June 16, 2026

Kazakhstan's critical minerals supply chain represents one of the most significant untapped opportunities in global resource development, yet institutional barriers continue to constrain the nation's transformation from raw material supplier to value-chain participant. Recent developments across the Critical Minerals Strategy landscape highlight the growing urgency for comprehensive supply chain diversification away from Chinese processing dominance.

Why Kazakhstan's Critical Minerals Strategy Could Reshape Global Supply Chains by 2030

Kazakhstan's position in the global critical minerals landscape represents both immense opportunity and strategic risk. Recent analysis reveals that institutional frameworks, not geological endowments, will ultimately determine whether the nation emerges as a supply chain power or remains relegated to raw material supplier status through the next decade.

The Central Asian Resource Advantage vs. Processing Reality Gap

Central Asia collectively holds significant reserves across multiple critical mineral categories, with Kazakhstan serving as the regional anchor due to its established mining infrastructure and geographical positioning. However, current processing capabilities capture less than 30% of extracted value domestically, creating a structural dependency on external refining networks.

The region's existing mining-metals foundation includes major operators such as KAZ Minerals, KazZinc Limited, and Eurasian Resources Group, yet these companies primarily focus on concentrate production rather than downstream value creation. This processing gap represents both the primary constraint and greatest opportunity for supply chain transformation.

Research utilising UN Comtrade and ITC Trade Map data spanning 2015-2023 reveals consistent export growth patterns, with linear forecasting models projecting continued expansion through 2027. However, these projections assume institutional stability and fail to account for potential supply chain disruptions, commodity price volatility, or geopolitical shifts that could fundamentally alter trade flows.

Export Growth Projections Through 2027: What the Numbers Reveal

Statistical analysis of Central Asian mineral exports demonstrates strengthening demand from both Asian and European markets, yet the composition of these exports remains heavily skewed toward raw materials and concentrates. Time-series modelling with residual testing indicates robust growth trajectories, but the methodology's linear assumptions limit predictive accuracy under volatile conditions.

Asian markets, particularly China, continue to dominate import volumes, creating a dependency relationship that undermines supply chain diversification objectives. European demand shows steady growth but remains secondary to Asian flows, reflecting both logistical constraints and limited processing partnerships between Kazakhstan and EU member states.

The forecast models project export value increases of 15-25% annually through 2027, yet this growth primarily reflects volume expansion rather than value-added processing integration. Without strategic intervention, continued export growth paradoxically strengthens external processing dominance rather than building domestic capabilities.

Institutional Barriers That Keep Resources Locked in Raw Form

Licensing transparency and regulatory predictability emerge as fundamental constraints on long-term capital investment in processing infrastructure. International comparative analysis positions Kazakhstan's institutional quality significantly below established mining jurisdictions like Australia and Chile, creating risk premiums that discourage advanced manufacturing investments.

Coordination mechanisms between government agencies and private sector operators remain underdeveloped, resulting in fragmented policy implementation and regulatory uncertainty. This institutional weakness manifests in extended project approval timelines, inconsistent environmental standards, and limited investor protection frameworks.

ESG integration requirements increasingly determine access to international capital markets, yet Kazakhstan's regulatory framework lacks standardised environmental reporting, community engagement protocols, and governance transparency measures. This compliance gap effectively excludes many projects from institutional investor portfolios and development finance institution support.

When big ASX news breaks, our subscribers know first

How Does Kazakhstan's Mineral Endowment Compare to Established Suppliers?

Kazakhstan's critical minerals portfolio positions the nation among global leaders in several strategic categories, yet processing limitations prevent full value capture from these geological advantages. Furthermore, comparative analysis reveals both competitive strengths and structural weaknesses relative to established suppliers.

