July 19, 2026

India's Deepwater Gas Problem Is Bigger Than One Field

Across global energy markets, the gap between a nation's domestic gas production capacity and its actual consumption needs is rarely a sudden rupture. It tends to be a slow erosion, driven by ageing reservoirs, undershooting exploration pipelines, and the brutal physics of deepwater depletion. India is now living through exactly this kind of structural stress, and the numbers emerging from the country's most significant offshore gas block are making that tension impossible to ignore.

Reliance BP KG-D6 gas output falls 7% on a year-on-year basis in the April-June 2026 quarter, with average daily production settling at 24.8 million standard cubic meters per day (mmscmd). That compares to 26.6 mmscmd in the same quarter of 2025, and represents a further step down from the 25.2 mmscmd recorded in the January-March 2026 quarter. The trajectory is clear, and its implications extend well beyond a single operator's earnings presentation.

When big ASX news breaks, our subscribers know first

Understanding the Scale of What KG-D6 Represents

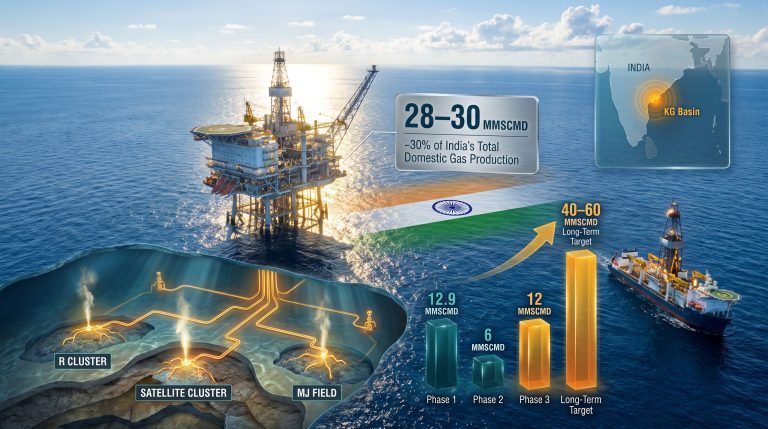

To appreciate why a 7% decline at one offshore block generates national-level concern, it helps to understand the structural weight KG-D6 carries within India's energy supply architecture. The block, formally designated KG-DWN-98/3 and located in the deep waters of the Bay of Bengal, contributes roughly 30% of India's total domestic natural gas production. Against a national consumption baseline of approximately 200 mmscmd, that is an enormous concentration of supply dependency in a single asset.

India does not have the luxury of easily substituting domestic shortfalls. When production at KG-D6 contracts, the immediate response involves pulling more liquefied natural gas (LNG) from international markets, which introduces both cost and energy price volatility. Spot LNG prices are susceptible to global demand shocks, geopolitical disruptions in exporting regions, and seasonal demand spikes in competing markets like Japan, South Korea, and Europe. Every mmscmd lost at KG-D6 is a mmscmd that must be sourced from a more expensive and less predictable supply chain.

A Decade of Output: From First Wave Failure to Second Wave Peak

KG-D6's production history is essentially a story told in two acts, both of which carry lessons about the limits of deepwater reservoir modelling.

The first act began in 2008 and 2009, when the MA oilfield and the D-1 and D-3 gas fields were brought into production. These were the flagship discoveries that initially positioned KG-D6 as a game-changer for India's energy self-sufficiency. However, the wells drilled across D-1 and D-3 encountered something the pre-production geological models had not adequately anticipated: severe water and sand ingress. Wellbore integrity degraded faster than expected, reservoir pressure fell sharply, and output collapsed well below projections. The MA field halted production entirely in September 2018, and D-1 and D-3 were shut down in February 2020.

Critically, BP had not yet joined as a technical partner when production planning for D-1 and D-3 was conducted. The partnership with BP, which took a 33.33% stake alongside Reliance's 66.67%, was formalised in 2011, after the first-wave production architecture had already been designed. This timing matters because it partially explains why the second wave incorporated substantially more sophisticated subsurface management from the outset.

The second act was built on a combined investment of approximately $5 billion, deploying three new deepwater development projects within the same KG-D6 block:

- R-Cluster: first gas achieved December 2020

- Satellites Cluster: production commenced April 2021

- MJ Field: brought online June 2023

At their designed peak capacity, these three fields were collectively projected to serve around 15% of India's total natural gas demand. They delivered on that ambition, reaching a combined peak of 30.6 mmscmd in the January-March 2024 quarter. That milestone, however, marked the ceiling of the second wave. Natural reservoir depletion began accelerating from mid-2025, and by the June 2026 quarter, cumulative output had contracted by roughly 19% from peak.

