June 25, 2026

The Quiet Revolution in Junior Mining M&A: How Permitted Assets Are Reshaping Growth Strategies

Across the global mining sector, a structural shift has been underway for several years that rarely receives the attention it deserves. Senior producers, under pressure to optimise capital returns and narrow operational focus, have been quietly divesting permitted, past-producing assets that no longer fit their portfolio thresholds. For junior and emerging mid-tier miners with the technical capability to restart these operations, this trend represents one of the most capital-efficient growth pathways available anywhere in the industry.

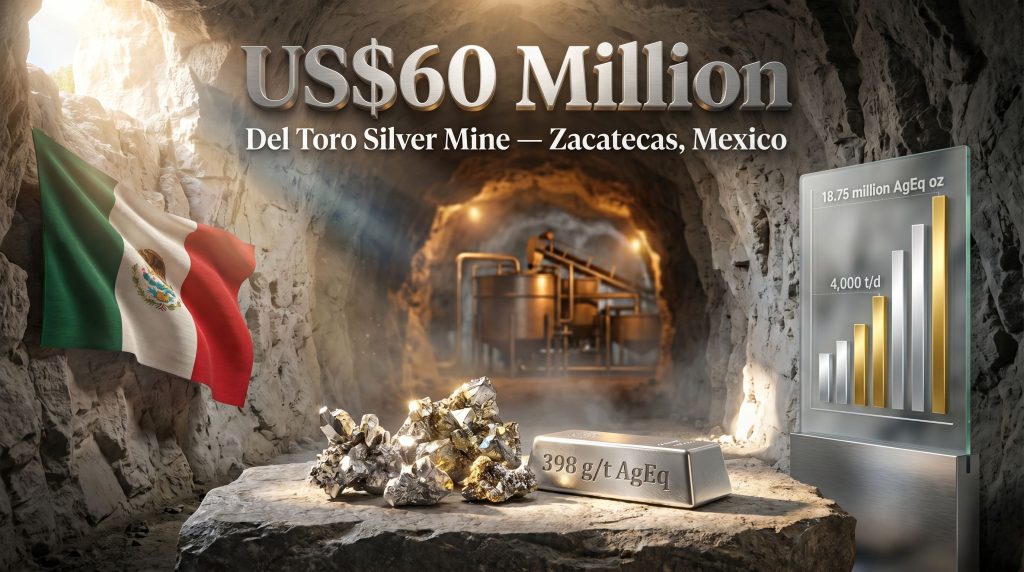

The Sierra Madre acquisition of Del Toro in Mexico is a textbook example of this dynamic playing out in real time. Completed on June 22, 2026, the transaction saw Sierra Madre Gold and Silver Ltd. take ownership of the Del Toro Silver Mine in Zacatecas State from First Majestic Silver Corp. for total consideration of up to US$60 million. Understanding why this deal matters requires looking well beyond the headline price tag.

When big ASX news breaks, our subscribers know first

Breaking Down the Del Toro Deal Structure

The architecture of this transaction is arguably more instructive than the asset itself. Rather than a straightforward cash acquisition, the deal deploys a layered payment structure that distributes financial risk across time and operational performance. Furthermore, these mining consolidation trends are increasingly shaping how junior producers approach growth without overextending their balance sheets.

| Payment Component | Amount | Timing and Conditions |

|---|---|---|

| Cash at Closing | US$20 million | Paid June 22, 2026 |

| Equity Consideration | 10.87 million shares at US$1.30/share (~US$14.1 million) | Issued to First Majestic at closing |

| Deferred Payment | US$10 million | Due within 18 months of closing |

| Milestone Payment 1 | US$10 million | Triggered if a technical report confirms 100 million+ AgEq oz resources within 48 months |

| Milestone Payment 2 | US$10 million | Triggered if commercial production reaches 4,000 t/d for 30 consecutive days within 60 months |

The milestone-linked components are particularly worth examining. Both contingent payments are tied directly to Del Toro's operational and geological performance, which effectively transforms First Majestic into a stakeholder with an ongoing interest in the project's success. If neither milestone is achieved, Sierra Madre's total acquisition cost reduces to approximately US$44 million in cash and equity, a meaningful difference when evaluating downside scenarios.

