July 22, 2026

Japan's Continued Reliance on Chinese Rare Earth Supplies

Japan leans on China for rare earths despite lower imports, demonstrating the persistent structural challenges facing nations attempting to diversify critical mineral supply chains. Despite sustained policy initiatives and strategic investment programs, Japan's dependency on Chinese rare earth processing infrastructure has actually increased in recent months. This trend highlights the complex dynamics between geopolitical tensions and industrial realities, where economic efficiency often supersedes supply chain security considerations. Understanding these patterns requires examining both quantitative trade flows and the qualitative factors that determine long-term strategic positioning in resource security frameworks.

When big ASX news breaks, our subscribers know first

East Asian Supply Chain Concentration Dynamics

Resource dependency patterns across Asia-Pacific economies reveal structural imbalances that traditional diversification strategies struggle to address effectively. Processing capacity concentration creates bottlenecks that persist despite policy initiatives aimed at supply chain resilience. These constraints manifest through cost structures, technical specifications, and operational timelines that favour incumbent suppliers over emerging alternatives.

The metallurgical requirements for high-performance applications determine sourcing patterns more than geopolitical preferences. Light rare earth elements (LREEs) including lanthanum, cerium, and neodymium serve electronics manufacturing and automotive applications with specific purity profiles. Heavy rare earth elements (HREEs) such as dysprosium, terbium, and yttrium require substantially higher technical standards for defence systems and advanced manufacturing applications.

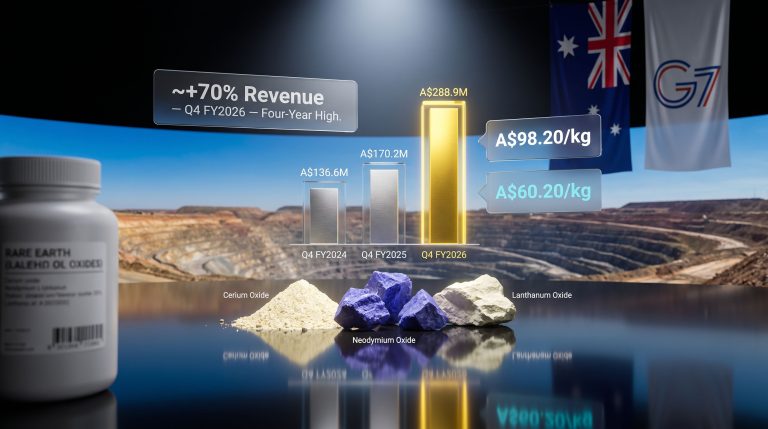

Japan's January 2026 import data demonstrates these structural realities. China supplied approximately 76% of rare earth materials imported by Japan, representing a 3.4 percentage point increase from the same period in 2025 when China's share stood at approximately 72.6%. This increased market concentration coincided with reduced absolute volumes, as Japan purchased 1,127 tons of metal equivalent from China in January 2026, representing a 5.7% decline compared to January 2025.

Understanding Processing Infrastructure Dependencies

Global rare earth processing capacity remains concentrated in China, which controls approximately 91% of global refining operations. This processing dominance creates structural advantages beyond raw material extraction, as downstream purification, separation, and alloying capabilities require specialised technical expertise and substantial capital investment.

The secondary supplier landscape demonstrates Japan's nascent diversification efforts, though progress remains constrained by processing capacity limitations. Vietnam emerged as the second-largest supplier in January 2026, shipping approximately 221 tons of metal equivalent, whilst France ranked third with 79 tons. Malaysian imports showed growth momentum, rising 32% in January 2026 to slightly over 1 ton of metal equivalent, though this absolute volume remains minimal relative to Chinese supplies.

Cost differentials between Chinese and alternative suppliers typically range from 5-6 times higher prices for comparable materials processed outside China's established infrastructure. These price gaps reflect not only economies of scale but also technological learning curves, environmental compliance costs, and supply chain integration efficiencies that favour mature processing operations.

Furthermore, the critical minerals strategy adopted by regional governments faces implementation challenges due to these entrenched cost advantages and technical barriers.

