May 14, 2026

Why Copper's Earnings Season Reveals More Than Just Commodity Prices

The mining sector has a habit of telling two stories simultaneously: one visible on the surface, another buried deeper in the financial statements. For investors trying to read the copper market in 2025, understanding which story matters more has rarely been as consequential as it is right now. Integrated copper producers operating across multiple jurisdictions, currencies, and commodity streams present a particularly layered picture, where headline profit figures and underlying operational momentum can point in opposite directions within the same reporting period.

Furthermore, the copper supply crunch that has been building across global markets adds another layer of complexity to interpreting quarterly earnings. This dynamic is precisely what makes the first-quarter 2025 results from KGHM Polska Miedź S.A. so instructive. Poland's dominant copper and silver mining group delivered a result that simultaneously beat and missed expectations, depending entirely on which metric investors chose to prioritise.

For those focused on operational cash generation, it was a standout quarter. For those anchored to net profit, the picture was more complicated. Navigating that distinction is central to understanding what the numbers actually mean.

When big ASX news breaks, our subscribers know first

KGHM Q1 Core Profit Beats Forecasts: Breaking Down a Complex Quarter

Adjusted Core Profit Surges Past Analyst Expectations

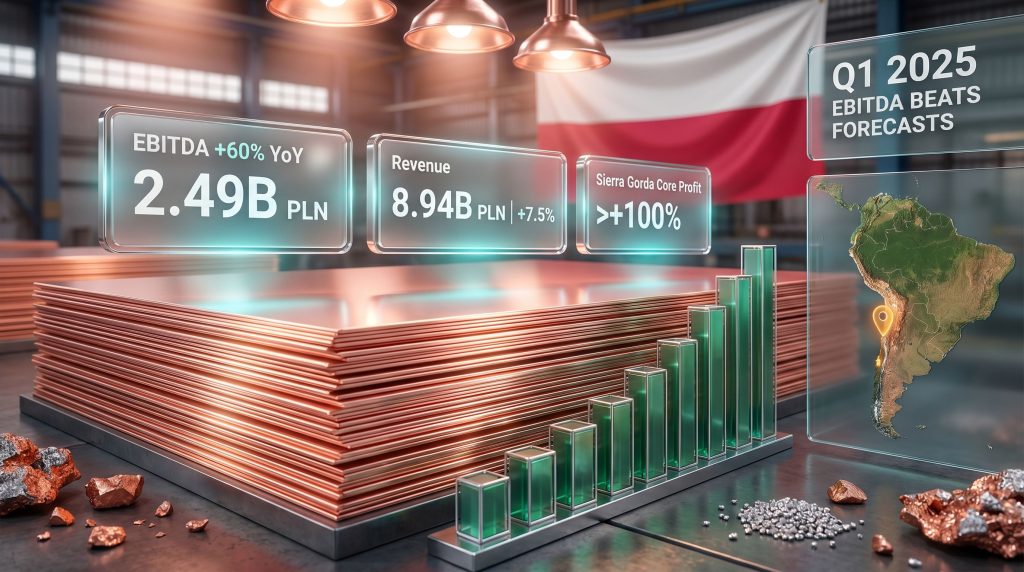

KGHM Q1 core profit beats forecasts on the operational front, and the headline from the January to March 2025 earnings release was unambiguous. Adjusted core profit for the period reached 5.46 billion zlotys (approximately $1.51 billion USD), significantly exceeding analyst consensus forecasts. This figure was primarily powered by the performance of KGHM's core Polish operations, where adjusted core profit more than tripled compared to the same period in the prior year, according to Reuters reporting via Kitco News.

The catalyst behind this surge was a combination of higher copper and silver spot prices amplifying revenue per tonne produced, alongside the positive effect of currency hedging strategies that partially cushioned the impact of a weakening US dollar on Polish zloty-denominated revenues. For a company that sells the majority of its production in USD while incurring a significant portion of operating costs in PLN, this hedging strategy played a material role in protecting margins.

Net profit for the same period climbed more than tenfold to 3.53 billion zlotys, substantially exceeding the 2.33 billion zloty estimate seen in a Reuters analyst poll. At the time of the report, the exchange rate stood at $1 = 3.6274 zlotys, providing useful context for USD-equivalent comparisons.

The Anatomy of a Vertically Integrated Copper Producer

To appreciate why KGHM's results carry significance beyond Polish borders, it helps to understand the structural nature of its operations. Unlike pure-play miners that sell ore or concentrate to third-party smelters, KGHM operates as a vertically integrated producer. It mines copper ore, processes it through its own smelting and refining infrastructure, and delivers finished copper products directly to industrial customers.

