June 26, 2026

The Geopolitics of Supply Chain Redundancy: Why Central Asia Is Now Central to European Strategy

Energy security planners have long understood that the most dangerous dependencies are the ones that only become visible during a crisis. For decades, Europe's reliance on Russian hydrocarbons was treated as a manageable commercial arrangement. The events of 2022 transformed that assumption permanently, forcing Brussels to accelerate a supply chain diversification agenda that had previously advanced at a diplomatic pace. Central Asia, and Kazakhstan in particular, has emerged as the most structurally significant beneficiary of this recalibration.

The Kazakhstan EU energy and trade deals concluded during President Kassym-Jomart Tokayev's Brussels visit in June 2026, collectively valued at more than $12 billion, represent far more than a single round of contract signings. They are the visible output of a multi-year institutional architecture designed to reorient European critical minerals supply chain across four distinct resource categories simultaneously: hydrocarbons, nuclear fuel, critical minerals, and emerging clean energy.

When big ASX news breaks, our subscribers know first

Kazakhstan's Unique Strategic Resource Profile

What distinguishes Kazakhstan from virtually every other potential EU supply partner is the sheer breadth of its resource portfolio. No single non-European nation offers comparable coverage across the full spectrum of European strategic needs.

| Resource Category | Kazakhstan's Position |

|---|---|

| Critical Raw Materials | Capable of supplying 21 of 34 EU-designated strategic minerals |

| Key Minerals | Copper, lithium, nickel, cobalt, rare earth elements |

| Crude Oil | Major volumes; predominantly routed via Russian territory historically |

| Uranium | World's largest producer; recognised EU supplier |

| Renewable Energy Potential | Multi-gigawatt wind and solar capacity under active development |

Kazakhstan's geology is particularly relevant here. The country sits atop the ancient Kazakh Platform, a geological formation that generates extraordinary mineral diversity. Unlike many resource-rich nations that specialise in one or two commodities, Kazakhstan's subsoil contains economically significant concentrations of materials spanning the entire periodic table of industrial relevance.

This geological diversity is not accidental. It reflects the country's position at the convergence of ancient tectonic zones that produced the mineralogical complexity now attracting coordinated Western investment interest.

The Enhanced Partnership and Cooperation Agreement (EPCA), ratified in 2015 and in force since March 1, 2020, provides the binding legal framework underpinning this relationship. This agreement distinguishes Kazakhstan from all other Central Asian states in terms of the depth of its formal EU institutional relationship, covering trade, investment, energy, transport, environmental standards, and judicial cooperation within a single treaty architecture.

Anatomy of the $12 Billion Brussels Deal Package

Understanding the composition of the Brussels agreements reveals a deliberate strategic logic rather than a collection of opportunistic commercial transactions.

Commercial Transactions

- Air Astana's procurement of 50 Airbus A320-family aircraft, valued at approximately €7.1 to €7.3 billion, constitutes the largest single transaction and simultaneously deepens Kazakhstan's aviation sector integration with European industrial supply chains

- A certification agreement processed through sovereign wealth vehicle Samruk Kazyna carries an estimated value of €8.3 billion, expanding the institutional framework for structured investment cooperation

- A €967 million service contract with French rail manufacturer Alstom secures long-term maintenance of Kazakhstan Railways' locomotive fleet, a transaction with direct operational significance for Middle Corridor freight reliability

- Connectivity memoranda totalling approximately €1.47 billion address European airline access to Kazakh airports and streamlined visa processing arrangements for Kazakh nationals

Strategic Resource and Energy Agreements

- A Memorandum of Understanding on Critical Raw Materials, originally signed November 7, 2022, was reinforced with updated operational coordination frameworks active since May 2023

- The 2025-2026 Strategic Partnership Roadmap formalises joint investment projects, geological research programmes, raw material supply integration, and ESG alignment frameworks

- Brussels formally recognised Kazakhstan's role as a supplier of crude oil and uranium while identifying renewable energy cooperation as a priority growth vector

Analytical Note: The Airbus transaction is frequently cited as the headline figure, but the more strategically consequential elements are the critical minerals roadmap and the implicit pipeline discussions. Commercial aviation deals generate short-term industrial value. Mineral supply chain integration reshapes industrial dependencies for decades.

