August 6, 2026

Japan to boost recycled materials supply through a comprehensive ¥1 trillion investment programme that aims to transform the nation's approach to resource security and economic independence. This ambitious initiative addresses critical vulnerabilities in Japan's industrial foundation while positioning the country as a leader in advanced circular economy development. Furthermore, the programme represents one of the most significant infrastructure transformations occurring across developed economies today, as nations confront intensifying resource scarcity and supply chain vulnerabilities.

Understanding Japan's Strategic Resource Security Framework

Japan's comprehensive circular economy transformation addresses fundamental weaknesses in its industrial foundation through targeted investment in domestic recycling infrastructure. The nation's overwhelming dependence on imported materials creates cascading vulnerabilities that extend across its entire manufacturing base, from automotive production to electronics assembly.

Critical Resource Dependencies

Japan imports more than 90 percent of its essential minerals, creating exposure to supply disruptions that can paralyse key industrial sectors. This dependency intensifies during geopolitical tensions when export restrictions from supplier nations threaten manufacturing continuity. Recent tightening of Chinese export controls on critical minerals while simultaneously strengthening domestic recycling capabilities has created asymmetric competitive pressures that Japan must address through strategic infrastructure development.

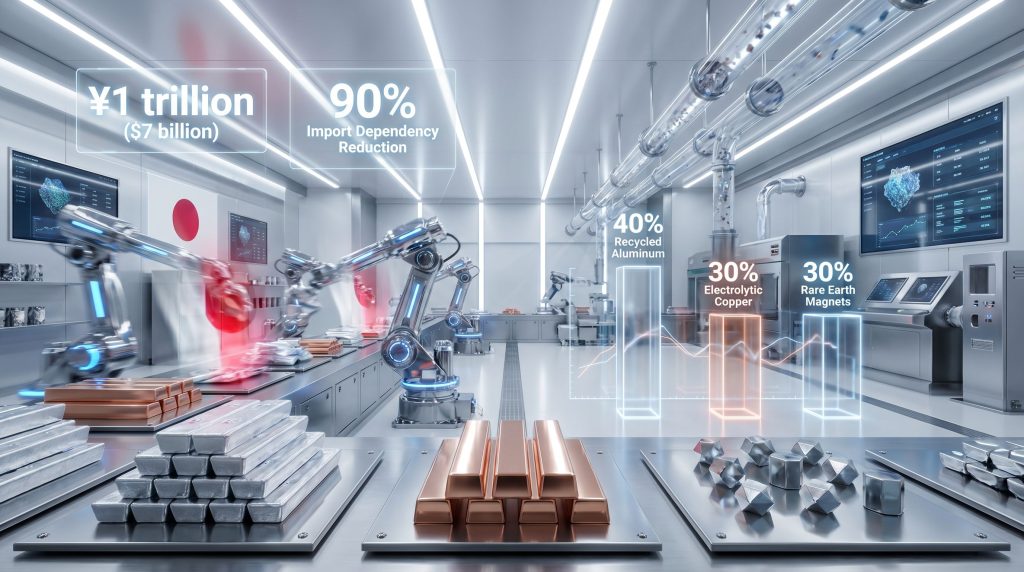

The ¥1 trillion combined public and private investment framework announced represents Japan's largest commitment to resource independence strategy. This financial commitment establishes measurable accountability mechanisms for both government agencies and private sector participants through 2030 implementation timelines.

Economic Security Through Material Independence

The initiative targets vulnerability across three critical material categories: metals including aluminium, copper, rare earth elements, and steel; plastics serving as crude oil and naphtha substitutes; and specialised materials essential for high-technology applications. This comprehensive approach recognises that single-material dependency creates unacceptable risk concentration in modern manufacturing supply chains.

Strategic timing coincides with international developments that validate domestic recycling capacity as essential infrastructure. The European Union's expanded rules on electronic scrap exports and stricter recycled plastics usage requirements create additional supply chain competition, while China's dual approach of export restrictions combined with domestic recycling expansion demonstrates the competitive advantages of circular economy development.