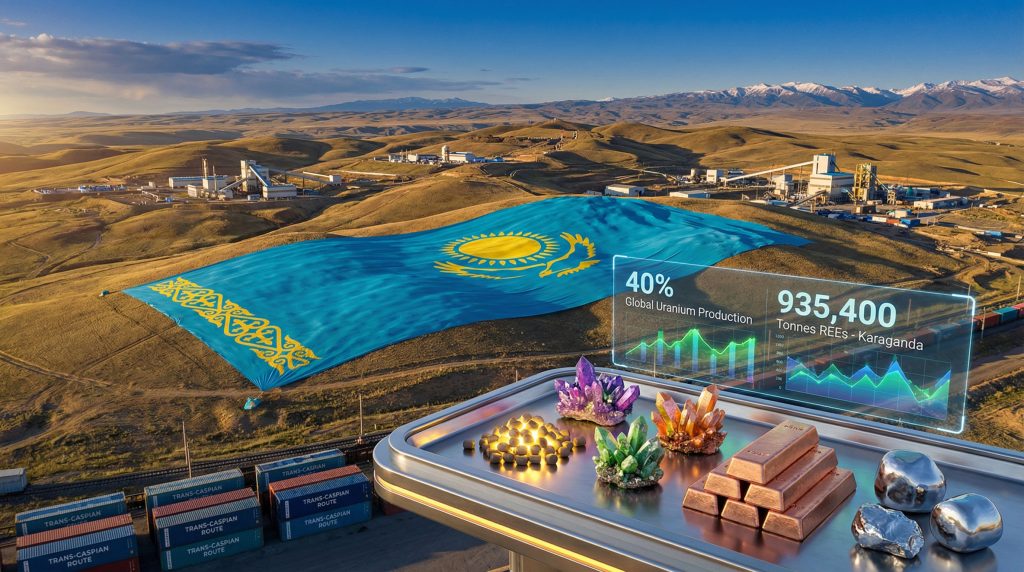

Uranium Dominance: 40% Global Production Share Analysis

Kazakhstan maintains overwhelming leadership in global uranium production, accounting for approximately 40% of world output through operations managed by NAC Kazatomprom and international partners. This dominance stems from favourable geology in the Syr Darya basin and roll-front deposit characteristics that enable low-cost in-situ recovery methods.

Production capacity exceeds 20,000 tonnes annually, positioning Kazakhstan as the indispensable supplier for global nuclear fuel cycles. Unlike competitors in Namibia, Australia, and Canada, Kazakhstan's uranium operations benefit from proximity to conversion facilities operated through partnerships with Russian nuclear industry entities.

However, uranium enrichment capabilities remain limited, requiring export of converted material to external facilities for fuel fabrication. This processing gap prevents Kazakhstan from capturing higher-value segments of the nuclear fuel cycle and maintains dependency on international partnerships for value-added manufacturing, unlike more comprehensive uranium market trends developing elsewhere.

Rare Earth Elements Discovery: 935,400 Tonnes in Karaganda Region

Recent geological surveys in the Karaganda region have identified substantial rare earth element deposits totalling 935,400 tonnes of measured and indicated resources. These discoveries position Kazakhstan as a potential alternative to Chinese rare earth dominance, though development timelines extend well beyond current supply chain pressures.

The identified reserves contain mixed light and heavy rare earth elements, with preliminary analysis suggesting favourable distribution patterns for permanent magnet applications. However, current development status remains in early exploration phases, requiring extensive metallurgical testing and environmental impact assessment before production feasibility can be established.

Processing infrastructure for rare earth separation and purification does not currently exist within Kazakhstan, necessitating either substantial domestic investment or continued reliance on Chinese processing networks. This technological gap represents the critical constraint on rare earth development timelines and strategic value.

Battery Metals Portfolio: Copper, Zinc, and Emerging Lithium Deposits

Kazakhstan's battery metals portfolio spans established copper and zinc operations alongside emerging lithium exploration prospects. KazZinc operations produce approximately 400,000 tonnes of copper annually through the Kounrad smelter complex, while zinc production exceeds one million tonnes across regional facilities.

