May 23, 2026

The Quiet Shift Underneath Africa's Growth Story

Across sub-Saharan Africa, a quiet rebalancing has been underway for several years. Economies that once relied heavily on commodity exports and rain-fed agriculture are gradually discovering that their most durable growth drivers are services, digital infrastructure, and intra-regional trade. Kenya sits at the centre of this transition, and its 2025 economic performance tells a story that is far more nuanced than any single headline figure can convey.

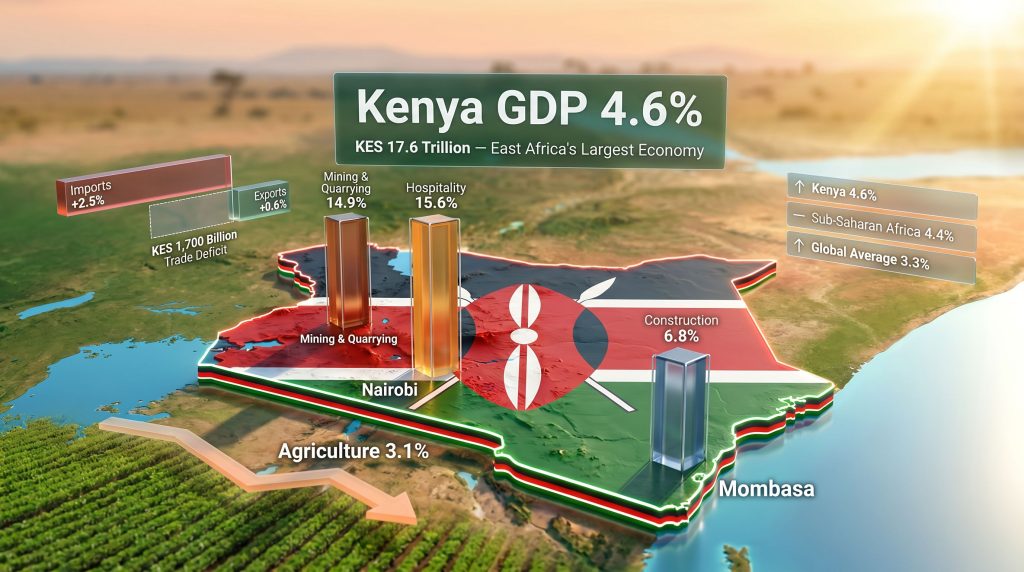

Understanding why Kenya economic growth slows in 2025 requires looking beyond the 4.6% GDP expansion reported by the Kenya National Bureau of Statistics in its April 2026 Economic Survey. The real insight lies in what is accelerating, what is dragging, and what structural vulnerabilities are quietly compounding beneath a headline number that, by most global benchmarks, still looks respectable.

When big ASX news breaks, our subscribers know first

Three Years of Deceleration: Reading the Pattern

Kenya's growth trajectory across recent years presents a clear directional signal that deserves careful interpretation rather than dismissal.

| Year | GDP Growth Rate | Agricultural Growth | Notable Pressure Points |

|---|---|---|---|

| 2023 | 5.7% | — | Strong baseline, post-recovery momentum |

| 2024 | 4.7% | 4.4% | Fiscal consolidation begins taking effect |

| 2025 | 4.6% | 3.1% | Weather disruption, trade gap widens |

The three-year consecutive deceleration is not catastrophic in isolation, but the direction matters as much as the magnitude. Each year, the economy has grown more slowly than the year before, and the gap between Kenya's performance and the regional sub-Saharan African average has compressed to just 0.2 percentage points in 2025, compared to a far more comfortable margin in 2023.

To place this in broader context:

- Kenya's 2025 growth of 4.6% exceeded the global average of 3.3%

- It also outpaced the sub-Saharan Africa average of 4.4%

- Kenya's nominal economy reached KES 17.6 trillion by end-2025, retaining its position as East Africa's largest economy ahead of Ethiopia at KES 14.2 trillion

"The narrowing performance gap between Kenya and its regional peers is not a crisis indicator, but it is a convergence signal that merits structural attention rather than cyclical optimism."