When big ASX news breaks, our subscribers know first

What Are Japan's Specific Recycling Targets for Critical Materials?

Japan has established precise material-by-material targets that reflect sophisticated understanding of supply chain vulnerabilities rather than pursuing uniform recycling rates across all categories. These differentiated targets acknowledge varying strategic importance levels and current recycling feasibility constraints.

Metals Sector Transformation

| Material Category | 2030 Target | Current Baseline | Strategic Significance |

|---|---|---|---|

| Recycled Aluminium (rolled products) | 40% | ~25% estimated | Automotive lightweighting, aerospace applications |

| Electrolytic Copper | 30% | ~15% estimated | Electronics manufacturing, power infrastructure |

| Rare Earth Magnets | 30% | <10% estimated | Electric vehicle motors, wind turbines |

| High-Grade Steel Scrap | +2 million tonnes/year | Limited availability | Green steel production, construction |

The aluminium target represents the most achievable near-term objective given established recycling technology and existing collection networks. Automotive manufacturers have demonstrated successful integration of recycled aluminium content, providing reference models for scaling from current 25 percent to targeted 40 percent domestic content levels.

Copper recycling expansion addresses electronics manufacturing supply security where consistent material specifications remain critical. The 30 percent target for domestically produced electrolytic copper requires substantial infrastructure investment in collection, sorting, and purification processes to meet semiconductor-grade quality standards.

Rare Earth Strategic Priority

Rare earth magnet recycling receives particular emphasis due to critical roles in electric vehicle motor production where China maintains substantial leverage through export control mechanisms. The 30 percent recycling target directly substitutes domestic supply for import vulnerability as global EV production accelerates and proportional magnet demand increases.

Current rare earth recycling capacity operates below 10 percent, indicating the technological maturation required to achieve targeted levels. This represents the most technically challenging component of Japan's recycling expansion, requiring development of cost-competitive separation and purification processes from recycled sources versus primary ore processing.

Infrastructure and Technology Integration

The plan incorporates development of AI-based sorting technologies to improve quality and reduce costs across recycling hubs and networks. This technological focus addresses quality consistency challenges that historically prevented manufacturer adoption of recycled materials due to property variability concerns.

Steel sector expansion targets high-quality scrap for green steel production with demonstrably lower greenhouse gas emissions. Processing capacity increases of approximately 2 million tonnes per year, combined with strengthened collection of scrap and industrial offcuts, positions Japan to capture market value from decarbonisation commitments requiring lower-emissions steel specifications.

Plastics Implementation Timeline

Japan will implement phased mandates on recycled content by fiscal year 2028, requiring manufacturers to formulate and report usage plans as precursors to mandatory compliance. This approach acknowledges that plastic recycling systems require collection infrastructure development and material quality standardisation before regulatory enforcement becomes economically viable.

How Will This Impact Global Commodity Markets?

Japan's transition to domestic recycled material supply will reshape global commodity markets through reduced import demand across multiple material categories. The magnitude of market impact depends on Japan's current consumption share for each commodity and the elasticity of supply responses from alternative sources.

Supply-Demand Rebalancing Dynamics

Substitution of recycled materials for virgin materials reduces demand pressure on primary mining and processing sectors globally. However, market effects vary significantly across commodity categories based on established recycling technology maturity, collection infrastructure requirements, and quality specification challenges.

Aluminium markets demonstrate established recycling economics with known cost structures and proven technology deployment. Japan's expansion from 25 percent to 40 percent recycled content represents incremental scaling of existing processes rather than fundamental technology development, suggesting predictable market transition dynamics.

Rare earth markets exhibit greater volatility due to technology immaturity and concentrated supply sources. Japan's domestic recycling development may reduce Chinese leverage but cannot eliminate dependency completely, particularly in rare earth elements where China maintains significant processing advantages beyond mining operations.

Price Stabilisation Mechanisms

Reduced Japanese import demand for virgin materials contributes to price stabilisation in critical mineral markets by decreasing volatility from single-nation demand fluctuations. This stabilisation benefit extends to other importing nations that experience reduced competition for limited global supply sources.