The Trade Relationship in Numbers

The scale of existing EU-Kazakhstan economic integration is frequently underappreciated in mainstream analysis of European energy policy. Furthermore, the EU-Kazakhstan partnership has been deepening steadily for years before the Brussels summit formalised its latest stage.

| Indicator | Value |

|---|---|

| EU Share of Kazakhstan's Total Trade | 32.4% (EU is Kazakhstan's largest trading partner) |

| Bilateral Goods Trade (2024) | €45 billion (up 6.1% from 2023) |

| EU Investment in Kazakhstan (2023) | €7.8 billion |

| Cumulative European Investment | €170 billion |

| Near-Term Trade Target | Increase bilateral trade to $50 billion |

These figures establish that the Brussels summit was not a pivot toward a new partner but rather a formalisation and acceleration of a relationship that has been deepening for years. The €170 billion in cumulative European investment places Kazakhstan firmly within Europe's existing economic architecture, not merely on its periphery.

The Middle Corridor: Why Bypass Infrastructure Matters

The Trans-Caspian International Transport Route (TITR), known informally as the Middle Corridor, is the physical infrastructure dimension of the EU-Kazakhstan strategic relationship that receives insufficient analytical attention relative to its importance.

The route connects China and Central Asia to Europe via Kazakhstan, the Caspian Sea, Azerbaijan, Georgia, and Turkey, bypassing Russian territory entirely. Following geopolitical disruptions to traditional Eurasian trade routes, the Middle Corridor's strategic value has increased dramatically. Kazakhstan functions as the eastern anchor of this system, meaning its railway capacity, logistics infrastructure, and transit reliability are direct European strategic assets.

The Alstom locomotive maintenance contract is best understood in this context. A €967 million commitment to maintaining the rolling stock of Kazakhstan Railways is, at its core, a European investment in Middle Corridor operational continuity. If Kazakhstan's freight rail network degrades, so does Europe's most viable alternative to Russian transit infrastructure.

Key factors driving Middle Corridor relevance include:

- Geopolitical disruption rendering traditional northern Eurasian routes commercially and politically unattractive

- Growing Chinese export volumes seeking western market access through non-Russian corridors

- European interest in reducing dependence on both Russian transit and Suez Canal throughput constraints

- The corridor's multimodal nature, combining rail, sea, and road segments, provides flexibility that single-mode alternatives cannot match

The Trans-Caspian Pipeline Question: New Reserves Change the Calculus

Perhaps the most consequential unresolved infrastructure question in European energy strategy is whether a trans-Caspian pipeline will be built to carry Kazakh oil directly westward, bypassing Russian territory entirely.

Currently, the overwhelming majority of Kazakhstan's oil exports transit through Russian pipeline infrastructure, a structural dependency that European energy planners view as strategically untenable over the medium term. The long-discussed trans-Caspian pipeline has repeatedly stalled on the twin obstacles of insufficient production volumes to justify capital expenditure and geopolitical complexity involving Caspian Sea legal frameworks.

Recent discoveries of substantial new oil and natural gas reserves in Kazakhstan's Ustyurt Plateau have materially altered the economic viability assessment. If those reserve volumes are confirmed through further appraisal drilling, the production case for a dedicated trans-Caspian export route strengthens considerably.

| Scenario | Key Conditions | Assessment |

|---|---|---|

| Pipeline proceeds within 5 years | Ustyurt reserves confirmed; EU financing committed | Increasingly plausible if appraisal drilling validates scale |

| Phased development over 10+ years | Incremental reserve development; partial institutional funding | Most likely base case under current information |

| Indefinite delay | Insufficient reserve volumes; unresolved Caspian legal complications | Risk diminishes materially with successful reserve confirmation |

What is less commonly understood is that the Ustyurt Plateau sits in a sedimentary basin that geologists have historically considered underexplored relative to Kazakhstan's more heavily drilled western provinces. New seismic technology and improved subsurface imaging have enabled exploration programmes that earlier generations of surveys could not have conducted with comparable resolution. The reserve discoveries therefore may reflect methodology improvements as much as geological fortune, suggesting further discoveries in the region remain possible.