Lithium exploration in the Mangystau region's Saryesik depression has identified brine deposits with favourable chemistry for extraction, though resource quantification remains preliminary. These deposits represent long-term potential rather than near-term production capacity, requiring extensive development infrastructure and processing technology transfer similar to other battery lithium refinery projects globally.

| Mineral | Kazakhstan Rank | Production Share | Key Deposits | Processing Status |

|---|---|---|---|---|

| Uranium | #1 | 40%+ | Syr Darya Basin | Advanced |

| Chromium | Top 3 | 15%+ | Aktobe | Semi-processed |

| Manganese | Top 5 | 8%+ | Kostanay | Raw export |

| REEs | Emerging | <1% | Karaganda | Exploration |

| Copper | Top 10 | 3%+ | Kounrad | Semi-processed |

| Zinc | Top 8 | 5%+ | Multiple | Semi-processed |

What Strategic Framework Could Transform Kazakhstan from Quarry to Value-Chain Power?

Transforming Kazakhstan's critical minerals sector from raw material extraction to integrated value chain participation requires coordinated institutional reform, infrastructure investment, and strategic partnership development. This transformation framework addresses three fundamental challenges: processing localisation, market diversification, and governance modernisation.

The "Rare Metals Valley" Processing Cluster Concept

Development of a concentrated processing cluster could address fragmented infrastructure and enable economies of scale in advanced manufacturing. The proposed "Rare Metals Valley" concept envisions co-located beneficiation, smelting, and refining facilities that reduce transportation costs and improve supply chain coordination.

Successful processing clusters in Australia's Pilbara region and Chile's Atacama demonstrate the viability of concentrated industrial development around mineral resources. These models require substantial upfront infrastructure investment but generate sustained competitive advantages through operational integration and shared technical expertise.

The cluster approach enables gradual processing sophistication, beginning with basic beneficiation and advancing through pyrometallurgical and hydrometallurgical operations toward high-purity product manufacturing. This evolutionary development path reduces capital risk while building domestic technical capabilities over extended timeframes.

Trans-Caspian Logistics Corridors for Market Diversification

Current export infrastructure heavily favours routing through Chinese and Russian networks, creating strategic vulnerabilities and limiting market access diversification. Trans-Caspian corridor development could enable direct access to European and Middle Eastern markets while reducing dependency on single-route logistics.

The Baku-Tbilisi-Kars Railway provides operational infrastructure for alternative routing, though current capacity utilisation remains below potential due to limited feeder connections and port infrastructure constraints. Seasonal limitations in Caspian Sea maritime transport further complicate year-round logistics reliability.

Strategic corridor development requires coordinated investment across multiple jurisdictions and transport modes, involving Kazakhstan, Azerbaijan, Georgia, and Turkey in comprehensive logistics integration. This multilateral approach complicates project financing but offers substantial strategic benefits through reduced transport vulnerability.

ESG Integration Requirements for International Investment

Environmental, social, and governance standards increasingly determine access to international capital markets and development finance institution support. Kazakhstan's current regulatory framework lacks standardised ESG reporting requirements, community engagement protocols, and environmental monitoring systems demanded by institutional investors.

Implementation of internationally recognised ESG frameworks requires regulatory harmonisation with World Bank Group Performance Standards, International Finance Corporation requirements, and emerging EU due diligence legislation. This compliance infrastructure represents both cost and competitive advantage in accessing patient capital for long-term processing investments.

Community stakeholder engagement protocols must address indigenous rights, local economic participation, and environmental impact mitigation throughout project lifecycles. These social licence requirements extend beyond legal compliance toward sustained community partnership development.

Can Kazakhstan Break Free from China's Processing Monopoly?

China's processing dominance across critical minerals supply chains creates strategic vulnerabilities for Kazakhstan's critical minerals supply chain integration aspirations. Breaking this dependency requires understanding current export flow patterns, processing capacity alternatives, and investment partnership opportunities with Western entities.

Current Export Flow Analysis: Asia vs. Europe Destination Split

Trade flow analysis reveals overwhelming Asian market orientation, with China absorbing approximately 60-70% of Kazakhstan's critical mineral exports across multiple commodity categories. This concentration reflects both geographical proximity and China's unmatched processing infrastructure capacity.

European market share remains limited to approximately 15-20% of total exports, primarily consisting of uranium for nuclear fuel cycles and semi-processed metals for industrial applications. This distribution pattern demonstrates both the challenge and opportunity for market diversification strategies.