Technical Specifications and Quality Standards

Manufacturing applications across Japan's critical sectors require specific metallurgical compositions that determine supplier qualification more than price considerations alone. Neodymium-iron-boron (NdFeB) magnets represent a critical application combining rare earths with other materials for uses ranging from consumer electronics to advanced defence systems.

The purity levels and elemental composition standards achieved by different suppliers create technical barriers to rapid diversification. Japanese manufacturers in electronics and automotive sectors requiring magnets for electric vehicles and advanced motor systems necessitate specific quality profiles that suppliers must demonstrate consistently over multiple production cycles before achieving qualification status.

Geopolitical Risk Frameworks and Supply Security

Trade restriction mechanisms create operational complexity that extends beyond binary supply disruptions. China's implementation of export restrictions on rare earth materials classified as dual-use products with potential military applications targets specific supply chains whilst maintaining civilian trade flows through selective licensing mechanisms.

The dual-use technology classification system distinguishes between civilian and military-applicable uses through administrative procedures that can shift rapidly based on diplomatic tensions. This creates planning uncertainty for industrial users who require consistent supply access for long-term production commitments and inventory management strategies.

Historical precedents from the 2010 diplomatic tensions demonstrated how supply constraints can emerge through administrative delays rather than outright trade bans. Current trade patterns suggest similar mechanisms may be operating, where processing and shipping timelines extend without complete supply cutoffs, creating operational pressure whilst maintaining plausible commercial explanations.

Moreover, the US-China trade war impact continues to influence global rare earth supply chains, creating additional complexity for Japanese importers navigating these geopolitical tensions.

Emergency Response Mechanisms and Strategic Reserves

Japan's strategic materials inventory management operates through both government stockpiling initiatives and private sector buffer stock requirements. The Japan Organization for Metals and Energy Security (Jogmec) coordinates strategic reserve accumulation targeting multiple months of consumption coverage across critical materials categories.

Government intervention protocols establish trigger mechanisms based on supply disruption severity and duration. These frameworks differentiate between temporary logistics delays, administrative restrictions, and fundamental supply source elimination, with escalating response measures calibrated to disruption intensity and strategic criticality of affected materials.

Private sector adaptation strategies include supplier qualification diversification, increased inventory positions, and substitute material development programs. Manufacturing companies maintain relationships with multiple suppliers whilst accepting higher costs for supply security, treating additional sourcing expenses as operational insurance against disruption risks.

In addition, Australia's development of a critical minerals reserve provides another strategic option for Japan's supply diversification efforts.

Strategic Assessment Framework:

Supply chain resilience requires evaluating multiple risk dimensions simultaneously, including geopolitical tensions, processing capacity constraints, technical qualification timelines, and cost structure sustainability across alternative sourcing options.

Alternative Processing Infrastructure Development

Regional processing capacity expansion faces substantial technical and financial barriers that constrain rapid diversification achievements. Vietnam's emergence as an intermediate processing hub reflects its integration within existing Chinese supply chains rather than independent processing infrastructure development.

Vietnamese rare earth processing operations likely involve partial refining of intermediate materials sourced from Chinese mining operations, with downstream finishing steps enabling market diversification whilst maintaining cost competitiveness. The specific technical capabilities, quality control systems, and production scaling potential of Vietnamese facilities determine their viability as sustained alternative suppliers.

Malaysia's processing infrastructure, anchored by Lynas Rare Earths facility, demonstrates the challenges confronting alternative capacity development. Despite the presence of established operations, Malaysian imports to Japan reached only slightly over 1 ton of metal equivalent in January 2026, indicating capacity constraints or market positioning limitations relative to demand requirements.

Investment Requirements and Development Timelines

Processing facility development requires substantial capital investment, typically measuring in hundreds of millions of dollars for comprehensive separation and purification capabilities. Environmental compliance, waste management systems, and specialised equipment procurement extend development timelines to multiple years even with committed financing and regulatory approval.

