June 25, 2026

Why Silver's Geography Matters More Than Its Price

Most investors tracking precious metals focus almost exclusively on commodity price movements, treating silver and gold as interchangeable financial instruments. Yet the most consequential variable in long-term precious metals supply is not the spot price trading on the COMEX — it is the geological and jurisdictional concentration of where these metals physically exist in the earth's crust. Understanding that dynamic begins with one country more than any other.

Mexico sits at the apex of global silver production, responsible for roughly 23–25% of the world's annual silver supply. That statistic alone would make it strategically significant, but the country's importance extends well beyond raw output volume. Mexico is simultaneously home to some of the world's largest undeveloped precious metals reserves, a deepening pipeline of the largest gold and silver projects, and an evolving regulatory landscape that is reshaping how capital flows into the sector. For investors, miners, and analysts tracking the largest gold and silver projects in Mexico, the picture in 2025 and 2026 is both compelling and complex.

When big ASX news breaks, our subscribers know first

How Mexico's Mining Landscape Is Structured — And Why It Matters

The Three-Tier Operator Framework

Mexico's precious metals sector does not operate as a uniform market. Understanding which tier a project occupies determines its risk profile, capital requirements, and time horizon to cash generation. Furthermore, mineral deposit tiers directly influence the valuation methodologies applied by institutional investors.

- Tier 1 — Operating Producers: Large-scale mines generating tens of millions of silver-equivalent ounces annually, with established processing infrastructure, long reserve lives, and predictable free cash flow generation.

- Tier 2 — Development Assets: Projects with defined mineral reserves or resources that have either received permits or are progressing through feasibility and environmental review. These carry construction risk and capital intensity but offer the highest upside relative to current valuation.

- Tier 3 — Exploration-Stage Assets: Early-stage prospects where resource definition is incomplete. Return potential is highest in absolute terms, but execution risk and timeline uncertainty are equally elevated.

The distinction between measured and indicated resources (geologically confirmed but not yet economically committed) and proven and probable reserves (the subset converted through feasibility studies into mineable material at a defined cost) is critical for investors evaluating development-stage assets. Mexico's pipeline contains projects at every stage of this conversion process.

The Mineral Belt Geography: Zacatecas, Chihuahua, and Beyond

The Sierra Madre Occidental mineral belt running through northwestern Mexico contains the geological foundation of the country's precious metals dominance. This north-south trending volcanic arc hosts the epithermal and skarn deposit types responsible for Mexico's highest-grade silver and gold mineralisation.

- Zacatecas hosts the greatest concentration of world-class silver operations, including four of Mexico's five largest producing silver mines within a relatively compact geographic area — creating infrastructure synergies that meaningfully reduce per-ounce operating costs.

- Chihuahua is home to Mexico's largest undeveloped polymetallic reserves and has emerged as the primary frontier for the next generation of large-scale silver-gold projects.

- Durango and Sinaloa represent secondary corridors where established mining districts are generating renewed interest as elevated commodity prices improve project economics at deposits previously considered marginal.

A less widely appreciated geological fact is that Mexico's most economically significant deposits are predominantly intermediate sulfidation epithermal systems — a deposit type that forms from hydrothermal fluids at moderate temperatures and depths, typically producing bonanza-grade silver veins interspersed with lower-grade bulk tonnage material. This structural duality is why so many Mexican silver mines combine high-grade underground stopes with lower-grade open pit ore bodies, requiring sophisticated blending strategies to optimise mill feed grades.