The next major ASX story will hit our subscribers first

Green Hydrogen and Kazakhstan's Clean Energy Export Potential

Beyond hydrocarbons, Kazakhstan is positioning itself within European clean energy transition planning through large-scale renewable energy projects with hydrogen production targets. In addition, the critical minerals demand driven by the energy transition further elevates Kazakhstan's strategic importance to Europe.

The Hyrasia One project, located in the Mangystau region and led by German developer Svevind, illustrates the scale of ambition involved:

- Combined wind and solar capacity target of 40 GW

- Annual green hydrogen production target of 2 million tonnes

- Located in a region with exceptional wind resource quality, a factor that materially improves the economics of electrolytic hydrogen production

A separate 1 GW wind farm in Kazakhstan's Zhambyl region, developed by France's TotalEnergies, adds further renewable generation capacity to the bilateral portfolio.

What makes Kazakhstan's green hydrogen proposition technically interesting is its wind resource profile. The country's vast steppe geography generates some of the most consistent high-velocity wind conditions in Asia, with capacity factors in certain corridors approaching those found in offshore North Sea installations. For electrolytic hydrogen economics, where electricity input cost is the primary variable, sustained high capacity factors translate directly into competitive production cost structures.

The EU's hydrogen strategy explicitly identifies Central Asia as a viable long-term supplier corridor. Kazakhstan's participation in green hydrogen value chains is embedded in both the 2022 MoU and the 2025-2026 Strategic Partnership Roadmap, meaning hydrogen cooperation has treaty-level institutional backing.

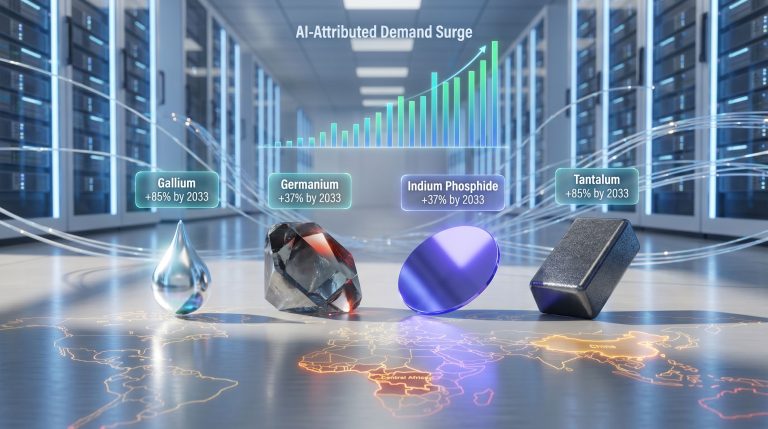

The Critical Minerals Race: Western Strategy Against Chinese Dominance

Kazakhstan's ability to supply 21 of the 34 raw materials classified as strategically critical by the European Union creates a supply diversification opportunity that no other single partner can replicate. However, understanding why this matters requires appreciating a supply chain dynamic that most general analysis obscures.

Raw material extraction and mineral processing are functionally different industries. China's competitive advantage in critical minerals does not rest primarily on ownership of ore deposits but on its commanding dominance of processing and refining capacity. Even where Western companies source raw materials from Kazakhstan or other non-Chinese jurisdictions, those materials frequently travel through Chinese processing facilities before reaching European manufacturers.

This means that simply shifting the geography of mining does not automatically reduce strategic dependency on China. The European critical raw materials agenda is partly designed to address this processing gap, not merely the extraction dimension.

Addressing this gap is also partly what animates the Orion Critical Mineral Consortium, a US government-backed investment vehicle seeking to raise $20 billion in funding to develop critical mineral supply chains across Asia. The consortium is backed by the US International Development Finance Corporation (DFC) and Abu Dhabi's sovereign wealth fund, with Kazakhstan and Uzbekistan identified as priority markets.

Scale Context: Consortium officials have estimated that fully realising Western access to Asian critical mineral supply chains, including processing and refining infrastructure, would require approximately $2.4 trillion in investment over 25 years. This figure captures the depth of the competitive gap relative to China's existing infrastructure position.