The technical expertise required for consistent rare earth processing involves metallurgical knowledge, chemical engineering capabilities, and quality control systems that represent significant barriers to entry. Training qualified personnel and establishing operational procedures requires extended periods beyond initial facility construction and equipment installation.

Australian mining operations combined with overseas processing represent one pathway for supply chain diversification, though transportation costs and logistics complexity add operational challenges. The geographic separation between mining and processing locations creates coordination requirements and inventory management complications that integrated operations avoid.

However, Japan has begun subsidising rare earth recycling initiatives as part of its broader strategy to reduce dependence on Chinese supplies.

Regional Supply Chain Integration Patterns

Supply Chain Development Matrix:

| Processing Location | Capacity (tons/year) | Primary Applications | Supply Sources |

|---|---|---|---|

| Malaysia (Lynas) | Limited commercial | Electronics, automotive | Australian mines |

| Vietnam (Multiple) | Intermediate processing | Electronics, consumer | Chinese integration |

| France (Recycling) | Specialty applications | High-tech, defence | EU waste streams |

| Japan (Domestic) | Research & development | Advanced materials | Recycled sources |

Furthermore, Europe's European CRM facility initiatives provide additional context for understanding global supply chain diversification efforts.

Market Structure Evolution and Pricing Dynamics

Rare earth market pricing reflects both supply concentration and demand volatility across different application sectors. Price formation mechanisms differ substantially between light and heavy rare earth elements due to abundance differentials and application-specific demand patterns.

Market volatility in rare earth pricing stems from the limited number of applications requiring these materials and the tendency for volumes to vary significantly even under normal market conditions. Monthly import fluctuations can exceed 20% due to inventory management decisions, production scheduling adjustments, and seasonal demand patterns across manufacturing sectors.

Hedging strategies for rare earth price exposure remain limited due to market concentration and the lack of standardised futures contracts for most elements. Industrial users typically manage price risk through long-term supply agreements, strategic inventory positioning, and substitute material development programs rather than financial hedging instruments.

Processing Capacity Investment Economics

Alternative processing infrastructure development requires sustained investment commitments spanning multiple economic cycles. The capital intensity of separation facilities, combined with uncertain demand volumes and competitive pricing pressure from established operations, creates challenging investment economics for new entrants.

Government support mechanisms, including loan guarantees, strategic project designation, and accelerated permitting, can improve investment economics for alternative processing capacity. However, commercial viability ultimately depends on achieving sufficient operational scale and technical capabilities to compete with established Chinese processing operations.

Technology transfer restrictions and intellectual property considerations create additional barriers for processing infrastructure development outside established supply chains. Equipment procurement, technical licensing, and operational expertise acquisition face scrutiny under dual-use technology export controls.

Consequently, the broader mining industry innovation trends play a crucial role in enabling alternative supply chain development.

Strategic Alliance Formation and Risk Distribution

International cooperation frameworks for critical minerals security involve both governmental agreements and private sector partnership structures. These arrangements aim to distribute supply risks across multiple jurisdictions whilst coordinating investment in alternative infrastructure development.

QUAD initiative mineral security components include information sharing, joint stockpiling mechanisms, and coordinated supplier development programs. These multilateral frameworks provide political support for diversification investments whilst establishing communication channels for supply disruption response coordination.

Japan-Australia bilateral cooperation extends beyond raw material supply agreements to include processing technology sharing, joint facility development, and coordinated research programs. These partnerships attempt to create integrated alternative supply chains spanning extraction, processing, and manufacturing applications.

Private Sector Partnership Models

Risk-sharing mechanisms between mining companies, processing operators, and end-users involve long-term supply agreements, joint venture structures, and shared infrastructure investments. These arrangements provide certainty for capacity expansion investments whilst distributing operational risks across multiple parties.

Investment syndication for alternative supply chain development spreads financial commitments across institutional investors, strategic partners, and government backing. This approach enables larger-scale infrastructure projects whilst reducing individual exposure to operational and market risks.

Technology licensing agreements and equipment sharing arrangements facilitate knowledge transfer and operational efficiency improvements across alternative processing operations. These cooperative structures help overcome technical barriers whilst accelerating capability development timelines.

