July 9, 2026

Institutional Capital and the Aluminium Supercycle: What Large-Scale Equity Moves Reveal About Metal Markets

Commodity markets rarely move in straight lines, and the investors who profit most from them are seldom those reacting to headlines. The most instructive signals often come from the quiet accumulation patterns of globally systemically important financial institutions, whose portfolio decisions reflect months of proprietary research, macroeconomic modelling, and commodity price scenario analysis. When a bank of JPMorgan's scale deliberately crosses a regulatory disclosure threshold in a major Chinese aluminium producer, the JPMorgan stake increase in Chalco deserves scrutiny that goes well beyond the transaction itself.

Understanding what this kind of equity positioning communicates, and why it matters to investors tracking the aluminium complex, requires examining the intersection of institutional portfolio theory, Hong Kong's disclosure architecture, and the structural forces reshaping global aluminium demand.

When big ASX news breaks, our subscribers know first

Decoding the JPMorgan Stake Increase in Chalco

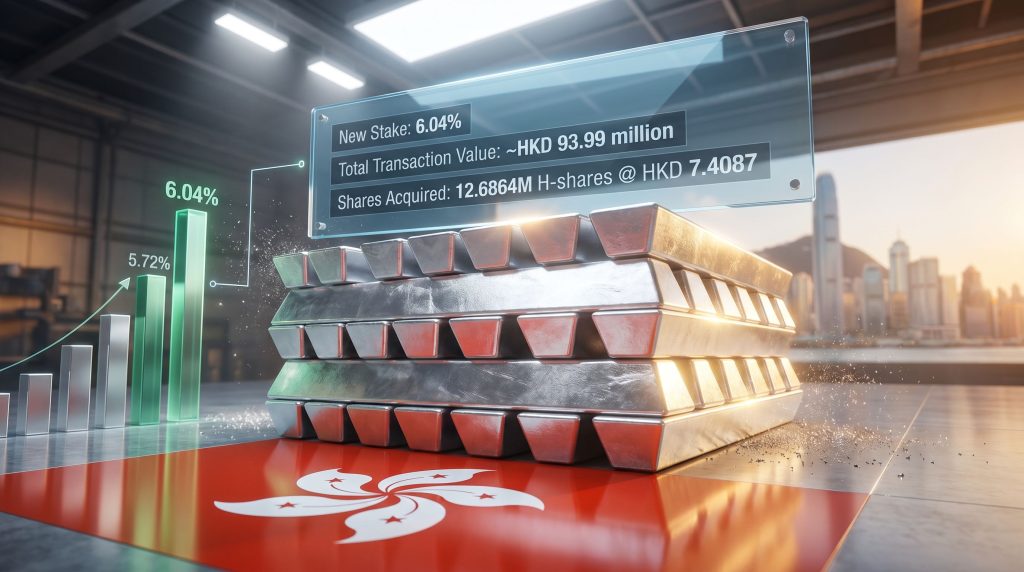

The JPMorgan stake increase in Chalco, formally the Aluminum Corporation of China (HKEx: 02600), was disclosed via the Hong Kong Stock Exchange on 8 July 2025, covering a transaction executed six days earlier on 2 July. The bank acquired an additional 12.6864 million H-shares, lifting its total position from 5.72% to 6.04% and bringing its aggregate holding to approximately 239 million shares.

The transaction was executed across two venue types, with on-exchange purchases averaging HKD 7.4087 per share and off-exchange transactions averaging HKD 7.4168 per share. The near-identical pricing across both legs points toward a deliberate, coordinated execution strategy rather than opportunistic buying. The total acquisition cost was approximately HKD 93.99 million, equivalent to roughly USD 11.9 million.

| Metric | Detail |

|---|---|

| Previous Stake | 5.72% |

| New Stake | 6.04% |

| Additional Shares Acquired | 12.6864 million H-shares |

| On-Exchange Average Price | HKD 7.4087 per share |

| Off-Exchange Average Price | HKD 7.4168 per share |

| Total Transaction Value | |

| Total Shares Held Post-Transaction | ~239 million shares |

| Transaction Date | 2 July 2025 |

| Disclosure Filing Date | 8 July 2025 (HKEX) |

The near-identical pricing between on-exchange and off-exchange legs of this transaction suggests deliberate execution strategy, minimising price impact while achieving a specific ownership target, rather than opportunistic market buying.