Agriculture's Outsized Influence on Headline Growth

Why 23% of GDP Can Move the Entire Economy

Agriculture remains Kenya's single largest sector, accounting for 23.2% of GDP in 2025. When it underperforms, the knock-on effects extend well beyond farming communities. The sector expanded by just 3.1% in 2025, down from 4.4% in 2024, representing a deceleration in momentum of 1.3 percentage points year-on-year.

A rough attribution calculation illustrates the scale of the drag. If agriculture represents 23.2% of GDP and its growth rate fell by 1.3 percentage points, the estimated direct contribution to headline deceleration is approximately 0.3 percentage points — accounting for roughly 38% of the total 0.8 percentage point slowdown from 2024 to 2025. The remaining deceleration reflects compositional shifts and modest softening across other sectors.

The weather dynamics behind this underperformance were uneven rather than uniformly negative:

- Long rains (March to May): Above-average precipitation benefited some food crop segments

- Short rains (October to December): Below-average rainfall constrained output in the second growing cycle

- Food crops: Maize, millet, and potato production increased; bean output declined

- Cash crops: Tea and sugarcane underperformed; most other cash crop segments posted positive results

This crop-level granularity is important. Agricultural weakness in 2025 was not a sector-wide productivity collapse. It was concentrated in specific commodities and specific seasonal windows, suggesting that targeted investments in irrigation infrastructure and crop calendar diversification could substantially reduce Kenya's exposure to future weather-driven growth volatility. Furthermore, this is consistent with broader critical minerals demand dynamics reshaping how emerging economies diversify their productive base beyond traditional agriculture.

The Climate-Structural Vulnerability Link

What makes Kenya's agricultural exposure particularly significant from a macroeconomic standpoint is that it represents a structural vulnerability rather than a purely cyclical risk. Fiscal policy cannot irrigate fields. Monetary easing cannot shift rainfall patterns.

Kenya's dependence on rain-fed agriculture means that a portion of its GDP growth potential is effectively hostage to climate variability in ways that peer economies with more developed irrigation infrastructure are not. Tea's underperformance is especially consequential given its importance as a foreign exchange earner. Kenya is among the world's top tea exporters, making cash crop weakness a direct contributor to the widening trade deficit discussed below.

The Sectors Holding Kenya's Economy Together

While agriculture weighed on the headline figure, several sectors delivered growth rates that would be impressive in any emerging market context. The diversification of Kenya's services and resource base is increasingly providing a portfolio-effect stabilisation that prevents agricultural volatility from generating sharper GDP declines.

| Sector | 2025 Growth Rate | GDP Share | Contribution Significance |

|---|---|---|---|

| Hospitality | 15.6% | Moderate | Tourism recovery driver |

| Mining & Quarrying | 14.9% | Smaller | High momentum, growing base |

| Public Administration | 8.3% | Significant | Government spending effect |

| Financial & Insurance | 6.5% | 8.3% | Stable anchor sector |

| Construction | 6.8% | Moderate | Infrastructure pipeline active |

| Information & Communication | 4.8% | Growing | Digital economy expansion |

| Transport & Storage | 3.7% | 11.8% | Large base, steady performer |

| Wholesale & Retail Trade | 3.6% | 7.8% | Consumer demand indicator |

| Real Estate | — | 8.2% | Large base, growth unspecified |

The hospitality sector's 15.6% expansion is particularly notable. It reflects a genuine recovery in international tourist arrivals and growing domestic tourism activity, indicating that Kenya's tourism infrastructure investments are yielding measurable dividends. Similarly, mining and quarrying's 14.9% growth suggests expanding resource extraction activity, though the sustainability of this rate depends on which specific minerals are driving the expansion.

Finance, ICT, real estate, and transport collectively represent a substantial share of Kenya's economic output. Their consistent positive performance suggests Kenya's growth model is undergoing a gradual but meaningful transition toward a services-led structure — a shift that carries significant implications for skills investment, regulatory reform, and infrastructure prioritisation. In addition, mineral investment trends across emerging markets highlight how resource sector momentum can meaningfully support broader economic diversification when managed strategically.

