June 12, 2026

When Governments Become Competitors: Kazakhstan's Shifting Rules for Critical Mineral Investment

There is a pattern that repeats itself across the history of resource-rich nations: once a commodity becomes indispensable to global industrial systems, the state's appetite for a larger share of the proceeds grows accordingly. The question is rarely whether this renegotiation happens, but how it happens, and whether the process is managed with enough transparency to preserve investor confidence. Kazakhstan critical mineral state control is now at precisely this inflection point, and the decisions made in Astana over the next several years will have consequences far beyond its own borders.

When big ASX news breaks, our subscribers know first

Kazakhstan's Position in the Global Critical Minerals Race

Few countries occupy as strategically complex a position in the global critical mineral supply chain as Kazakhstan. The country holds 17 minerals appearing on the U.S. Department of Energy's Critical Minerals List, a figure that immediately positions it as a priority jurisdiction for any Western government seeking to reduce dependence on Chinese-controlled processing and supply networks. Furthermore, the critical minerals demand surge globally is only intensifying the spotlight on Kazakhstan's resource base.

Why Uranium Makes Kazakhstan Unmissable

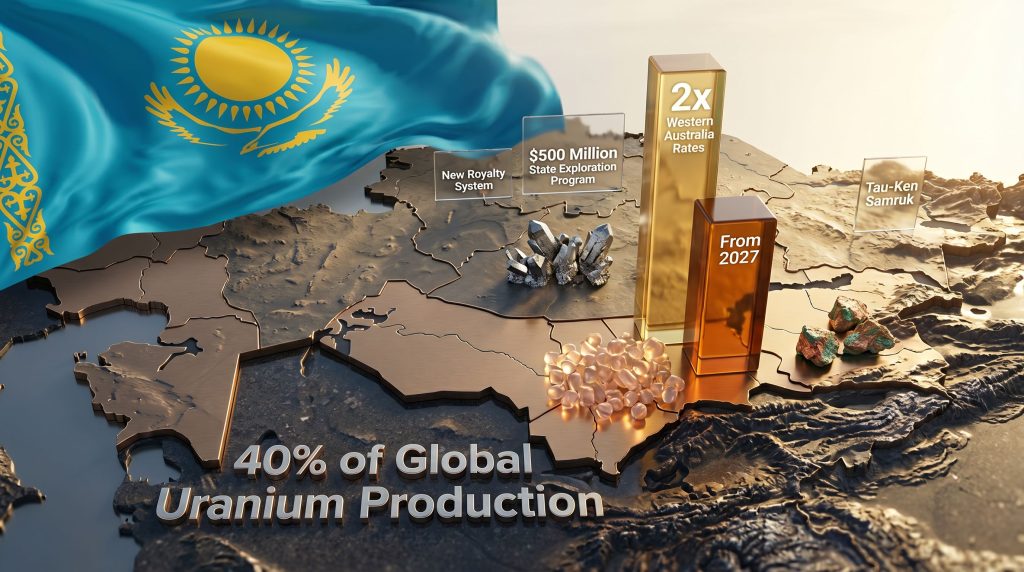

The uranium dimension alone makes Kazakhstan impossible to ignore. The country accounts for approximately 40% of global primary uranium production, according to the World Nuclear Association, making Kazatomprom the single most consequential uranium producer on the planet at a time when nuclear energy is experiencing a genuine commercial renaissance. In addition, substantial deposits of tungsten, copper, and materials adjacent to the rare earth category are attracting intensifying interest from Western industrial and defence supply chains.

Kazakhstan's geographic reality adds another layer of complexity. Positioned between Russia and China, with significant existing commercial ties to both, the country simultaneously finds itself being courted aggressively by the United States and European Union member states. This tripartite dynamic is not merely a geopolitical curiosity; it is the structural context within which every regulatory decision in the mining sector must be understood.

The 2018 Reforms and the Investment Wave They Unleashed

To understand the current regulatory environment, it is necessary to revisit the policy architecture that preceded it. Kazakhstan's 2018 amendments to its sub-soil use and mining laws represented a genuine break from Soviet-era governance patterns. The reforms introduced a first-come-first-served licensing model, systematically reduced bureaucratic barriers to entry, and signalled a market-oriented philosophy toward resource development.