This integration creates a distinct cost and margin profile:

- Vertical integration captures value at each production stage rather than surrendering margin to third-party processors

- Fixed-cost smelting infrastructure means that production volume changes have an outsized impact on per-unit margins

- When copper prices rise, the leverage effect across an integrated value chain amplifies profit growth disproportionately relative to price increases alone

- Currency exposure is concentrated at the revenue line (USD-priced copper) while costs are split between PLN domestically and USD internationally

KGHM's operations span three principal geographic areas: the Legnica-Glogow Copper Belt in Poland, which hosts its core mining and smelting infrastructure; the Sierra Gorda joint venture in Chile's Atacama Desert; and various North American assets. This geographic spread introduces different cost structures, regulatory environments, and currency exposures into a single consolidated reporting entity.

Understanding the EBITDA-to-Net-Profit Divergence in Mining

Why Adjusted Core Profit Is the Preferred Lens for Operational Assessment

One of the most important analytical frameworks for evaluating integrated mining companies involves understanding why adjusted core profit (often aligned with EBITDA) and statutory net profit can diverge so dramatically within the same quarter. For investors unfamiliar with the mechanics of capital-intensive resource extraction, this gap can appear alarming when it is often explainable through predictable accounting factors. In fact, the broader relationship between commodity prices and mining performance is one that rewards patient, methodical analysis.

In capital-intensive industries like copper mining, adjusted core profit strips away depreciation, amortization, interest charges, and tax impacts, all of which can be heavily distorted by debt structure, asset age, and one-off accounting events. The result provides a cleaner window into the actual cash-generating capacity of the operations themselves.

The four most common factors that create divergence between operational profitability and reported net profit in mining companies are:

-

Foreign exchange translation effects: Revenue earned in USD must be converted to the reporting currency (PLN for KGHM), and when the USD weakens relative to the PLN, the translated value of revenue falls even if underlying volumes and USD prices remain strong.

-

Depreciation and amortization: Mining assets are depreciated over their useful lives, and large capital investments in smelting infrastructure or mine development create substantial non-cash charges that reduce net profit without affecting operational cash flows.

-

Deferred tax positions: Tax liabilities can fluctuate based on asset revaluations, changes in effective tax rates across jurisdictions, or temporary timing differences between accounting income and taxable income.

-

Joint venture accounting: In structures like Sierra Gorda, KGHM's proportional share of the JV's profit or loss flows through its consolidated statements, meaning a net loss at the JV level depresses group net profit even when the operation generates positive EBITDA.

For professional investors and analysts covering the mining sector, adjusted core profit is the standard comparative metric precisely because it isolates these accounting distortions.

Sierra Gorda: The International Wildcard in KGHM's Portfolio

How a Chilean Copper Mine Shapes Polish Financial Results

The Sierra Gorda copper-molybdenum-gold mine in Chile's Region II, in which KGHM holds a 55% controlling interest through a joint venture with Sumitomo Metal Mining, represents both the most significant source of geographic diversification and one of the most complex variables in KGHM's financial reporting. Indeed, Chile's copper supply gap has broader implications for producers operating in the region, making Sierra Gorda's performance all the more strategically important.

Located at high altitude in one of the world's driest desert environments, Sierra Gorda processes a large-tonnage, lower-grade porphyry copper deposit. This geological profile is typical of South American copper porphyries, which are characterised by:

- Large resource bases measured in hundreds of millions to billions of tonnes

- Relatively low copper head grades, typically ranging from 0.3% to 0.6% copper equivalent

- Significant molybdenum and gold by-product credits that meaningfully reduce net operating costs

- High capital intensity from large-scale milling and concentration infrastructure

- Sensitivity to reagent costs, water availability, and energy pricing in remote locations

By-product credits from gold and molybdenum production at Sierra Gorda can substantially reduce the all-in sustaining cost per pound of copper equivalent produced. This is why quarterly fluctuations in gold and molybdenum prices matter to KGHM's group economics even though copper remains the primary revenue driver.

During Q1 2025, Sierra Gorda delivered a standout performance contribution, with its core profit result more than doubling relative to the prior year period, driven by increased output volumes alongside favourable spot pricing for copper and gold. This represented a material positive swing after periods where the JV had weighed on group financials.

KGHM's Strategic Expansion: Securing Ore Supply for the Long Term

The Morocco and Europe Acquisition Strategy Explained

One of the most strategically significant disclosures from KGHM's April 2025 communications was the company's stated objective to pursue mining asset acquisitions in Europe and Morocco. This ambition reflects a structural vulnerability that has historically characterised European smelter-based copper producers: the dependence on imported copper concentrate from geographically distant mine operations.