The Production Timeline: Key Figures at a Glance

| Period | Output (mmscmd) | Change |

|---|---|---|

| January-March 2024 | 30.6 | Second-wave peak |

| April-June 2025 | 26.6 | Baseline comparison |

| January-March 2026 | 25.2 | Sequential decline |

| April-June 2026 | 24.8 | ~7% YoY fall |

| Decline from peak | ~19% | Cumulative contraction |

The Geology Behind the Decline: Why Deepwater Reservoirs Are Uniquely Difficult

The KG basin's subsurface geology is not forgiving. Deepwater reservoirs in the Bay of Bengal exhibit complex pressure dynamics that differ substantially from the onshore and shallow-water fields that form the backbone of India's mature production base. Once a deepwater reservoir moves past its peak pressure support phase, production decline can accelerate in ways that are difficult to arrest through conventional well intervention techniques.

Unlike shallower formations where operators can implement relatively low-cost pressure maintenance programs, deepwater wells involve enormous per-well costs and limited workover windows. The logistical complexity of operating at depth, combined with the thermal and pressure conditions that affect wellbore integrity, means that remediation campaigns require both substantial capital commitment and considerable lead time.

The KG-D6 block contains 19 gas discoveries within the KG-DWN-98/3 acreage, yet only a fraction have progressed to commercial production. This gap between discovery count and producing fields reflects just how demanding the subsurface conditions in this part of the Bay of Bengal truly are.

The water and sand ingress problems that terminated the first wave of production have not been fully eliminated in the second wave either. While BP's involvement introduced more sophisticated drilling and reservoir management techniques, the fundamental geological characteristics of the basin continue to represent a wildcard in any production forecasting exercise.

Gas Pricing Compression Compounds the Volume Problem

The production decline is occurring alongside a deterioration in gas price realisations, creating a compounding effect on revenue. Reliance achieved a gas realisation of $8.89 per MMBtu in the April-June 2026 quarter, compared to $9.97 per MMBtu in the same period of the prior year. That represents a decline of approximately 11% in realised pricing, layered on top of the 7% volume contraction.

There is a partial offset worth noting. Condensate and oil realisation from the block improved significantly to $107.4 per barrel in Q1 2026, up from $69.9 per barrel in the year-earlier quarter. While this uplift in condensate pricing provides meaningful revenue support, condensate volumes are materially smaller than gas volumes, meaning the pricing improvement cannot fully compensate for the gas-side deterioration.

Can the Decline Be Arrested? Known Strategies and Remaining Questions

Reliance confirmed at its Q1 FY27 analyst briefing that a mitigation plan exists. The company indicated that the current rate of natural decline is actually tracking below its own worst-case internal projections, suggesting that reservoir behaviour has been somewhat more manageable than the modelling had assumed. The company stated that plans were in place to address the ongoing decrease, though specific details regarding well intervention timelines, infill drilling programmes, or capital commitments were not disclosed publicly.

The range of potential strategies available to Reliance and BP spans several categories:

| Strategy | Description | Feasibility Assessment |

|---|---|---|

| Infill drilling | Targeting undrained reservoir compartments with new wells | High cost; technically demanding at depth |

| Well workover programmes | Remediating existing wells affected by water ingress | Partial mitigation potential |

| Reservoir pressure management | Optimising production rates to extend pressure support | Limited by underlying geology |

| New discovery development | Advancing some of the 19 KG-D6 discoveries toward production | Long lead times; capital intensive |

| LNG supplementation | Importing additional LNG to cover domestic shortfall | Immediate but structurally more expensive |

Three Production Scenarios Through FY28

Scenario A – Managed Decline: Mitigation efforts succeed in stabilising the decline rate at 5 to 7% annually. Output plateaus in the 20-22 mmscmd range by FY28. India manages the resulting supply gap through moderate LNG supplementation without significant downstream disruption.

Scenario B – Accelerated Depletion: Interventions prove insufficient as reservoir pressure dynamics deteriorate faster than expected. Decline steepens to 10-12% annually, pushing output below 20 mmscmd by FY27. Fertiliser producers, city gas distribution networks, and gas-fired power generators face supply tightness and pricing pressure.