The strategic positioning includes recognition that technology transfer from Japanese recycling innovations will spread globally, potentially establishing Japanese technology standards as international benchmarks. This creates long-term technology export opportunities beyond immediate domestic recycling capacity expansion.

Competitive Response Implications

Other developed nations must address Japan's competitive advantage through their own circular economy initiatives or accept deteriorating relative positions in materials-intensive manufacturing sectors. The European Union's parallel circular economy framework suggests international policy alignment around similar strategic objectives, though implementation approaches differ significantly.

China's existing combination of domestic recycling expansion plus export restrictions on virgin materials creates asymmetric competitive environments that Japan's strategy directly addresses. By developing independent recycling capacity, Japan reduces leverage that export-restricting nations can exercise over its manufacturing sectors.

What Technologies Enable Japan's Recycling Revolution?

Advanced processing technologies form the foundation of Japan's circular economy transformation, requiring substantial innovation investment alongside physical infrastructure development. The technological requirements vary dramatically across material categories, from established aluminium recycling systems to experimental rare earth separation processes.

Artificial Intelligence Integration

AI-based sorting technologies address quality consistency barriers that traditionally prevented manufacturer adoption of recycled materials. Automated sorting systems promise standardised material characteristics, reducing manufacturer risk in recycled material substitution decisions.

These systems combine computer vision, spectroscopy, and machine learning algorithms to identify and separate materials with precision levels approaching manual sorting accuracy while achieving industrial-scale throughput rates. Implementation costs remain significant, but operational benefits include reduced labour requirements and improved material purity levels.

Chemical Processing Advancements

Plastic-to-chemical conversion through advanced pyrolysis and gasification represents emerging technology categories requiring process-specific infrastructure investment and feedstock quality management. Pyrolysis involves heating plastic waste without oxygen to break molecular bonds, while gasification extends this process to produce synthesis gas suitable for chemical manufacturing.

Both processes require substantial energy inputs and chemical-intensive processing steps, raising questions about net environmental benefits compared to virgin material production. Energy efficiency improvements and renewable energy integration become critical factors determining economic viability of chemical recycling expansion.

Rare Earth Separation Innovation

Rare earth element separation from recycled sources requires selective dissolution, precipitation, and crystallisation steps with high energy requirements. Current technology maturity levels for cost-competitive rare earth recycling from magnets versus primary ore processing remain experimental, representing the most technically challenging aspect of Japan's recycling targets.

Japanese electronics manufacturers' technical expertise in component design provides advantages for reverse-engineering cost-effective e-waste processing technology. Understanding original manufacturing processes facilitates development of efficient disassembly and material recovery systems.

Digital Infrastructure Components

Blockchain-based material provenance tracking addresses manufacturer concerns regarding recycled material sourcing authenticity and environmental impact credibility. Implementation enables transparent documentation of material collection, sorting, processing, and certification steps, creating quality assurance mechanisms essential for manufacturer confidence.

Predictive analytics for recycled input demand optimises supply-demand matching as recycled material supply becomes domestically sourced but geographically distributed. Real-time demand forecasting improves logistics efficiency and inventory management across complex collection and processing networks.

Which Industries Benefit Most from Japan's Recycling Push?

Industrial sectors experience varying levels of impact based on material intensity characteristics and supply chain vulnerability exposure. Manufacturing industries with high material content and established supply relationships gain the most immediate advantages from domestic recycling expansion.

Automotive Manufacturing Transformation

The automotive sector benefits significantly from aluminium and steel recycling expansion, given material intensity levels where metal content represents substantial cost components. Recycled aluminium pricing advantages combined with supply security improvements create competitive positioning benefits for Japanese manufacturers versus international competitors dependent on import supply chains.

Electric vehicle production requires rare earth magnets where domestic recycling directly addresses supply chain vulnerabilities. As EV manufacturing scales globally, magnet demand grows proportionally, making domestic recycling capacity a strategic competitive advantage rather than merely cost optimisation.