The Five Largest Producing Silver Mines in Mexico Right Now

The following table presents verified 2023 production data for Mexico's five highest-output silver operations — the backbone of the country's global supply dominance.

| Rank | Mine | State | Operator | 2023 Silver Output | Mining Method |

|---|---|---|---|---|---|

| #1 | Peñasquito | Zacatecas | Newmont | 20.68 million oz | Open pit |

| #2 | Juanicipio | Zacatecas | Industrias Peñoles | 14.89 million oz | Underground |

| #3 | San Julian | Chihuahua | Industrias Peñoles | 13.59 million oz | Underground |

| #4 | Fresnillo | Zacatecas | Industrias Peñoles | 13.32 million oz | Underground |

| #5 | Saucito | Zacatecas | Industrias Peñoles | 11.60 million oz | Underground |

Peñasquito — Mexico's Most Strategically Important Precious Metals Asset

The Peñasquito mine occupies a unique position in global mining: it is simultaneously Mexico's largest gold mine and one of the world's top-ranked silver producers by annual output. Operated by Newmont following its 2019 acquisition of Goldcorp, Peñasquito contains 1.7 million ounces of gold and 195.1 million ounces of silver in total resources — figures that place it in rare company globally.

What makes Peñasquito particularly instructive as a case study is its polymetallic revenue architecture. The mine produces not only gold and silver but also significant volumes of zinc and lead, which function as margin-enhancing byproduct credits that materially reduce the all-in sustaining cost (AISC) per gold-equivalent ounce. In a market environment where cost discipline separates tier-one operators from the rest, Peñasquito's multi-commodity revenue stream provides a structural cost advantage that single-metal mines cannot replicate.

A critical but underappreciated aspect of polymetallic silver-gold deposits like Peñasquito is that byproduct credit volatility — driven by zinc and lead price cycles — can swing net AISC by US$150–250 per gold-equivalent ounce in either direction. This makes commodity correlation analysis essential for accurate project-level financial modelling.

The Peñoles Dominance Factor

Industrias Peñoles, Mexico's domestically listed mining giant, controls four of the country's five largest silver-producing mines. This concentration is not a coincidence — it reflects decades of systematic acquisition, exploration, and vertical integration across the Zacatecas silver district. Peñoles' integrated model, combining mine production with downstream smelting and refining through its Met-Mex Peñoles subsidiary, creates cost efficiencies and margin capture that pure-play miners cannot easily replicate.

The Juanicipio mine, which delivered 14.89 million ounces of silver in 2023, benefits directly from its proximity to the Fresnillo district's established processing infrastructure. The operational integration between Juanicipio and the legacy Fresnillo mine reduces trucking distances, shared overhead costs, and concentrate handling expenses — a network effect that inflates the economic returns of adjacent assets beyond what standalone project economics would suggest.

The Largest Undeveloped Gold and Silver Projects in Mexico

Cordero, Chihuahua — A Reserve Base of Global Significance

The Cordero project, located in Chihuahua state, represents one of the most significant undeveloped silver deposits anywhere on earth. Its polymetallic profile — combining silver with substantial gold, lead, and zinc resources — positions it as a potential future anchor for Mexico's silver supply growth. Projects of this scale require initial capital commitments in the hundreds of millions to multiple billions of dollars, long permitting timelines, and careful navigation of community consultation requirements before construction can commence.

The critical investment consideration for Cordero is the relationship between resource conversion rate and capital intensity. The project's size means that even at partial production capacity, its contribution to the largest gold and silver projects in Mexico would be material — which is precisely why its feasibility study progression is one of the sector's most watched development milestones.

Media Luna, Guerrero — Mexico's Most Capital-Significant Gold Development

Torex Gold Resources' Media Luna project represents a fundamentally different risk-return profile than Cordero. Where Cordero is a bulk-tonnage polymetallic system, Media Luna is a higher-grade gold-dominant deposit within a broader mining district that Torex has operated for years through its existing Morelos complex.

The project is part of a broader US$3.4 billion gold investment cluster in Mexico and is advancing through its construction and ramp-up phase in 2025–2026. Media Luna's underground mine design targets a high-grade gold-silver-copper orebody using methods that differ from the large-scale open pit approach used at Morelos — requiring a parallel operational capability build within the same management team.

Additional Development Assets Reshaping Mexico's Pipeline

Several other projects round out Mexico's development-stage pipeline:

- Plomosas, Sinaloa: Situated within the historically productive Rosario Mining District, this asset benefits from access to established regional infrastructure while offering resource growth potential through systematic exploration of its silver-gold system.

