July 18, 2026

India's Deep-Water Gas Dilemma: Why the KG-D6 Block Carries the Weight of a Nation's Energy Future

The economics of deep-water gas development are rarely straightforward. Subsea infrastructure is capital-intensive, reservoir pressure management is technically demanding, and the gap between discovery and first production can stretch across nearly a decade. Yet for India, the calculus around the Krishna-Godavari Basin's KG-D6 block transcends conventional upstream investment logic. When a single offshore block accounts for roughly 30% of a country's total domestic gas output, the decisions made in its drilling programme become questions of national energy policy as much as corporate strategy.

Understanding why the Reliance KG-D6 gas production plan commands such attention requires stepping back from the field-level metrics and examining the structural supply challenge India has been navigating for years.

When big ASX news breaks, our subscribers know first

The Structural Deficit Driving Upstream Urgency

India occupies an unusual position in the global gas market. It is simultaneously one of the world's fastest-growing energy consumers and a country with substantial untapped domestic hydrocarbon resources. The gap between these two realities has historically been filled by liquefied natural gas imports, primarily routed through Gulf terminals and transiting the Strait of Hormuz corridor.

This dependence creates layered vulnerability. LNG import pricing is subject to global benchmark fluctuations, shipping route disruptions, and foreign currency exposure. Domestic gas production, by contrast, offers price predictability and supply security that imported volumes fundamentally cannot replicate. Furthermore, India's LNG import taxes add an additional cost burden that makes domestic supply even more economically attractive. It is within this context that the Krishna-Godavari Basin emerged as India's most strategically significant hydrocarbon province.

The KG Basin's geology is characterised by deep-water Cretaceous-age sedimentary sequences that accumulated substantial organic material over millions of years. The D6 block specifically sits in water depths ranging from several hundred to over 1,500 metres, requiring sophisticated subsea production systems, flexible risers, and floating production vessels that place it firmly in the technical frontier category of upstream development.

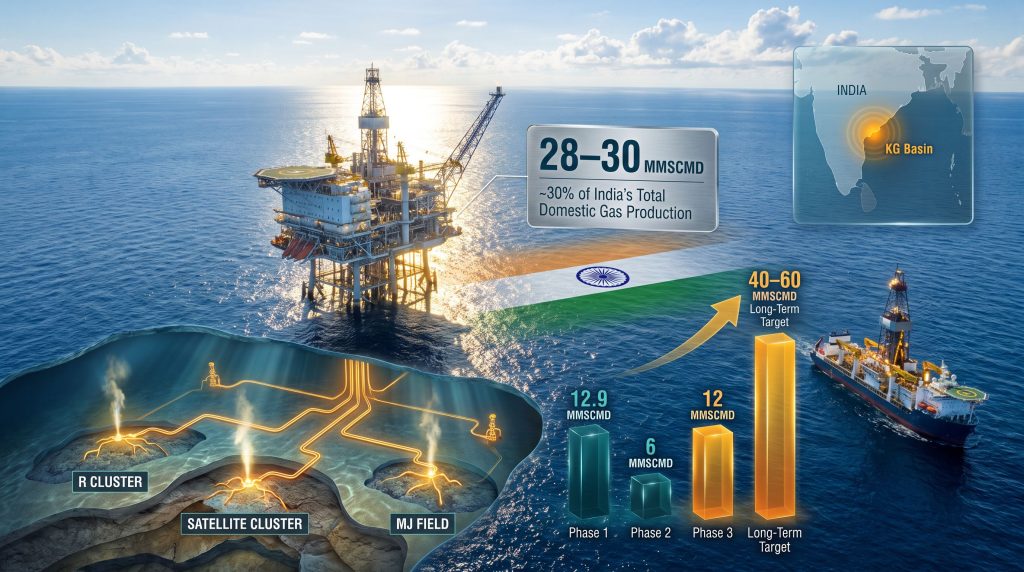

The KG-D6 block currently produces approximately 28 to 30 MMSCMD of natural gas across its three active fields, a volume that satisfies an estimated 15% of India's total gas demand and represents approximately 30% of domestic production.

