June 11, 2026

The Anatomy of a Chokepoint: Why Kharg Island Sits at the Centre of Global Energy Risk

Most energy market disruptions begin at the margins, affecting secondary pipelines, minor terminals, or regional distribution networks. The geopolitical confrontation now unfolding between Washington and Tehran is fundamentally different in one critical respect: Trump threatens strikes on Iran's Kharg Island oil export hub, and the asset being threatened sits directly at the heart of a major oil-exporting nation's entire export architecture. When a single facility processes the overwhelming majority of a country's petroleum shipments, it ceases to function as infrastructure alone. It becomes a sovereign pressure point, a fiscal mechanism, and a geopolitical lever simultaneously.

That is precisely the position Kharg Island occupies in Iran's energy economy. Located approximately 25 kilometres off Iran's southwestern coast in the Persian Gulf, the island has served as the backbone of Iranian crude exports for decades. Its loading terminals, pipeline connections to onshore production fields, and tanker throughput capacity make it not merely convenient but essentially irreplaceable within Iran's current export configuration. An estimated 85 to 95% of Iran's total crude oil export volume moves through Kharg, meaning the terminal does not support Iran's petroleum commerce so much as it constitutes it.

Understanding why this single island commands such disproportionate strategic weight requires appreciating how Iran's oil infrastructure evolved. Following the 1979 revolution and the subsequent Iran-Iraq War during the 1980s, Iranian export capacity was severely damaged across multiple terminal locations. Kharg Island, despite absorbing strikes during the so-called Tanker War period of the mid-1980s, was rebuilt and expanded to become the singular dominant hub for outbound crude, reflecting both geographic advantage and infrastructure investment decisions made over several subsequent decades.

Iran's Oil Export Dependency: A Macro Snapshot

| Metric | Estimated Figure |

|---|---|

| Share of exports via Kharg Island | 85–95% |

| Iran's approximate crude export volume | ~1.5–1.7 million bpd |

| Global oil supply share (Iranian crude) | ~1.5% of global supply |

| Distance from Iran's southwestern coast | ~25 kilometres |

"Kharg Island is not merely an oil terminal. It is the financial lifeline of the Iranian state. Any sustained disruption to its operations would cascade directly into Iran's fiscal capacity, military funding, and geopolitical leverage."

At approximately 1.5 to 1.7 million barrels per day of crude exports, Iran contributes roughly 1.5% of global oil supply. That percentage may appear modest in isolation, but energy markets do not respond to supply disruptions in linear proportion to percentage share. Tight global inventory conditions, the speed of alternative supply mobilisation, and the psychological amplification effect of conflict in a historically volatile region all serve to magnify the market impact of even relatively small absolute supply removals. Furthermore, understanding the broader oil price rally risks in this environment is essential context for any market participant tracking this situation.

When big ASX news breaks, our subscribers know first

How Did Trump's Threats Against Iran's Kharg Island Oil Export Hub Reach This Point?

The immediate trigger for the current escalation cycle was the collapse of a two-month ceasefire that had broadly held since April 2026. According to reporting from World Oil, the breakdown followed Iran downing a U.S. military helicopter, an incident that set off retaliatory military exchanges from both sides. What began as a ceasefire violation has since accelerated into a confrontation with a qualitatively different character: the explicit targeting of economic infrastructure rather than purely military assets.

On June 11, 2026, President Trump publicly declared that the United States would strike Iran's key oil hub again and simultaneously raised the prospect of the U.S. taking control of Kharg Island and other Iranian oil infrastructure assets. The framing of this declaration deserves careful analytical attention. Previous U.S. pressure on Iran's energy sector has operated primarily through the financial system via sanctions, restricting access to dollar-clearing mechanisms, tanker insurance, and international banking relationships. Threatening physical seizure or destruction of the terminal itself represents a fundamentally different category of action.

Subsequent statements, however, introduced notable ambiguity into the picture. In television commentary following the initial social media post, Trump questioned whether the United States possessed the resolve for a prolonged conflict over the island. That qualification matters enormously from both a military planning perspective and a market assessment standpoint.

"The gap between a leader's social media declaration and subsequent measured television commentary reflects a pattern of strategic ambiguity. This posture simultaneously functions as a deterrent signal and a negotiating lever, without committing to irreversible action."

This distinction between declaratory posture and operational intent is well established in geopolitical analysis. Aggressive public statements can serve multiple strategic functions simultaneously: signalling resolve to domestic audiences, pressuring adversaries to recalibrate their threat assessments, and creating negotiating leverage without triggering irreversible escalation. The difficulty from a market perspective is that strategic ambiguity, by design, resists straightforward interpretation.

What Would Trump's Threats Against Iran's Kharg Island Oil Export Hub Mean for Global Oil Supply?