Kenya's Trade Balance: A Widening Structural Problem

The Import-Export Asymmetry

One of the most consequential developments in Kenya's 2025 macroeconomic profile is the continued deterioration of its external trade position. The data reveals an asymmetry that, if left unaddressed, creates mounting pressure on foreign exchange reserves and the current account balance.

| Metric | 2024 | 2025 | Change |

|---|---|---|---|

| Trade Deficit | KES 1,600B (~$12.4B) | KES 1,700B | +KES 100B (~+6.25%) |

| Export Growth | — | +0.6% | Sluggish |

| Import Growth | — | +2.5% | Accelerating |

Imports expanded at more than four times the rate of exports in 2025. This ratio is not sustainable over the medium term without either a significant boost to export revenues or a compression of import demand — neither of which is easily achievable in a growing economy with rising consumer and industrial needs.

Where Kenya Trades: The Regional Bright Spot and the Asian Challenge

Kenya's export geography tells a story of regional strength and extra-regional weakness:

- Africa remains the primary export destination, generating KES 452.8 billion in 2025

- Uganda was the standout performer within the East African Community, with demand for Kenyan goods surging 28.8% and representing 14.5% of total export earnings

- Asia recorded a significant decline in Kenyan export receipts, falling 13.2% to KES 275.7 billion

On the import side, the picture reverses sharply. Asia strengthened its dominance as Kenya's leading supplier, accounting for 70% of total imports in 2025, up from 66.4% in 2024. This concentration creates a dual vulnerability: Kenya is increasingly dependent on Asian suppliers while simultaneously losing Asian export market share.

"Kenya's growing dependence on Asian imports, combined with declining export performance to Asian markets, creates a compounding external imbalance. Rising import costs are not offset by corresponding export revenue from the same trading partner."

The Uganda export surge offers a more constructive narrative. A 28.8% increase in bilateral trade within the East African Community demonstrates that intra-regional demand for Kenyan manufactured and processed goods is growing robustly. This suggests that deepening EAC trade integration could provide a meaningful export diversification pathway. Moreover, African mining finance trends across the continent underscore how regional economic integration increasingly shapes trade competitiveness in ways that extend well beyond raw commodity flows.

Fiscal Position: The Deficit Behind the Headline

Where Kenya's Budget Stands Against Its Own Targets

Kenya's 2025 fiscal deficit reached 5.9% of GDP, materially exceeding the stated target of 4.3%. This 1.6 percentage point overshoot is not a budgetary footnote. It signals that government expenditure consistently outpaced revenue generation throughout the year, creating three compounding consequences:

- Reduced future stimulus capacity — a larger existing deficit constrains the government's ability to deploy counter-cyclical spending in future downturns

- Elevated debt servicing obligations — higher deficit financing increases interest payment burdens, which crowd out productive public investment

- Narrowed policy space — the gap between Kenya's actual and target fiscal position limits the range of credible policy responses available to policymakers

The World Bank's May 2025 update projected average growth of 4.9% for the 2025 to 2027 period. Kenya's actual 2025 result of 4.6% fell approximately 0.3 percentage points below that projection, reflecting the compounding effects of agricultural underperformance, fiscal slippage, and elevated public debt levels constraining government investment capacity.

The next major ASX story will hit our subscribers first

Three Structural Vulnerabilities Policymakers Cannot Ignore

Taken together, Kenya's 2025 economic data points toward three structural challenges that require coordinated long-term responses rather than short-term cyclical management:

1. Climate Exposure as a Macro Risk

Agricultural volatility driven by irregular rainfall functions as a ceiling on Kenya's growth potential. Until irrigation coverage expands significantly and crop diversification reduces dependence on rain-sensitive commodities, Kenya's headline GDP will remain partially hostage to seasonal weather patterns. This is a structural vulnerability that fiscal and monetary policy tools cannot directly address.

2. The Trade Deficit as a Structural, Not Cyclical, Challenge

With Asian suppliers accounting for 70% of total imports and export performance to Asian markets declining by 13.2%, Kenya faces a structural trade imbalance that will not self-correct through cyclical recovery alone. A deliberate export promotion strategy targeting high-growth regional markets — particularly within the EAC — appears to be Kenya's most viable near-term diversification pathway given Uganda's exceptional 28.8% import growth.