KGHM's Polish smelting infrastructure, centred on the Legnica and Glogow smelters, requires a consistent supply of copper concentrate feed. By acquiring mines geographically closer to its Polish processing infrastructure, the company aims to:

- Reduce ore transport distances and associated freight costs

- Improve control over feed quality and consistency, which matters for smelter efficiency

- Reduce exposure to global concentrate trading market volatility

- Build a more vertically secure supply chain ahead of anticipated tightening in global copper concentrate availability

The Morocco angle is particularly interesting from a geological perspective. Morocco hosts significant polymetallic mineralisation, including copper-bearing skarn and sediment-hosted deposits in the Anti-Atlas region, some of which have historically been underexplored relative to their potential. Proximity to European smelting infrastructure via Mediterranean shipping routes makes Moroccan assets logistically attractive compared to Chilean or Congolese alternatives.

Copper's Structural Demand Drivers: Why 2025 Results Matter Beyond One Quarter

The Industrial Megatrends Amplifying Copper Producer Margins

KGHM Q1 core profit beats forecasts did not occur in isolation. It reflected a broader environment in which copper's role in the global industrial economy has structurally expanded beyond its traditional applications in construction and electrical wiring. The copper price growth drivers underpinning this expansion are now well established across institutional investment research.

Three demand categories are reshaping copper consumption at scale:

| Demand Category | Copper Intensity | Growth Driver |

|---|---|---|

| Electric Vehicles (Battery EVs) | ~83 kg per vehicle vs ~23 kg in combustion engines | Accelerating EV adoption across major markets |

| Power Grid Infrastructure | ~5 tonnes per MW of transmission capacity | Grid modernisation and renewable integration |

| Renewable Energy Generation | ~3-5 tonnes per MW (onshore wind/solar) | Energy transition capex cycles globally |

This demand expansion is colliding with a supply side that faces structural constraints. Many of the world's largest copper mines are ageing, with declining ore grades requiring more material to be processed per tonne of copper produced. Processing more ore at lower grades requires more energy, more reagents, and more capital expenditure to maintain output.

For integrated producers like KGHM with established, permitted, and operating infrastructure, this environment creates a sustained period of margin expansion as higher spot prices flow through to operational cash generation faster than new supply can enter the market.

The next major ASX story will hit our subscribers first

Hedging Strategy as a Margin Management Tool

Why Currency Hedging Is Both a Shield and a Constraint

KGHM's confirmation that its currency hedging programme partially offset USD weakness during Q1 2025 highlights a nuanced dimension of how European copper producers manage earnings volatility. The core challenge is structural: copper is a globally traded commodity priced in USD, but KGHM's largest cost base (labour, energy, domestic services) is denominated in PLN.

When the USD weakens against the PLN, the PLN value of each tonne of copper sold falls, compressing margins even when copper spot prices in USD terms remain elevated. Currency hedging using forward contracts or options allows KGHM to lock in exchange rates for a portion of its future USD revenue streams, providing earnings visibility but also capping the upside during periods of USD strength.

The Q2 2025 period illustrated the flip side of this dynamic, when a strengthening PLN and persistent USD softness created headwinds that compressed reported net profit even as production volumes remained on target. This highlights why consecutive quarterly results from currency-exposed commodity producers should be evaluated as part of a multi-period trend rather than in isolation.

Key Metrics and Monitoring Framework for Investors

What to Watch in Future KGHM Reporting Periods

Investors and industry observers tracking KGHM's trajectory in the wake of its Q1 2025 results should consider a range of copper investment strategies and monitor several interconnected variables:

- Copper spot price levels: Sustained prices above the $4.50 per pound threshold provide the pricing environment necessary for continued EBITDA outperformance at Polish domestic operations

- Sierra Gorda production volumes and unit costs: Recovery and growth at the Chilean JV is central to closing the gap between group adjusted core profit and reported net profit

- PLN/USD exchange rate movements: Given the structural revenue-cost currency mismatch, exchange rate trends remain one of the highest-impact variables on quarterly earnings

- Electrolytic copper production at Polish operations: Reversing the decline in domestic output is an operational priority that will determine whether volume can supplement price as a growth driver

- M&A progress in Europe and Morocco: Successful acquisition of ore-supplying assets would represent a structural improvement in KGHM's long-term cost profile and supply security

According to KGHM's investor results centre, the company remains committed to transparent financial reporting across its diversified asset base, providing investors with the granular data needed to assess performance across each operational segment independently.

The broader signal from KGHM's Q1 2025 results is that commodity price leverage, geographic diversification, and disciplined financial risk management can produce material earnings beats even when specific operational metrics face headwinds. The divergence between adjusted core profit and net profit warrants ongoing monitoring, but it does not diminish the operational quality of the underlying quarter or the structural positioning of the company within a tightening global copper market.

This article is intended for informational and educational purposes only and does not constitute financial advice or a solicitation to trade in any financial instrument. All financial figures referenced are sourced from Reuters reporting via Kitco News. Past performance of commodity prices or company earnings is not indicative of future results. Readers should conduct their own due diligence and consult qualified financial advisors before making investment decisions.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex geological and commodity data into actionable investment insights — explore the historic returns generated by major mineral discoveries to understand the scale of opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.