This kind of earn-out architecture has become increasingly standard in junior mining mergers and acquisitions. It allows buyers to price in optionality rather than paying a premium for potential that may or may not materialise, while giving sellers exposure to upside they would otherwise forgo through an outright sale.

The transaction also required antitrust clearance from COFECE, Mexico's Federal Economic Competition Commission, alongside shareholder approval from Sierra Madre's investor base. Both approvals were secured before the June 22 closing date, which signals a clean regulatory pathway and meaningful shareholder conviction in the company's stated growth thesis.

What Sierra Madre Actually Acquired: A Technical Profile of Del Toro

Del Toro is not a speculative exploration asset. It is a fully permitted, past-producing underground mine with documented operational history spanning 2013 to 2019, sitting within the Chalchihuites District of Zacatecas State, one of Mexico's most historically significant silver-producing corridors.

The property encompasses 2,129 hectares and includes three permitted underground mine portals alongside an operational 3,000 tonne per day flotation processing circuit. The presence of this infrastructure cannot be overstated from a capital efficiency perspective. Constructing a comparable processing facility from scratch in Mexico today would cost multiples of what Sierra Madre paid for the entire asset.

Current Mineral Resource Inventory

| Resource Category | Tonnes | Grade (AgEq g/t) | Estimated AgEq Ounces |

|---|---|---|---|

| Measured and Indicated (Historical) | 592,000 t | 398 g/t | ~7.57 million oz |

| Inferred (Historical) | 1.19 million t | 293 g/t | ~11.18 million oz |

| Combined Total | ~1.78 million t | n/a | ~18.75 million oz |

Important disclaimer: These figures represent historical mineral resource estimates that have not been verified or restated under current NI 43-101 or equivalent modern resource classification standards. They should not be treated as current resource declarations. Sierra Madre's planned definitive feasibility study and technical report, due within 48 months of closing, will seek to update and potentially expand these estimates under contemporary frameworks.

The 398 g/t AgEq grade recorded in the Measured and Indicated category is notably high by global comparison. For context, the average silver grade at primary silver mines globally has been declining for decades as higher-grade deposits are progressively mined out. Assets capable of delivering near-400 g/t silver-equivalent mineralisation from proven underground vein systems are increasingly difficult to find at any price, let alone within a permitted, infrastructure-equipped package.

The polymetallic nature of Del Toro is another underappreciated characteristic. The silver-gold-lead mineralisation profile means the operation generates multiple revenue streams simultaneously. Lead credits in particular can materially reduce net unit production costs when processing high-grade polymetallic ore, improving project economics at silver prices that might otherwise make a pure silver operation marginal.

The Chalchihuites District Advantage: Geology and Geography Working Together

Zacatecas State accounts for a disproportionate share of Mexico's silver output relative to its geographic footprint. The state's geological architecture, dominated by low-sulphidation epithermal vein systems formed through ancient hydrothermal activity, consistently produces the high-grade silver-gold-lead mineralisation that makes underground narrow-vein mining economically viable.