The strategic weight behind this transaction should not be underestimated. Crossing from 5.72% to 6.04% is not simply an arithmetic increment. In institutional portfolio construction, a deliberate threshold crossing in a large-cap commodity producer signals that position managers have made an active decision to deepen conviction. This is categorically different from passive index rebalancing, which typically involves proportional adjustments tied to benchmark weights rather than targeted ownership goals.

Furthermore, this move aligns with the broader JPMorgan mining upgrade thesis, suggesting the bank's commodity conviction extends meaningfully across multiple resource classes.

How Hong Kong's Equity Disclosure Framework Shapes Market Transparency

The HKEX 5% Rule and Its Market Function

Hong Kong's regulatory framework mandates that any entity holding 5% or more of a listed company's issued share capital must formally disclose that interest, and subsequently report any change of 1% or more in either direction. This requirement applies uniformly to institutional investors, sovereign wealth funds, and corporate entities. Directors and senior executives of listed companies face parallel obligations covering both equity and debt instrument holdings.

The legal basis for this framework sits within Hong Kong's Securities and Futures Ordinance (SFO), which requires disclosure filings to be submitted within three business days of the triggering event. JPMorgan's 2 July transaction and its 8 July disclosure are fully consistent with this regulatory window.

The practical functions of this framework extend across several dimensions of market operation:

- Price discovery: Mandatory filings allow market participants to reprice securities based on verified large-holder positioning, reducing information asymmetry.

- Control identification: Regulators and investors can trace which entities hold meaningful economic influence over listed companies, even without formal board seats.

- Conflict of interest mapping: Disclosure obligations expose potential conflicts when large shareholders engage in related-party transactions or asset transfers involving the listed entity.

- Sentiment signalling: Institutional accumulation patterns, once disclosed, serve as lagging but meaningful indicators of sophisticated investor conviction in specific sectors.

Why the Off-Exchange Leg of This Transaction Is Analytically Significant

The use of both on-exchange and off-exchange execution venues is a practised technique among large institutional buyers seeking to acquire significant share volumes without triggering material price movement. Off-exchange, or block, transactions are negotiated directly between parties at agreed prices, which substantially reduces the market impact that would result from placing a large order through the open order book.

The fact that JPMorgan employed both channels simultaneously suggests a volume requirement that exceeded what the open market could efficiently absorb at the target price. According to Reuters reporting on JPMorgan's recent stake activity, the bank has demonstrated a consistent pattern of deliberate accumulation in major resource equities, reinforcing the view that this Chalco transaction is part of a broader, coordinated strategic approach.

Chalco's Strategic Position Within the Global Aluminium Supply Architecture

Scale, Integration, and State Linkage

Chalco is among the most vertically integrated aluminium mining companies in the world, operating across every stage of the value chain from bauxite extraction and alumina refining through to primary aluminium smelting and downstream product fabrication. As a subsidiary of Chinalco, one of China's largest state-owned enterprises, Chalco functions simultaneously as a commercial entity and as a structural component of China's industrial policy apparatus.

China currently accounts for approximately 57 to 59% of global primary aluminium production, a share that has remained relatively stable even as environmental and energy constraints have introduced periodic supply volatility. Chalco represents a meaningful proportion of this domestic output, making its financial performance closely correlated to both Chinese energy policy and global aluminium price cycles. For context on the broader competitive landscape, reviewing leading aluminium mining companies helps illustrate where Chalco sits within the global hierarchy.

Production Dynamics and Near-Term Variables

Several operational factors create complexity for institutional investors modelling Chalco's forward earnings:

- Hydropower dependency in Yunnan province: A significant share of China's aluminium smelting capacity is located in Yunnan, where smelters are powered by hydroelectric generation. During drought periods or grid management interventions, provincial authorities have mandated production cuts that directly reduce output volumes. This introduces seasonal and climatic risk into supply forecasts.