Established automotive recycling networks provide infrastructure foundations for expanding collection and processing capabilities. End-of-life vehicle processing systems already capture significant material volumes, requiring efficiency improvements and quality upgrades rather than entirely new collection networks.

Electronics Sector Supply Security

Electronics manufacturing demands precise material specifications where contamination tolerances remain extremely narrow. Recycled copper and rare earth elements must meet semiconductor-grade quality standards, requiring advanced purification processes and quality assurance systems.

Japanese electronics companies possess technical expertise in component design that facilitates reverse-engineering of efficient disassembly and material recovery systems. Understanding original manufacturing processes provides advantages for developing cost-effective e-waste processing technology.

Supply chain diversification benefits extend beyond cost considerations to include reduced dependency on volatile import sources. Electronics manufacturers gain operational flexibility through domestic sourcing options that reduce exposure to geopolitical supply disruptions.

Steel Industry Modernisation

Green steel production represents premium market positioning opportunities for manufacturers capable of demonstrating lower greenhouse gas emissions through high-quality recycled feedstock utilisation. Processing capacity expansion of 2 million tonnes per year targets this emerging market segment.

Industrial construction and infrastructure sectors increasingly specify lower-emissions materials to meet sustainability commitments, creating market demand for recycled steel products. Japanese steel producers gain competitive positioning through early development of reliable green steel supply capabilities.

Energy efficiency advantages in recycled steel production versus primary steelmaking provide cost benefits alongside emissions reductions. Electric arc furnace technology utilising recycled feedstock requires substantially less energy than blast furnace operations processing iron ore.

What Are the Economic Security Implications?

Japan's circular economy strategy directly addresses economic security vulnerabilities that extend far beyond environmental considerations. Resource independence capabilities reduce susceptibility to supply chain weaponisation while creating new competitive advantages in strategic manufacturing sectors.

Strategic Independence Metrics

Import substitution rates across critical materials provide quantifiable measures of reduced vulnerability to external supply control. Each percentage point of domestic recycling capacity represents decreased leverage that resource-exporting nations can exercise through export restrictions or supply manipulation.

Supply chain resilience improvements extend beyond immediate cost considerations to include operational continuity during crisis periods. Domestic recycling capacity provides buffer supply that moderates price volatility from external supply disruptions, enabling more predictable manufacturing planning and investment decisions.

Industrial base strength depends on maintained manufacturing competitiveness as global resource competition intensifies. Nations lacking domestic recycling capabilities face deteriorating relative positions in materials-intensive industries where input costs increasingly determine competitive outcomes.

Geopolitical Risk Reduction

Diversified sourcing through domestic recycling reduces single-source dependencies that create vulnerability to resource diplomacy. China's demonstrated willingness to utilise export restrictions for political leverage validates Japan's assessment that alternative supply sources represent essential infrastructure rather than optional efficiency improvements.

Allied cooperation opportunities emerge as Japanese recycling technology and expertise become exportable assets. Technology transfer and infrastructure development partnerships create positive-sum relationships that strengthen alliance networks while generating revenue streams.

Economic leverage reduction works bidirectionally as reduced susceptibility to resource diplomacy simultaneously provides Japan with greater negotiating flexibility in international relationships. Resource independence enables more assertive positions in trade negotiations and political disputes.

Innovation Export Potential

Japanese technology leadership in advanced recycling processes creates export opportunities as other nations develop their own circular economy capabilities. Equipment, expertise, and process licensing generate revenue streams that extend economic benefits beyond domestic cost savings.

Technology standards establishment through early deployment positions Japanese systems as international benchmarks, creating competitive advantages for domestic companies in global recycling infrastructure development markets.

The next major ASX story will hit our subscribers first

How Does This Compare to Global Circular Economy Trends?

Japan's approach aligns with international circular economy development while differentiating through specific implementation methodologies and strategic emphasis areas. Comparative analysis reveals varying national priorities and technological focus areas across major economies.

European Union Framework Comparison

The EU emphasises regulatory mandates requiring recycled content across multiple industries, contrasting with Japan's voluntary compliance mechanisms combined with infrastructure investment incentives. Both approaches target similar 2030 implementation timelines, suggesting international policy coordination around resource security objectives.