How the Three-Phase Development Programme Was Built

The architecture of the KG-D6 development programme reflects careful sequencing designed to manage subsea execution risk while building toward a sustained production plateau. Each phase targeted distinct reservoir clusters with different pressure regimes and well configurations.

| Phase | Field | First Production | Peak Output |

|---|---|---|---|

| Phase 1 | R Cluster | December 2020 | ~12.9 MMSCMD |

| Phase 2 | Satellite Cluster | Mid-2021 | ~6 MMSCMD |

| Phase 3 | MJ Field | Q1 FY24 (April 2023) | ~12 MMSCMD |

Phase 1 targeted the R Cluster, originally scheduled for commissioning in May 2020 before COVID-19 pandemic disruptions pushed first gas to December of that year. The Satellite Cluster followed in mid-2021, adding a secondary production stream that diversified reservoir exposure within the block. The MJ Field, the third and most technically complex phase, completed the ramp-up in Q1 FY24, bringing combined block output to the 30 MMSCMD target plateau.

The financial scale of this build-out is significant. Approximately $5 billion has already been deployed to bring all three fields into production. Total approved capital expenditure across the block stands at $8.8 billion, with $5.6 billion committed to date. The remaining allocation headroom provides the financial framework for the next phase of the Reliance KG-D6 gas production plan.

The recoverable reserves underpinning this three-phase programme total approximately 3 trillion cubic feet (tcf), a resource base substantial enough to support multi-decade production if managed effectively.

The BP Partnership: Technical Depth Behind the Development Strategy

Reliance operates KG-D6 in joint venture with BP, a partnership that brings international deep-water technical expertise directly into the reservoir management and well design process. BP's global subsea engineering capability is particularly relevant for deep-water completions where wellbore stability, sand control, and flow assurance in cold, high-pressure environments require specialised competencies that few operators possess.

The joint venture structure also distributes capital risk across a major international partner, providing additional financial resilience for an investment programme of this scale. New well sanction decisions and expansion phase approvals flow through joint venture governance frameworks, meaning BP's technical assessment carries material weight in shaping the production growth trajectory.

Natural Decline and the Operational Case for New Drilling

One of the less widely understood aspects of deep-water gas production is the nature of reservoir pressure decline. Unlike onshore gas fields where operators can sometimes sustain output through compression alone, deep-water reservoirs in turbidite and channelised sand systems tend to exhibit steeper decline curves once pressure support diminishes. Without active well intervention and infill drilling, plateau production at KG-D6 would erode meaningfully over a three to five year horizon.

This is the operational rationale behind the approved four-well drilling programme. Reliance has received government approval to drill three new wells within the R Cluster and one within the Satellite Cluster, targeting an additional 240 billion cubic feet (BCF) of recoverable gas from existing reservoir structures. The expected production impact is an incremental 4 to 5 MMSCMD of additional capacity layered onto current output levels.

The R Cluster focus is geologically logical. The R Cluster reservoirs are deep-water fan deposits with heterogeneous sand distribution, meaning that infill wells targeting previously unswept compartments can access bypassed gas that existing producing wells have not drained. This is a common and technically well-understood strategy in mature deep-water developments globally.

Beyond the deep-water programme, Reliance is simultaneously prosecuting a 40-well multilateral drilling programme across its coal-bed methane blocks. CBM represents a fundamentally different production mechanism: gas is held within coal cleats and matrix by reservoir pressure, and production depends on dewatering the formation to allow gas desorption. Multilateral well designs in CBM improve drainage area and reduce the capital cost per unit of gas recovered, making them the preferred approach for large-scale CBM development.

Geopolitical Pricing Dynamics and the Revenue Environment

The timing of the Reliance KG-D6 gas production plan expansion intersects with a materially altered pricing environment shaped by geopolitical disruption. The conflict in West Asia triggered significant disruption to LNG trade flows transiting the Strait of Hormuz corridor, stranding volumes and compressing supply to Asian import terminals. Benchmark gas prices surged in response, and understanding the broader natural gas price trends helps contextualise why these dynamics matter so much for KG-D6's investment case.