Russian transit routes facilitate the majority of China-bound exports, creating dual dependency on both processing destination and transport infrastructure. Disruption of either element could severely impact export revenue and market access, highlighting the strategic importance of diversification efforts.

The China Dependency Risk in Raw Materials Trade

China's processing monopoly extends beyond simple market share toward comprehensive technological and infrastructure control across critical minerals value chains. Chinese entities control approximately 70% of global rare earth refining, 60% of cobalt processing, and 50% of lithium chemical production capacity.

This processing concentration enables Chinese companies to influence global pricing, quality standards, and supply allocation decisions across multiple mineral categories. Kazakhstan's raw material export dependency effectively subsidises Chinese processing capabilities while limiting domestic value capture opportunities.

Strategic dependency risks extend beyond economic considerations toward national security implications for Kazakhstan's resource sovereignty. Over-reliance on single-destination exports creates vulnerability to trade policy changes, processing capacity constraints, and geopolitical tensions beyond Kazakhstan's control, as highlighted in recent European supply chain discussions.

Western Partnership Opportunities and Investment Barriers

Western mining companies and investment institutions demonstrate growing interest in Kazakhstan's critical minerals potential, driven by supply chain security concerns and Chinese processing dependency reduction objectives. However, institutional barriers and risk perception challenges limit partnership development.

Investment barriers include regulatory uncertainty, currency stability concerns, political risk perception, and limited local content requirements that could guarantee market access for processed products. Western entities require predictable regulatory frameworks and investor protection mechanisms before committing capital to processing infrastructure.

Strategic partnerships with Western entities could provide technology transfer, market access guarantees, and ESG compliance expertise necessary for processing localisation success. However, these partnerships require institutional reforms that address regulatory transparency, contract enforcement, and political stability concerns, particularly regarding institutional development requirements.

Which Institutional Reforms Could Unlock Kazakhstan's Supply Chain Potential?

Institutional quality emerges as the binding constraint on Kazakhstan's critical minerals development potential. Comparative analysis with established mining jurisdictions reveals specific reform priorities that could unlock international investment and enable processing localisation.

Licensing Transparency and Regulatory Predictability Gaps

Mining licensing procedures in Kazakhstan lack the transparency and predictability standards expected by international investors. Current frameworks involve multiple agencies with overlapping jurisdictions, creating approval delays and regulatory uncertainty that discourage long-term capital commitments.

Established mining jurisdictions like Australia and Chile maintain centralised licensing systems with defined timelines, standardised criteria, and appeal mechanisms that provide investors with predictable regulatory pathways. Kazakhstan's fragmented approach increases transaction costs and creates opportunities for discretionary decision-making.

Regulatory reform priorities include licensing system consolidation, standardised environmental assessment procedures, and defined timelines for permit approvals. These improvements could significantly reduce project development risk and attract patient capital necessary for processing infrastructure investment.

Investment Climate Comparison: Kazakhstan vs. Australia and Chile

Comparative analysis positions Kazakhstan's investment climate substantially below established mining jurisdictions across multiple dimensions. Australia and Chile benefit from stable legal frameworks, transparent regulatory processes, and predictable tax regimes that encourage long-term mining investments.

Contract enforcement mechanisms in Kazakhstan lack the reliability and independence demonstrated by common law jurisdictions, creating uncertainties around dispute resolution and property rights protection. International arbitration access remains limited compared to established investment treaties in competing jurisdictions.

Tax regime complexity and frequent changes undermine investment predictability, particularly for projects requiring decade-long payback periods typical in processing infrastructure. Stable fiscal frameworks with grandfathering provisions could address these investor concerns while maintaining government revenue objectives.

Coordination Mechanisms Between Government and Private Sector

Effective coordination between government agencies and private sector operators remains underdeveloped in Kazakhstan's mining sector. Fragmented policy implementation and limited stakeholder consultation create misalignment between national strategic objectives and private investment incentives.

Successful mining jurisdictions maintain formal consultation mechanisms that enable private sector input into regulatory development, infrastructure planning, and strategic policy formulation. These institutional arrangements improve policy effectiveness while reducing implementation resistance.