- La Guitarra, Temascaltepec: An intermediate sulfidation epithermal silver-gold vein system operated by Sierra Madre Gold and Silver, currently in production ramp-up. The vein system continuity makes it a candidate for resource expansion through underground definition drilling — a lower-cost growth pathway compared to greenfields exploration.

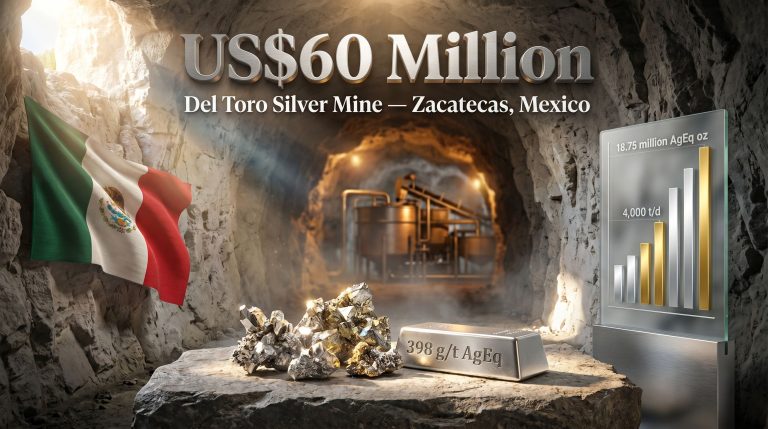

- Del Toro, Zacatecas: A three-mine underground complex with an integrated 3,000 tonnes per day (TPD) flotation processing plant. The existing processing infrastructure represents a significant embedded asset value, as constructing equivalent capacity from scratch would cost multiples of its current implied valuation in acquisition scenarios.

Operating vs. Development: The Investment Metrics Divide

| Metric | Operating Tier-1 Mines | Development-Stage Projects |

|---|---|---|

| Annual Silver Output | 11–21 million oz | Pre-production |

| Capital Intensity | Sustaining capex only | US$500M to US$2B+ |

| Revenue Certainty | High (current cashflow) | Low (construction risk) |

| Reserve Life | 10–25+ years | Feasibility-dependent |

| Permitting Risk | Low | Moderate to High |

| Polymetallic Revenue | Yes (zinc, lead, copper) | Yes (gold, lead, zinc) |

One structural insight that is not always apparent from headline production figures: Mexico's development pipeline is predominantly underground in its mine design orientation. This reflects the geological character of Mexico's undeveloped silver-gold orebodies — they tend to be higher-grade, narrower vein or manto systems that are not economically suited to bulk open pit extraction.

Underground operations carry higher capital intensity per tonne of ore processed but generate superior grade profiles and smaller surface disturbance footprints, both of which matter increasingly in Mexico's current social and regulatory environment. Indeed, silver's dual role as both a monetary metal and industrial input makes supply chain security from these underground systems increasingly critical to global markets.

Mexico's Regulatory Landscape: The Variable That Overrides Everything Else

Mining Law Reforms and Their Capital Consequences

The 2022–2023 reforms to Mexico's mining legislation introduced material changes to concession renewal processes, water use permit requirements, and the scope of community consultation obligations. These changes have extended the regulatory timeline for development projects and introduced uncertainty around the long-term security of existing concession tenure — a critical variable for miners evaluating multi-decade capital commitments.

Mexico's permitting architecture involves multiple federal agencies including SEMARNAT (the environmental regulator) and the DGMR (the mining directorate), alongside state-level processes. The interaction between these layers creates a complex approval pathway that experienced operators navigate more efficiently than new entrants. In addition, definitive feasibility studies must now account for these extended timelines when modelling project NPV.