For KG-D6 specifically, the applicable ceiling price currently sits at $8.9 per mmBtu, approximately one dollar below the prior half-year level. However, management at Reliance has indicated an expectation that this ceiling price will trend toward $9.9 per mmBtu in the second half of the year, driven by continued geopolitical price support flowing through benchmark price mechanisms.

Sanjay Barman Roy, President of E&P at Reliance Industries, indicated on an earnings call in July 2026 that sustained regional escalation is expected to keep gas prices elevated, with the KG-D6 ceiling price anticipated to rise by at least $1 per mmBtu based on management's assessment of the geopolitical situation.

This creates an unusual investment dynamic. Higher prices improve revenue realisation per unit of gas produced, directly enhancing the project economics for incremental drilling. The four approved wells and any subsequent phases therefore carry better expected returns today than they would have in a pre-conflict pricing environment. Consequently, the energy trade disruption risks stemming from regional conflict have paradoxically strengthened the strategic case for accelerating domestic production.

India's Demand Paradox: Lower Consumption, Higher Prices

The demand picture complicates the revenue narrative in an instructive way. Domestic gas consumption in India declined approximately 10% year-on-year during the June quarter of FY26. Reliance management attributed this contraction to the disruption of traditional LNG import routes caused by regional tensions, which reduced the total gas available to the Indian market and suppressed consumption volumes rather than reflecting a structural demand pullback.

This creates a near-term paradox worth examining carefully:

- Higher prices improve per-unit revenue for KG-D6 production

- Lower consumption volumes reduce the total demand pool being served

- The shortfall in import supply positions domestic producers like KG-D6 as even more critical to market stability

- As supply route disruptions resolve, demand recovery is likely to absorb incremental production rapidly

The 10% demand decline is widely assessed as cyclical rather than structural, underpinned by India's long-term gas demand growth trajectory across city gas networks, industrial fuel switching, and power generation.

The Capital Efficiency Argument: $1.5 Billion Against $60 Billion

Perhaps the most compelling dimension of the Reliance KG-D6 gas production plan is the implied capital efficiency of incremental investment. An estimated additional $1 to $1.5 billion in capital expenditure could unlock access to approximately 4 to 5 tcf of additional gas reserves across the block's identified but undeveloped structures.

The scale of the LNG import substitution value this represents is striking. Over the productive life of those reserves, the gas volumes produced domestically could substitute approximately $60 billion in LNG import costs for India at current price benchmarks. This implies an LNG import substitution ratio of roughly 40 to 60 times the incremental capital outlay, a return profile that is extraordinarily difficult to replicate through alternative supply pathways.

For context, LNG import substitution at this scale would also reduce India's foreign exchange outflow substantially, improve the current account balance, and insulate the domestic gas market from the kind of supply route disruption that compressed consumption by 10% in Q1 FY26.

In addition, when viewed alongside the global LNG supply outlook, which remains constrained by delayed project approvals and infrastructure bottlenecks, the strategic value of domestic production becomes even clearer for energy-importing nations like India.

The next major ASX story will hit our subscribers first

Long-Term Production Ambition: The Path to 40-60 MMSCMD

The near-term target sits at a 30 to 35 MMSCMD output band, achievable through the existing three fields combined with the four approved infill wells. The longer-term strategic horizon extends considerably further.

| Growth Horizon | Target Output | Key Enabler |

|---|---|---|

| Near-term plateau | 30 to 35 MMSCMD | Existing fields plus 4 new wells |

| Medium-term expansion | 40+ MMSCMD | New deep-sea discoveries |

| Long-term potential | 40 to 60 MMSCMD | Common infrastructure optimisation |

Reaching the 40 to 60 MMSCMD range requires new deep-water discoveries within the KG Basin to be brought into production through shared infrastructure. The economic logic of common infrastructure is powerful in deep-water environments. Subsea pipelines, floating production vessels, and onshore processing terminals represent fixed-cost assets that become progressively more efficient as throughput volumes increase.