What makes the Chalchihuites District specifically compelling for Sierra Madre is not just Del Toro in isolation, but what it represents alongside the company's existing La Guitarra Mine, also acquired from First Majestic Silver Corp. The two assets sit within the same district, creating conditions for:

- Shared technical teams across both operations

- Consolidated equipment procurement and maintenance contracts

- Potential integration of processing logistics at scale

- A unified community relations and environmental management framework

Sierra Madre's Twin-Asset Framework at a Glance

| Factor | La Guitarra | Del Toro |

|---|---|---|

| Previous Owner | First Majestic Silver Corp. | First Majestic Silver Corp. |

| Operational Status | Active, expansion underway | Restart phase, mid-2027 target |

| Processing Capacity | Expanding toward doubled throughput by mid-2027 | 3,000 t/d flotation circuit in place |

| Primary Metals | Silver, Gold | Silver, Gold, Lead |

| District | Chalchihuites, Zacatecas | Chalchihuites, Zacatecas |

The fact that both assets were acquired from the same vendor is strategically significant. Sierra Madre's technical teams will have already developed familiarity with First Majestic's operational data, geological models, and infrastructure documentation during the La Guitarra integration. This institutional knowledge transfer reduces the learning curve at Del Toro considerably, a factor that rarely appears in project economics but meaningfully compresses restart timelines in practice.

Del Toro's Restart Roadmap: From Rehabilitation to Commercial Production

Restarting an underground mine that has been idle since 2019 is a more complex undertaking than activating a surface operation. Underground environments evolve during periods of inactivity. Ground conditions shift, ventilation systems degrade, water infiltration can alter stope geometries, and equipment left underground requires significant refurbishment before it is fit for purpose again. Sierra Madre's staged restart timeline reflects this reality.

- 2026 (Post-Acquisition): Site assessment, environmental baseline updates, underground condition mapping, and preliminary rehabilitation planning across all three portals

- Mid-2027: Formal mine restart commences, covering portal rehabilitation, ventilation system upgrades, and processing plant recommissioning

- Mid-2028: First production targeted from the recommissioned underground workings

- Within 48 Months of Closing: Delivery of an updated technical resource report targeting a minimum of 100 million AgEq ounces to trigger the first milestone payment

- Within 60 Months of Closing: Scaling to 4,000 tonnes per day of commercial production for 30 consecutive days to trigger the second milestone payment

Risk note for investors: The gap between mid-2027 (restart initiation) and mid-2028 (first production) reflects a deliberately conservative engineering timeline rather than an aggressive ramp-up assumption. Geotechnical variables in underground mines idle for six-plus years can be significant, and any acceleration of the rehabilitation schedule carries meaningful technical risk. Investors should monitor quarterly operational updates for any revisions to these timelines.

The 100 million AgEq oz resource milestone deserves particular scrutiny. Against a current historical resource base of approximately 18.75 million AgEq oz, this target implies a greater than fivefold increase in the mineral inventory. Achieving this would require either the discovery of substantially new mineralised zones within the 2,129-hectare concession boundary or a significant reclassification of currently uncategorised material identified through historical drilling campaigns. Investors interested in interpreting drill results from upcoming exploration programmes at Del Toro will find this milestone a useful benchmark against which to measure early-stage progress.

It is not an unreasonable target given the Chalchihuites District's documented geological productivity, but it is unambiguously ambitious. Investors should treat it as an exploration objective rather than a near-term certainty.

Silver Market Fundamentals: Why Del Toro's Timing May Be Fortuitous

The broader silver market context matters when evaluating any new production-stage project. Unlike gold, silver's dual demand as both a monetary asset and an industrial commodity has fundamentally changed the supply-demand calculus over the past decade. Consequently, understanding silver's dual demand profile is essential context for any investor assessing the long-term case for a project like Del Toro.

Key structural demand drivers now include:

- Solar photovoltaic manufacturing: Silver paste is a critical component in solar cell production, and global solar installation targets across multiple major economies are driving sustained demand growth

- Electric vehicle architecture: Silver is used extensively in EV electrical systems, connectors, and power management components

- Electronics and semiconductors: The push toward miniaturised, high-performance electronics continues to expand silver's industrial consumption base

- Antimicrobial applications: Medical and consumer product applications for silver's antibacterial properties represent a smaller but growing demand category

Against this demand profile, global primary silver mine supply has faced structural headwinds. Declining grades at mature operations, deferred capital investment during periods of price weakness, and the complexity of permitting in mining new project development have all constrained supply response. Assets like Del Toro, offering high historical grades, permitted status, and existing processing infrastructure, occupy a genuinely scarce position in the current project pipeline.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways for Sierra Madre Post-Acquisition

Investors evaluating the Sierra Madre acquisition of Del Toro should think in scenarios rather than point estimates. The milestone-linked deal structure creates materially different outcomes depending on execution quality.