- Export tax policy shifts: China's government has periodically adjusted export taxes on aluminium and aluminium products to manage domestic supply availability and support downstream manufacturing competitiveness. Changes to this policy create direct earnings volatility for producers with international sales exposure.

- Carbon regulation trajectory: China's evolving emissions trading scheme (ETS) and broader decarbonisation targets are placing increasing cost pressure on energy-intensive smelting operations, with implications for long-run production economics.

The Macro Case for Institutional Accumulation in Chinese Aluminium Equities

Aluminium as a Critical Transition Metal

Aluminium's role in the global energy transition has undergone a significant reappraisal over the past several years. Once viewed primarily as a commodity tied to construction and packaging cycles, it is now recognised as structurally essential to multiple clean energy applications:

- Electric vehicle battery housings, structural frames, and heat management systems require substantial aluminium volumes per unit, with EV platforms typically containing significantly more aluminium than equivalent internal combustion vehicles.

- Solar panel framing and mounting systems rely on extruded aluminium profiles, meaning that every gigawatt of installed solar capacity translates into measurable incremental demand.

- Grid infrastructure expansion, including transmission line conductors and transformer components, uses aluminium extensively as a lower-weight, cost-effective alternative to copper in certain applications.

This broadening demand base has prompted institutional commodity research teams to revise aluminium's long-run demand trajectory upward, particularly in scenarios where EV adoption accelerates beyond current baseline projections. However, it is also worth noting that the aluminium tariff impacts from US trade policy add a layer of complexity to near-term price forecasting for globally exposed producers.

H-Share Valuation Dynamics and Structural Discount

Chinese H-shares, by which companies incorporated in mainland China list on the Hong Kong Stock Exchange for international investor access, have historically traded at a persistent discount to their A-share equivalents listed on the Shanghai or Shenzhen exchanges. This valuation gap reflects a combination of factors including differing investor bases, liquidity dynamics, and historical restrictions on cross-border capital flows.

For institutional investors with access to HKEX-listed securities, this structural discount can represent a meaningful entry advantage. Acquiring economic exposure to the same underlying business at a lower per-share valuation, in a freely tradeable currency, is a structurally attractive proposition when the underlying commodity thesis is constructive.

| Investment Approach | Mechanism | Risk Profile | Liquidity |

|---|---|---|---|

| H-share equity (e.g., Chalco 02600) | Direct ownership via HKEX | Moderate-High | High |

| LME aluminium futures | Derivatives contract | High | Very High |

| Aluminium ETFs (global) | Fund-level exposure | Low-Moderate | High |

| A-share equity (Shanghai-listed) | Restricted foreign access | High (regulatory) | Moderate |

| Alumina/bauxite producer equities | Upstream exposure | High | Variable |

Reading Institutional Signals as a Barometer for Sector Outlook

When globally systemically important banks increase direct equity exposure to primary aluminium producers, the move often reflects proprietary views on commodity price trajectories that precede the formation of broader market consensus. The timing of JPMorgan's acquisition in early July 2025 coincides with a period of aluminium price consolidation following earlier volatility driven by Chinese energy policy adjustments and evolving global trade frameworks.

If aluminium prices recover materially through the second half of 2025 driven by infrastructure stimulus or accelerated EV adoption, a position in Chalco at sub-HKD 7.50 per share could represent a highly asymmetric risk-reward profile for a long-duration institutional portfolio.

It is worth noting that equity stake acquisitions do not directly affect physical commodity supply or demand. However, they function as a credible signal that sophisticated capital has formed a constructive medium-term view on sector fundamentals, and institutional investors monitoring HKEX disclosure filings as a sentiment indicator will have noted this filing with interest.

Lesser-Known Dynamics That Inform This Positioning

The Aluminium Inventory Cycle and Its Relationship to Institutional Positioning

One aspect of aluminium market mechanics that receives less mainstream attention is the relationship between bonded warehouse inventory levels in China and the timing of institutional equity accumulation. When Chinese aluminium inventories at key bonded facilities decline, it typically signals improving domestic demand absorption, which historically precedes price recovery cycles.