Regulatory enforcement mechanisms differ significantly between regions. EU recycled content mandates create compliance requirements with financial penalties, while Japan's investment-based approach incentivises voluntary adoption through cost advantages and supply security benefits.

Technology development priorities show regional specialisation patterns. Japan emphasises advanced processing technologies and quality standardisation, while EU initiatives focus more heavily on collection network expansion and waste stream standardisation.

Chinese Strategy Contrasts

China's recycling approach prioritises volume throughput and domestic supply security rather than high-value material quality specifications. This creates market segmentation opportunities where Japan targets premium recycled materials while China serves volume-oriented applications.

Technology development strategies reflect different competitive positioning objectives. Japan promotes international cooperation and technology sharing, while China emphasises self-sufficiency and domestic technology development with limited external collaboration.

Market integration approaches differ substantially between nations. Japan's strategy assumes continued international trade relationships with enhanced domestic capabilities, while China's approach suggests greater economic decoupling and reduced import dependency across all material categories.

International Coordination Mechanisms

Technology sharing opportunities emerge as developed nations pursue complementary rather than competitive circular economy strategies. Japanese advanced processing technology combined with EU collection networks and US innovation capabilities creates potential alliance frameworks for addressing Chinese competitive advantages.

Furthermore, Japan's business federation proposes circular economy initiatives that align with global standards harmonisation across allied nations, providing market access benefits for companies developing recycling technologies. Compatible certification systems enable equipment and expertise transfer while maintaining quality assurance capabilities.

What Investment Opportunities Emerge from This Strategy?

The ¥1 trillion investment commitment creates multiple channels for capital deployment across technology development, infrastructure construction, and operational scaling. Investment opportunities span established recycling technologies and experimental processing methods with varying risk-return profiles.

Technology Development Investments

Advanced separation and purification systems represent high-value investment opportunities with significant intellectual property potential. Companies developing AI-based sorting technologies and automated processing equipment can capture substantial market share as recycling infrastructure expands globally.

Research and development investments in next-generation recycling technologies offer long-term competitive positioning advantages. Breakthrough innovations in rare earth separation or chemical recycling efficiency create market leadership opportunities with substantial barriers to entry.

Digital infrastructure investments including supply chain management platforms and quality assurance systems provide scalable business models with recurring revenue potential. Blockchain-based provenance tracking and predictive analytics systems serve multiple industries and geographic markets.

Infrastructure Development Opportunities

Regional recycling hub development requires substantial capital investment with stable, long-term revenue generation potential. Processing facilities serving specific material categories or geographic regions provide essential infrastructure with regulated utility-like characteristics.

Collection network expansion investments include transportation systems, storage facilities, and aggregation centres that connect dispersed waste sources with centralised processing capabilities. These investments provide predictable cash flows while serving essential economic functions.

Strategic material reserves represent government-backed investment opportunities with national security implications. Storage capacity for critical recycled materials provides supply security benefits while generating returns through price arbitrage and strategic stockpile management.

Market Development Investments

Quality assurance and certification capabilities create value-added services with high margins and strong competitive moats. Testing facilities and certification systems enable recycled material market expansion by providing manufacturer confidence in material specifications.

Supply chain integration investments connect recycling capacity with end-user manufacturing requirements through specialised logistics and inventory management systems. These investments capture value from improved material flow efficiency and reduced transaction costs.

What Challenges Could Limit Success?

Despite comprehensive planning and substantial financial commitments, several structural and technical constraints could prevent Japan to boost recycled materials supply from achieving its circular economy objectives. Understanding these limitations enables more realistic assessment of implementation timelines and investment risks.

Technology Maturity Constraints

Many recycling processes, particularly for rare earth elements and advanced plastics, remain experimental with unproven commercial viability at scale. Laboratory demonstrations do not guarantee successful industrial implementation, especially when cost competitiveness with virgin materials becomes the determining factor.