Bull Case: Full Milestone Achievement

Both milestone payments are triggered within their respective windows. La Guitarra's expansion completes on schedule, and Del Toro reaches 4,000 t/d commercial production by late 2031. Sierra Madre consolidates as a meaningful two-mine producer in the Chalchihuites District, with total acquisition cost of US$60 million justified by the scale of the combined operation.

Base Case: Partial Execution

Del Toro restarts on schedule and contributes meaningful production, but the 100 million AgEq oz resource milestone is not achieved within 48 months. Sierra Madre operates profitably across both mines without triggering contingent payments. Total acquisition cost settles at approximately US$44 million.

Bear Case: Execution Delay

Underground rehabilitation at Del Toro encounters geotechnical or community relations complications, pushing first production beyond mid-2028. Silver price weakness reduces the urgency of capital deployment. Milestone windows expire without triggering, capping acquisition cost at US$44 million but delivering lower-than-anticipated production growth.

Key Risk Factors for Investor Monitoring

- Underground condition risk: Six years of inactivity creates genuine uncertainty around ground stability and equipment serviceability across all three portals

- Resource verification risk: Historical estimates require formal NI 43-101 validation before they can be relied upon for investment decisions

- Restart capital risk: The total capital required to recommission Del Toro has not been publicly quantified. Until a restart capital estimate is released, the full investment case cannot be properly stress-tested

- Commodity price sensitivity: Project economics and milestone timeline incentives are directly linked to silver price levels. A sustained period of silver price weakness could alter the calculus around capital prioritisation between the two mines

- Regulatory and community relations risk: Mexican mining operations are subject to evolving community consultation requirements, and maintaining constructive relationships with local stakeholders in the Chalchihuites District will be a critical operational variable

What This Transaction Signals for Latin American Mining M&A

The Sierra Madre acquisition of Del Toro in Mexico reflects a broader pattern reshaping junior mining deal-making across Latin America. Senior producers like First Majestic are rationalising portfolios to concentrate capital on flagship assets, creating a supply of permitted, infrastructure-equipped properties at prices that genuinely reflect the current operating environment rather than peak-cycle valuations. According to the official closing announcement, the transaction was structured to align incentives across both parties through its milestone-based payment architecture.

For well-capitalised juniors with proven management teams and existing operational presence in relevant jurisdictions, this creates a repeatable acquisition model. Sierra Madre has now executed this approach twice with the same vendor, demonstrating both the availability of suitable assets and the company's capacity to identify and close on them. Industry observers at Mining Weekly have noted that this type of disciplined, milestone-linked deal structure is gaining wider traction as juniors seek to limit acquisition risk while maintaining meaningful upside exposure.

The key insight for investors is that the value creation thesis here is not primarily geological. It is operational and financial. The ability to acquire proven infrastructure below replacement cost, apply a performance-linked payment structure that limits downside exposure, and leverage existing district knowledge across two proximate assets represents a capital allocation discipline that sophisticated mining investors increasingly reward.

This article contains forward-looking statements and scenario projections based on publicly available information. Mineral resource figures cited are historical estimates and have not been verified under current classification standards. Nothing in this article constitutes financial advice. Investors should conduct their own due diligence and consult qualified advisers before making investment decisions related to any mining company or project discussed herein.

Want to Catch the Next Major ASX Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex mineral data into actionable insights for both short-term traders and long-term investors — explore historic examples of exceptional discovery returns or start your 14-day free trial today to position yourself ahead of the market.