Development of public-private partnership frameworks could align government infrastructure investment with private sector processing capacity development. Coordinated planning mechanisms would optimise resource allocation while reducing duplicative investments across the value chain, similar to approaches used in other strategic minerals reserve initiatives.

What Are the Investment Implications for Western Supply Chain Security?

Kazakhstan's critical minerals potential represents both opportunity and risk for Western supply chain security objectives. Investment implications span development timelines, capital requirements, and risk assessment frameworks that determine project viability and strategic value.

Timeline Analysis: 16-Year Exploration-to-Production Lag Challenges

Current data indicates an average 16-year lag from initial exploration to commercial production in Kazakhstan's mining sector, significantly exceeding the 8-12 year timelines typical in established jurisdictions like Australia. This extended development period reflects regulatory complexity, infrastructure constraints, and financing challenges.

Extended development timelines create strategic risks for supply chain security planning, as current critical minerals shortages require solutions within 5-10 year timeframes. Kazakhstan's institutional constraints effectively delay supply chain contributions beyond immediate strategic requirements.

Accelerated development pathways require regulatory streamlining, infrastructure pre-investment, and risk-sharing mechanisms that reduce private sector development timelines. Government infrastructure investment and regulatory reform could potentially reduce project timelines to competitive levels with other jurisdictions.

Capital Requirements for Domestic Processing Infrastructure

Processing infrastructure development requires substantial capital investments that extend well beyond typical mining project scales. Estimates suggest $17-21 billion in total investment across foundation, processing, and integration phases spanning 2025-2035.

| Phase | Years | Key Milestones | Investment Required |

|---|---|---|---|

| Foundation | 2025-2027 | Regulatory reform, infrastructure | $2-3 billion |

| Processing | 2027-2030 | Domestic refining capacity | $5-8 billion |

| Integration | 2030-2035 | Value-chain participation | $10+ billion |

Capital requirements exceed most single-company capabilities, necessitating consortium financing approaches or development finance institution participation. Risk-sharing mechanisms and government co-investment could improve project economics while maintaining private sector operational efficiency.

Risk Assessment: Political Stability vs. Resource Access Trade-offs

Investment risk assessment must balance Kazakhstan's substantial resource potential against political stability concerns, regulatory uncertainty, and operational challenges. Political risk insurance and bilateral investment treaty protections could mitigate some investor concerns but cannot eliminate underlying institutional weaknesses.

Resource access benefits include geological diversity, established mining operations, and strategic positioning between Asian and European markets. However, these advantages must be weighed against institutional quality gaps and dependency risks that could affect long-term project viability.

Strategic investors require comprehensive risk assessment frameworks that quantify institutional, operational, and market risks against potential supply chain security benefits. Government reform commitments and international partnership agreements could improve risk-return calculations for patient capital providers.

The next major ASX story will hit our subscribers first

How Could Kazakhstan's Strategy Impact Global Critical Minerals Markets?

Successful implementation of Kazakhstan's critical minerals supply chain strategy could significantly reshape global supply patterns, pricing dynamics, and strategic relationships across multiple commodity categories. These impacts would extend beyond bilateral trade relationships toward broader market structure transformation.

Supply Diversification Benefits for Western Manufacturers

Kazakhstan's processing capacity development would provide Western manufacturers with alternative supply sources outside Chinese-controlled networks. This diversification could reduce supply chain vulnerabilities and improve negotiating leverage with existing suppliers.

Geographic diversification benefits include reduced transport risks, alternative routing options, and competitive pricing from multiple source development. Western manufacturers require supplier diversification to meet emerging supply chain due diligence requirements and reduce concentration risks.

However, diversification benefits depend on Kazakhstan's ability to achieve international quality standards, reliable delivery schedules, and competitive pricing relative to established suppliers. Processing technology transfer and quality certification programmes would be essential for market access success.

Price Stability Implications of New Processing Capacity

Additional processing capacity could moderate price volatility across critical minerals markets by reducing supply concentration and improving market competition. Increased competition typically benefits downstream manufacturers through improved pricing power and supply reliability.