The response from Western capital was significant. Mining companies from Canada, the United Kingdom, Australia, and the United States established or expanded operations across multiple commodity categories. First Quantum Minerals, the Canadian mining firm, has specifically cited the 2018 reforms as the catalyst for its decision to investigate Kazakhstan as an investment destination, according to reporting by Eurasianet (April 2026). However, that foundation is now being modified in ways that are raising questions about whether those conditions will persist.

Kazakhstan Critical Mineral State Control: A Multi-Instrument Policy Progression

What Kazakhstan is doing is not a single legislative event. Kazakhstan critical mineral state control is being asserted through a layered set of policy instruments that have accumulated incrementally since approximately 2023, each individually defensible, but collectively representing a meaningful shift in the risk profile of the jurisdiction.

| Policy Instrument | Key Detail | Investor Implication |

|---|---|---|

| New Royalty System | Applies only to operations licensed from 2027 onward | Grandfathers existing operations but raises cost baseline for new entrants |

| Royalty Rate Level | Reportedly double the rates applied in Western Australia | Places Kazakhstan at the higher end of the global fiscal spectrum |

| Gold, Silver & Uranium Tax Increases | Upward revisions implemented alongside rising commodity prices | Increases operating cost burden on existing mines |

| State Exploration Program | $500 million allocated for exploration of 20 projects (announced February 2025) | Positions the government as a direct competitor to private explorers |

| Priority Licensing Reintroduction | Preferential access for companies committing to in-country processing | Replaces the competitive 2018 first-come-first-served model |

| Tau-Ken Samruk First-Right Discussions | Parliamentary discussions on state mining company pre-emption rights | Introduces potential state veto over private license applications |

The royalty rate comparison is particularly significant from an investment modelling perspective. Maxim Kononov, First Deputy Director of the Republican Association of Mining and Metallurgical Enterprises, stated at a Minex Kazakhstan panel on April 16, 2026, that the overall direction of policy represented an unambiguous increase in the budgetary tax burden on the sector. His assessment of royalty rates relative to Western Australia provides a concrete benchmark that investors can use when modelling comparative project economics.

Western Australia's royalty rates are widely regarded across the international mining industry as a competitive benchmark. If Kazakhstan's new framework sits at double that rate for comparable minerals, it moves the country from the lower-cost tier of emerging jurisdictions into a category that requires higher commodity prices or exceptional deposit quality to justify investment.

The Uranium Sector as a Policy Template

The government's 2024 decision to effectively ring-fence the uranium sector for state-owned Kazatomprom deserves analysis that goes beyond its immediate commercial implications. Kazakhstan uranium dominance is not merely the most commercially significant mineral story Kazakhstan produces; it is the sector where the government has most clearly demonstrated its willingness to prioritise state control over market competition when strategic value reaches a certain threshold.

The mechanism is instructive. As global nuclear energy demand accelerated and uranium prices responded, the commercial and strategic importance of the sector increased simultaneously. The government's response was consolidation rather than liberalisation, using Kazatomprom as the instrument of state capture. Consequently, the question that several industry participants have begun asking, quietly but with increasing urgency, is whether uranium represents a template that will be applied to other critical minerals as their own strategic value increases.

Tungsten, copper, and rare earth-adjacent materials are all subject to intensifying Western demand. If the government perceives that Western desperation for supply chain diversification gives it sufficient leverage, the uranium model could become a blueprint rather than an exception. Indeed, the broader geopolitical mining landscape suggests this pattern is not unique to Kazakhstan.

Forum Voices: Three Readings of the Same Regulatory Landscape

The Minex Kazakhstan '26 forum held in Astana in mid-April 2026 provided an unusually concentrated snapshot of how different stakeholder groups are processing the same policy environment. Three distinct interpretive frameworks emerged from the event.