Social Licence: The Non-Negotiable Approval

Under Mexico's constitutional framework and obligations under ILO Convention 169, projects affecting indigenous communities require free, prior, and informed consent processes that go beyond standard public consultation. The practical consequence is that social licence timelines can extend project development schedules by two to five years in contested areas. Consequently, indigenous consultation requirements — while framed differently across jurisdictions — reflect a global shift in how mining projects must engage with host communities. This risk does not appear in technical feasibility studies but can dwarf permitting timelines in its impact on project NPV.

Taxation Structure Compared to Peer Jurisdictions

| Jurisdiction | Special Mining Duty | Precious Metals Royalty |

|---|---|---|

| Mexico | 7.5% | 0.5% |

| Peru | 1–12% (sliding scale) | 1–3% |

| Chile | 5–14% (new framework) | N/A (separate regime) |

| Canada | Provincial (varies) | Minimal at federal level |

Mexico's royalty structure is relatively competitive at the 0.5% precious metals extraction royalty level, though the combined tax burden including the special mining duty requires careful modelling at the project feasibility stage to accurately assess post-tax returns.

The next major ASX story will hit our subscribers first

The US$8.4 Billion Pipeline: Translating Capital Into Production Capacity

The combined capital value of Mexico's top ten gold and silver projects entering the development or construction phase totals approximately US$8.4 billion. To contextualise that figure: it represents one of the largest concentrated precious metals investment cycles in Mexico's modern mining history. Three scenarios frame the range of outcomes for this capital deployment:

- Base Case: Regulatory stability holds, existing projects advance on modified schedules, and Mexico grows gold output by 15–20% over the decade while maintaining silver production leadership above 190 million ounces annually.

- Upside Case: Legislative clarification attracts renewed foreign direct investment, accelerating development timelines for assets like Cordero and improving Mexico's share of incremental global silver supply during a period of sustained high commodity prices.

- Downside Case: Stricter concession controls and expanded community consultation requirements delay multiple projects simultaneously, compressing the supply growth trajectory and pushing marginal capital toward lower-risk jurisdictions like Canada and Australia.

Mexico's precious metals pipeline presents asymmetric upside in a sustained elevated commodity price environment. However, the regulatory reform cycle, social licence complexity, and capital intensity of its largest development projects require investors to apply meaningful discount rates to development-stage asset valuations. The geological quality of assets like Cordero and Media Luna is not in question — the execution pathway is.

Frequently Asked Questions: Mexico's Gold and Silver Mining Sector

What is the largest gold mine in Mexico?

The Peñasquito mine in Zacatecas, operated by Newmont, holds this distinction — containing 1.7 million ounces of gold in resources alongside 195.1 million ounces of silver, making it a dual-category leader among the largest gold and silver projects in Mexico.

Which company dominates silver production in Mexico?

Industrias Peñoles controls four of Mexico's five largest silver-producing mines — Juanicipio, San Julian, Fresnillo, and Saucito — and operates an integrated downstream refining business through Met-Mex Peñoles.

How much silver does Mexico produce annually?

Mexico consistently produces between 190 and 220 million ounces of silver per year, representing approximately one-quarter of total global annual supply.

What is the largest undeveloped silver project in Mexico?

The Cordero project in Chihuahua is widely regarded among industry analysts as one of the world's largest undeveloped silver deposits, supported by significant gold, lead, and zinc co-product resources.

Is Mexico considered a safe mining investment jurisdiction?

Mexico offers exceptional geological endowment across the Sierra Madre Occidental mineral belt, but investors must carefully evaluate concession tenure security, evolving water use regulations, community consultation obligations, and state-level social licence dynamics before committing capital — particularly for development-stage assets in areas with indigenous community presence.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Forward-looking statements, scenario projections, and production forecasts involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent due diligence and consult qualified financial advisers before making investment decisions.

Want to Capitalise on the Next Major Precious Metals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly converting complex mineral data across 30+ commodities into clear, actionable investment insights — so subscribers identify significant silver, gold, and polymetallic discoveries the moment they hit the exchange. Explore how historic mineral discoveries have delivered exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.