechanisms:

• Processing quota adjustments: Limiting exports to countries developing alternatives

• Technology restrictions: Preventing access to advanced processing equipment

• Pricing discrimination: Preferential terms for committed customers

• Investment limitations: Restricting Chinese participation in alternative projects

Alliance coordination difficulties during supply crises represent another significant risk factor. Coordinating responses across multiple countries with different economic interests, political systems, and industrial priorities may prove challenging during actual crisis conditions.

Furthermore, growing competitive dynamics in rare earth markets add complexity to Japan's strategic positioning as other nations develop alternative supply chains.

Technology transfer limitations and intellectual property concerns could slow development of alternative processing capabilities. Chinese companies possess decades of accumulated expertise in rare earth processing that may be difficult to replicate without technology sharing arrangements.

Future Outlook: Scenario Planning for 2030-2035

Conservative Scenario Analysis

Under conservative assumptions, Japan's rare earth strategy achieves limited success due to economic, technical, and geopolitical constraints. Chinese processing capacity continues expanding while alternative suppliers struggle with cost competitiveness and scale development.

Conservative Scenario Characteristics:

• Limited processing diversification: China maintains 75-80% market share

• Continued high dependence: Japan reduces Chinese reliance only modestly to 50-60%

• Modest recycling progress: Urban mining achieves 5-10% of consumption

• Deep-sea mining delays: Commercial viability remains uncertain beyond 2035

In this scenario, Japan maintains vulnerability to supply disruptions while paying premium prices for alternative suppliers. Economic competitiveness pressures may force renewed dependence on Chinese sources during cost-sensitive periods.

Ambitious Transformation Scenario

An ambitious scenario envisions successful implementation of Japan's rare earth strategy through breakthrough recycling technologies, commercial deep-sea mining, and effective alliance coordination reducing systemic supply risks. Regional initiatives such as the NSW critical minerals program could support alternative supply chain development.

Ambitious Scenario Elements:

• Breakthrough technologies: 90%+ recycling rates and reduced material intensity

• Successful deep-sea mining: Commercial operations providing 10-15% of demand

• Effective alliance coordination: Coordinated investment achieving scale economies

• Chinese market share reduction: Processing dependence below 50%

This scenario requires sustained government support, successful technology development, and coordinated international investment exceeding current commitment levels. Success would provide Japan with genuine supply security while maintaining access to competitive global markets.

The transformation timeline extends through 2030-2035 even under optimistic assumptions, reflecting the technical complexity and capital intensity of rare earth processing operations. Intermediate milestones include demonstration of recycling technologies, deep-sea mining feasibility, and alternative processing capacity development. Implementing a comprehensive critical minerals strategy remains essential for achieving these ambitious objectives.

FAQ Section

How much has Japan reduced its rare earth dependence on China since 2010?

Japan decreased its reliance from approximately 90% in 2010 to 60-70% currently through strategic diversification initiatives, Australian supplier partnerships, technological innovation in magnet design, and expanded recycling infrastructure development.

When will Japan's deep-sea rare earth mining become commercially viable?

Commercial viability assessment is expected by the early 2030s following exploratory phases beginning in 2026 and demonstration systems testing through 2032. Economic competitiveness remains uncertain due to technical complexity and environmental compliance requirements.

What makes rare earth processing more challenging than mining?

Processing requires sophisticated separation technologies achieving 99.99% purity levels, significant capital investment of $300-500 million minimum, environmental management of acidic waste streams and radioactive byproducts, and decades of operational experience for efficiency optimisation.

How does Japan's strategy differ from US and European approaches?

Japan emphasises technological innovation and efficiency improvements over production scale competition, focusing on reducing material intensity through advanced magnet design, recycling infrastructure, and strategic partnerships rather than competing directly on processing volume with Chinese integrated operations.

Looking for the Next Big Mining Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 30-day free trial today to position yourself ahead of the market.