For investors monitoring this space, the $2.4 trillion figure functions as a structural investment thesis rather than a projection. It describes the scale of capital required to build a complete, China-independent critical mineral supply chain from extraction through processing to manufactured end-use. Projects that advance individual segments of this chain, whether in Kazakhstan, Uzbekistan, or elsewhere in Central Asia, are participating in a capital deployment cycle of generational duration.

Comparing Kazakhstan's Strategic Value Against Other EU Supply Partners

| Supply Category | Kazakhstan | Norway | Gulf States | North Africa |

|---|---|---|---|---|

| Crude Oil | Yes, significant | Yes, major | Yes, major | Yes, moderate |

| Uranium | Yes, world's largest producer | No | No | Limited |

| Critical Minerals (21 of 34 EU-strategic) | Yes | Limited | Limited | Limited |

| Green Hydrogen (developing) | Yes, projects underway | Yes, developing | Yes, developing | Yes, developing |

| Middle Corridor Transit Anchor | Yes | No | No | No |

This comparison illustrates why Kazakhstan occupies a structurally distinct position in European supply chain planning. Norway provides oil and gas but cannot address critical minerals, uranium, or Middle Corridor transit. Gulf states offer hydrocarbons but lack mineral diversity and Eurasian transit relevance. North Africa contributes to renewable energy ambitions but cannot supply the battery-critical minerals that European manufacturing increasingly requires.

Furthermore, Kazakhstan's uranium dominance as the world's largest producer adds a nuclear fuel dimension that no other alternative supply partner can replicate. Only Kazakhstan covers all five strategic categories simultaneously.

What Investors and Analysts Should Watch

Several forward-looking indicators will determine whether the Brussels deal architecture translates into durable strategic realignment or remains primarily symbolic:

- Ustyurt Plateau appraisal results: Confirmation of reserve volumes at the scale implied by initial discoveries would trigger a definitive reassessment of trans-Caspian pipeline economics

- Orion Consortium capital deployment: Whether the consortium reaches its $20 billion fundraising target and begins deploying capital in Kazakhstan will signal Western institutional commitment to the critical minerals agenda

- Middle Corridor throughput data: Volume growth along the Trans-Caspian route provides a measurable proxy for how effectively the Alstom and connectivity investments are translating into operational improvements

- Hyrasia One financing milestones: Green hydrogen projects at the 40 GW scale face substantial project finance complexity; early financing confirmations will validate the timeline

- EPCA implementation depth: How extensively the 2025-2026 Strategic Partnership Roadmap is operationalised across geological research, ESG alignment, and supply integration will determine whether the institutional framework produces tangible outcomes

The critical minerals geopolitics shaping European supply chain strategy extend well beyond any single bilateral relationship. However, the EU's formal engagement with Kazakhstan illustrates how institutional depth can translate resource geography into durable strategic advantage.

Disclaimer: The forward-looking scenarios and investment considerations discussed in this article are analytical frameworks based on publicly available information and should not be construed as financial advice. Geopolitical developments, reserve confirmation outcomes, and capital market conditions may differ materially from any scenarios presented.

The Kazakhstan EU energy and trade deals concluded in Brussels in June 2026 represent the most substantive institutional deepening of this relationship since the EPCA entered force. Whether that deepening translates into the structural supply chain reconfiguration that European energy planners are seeking will depend on technical, financial, and geopolitical variables that remain genuinely uncertain. What is clear is that no other partner offers Europe the same combination of resource breadth, geographic positioning, and institutional engagement that Kazakhstan currently provides.

Want to Track the Next Major Mineral Discovery Before the Market Does?

The critical minerals supply chain transformation reshaping European and global strategy creates significant opportunities for investors positioned ahead of major ASX discoveries — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across copper, lithium, cobalt, rare earths, and more than 30 other commodities, while its dedicated discoveries page showcases the historic returns that major mineral discoveries have generated, illustrating precisely why early identification matters. Begin your 14-day free trial today and secure a market-leading advantage as the global race for critical minerals intensifies.