Market impacts would vary by commodity category, with greatest benefits in markets currently dominated by single-source suppliers. Rare earth elements, battery chemicals, and specialty metals would likely experience the most significant competitive effects from new processing capacity.

Price discovery mechanisms could improve through increased market participation and reduced information asymmetries. Transparent pricing and long-term contract availability would enhance market predictability for downstream manufacturers and end-users.

Geopolitical Risk Reduction Through Alternative Supply Routes

Trans-Caspian corridor development could reduce Western dependency on transport routes controlled by potentially hostile entities. Alternative routing options improve supply security while reducing geopolitical leverage over critical materials access.

Strategic route diversification enables more resilient supply chain planning and reduces vulnerability to transport disruptions, trade disputes, and sanctions regimes. These security benefits justify infrastructure investment beyond purely commercial considerations.

Multilateral coordination requirements for corridor development create opportunities for strengthened strategic partnerships between Kazakhstan and Western entities. Successful cooperation could establish frameworks for broader economic and security cooperation beyond minerals trade.

What Are the Key Success Factors for Kazakhstan's Critical Minerals Transformation?

Successful transformation requires coordinated progress across multiple dimensions including technology transfer, workforce development, international standards adoption, and strategic partnership cultivation. These success factors must be addressed simultaneously rather than sequentially.

Technology Transfer Requirements for Advanced Processing

Advanced processing capabilities require sophisticated metallurgical expertise that does not currently exist within Kazakhstan's technical workforce. Technology transfer partnerships with established processors could provide essential knowledge while building domestic capabilities.

Successful technology transfer requires long-term partnership commitments that include training programmes, joint operations, and gradual capability transfer over multi-year timelines. One-time consulting arrangements would be insufficient for developing competitive processing capabilities.

Intellectual property protection frameworks must be strengthened to encourage technology transfer partnerships with international entities. Clear patent protection, trade secret safeguards, and contract enforcement mechanisms are prerequisites for advanced technology sharing agreements.

Workforce Development for High-Value Manufacturing

Processing operations require specialised technical expertise in metallurgy, chemical engineering, environmental management, and quality control that extends beyond traditional mining capabilities. Comprehensive workforce development programmes must address these skill gaps through education and training initiatives.

International partnership programmes with established mining and processing companies could provide practical training opportunities and technical expertise transfer. These programmes require sustained commitment over 5-10 year periods to develop competitive capabilities.

University-industry cooperation frameworks could align educational programmes with processing industry requirements while building research capabilities for innovation and continuous improvement. Long-term human capital investment is essential for sustained competitiveness.

International Standards Adoption for ESG Compliance

ESG compliance requirements increasingly determine market access and investment availability for mining and processing operations. Kazakhstan must adopt internationally recognised environmental, social, and governance standards to compete in global markets.

Environmental standards adoption includes waste management protocols, emissions monitoring systems, and remediation procedures that meet international best practices. These requirements extend beyond legal compliance toward operational excellence that demonstrates long-term sustainability.

Social standards encompass community engagement, worker safety, and indigenous rights protection that align with international expectations. Governance standards include transparency, accountability, and stakeholder engagement that meet institutional investor requirements.

Frequently Asked Questions About Kazakhstan's Critical Minerals Future

Understanding Kazakhstan's critical minerals development requires addressing common questions about competitive advantages, investment risks, strategic partnerships, and market access opportunities.

What minerals does Kazakhstan have the most competitive advantage in?

Kazakhstan's greatest competitive advantages exist in uranium production, where 40%+ global market share provides established infrastructure and operational expertise. Chromium and manganese deposits in Aktobe and Kostanay regions respectively offer significant expansion potential with favourable geology and existing mining operations.

Emerging competitive advantages in rare earth elements depend on successful development of Karaganda region deposits and processing infrastructure investment. Battery metals including copper, zinc, and lithium represent longer-term opportunities requiring substantial technology transfer and capital investment.

How does political risk affect long-term mining investments?

Political risk represents the primary concern for international investors considering long-term commitments in Kazakhstan's mining sector. Regulatory uncertainty, contract enforcement challenges, and policy stability concerns create risk premiums that affect project economics and investment decisions.