Quality consistency challenges across diverse waste streams require technological solutions that may not exist at required performance levels. Recycled materials must meet exact specifications for manufacturing applications, demanding precision that current sorting and processing technologies may not achieve reliably.

Scale requirements for economic viability may exceed Japan's domestic waste generation capacity in certain material categories. If insufficient feedstock volumes exist to support efficient processing operations, economic targets become unachievable regardless of technology development success.

Market Adoption Barriers

Manufacturer acceptance of recycled inputs requires overcoming institutional resistance and established supply relationships. Quality concerns, supply reliability questions, and procurement policy constraints create adoption barriers that persist despite cost advantages.

Consumer acceptance of products containing recycled materials remains variable across applications. Premium market segments may resist recycled content due to perceived quality compromises, limiting market development potential for certain product categories.

International supply chain integration challenges arise when domestic recycling capabilities must interface with global manufacturing networks. Compatibility requirements with international quality standards and certification systems create complexity that may delay implementation.

Economic Competitiveness Challenges

Virgin material price competitiveness depends on commodity market dynamics beyond Japan's control. If global mining costs decrease or new supply sources develop, recycled materials may lose competitive advantages that justify infrastructure investment costs.

Energy requirements for recycling processes, particularly chemical recycling and rare earth separation, may exceed energy costs for virgin material production. Without substantial renewable energy cost reductions, recycling economics may remain unfavourable.

Capital cost recovery timelines for recycling infrastructure investment may extend beyond investor patience or government commitment periods. Long payback periods create financing challenges and political sustainability risks for sustained policy support.

Long-term Implications for Global Resource Markets

Japan's circular economy transformation establishes precedents that will influence how other developed nations approach resource security challenges while maintaining industrial competitiveness. The success or failure of this initiative will determine the viability of similar strategies globally.

Market Structure Evolution Pathways

Recycling premium development creates value differentiation opportunities for circular materials that command price premiums over virgin equivalents. Success in establishing quality certification systems enables recycled materials to capture value from sustainability commitments across industrial sectors.

Supply chain localisation trends accelerate as nations prioritise domestic processing capabilities over international efficiency optimisation. Regional recycling clusters may replace global commodity trading networks for critical materials, fundamentally altering international trade patterns.

Technology standardisation through Japanese innovation deployment potentially establishes global benchmarks for recycling processes and quality assurance systems. Early implementation advantages create competitive positions that persist through technology licensing and expertise transfer.

Strategic Positioning Outcomes

Industrial leadership transition may favour nations with advanced recycling capabilities as resource scarcity intensifies and environmental regulations tighten. Japan's early investment in circular economy infrastructure positions it advantageously for competing in resource-constrained global markets.

Economic resilience improvements through reduced vulnerability to supply disruptions enable more assertive international positioning and greater negotiating flexibility in trade relationships. Resource independence capabilities translate into political and economic leverage advantages.

Innovation export development creates new economic sectors focused on recycling technology and expertise transfer. Japanese companies may capture substantial international market share in recycling infrastructure development as other nations implement similar strategies.

The transformation represents a fundamental shift from resource consumption toward resource circulation, with implications extending far beyond Japan's borders. Success demonstrates the viability of circular economy approaches for addressing resource security challenges, while failure would validate continued dependence on traditional commodity supply chains despite associated vulnerabilities.

Moreover, this strategic initiative builds upon existing battery recycling breakthrough technologies and enhances the overall battery recycling process across various industries. Additionally, Japan's approach integrates innovative waste management solutions and leverages data-driven operations to optimise efficiency throughout the recycling value chain. Consequently, this comprehensive strategy supports the broader critical minerals energy transition essential for achieving long-term energy security and sustainable economic development.

Investment decisions based on resource market developments should consider the evolving regulatory landscape and technological maturation timelines. This analysis does not constitute investment advice and readers should conduct independent research before making financial commitments.

Want to Stay Ahead of Critical Minerals Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities as resource markets evolve rapidly with changing recycling technologies and supply chain dynamics. Start your 14-day free trial today to position yourself ahead of the market as global resource strategies reshape investment opportunities across critical minerals sectors.