1. Pragmatic Acceptance

Ruslan Baimishev, President of the Kazakhstan Chamber of Mines, characterised the current framework as a workable equilibrium. His position acknowledged that gold and silver tax increases reflect genuinely elevated global commodity prices and are therefore commercially rational adjustments. On royalties, he argued that when the full tax architecture is considered holistically rather than in isolation, the overall burden remains within a reasonable range.

The chamber did oppose the reintroduction of licensing priorities, but Baimishev noted that new procedural safeguards, specifically requirements for prime ministerial and presidential sign-off on priority licensing decisions, provide a meaningful degree of investor protection.

2. Cautious Concern

James Banyard, Exploration Manager at First Quantum Minerals, offered a more nuanced reading. He acknowledged that the government had demonstrated receptiveness to industry feedback and that the changes had not yet directly affected his company's investment decisions. However, he identified the government's move into direct mineral exploration as particularly significant, arguing that it effectively positions the state as a competitor to private sector operators.

He described the situation as raising red flags without yet constituting a crisis, a distinction that matters enormously for capital allocation decisions.

3. Structural Alarm

The most pointed concerns came from Timur Odilov, an Astana-based lawyer directly involved in drafting the 2018 reforms. His assessment was that the systematic erosion of that framework risks repositioning Kazakhstan as a non-transparent jurisdiction in the eyes of international capital markets. He specifically noted that it is competitive private sector activity, not government-directed exploration, that has historically been responsible for the major mineral discoveries that transform a country's resource base.

Sally Axworthy, the British Ambassador to Kazakhstan, captured the diplomatic community's position with careful precision during a panel discussion on April 15, 2026. Her remarks emphasised the importance of predictable, linear reform processes and specifically called on the government to maintain structured consultation with industry stakeholders before implementing further changes.

The next major ASX story will hit our subscribers first

Comparing Kazakhstan's Fiscal Framework to Global Peers

Understanding where Kazakhstan sits in the global landscape of mining fiscal regimes requires comparative context. The following table provides a structured overview of how the jurisdiction compares to peers competing for similar Western investment flows.

| Jurisdiction | Approximate Royalty Framework | Sovereign Risk Profile | Notes |

|---|---|---|---|

| Kazakhstan (from 2027) | Reportedly 2x Western Australia for comparable minerals | Moderate, trending higher | New framework applies to new licenses only |

| Western Australia | Established competitive benchmark | Low | Widely used as investor baseline |

| Canada (by province) | Generally competitive | Low to moderate | Provincial variation creates complexity |

| Chile | Moderate, recently revised upward | Low to moderate | State increasing take on lithium specifically |

| Democratic Republic of Congo | Variable, frequently higher | High | Sovereign risk premium required |

| Namibia | Moderate | Low to moderate | Emerging jurisdiction with uranium significance |

The royalty rate comparison does not exist in isolation. Investors model total government take, which encompasses royalties, corporate taxes, withholding taxes, and various levies collectively. Even if Kazakhstan's royalty rates are elevated relative to Western Australia, the total fiscal burden depends on how those royalties interact with other components of the tax code.

The Oil Sector Precedent: A Cautionary Data Point for Mining Investors

Resource sector investors evaluating Kazakhstan cannot responsibly ignore what has transpired in the country's oil industry. Kazakhstan has been engaged in extended legal disputes with international oil majors for years. In January 2026, an international arbitration tribunal awarded Kazakhstan billions of dollars from an international consortium in a decision that sent immediate signals through the broader investment community. According to Reuters reporting from February 6, 2026, Shell subsequently announced a pause on further investment in Kazakhstan following the resolution of those legal disputes.

This sequence matters for mining investors for several reasons:

- It demonstrates that Kazakhstan is willing and capable of pursuing aggressive legal and arbitration strategies against international majors when it believes state interests have been inadequately served

- It shows that investment pauses by major Western companies are a real and documented outcome of these disputes, not merely a theoretical risk

- It illustrates contagion dynamics: a dispute resolved in the oil sector created uncertainty that affected investor sentiment across the broader Kazakhstan resource investment environment

- It suggests that the government's confidence in using legal mechanisms to assert state interests may be reinforced by successful outcomes in prior cases

The oil sector precedent is not a reason to categorically avoid Kazakhstan. It is, however, a material risk factor that belongs in any serious investment analysis of Kazakh critical mineral assets.