Risk mitigation strategies include political risk insurance, bilateral investment treaty protections, and multilateral development finance institution participation. However, these mechanisms cannot substitute for fundamental institutional improvements in transparency, predictability, and rule of law.

What role do Chinese partnerships play in Kazakhstan's strategy?

Chinese partnerships provide market access, processing expertise, and capital investment that enable current mining operations but potentially constrain value chain advancement. Balancing Chinese cooperation with diversification objectives represents a key strategic challenge for Kazakhstan's development planning.

Chinese entities offer established supply chain integration and technology transfer opportunities but may prioritise raw material export over domestic processing development. Strategic partnership frameworks must align Chinese capabilities with Kazakhstan's value chain advancement objectives.

Which Western companies are already investing in Kazakhstan's mining sector?

Several Western mining companies maintain operations or exploration interests in Kazakhstan, including European and North American entities focused on uranium, copper, and zinc projects. However, specific company identification requires current verification due to frequent partnership changes and project status updates.

Western investment patterns typically focus on established commodities with existing infrastructure rather than emerging critical minerals requiring processing development. Expanding Western participation requires addressing institutional barriers and risk perception challenges that currently limit investment flows.

Investment Outlook: Scenarios for Kazakhstan's Critical Minerals Development

Three primary scenarios capture the range of potential outcomes for Kazakhstan's critical minerals supply chain development through 2035. Each scenario reflects different institutional reform trajectories and international partnership success levels.

Best-Case Scenario: Successful Processing Localisation by 2030

The optimistic scenario envisions successful regulatory reform, substantial international investment, and effective technology transfer that enables competitive processing capabilities within five years. This outcome requires coordinated government action, private sector engagement, and sustained political commitment to institutional modernisation.

Success indicators would include operational rare earth separation facilities, expanded battery metal refining capacity, and established European market access through Trans-Caspian corridors. Processing depth would advance from current 30% to 70%+ across major commodity categories.

Investment requirements approach $15-20 billion over the scenario period, with significant development finance institution participation and Western mining company partnerships. Employment effects could reach 50,000+ skilled positions in processing operations and supporting industries.

Base-Case Scenario: Continued Raw Export Dependence

The most likely scenario projects gradual improvement in mining operations but limited processing advancement due to institutional constraints and financing challenges. Export growth continues at current rates while value capture remains concentrated in raw materials and basic concentrates.

This scenario reflects persistent regulatory uncertainty, limited international partnership development, and continued Chinese processing dominance. Infrastructure development proceeds slowly while institutional reforms achieve modest improvements without fundamental transformation.

Economic benefits include employment in expanded mining operations and incremental export revenue growth. However, strategic value remains limited due to continued raw material export dependence and limited value chain participation.

Risk Scenario: Increased Chinese Processing Control

The pessimistic scenario envisions deepening Chinese processing integration without corresponding domestic capability development. Kazakhstan becomes more tightly integrated into Chinese supply chains while losing strategic flexibility and value chain advancement potential.

Risk factors include continued institutional weakness, limited Western investment, and strategic partnership failures that leave Chinese entities as primary development partners. Processing investments concentrate in Chinese-controlled facilities rather than domestic capacity building.

Strategic implications include reduced supply chain diversification potential for Western entities and increased dependency relationships that could constrain future policy flexibility. Economic benefits exist but remain subordinated to external supply chain priorities.

Despite holding world-class reserves in 25+ critical minerals, Kazakhstan processes less than 30% domestically. This creates a strategic vulnerability where raw materials flow to external processors—particularly China—while finished products are imported back at premium prices.

Investment Disclaimer: This analysis is based on current research and publicly available information as of 2025. Critical minerals markets involve substantial risks including commodity price volatility, regulatory changes, geopolitical instability, and technology disruption. Investment decisions should consider comprehensive due diligence and professional financial advice. Forecasts and projections are inherently uncertain and should not be relied upon as investment recommendations.

Looking to Invest in Kazakhstan's Critical Minerals Transformation?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, showcasing exceptional examples, and begin your 30-day free trial today to position yourself ahead of the market.