Sophisticated institutional investors tracking these physical market indicators alongside equity valuation metrics can identify positioning opportunities that are not visible to investors relying solely on financial statement analysis. Periods of destocking in Chinese aluminium markets have repeatedly coincided with improved operational leverage for producers like Chalco, as higher realised prices flow directly through to margin expansion given the relatively fixed cost structure of smelting operations.

Bauxite Supply Concentration and Upstream Risk

A dimension of Chalco's strategic positioning that warrants attention is its exposure to bauxite supply concentration risk. Global bauxite reserves are heavily concentrated in a small number of countries including Australia, Guinea, Brazil, and Indonesia. China is not among the world's leading bauxite reserve holders on a per-capita basis, meaning that domestic aluminium production depends substantially on imported raw material, particularly from Guinea, which has emerged as a critical supply node.

Any disruption to bauxite supply chains, whether from geopolitical instability, export restrictions, or logistical constraints, creates upstream cost pressure for Chinese smelters including Chalco. Institutional investors building long-duration positions in Chalco are implicitly accepting this upstream supply risk as part of their exposure profile.

In addition, the China metals demand outlook remains a critical variable, as any softening in domestic industrial activity could meaningfully compress the demand side of Chalco's earnings equation.

The Significance of Crossing 6% in a State-Linked Entity

It is important to contextualise what a 6.04% stake does and does not confer in the context of a state-owned enterprise. Chalco's controlling shareholder is Chinalco, which holds the overwhelming majority of economic and voting interest. A 6% position grants JPMorgan disclosure obligations under HKEX rules and a proportional economic claim on Chalco's earnings and assets, but no meaningful board representation or operational influence.

This structural reality means that JPMorgan's position is a pure directional commodity and equity market bet, with no governance optionality embedded in the holding. For investors evaluating the signal value of this transaction, that clarity is actually useful: the acquisition reflects a straightforward conviction on aluminium price trajectory and Chalco's operating leverage, uncomplicated by activist or control ambitions. Consequently, this contrasts with structures such as the Alcoa joint venture model, where strategic partners retain operational influence alongside their equity positions.

Futunn's reporting on JPMorgan's increased stake in Chalco further confirms the transactional details outlined in the HKEX filing, providing additional verification for investors cross-referencing the disclosure data.

The next major ASX story will hit our subscribers first

Key Takeaways for Investors Tracking Aluminium Market Dynamics

Synthesising the transaction details, regulatory context, and macroeconomic backdrop, several conclusions stand out for investors monitoring the aluminium complex:

- The JPMorgan stake increase in Chalco from 5.72% to 6.04% represents a deliberate conviction trade executed with sophisticated dual-venue methodology, not passive index rebalancing.

- Hong Kong's SFO-based disclosure regime provides investors with a reliable, time-bound transparency mechanism that makes large institutional positioning visible within three business days of execution.

- Chalco's position as a vertically integrated, state-linked producer within the world's dominant aluminium-producing nation gives this equity stake significant structural leverage to commodity price recovery.

- Aluminium's expanding role in electric vehicles, solar infrastructure, and grid buildout provides a credible long-duration demand thesis that supports institutional accumulation at current valuation levels.

- Structural H-share discounts relative to A-share equivalents offer foreign institutional investors a cost-efficient entry point into Chinese aluminium exposure.

- Upstream bauxite dependency and hydropower-linked production variability represent the most material risk factors embedded in a Chalco long position.

- Threshold-crossing acquisitions by globally systemically important banks in large-cap commodity producers have historically functioned as leading indicators of broader sector re-rating events, though past patterns do not guarantee future outcomes.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial advice or an investment recommendation. All forward-looking statements, scenario projections, and market outlook commentary involve inherent uncertainty. Past institutional positioning patterns are not a reliable indicator of future price performance. Investors should conduct independent due diligence and consult qualified financial advisers before making investment decisions.

Want to Catch the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and translating complex data into actionable investment opportunities — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.