Scenario C – Partial Recovery: Successful infill drilling or accelerated commercialisation of existing KG-D6 discoveries reverses some of the decline. Output recovers toward the 27-28 mmscmd range by late FY27, requiring significant capital deployment and efficient subsurface execution.

Note: The above scenarios are illustrative projections based on historical decline rates and publicly available operational data. They do not constitute investment advice or represent company guidance.

BP's Expanding Role Across India's Upstream Sector

One of the less-discussed dimensions of this story is what KG-D6's challenges reveal about BP's evolving strategic position in India's oil and gas sector. Beyond its partnership with Reliance on KG-D6, BP has been engaged by state-owned Oil and Natural Gas Corporation (ONGC) as a technical partner to address declining production at Mumbai High and India's western offshore fields, which collectively represent the country's largest producing asset base.

This dual mandate positions BP as one of the most consequential technical actors in India's upstream sector, operating across both private and state-owned production infrastructure simultaneously. Furthermore, it signals something important about the nature of India's upstream challenge: the problem is not confined to KG-D6. Mature field decline is a system-wide issue, and the engagement of a global deepwater specialist across multiple flagship assets reflects the urgency attached to reversing that trend. The broader India energy market reforms underway also suggest that policymakers are acutely aware of these structural vulnerabilities.

The next major ASX story will hit our subscribers first

What the KG-D6 Decline Means for India's National Gas Balance

The block's contraction has already contributed to a 3% decline in India's aggregate natural gas production during the first half of the fiscal year. That is a meaningful deterioration in domestic supply at a time when the country's gas consumption ambitions are moving in the opposite direction.

India has been actively expanding its city gas distribution network, pushing gas deeper into industrial feedstock chains, and pursuing gas-to-power capacity as part of its broader energy strategy. However, the energy transition challenges associated with replacing declining domestic supply are considerable. A continued decline at KG-D6 does not derail these ambitions outright, but it raises the cost of pursuing them by increasing the LNG import bill and widening the domestic supply deficit that alternative sources will need to fill.

The block's 19 gas discoveries in the KG-DWN-98/3 acreage represent one potential future supply source, but converting exploration success into production volumes requires years of development work, regulatory clearances, and capital allocation. In addition, the global LNG supply outlook suggests that competition for flexible LNG cargoes will remain intense. There is no near-term replacement for KG-D6's current contribution available within India's domestic exploration pipeline.

The structural reality is that no comparable deepwater domestic asset exists in a production-ready state that could substitute for KG-D6 volumes within a 12 to 24 month timeframe. The block's decline is therefore a structural supply challenge requiring a medium to long-term response, not a problem that can be resolved through short-term operational adjustments alone.

Consequently, the question of how India manages this shortfall has significant implications for India LNG import taxes and broader import policy settings, as policymakers weigh the cost of increased LNG dependency against the urgency of maintaining gas supply to critical end-users.

Frequently Asked Questions

What is the KG-D6 block?

The KG-D6 block, formally designated KG-DWN-98/3, is a deepwater natural gas and condensate block in the Bay of Bengal. Reliance Industries operates it with a 66.67% equity stake, while BP holds 33.33%.

Why has Reliance BP KG-D6 gas output fallen?

The primary driver is natural reservoir depletion in the deepwater formations, which accelerated from mid-2025. Geological complexity, including historical water and sand ingress challenges, compounds the underlying pressure decline. The government has also sought $30 billion from Reliance and BP in a separate dispute over gas shortfalls at the block, adding a further dimension to the operational and regulatory pressures facing the partnership.

What was peak production at KG-D6?

The second-wave developments reached combined peak output of 30.6 mmscmd in January-March 2024. By the June 2026 quarter, output had contracted by approximately 19% from that level.

How significant is KG-D6 to India's gas supply?

KG-D6 contributes approximately 30% of India's domestic natural gas production. Its decline has contributed to a 3% contraction in India's overall gas output during the first half of the fiscal year.

What price did Reliance receive for KG-D6 gas in Q1 FY27?

Gas was realised at $8.89 per MMBtu, down from $9.97 per MMBtu a year earlier. Condensate realisation improved to $107.4 per barrel from $69.9 per barrel in the prior year.

Want to Stay Ahead of the Next Major Energy and Resources Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial to position yourself ahead of the broader market.