3. Services as the Emerging Growth Engine

The consistent outperformance of finance, ICT, hospitality, and transport sectors relative to GDP growth suggests Kenya's long-term growth model is shifting toward services leadership. This transition has important implications for education and skills investment, digital infrastructure prioritisation, and regulatory modernisation. Furthermore, understanding north american mining trends and similar resource-driven growth models globally can offer useful comparative frameworks as Kenya refines its own sector diversification strategy.

What Does 2026 Look Like From Here?

Forecasts carry inherent uncertainty, and the following represents analyst consensus rather than confirmed outcomes. Several factors point toward a modest recovery in 2026:

- Improved early-year rainfall patterns are expected to support agricultural output recovery and partially reverse 2025 crop underperformance

- Services sector momentum, particularly in finance, ICT, and hospitality, appears structurally intact

- Stable external inflows including remittances and foreign direct investment provide a demand buffer against external shocks

- Expanding intra-regional trade, particularly within the EAC, offers an export revenue growth pathway that does not depend on recovering Asian market demand

- Mining's 14.9% expansion and construction's 6.8% growth suggest that Kenya's infrastructure and resource extraction pipeline remains active

Whether Kenya closes the gap toward the World Bank's projected 4.9% average for the 2025 to 2027 period will depend significantly on whether agricultural conditions normalise and whether the fiscal deficit trajectory shows credible signs of narrowing toward the 4.3% target. Indeed, the question of how Kenya economic growth slows in 2025 will ultimately determine the ambition and urgency of the policy reforms that follow.

Frequently Asked Questions

What was Kenya's GDP growth rate in 2025?

Kenya's economy expanded by 4.6% in 2025, according to the Kenya National Bureau of Statistics 2026 Economic Survey released on April 29, 2026. This marked a deceleration from 4.7% in 2024 and 5.7% in 2023.

Why did Kenya's economic growth slow in 2025?

The primary driver was weaker agricultural performance, with the sector growing at only 3.1% compared to 4.4% in 2024, largely due to uneven weather patterns. A widening trade deficit — where imports grew at 2.5% against export growth of just 0.6% — and a fiscal deficit overshooting its target also contributed to the broader slowdown.

Which sectors grew fastest in Kenya in 2025?

Hospitality led with 15.6% growth, followed by mining and quarrying at 14.9%, public administration at 8.3%, and construction at 6.8%.

How does Kenya's 2025 growth compare to regional averages?

Kenya's 4.6% growth exceeded both the sub-Saharan African average of 4.4% and the global average of 3.3%, though the margin of outperformance has narrowed significantly compared to prior years.

What is Kenya's total GDP value as of 2025?

Kenya's economy reached KES 17.6 trillion by end-2025, making it the largest economy in East Africa by nominal measure, ahead of Ethiopia at KES 14.2 trillion.

What is Kenya's trade deficit in 2025?

The trade deficit widened to approximately KES 1,700 billion in 2025, up from KES 1,600 billion in 2024, driven by import growth of 2.5% against export growth of just 0.6%.

What is the economic outlook for Kenya in 2026?

Analysts anticipate a modest recovery supported by improved agricultural conditions, continued services sector growth, stable remittance inflows, and expanding intra-regional trade within the East African Community. However, as Kenya economic growth slows in 2025, the pathway to recovery will depend heavily on structural reform momentum. These projections carry inherent uncertainty and should not be treated as guaranteed outcomes.

Data in this article is sourced from the Kenya National Bureau of Statistics 2026 Economic Survey (released April 29, 2026) as reported by Ecofin Agency. Regional and global growth comparisons reference World Bank projections. Forward-looking statements involve uncertainty and should not be construed as financial advice. Readers are encouraged to consult independent economic analysis before drawing investment or policy conclusions.

Want to Identify the Next Major Mineral Discovery Before the Market Does?

While Kenya's evolving economic landscape highlights the growing importance of resource sector diversification across emerging markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data across 30-plus commodities into actionable insights for investors at every level. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.