New field tie-backs to existing KG-D6 infrastructure carry substantially lower development costs per unit of gas than standalone greenfield developments would. A strategy centred on unlocking a further 30 to 35 MMSCMD of incremental capacity through new discoveries tied into the existing KG-D6 infrastructure backbone is under joint development between Reliance and relevant stakeholders. If realised, the combined output would materially reshape India's domestic gas supply balance and significantly reduce structural dependence on LNG imports. Moreover, Australia's own energy export challenges demonstrate how critical it is for major producers to sustain investment in proven basins rather than allow infrastructure to sit underutilised.

The Downstream Consequence: Stranded Power Capacity

One dimension of the KG-D6 production story that receives insufficient attention is its direct connection to India's gas-fired power sector. Approximately 8,000 MW of gas-fired power generation capacity across India currently operates below its design utilisation rate, not because of mechanical issues, but because adequate domestic gas supply at economically viable prices is unavailable.

Sustained KG-D6 output above 30 MMSCMD represents one of the few credible near-term pathways to improving fuel availability for these plants. The economics of domestic gas versus imported LNG for power generation are materially different. When domestic gas is priced below LNG import parity, gas-to-power economics improve substantially, potentially restoring commercial viability to plants that are currently underutilised or burning LNG at margins that make generation uneconomic.

Beyond power generation, incremental KG-D6 gas is being directed toward priority sectors including:

- Fertiliser manufacturing, where gas is a primary feedstock and domestic supply reduces subsidy burdens

- City gas distribution networks, supporting clean cooking fuel expansion across urban and peri-urban areas

- Industrial fuel switching programmes targeting emissions reduction in energy-intensive sectors

This priority sector allocation framework provides an additional layer of demand certainty for upstream investment planning, as offtake from these sectors tends to be more price-inelastic than power generation.

Frequently Asked Questions: Reliance KG-D6 Gas Production Plan

What is the current production level from KG-D6?

The three active fields within the block — the R Cluster, Satellite Cluster, and MJ Field — are collectively producing approximately 28 to 30 MMSCMD of natural gas. This represents around 30% of India's total domestic gas production and satisfies an estimated 15% of total national gas demand.

What is the current ceiling price for KG-D6 gas?

The ceiling price applicable to KG-D6 gas currently stands at $8.9 per mmBtu. Reliance management expects this to trend toward approximately $9.9 per mmBtu in the second half of the year, reflecting geopolitical benchmark price movements.

How many new wells has Reliance been approved to drill?

Reliance has received government approval to drill four new wells, comprising three within the R Cluster and one within the Satellite Cluster. These wells are designed to recover an additional 240 BCF of gas and add an estimated 4 to 5 MMSCMD of incremental production capacity.

What is the long-term production target for the block?

The near-term target is 30 to 35 MMSCMD. The longer-term strategic ambition extends to 40 to 60 MMSCMD, contingent on new deep-sea discoveries being brought into production through the block's shared infrastructure.

How much capital has been invested in KG-D6 to date?

Approximately $5 billion has been deployed to bring the three producing fields online. Total approved capital expenditure across the block stands at $8.8 billion, with $5.6 billion committed to date.

Why did India's domestic gas consumption fall in Q1 FY26?

Domestic gas consumption declined approximately 10% year-on-year in the June quarter of FY26. Reliance management attributed this contraction to supply chain disruptions caused by regional geopolitical tensions affecting traditional LNG import routes rather than any structural shift in demand fundamentals.

This article contains forward-looking statements and management projections sourced from publicly available earnings commentary and industry reporting. Production targets, price forecasts, and capital expenditure estimates are subject to change based on reservoir performance, geopolitical developments, regulatory outcomes, and market conditions. This article does not constitute financial advice. Readers should conduct independent research before making investment decisions.

Want to Identify the Next Major Energy Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including energy commodities — instantly translating complex geological and market data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.