The Geopolitical Dimension: Why Astana Can Afford to Push Back

A critical insight that is frequently underweighted in investment analyses of Kazakhstan is the degree to which the country's geopolitical positioning gives it structural leverage to pursue resource nationalism without fully alienating any single major power. This mirrors the broader geopolitical minerals race playing out globally as nations compete for resource security.

As James Banyard observed on the sidelines of the Minex forum, the Kazakh government is acutely aware of its position between major powers and is adjusting its approach to reflect that new normal, according to Eurasianet's April 2026 reporting. Kazakhstan has formalised engagement with the United States through a memorandum of understanding on critical minerals cooperation, with active commercial negotiations involving American companies and the country's tungsten sector, assets valued in the billions of dollars. Simultaneously, Chinese commercial partnerships and Russian transit infrastructure relationships remain intact.

Furthermore, the more desperate Western governments become about supply chain security, the stronger Kazakhstan's negotiating position becomes, and the more comfortable Astana feels in pushing the regulatory envelope. This dynamic is well-documented by OilPrice.com in its analysis of how Kazakhstan's critical mineral boom directly collides with state control priorities.

Scenario Analysis: Three Possible Trajectories for Kazakhstan Mining Investment

The following scenarios represent analytical projections based on current observable trends and should not be treated as forecasts or investment advice. Outcomes will depend on factors that cannot be predicted with certainty.

Scenario 1: Managed Equilibrium (Base Case)

The government continues incremental adjustments to the fiscal and licensing framework but maintains sufficient consultation with industry to prevent large-scale capital withdrawal. Higher royalties and state participation are accepted as the price of access to a strategically significant jurisdiction, and Western investment continues at a moderated pace.

Scenario 2: Accelerated State Consolidation (Downside Case)

Parliamentary discussions on Tau-Ken Samruk's priority licensing rights advance into legislation. The government's $500 million exploration programme expands, effectively pre-selecting state-preferred development corridors. Private sector exploration activity contracts as the commercial rationale for early-stage investment diminishes. The uranium sector template is applied to tungsten and copper.

Scenario 3: Geopolitical Realignment (Tail Risk)

A significant deterioration in Western-Kazakhstan diplomatic relations, or a high-profile arbitration loss by a Western mining company, triggers a fundamental reassessment of the jurisdiction's risk profile. Capital flows toward alternative jurisdictions in Africa or Latin America, and Kazakhstan's window for integration into Western-aligned critical mineral supply chains narrows considerably. The Kazakhstan rare earth discovery potential may consequently go unrealised under Western partnership frameworks.

Key Takeaways for Investors and Industry Observers

- Kazakhstan critical mineral state control is being pursued through a deliberate, multi-instrument strategy, not as an isolated or reactive response to market conditions

- The 2018 reforms that catalysed Western investment are being systematically modified; each individual change is manageable, but the cumulative directional trend is unmistakable

- The uranium sector's treatment in 2024 may represent a policy template that is progressively applied to other high-value minerals as their strategic importance increases

- Royalty rates reportedly double those of Western Australia place Kazakhstan at the higher end of the global fiscal spectrum for emerging critical mineral jurisdictions

- The oil sector's arbitration history and Shell's subsequent investment pause provide documented evidence of the real-world consequences of resource disputes in Kazakhstan

- Kazakhstan's position between the United States, China, and Russia gives Astana structural leverage to pursue state participation strategies without fully alienating any single partner, an asymmetry that investors must factor into long-term jurisdiction risk assessments

This article is intended for informational purposes only and does not constitute investment advice. Regulatory environments can change rapidly, and investors should conduct independent due diligence before making any investment decisions related to Kazakhstan's mining sector. Scenario projections represent analytical frameworks, not predictions of specific outcomes.

Want To Stay Ahead Of Major ASX Mineral Discoveries As Critical Mineral Dynamics Shift Globally?

As state control tightens across resource-rich jurisdictions like Kazakhstan, identifying where the next transformative discovery is announced becomes increasingly valuable — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into actionable insights for investors at every experience level. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the broader market.