The next major ASX story will hit our subscribers first

Investment Implications and Market Psychology

Critical minerals supply security creates investment opportunities across multiple segments of alternative supply chain development. These opportunities span mining operations, processing infrastructure, recycling technology, and substitute material development, each with distinct risk-return profiles and investment timelines.

Mining companies with diversification mandates from major importing countries benefit from strategic support mechanisms and preferential supply agreement access. However, operational execution capabilities and geological resource quality determine long-term commercial success beyond policy support advantages.

Processing facility development projects represent higher-risk, higher-return investment profiles due to technical complexity and market concentration challenges. Successful projects require substantial capital commitments, extended development timelines, and sustained operational expertise to achieve competitive positioning.

Technology Development Investment Themes

Recycling technology advancement offers potentially attractive investment returns through material recovery efficiency improvements and processing cost reductions. Magnet recycling capabilities, electronic waste processing, and industrial waste stream utilisation represent growing market segments with favourable supply-demand dynamics.

Substitute material development involves research-intensive investments with uncertain commercial outcomes but potentially transformative market impacts. Success in developing viable alternatives to rare earth applications could fundamentally alter supply chain dependencies and market structures.

Investment Risk Assessment Framework:

- Geopolitical escalation probability and trade disruption scenarios

- Infrastructure development timelines for alternative sources

- Technology transfer restrictions and intellectual property considerations

- Currency fluctuations affecting import cost structures

- Regulatory changes affecting mineral trade and processing

According to insights from Japan's critical minerals strategy analysis, the nation continues to face significant challenges in achieving meaningful supply chain diversification despite sustained policy efforts.

Future Market Evolution and Strategic Positioning

Long-term demand projections for rare earth materials reflect electric vehicle production growth, defence sector requirements, and electronics manufacturing expansion across Asia-Pacific economies. These demand drivers create sustained growth potential despite supply chain diversification efforts and substitute material development.

Electric vehicle adoption acceleration in Japan and export markets increases neodymium and dysprosium requirements for high-performance motor magnets. This demand growth creates market expansion opportunities for alternative suppliers whilst maintaining upward pressure on pricing across global markets.

Defence sector strategic stockpiling and redundant supply chain requirements represent additional demand sources that support alternative supplier development. Military applications often accept higher costs for supply security, creating market segments where alternative suppliers can achieve commercial viability despite cost disadvantages.

Regulatory Evolution and Policy Frameworks

Government intervention mechanisms continue evolving to address supply chain vulnerabilities whilst supporting alternative infrastructure development. These policy frameworks balance market efficiency considerations with strategic security objectives through subsidies, stockpiling programs, and international cooperation initiatives.

International cooperation frameworks including bilateral agreements and multilateral initiatives provide diplomatic support for diversification investments whilst coordinating response mechanisms for supply disruptions. These arrangements create political foundations for sustained alternative supply chain development.

Trade policy evolution affects import procedures, tariff structures, and administrative requirements that influence supply chain economics. Regulatory changes can shift competitive advantages between different sourcing options whilst creating opportunities for strategic positioning across alternative supply chains.

Japan leans on China for rare earths despite lower imports, reflecting the enduring reality of established processing infrastructure advantages and technical barriers to diversification. Japan's experience with rare earth supply dependencies demonstrates the complex interplay between market forces, technological constraints, and geopolitical considerations that shape critical minerals security. Furthermore, whilst diversification efforts continue advancing, structural advantages of established processing infrastructure create persistent challenges that require sustained investment commitments and international cooperation to address effectively.

Investment Disclaimer: This analysis contains forward-looking statements and market projections that involve uncertainty and risk. Rare earth market investments carry substantial volatility, regulatory risk, and geopolitical exposure that may result in significant losses. Readers should conduct independent research and consult qualified advisors before making investment decisions related to critical minerals or supply chain security themes.

Want to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including rare earths and critical minerals sectors, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, then begin your 14-day free trial today to position yourself ahead of the market.