Modelling the Market Impact: Three Escalation Scenarios

The range of potential outcomes from any military action against Kharg Island spans an enormous spectrum, from a temporary loading disruption lasting days to a sustained regional conflict affecting the entirety of Persian Gulf energy flows. Structuring the analysis around three plausible scenarios helps frame the risk asymmetry energy market participants are currently navigating. Consequently, tracking oil price movements in real time becomes critical for investors and analysts alike.

Scenario 1: Targeted Disruption (Limited Strike)

A partial strike causing damage to specific loading infrastructure without a complete terminal shutdown would likely remove an estimated 500,000 to 800,000 barrels per day from global markets during the repair period. Historical precedent from infrastructure damage events suggests Brent crude could spike $10 to $20 per barrel within 48 to 72 hours of confirmed disruption, with the price trajectory thereafter depending heavily on repair timelines, OPEC+ response speed, and diplomatic signalling.

Scenario 2: Full Terminal Incapacitation

Complete destruction or seizure of Kharg's loading and storage systems would effectively halt Iranian crude exports for an extended period, potentially months to years depending on the nature and extent of infrastructure damage. Under this scenario, the potential Brent crude price response is estimated at $20 to $40 or more per barrel, with secondary effects including dramatic increases in tanker war risk insurance premiums across the entire Persian Gulf and a fundamental repricing of the risk premium embedded in all regional energy flows.

Scenario 3: Regional Escalation Involving the Strait of Hormuz

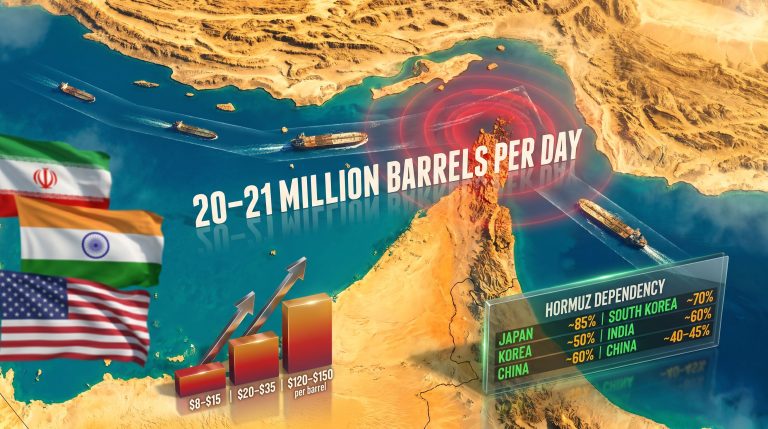

The most severe scenario involves Iranian retaliation targeting Gulf Cooperation Council energy infrastructure or an attempt to restrict transit through the Strait of Hormuz. Approximately 20% of globally traded oil transits through this narrow maritime passage. A credible closure attempt would transform a bilateral confrontation into a global energy security emergency, likely triggering International Energy Agency (IEA) strategic petroleum reserve releases and diplomatic mobilisation from major Asian importers who are the primary customers for Persian Gulf crude.

Scenario Comparison Table

| Scenario | Supply Impact | Estimated Price Spike | Recovery Timeline |

|---|---|---|---|

| Limited Strike | 500K–800K bpd | +$10–$20/bbl | Weeks to months |

| Full Incapacitation | ~1.5M+ bpd | +$20–$40+/bbl | Months to years |

| Regional Escalation | 20%+ of global trade | Extreme volatility | Indeterminate |

A less-discussed but analytically important dimension of the full incapacitation scenario concerns the cascade effects on tanker routing and insurance. The Persian Gulf carries crude not only from Iran but from Saudi Arabia, Iraq, Kuwait, the UAE, and Qatar. A conflict-driven escalation in war risk premiums would increase shipping costs for all regional exports, effectively functioning as a supply-side tax on the broader Gulf energy complex regardless of whether non-Iranian terminals sustain direct damage.

Who Bears the Greatest Risk if Kharg Island Is Disrupted?

Asia's Import Dependency: The Overlooked Vulnerability

The geographic distribution of Persian Gulf crude consumption reveals that the countries bearing the greatest economic exposure to a Kharg disruption are predominantly in Asia rather than the Western nations more directly involved in the current confrontation. China, India, Japan, and South Korea collectively represent the dominant destination markets for Persian Gulf crude exports.

A sustained disruption forcing Asian refiners to seek alternative supply would trigger competitive purchasing across West African, American, and Russian crude streams simultaneously. The resulting surge in freight rates, combined with potential refinery configuration mismatches as facilities optimised for Middle Eastern crude grades attempt to process alternative feedstocks, would compress refining margins and transmit inflationary pressure through Asian manufacturing supply chains.

-

China depends heavily on Middle Eastern crude for its refinery complex and would face both supply and pricing pressure from any significant Kharg disruption.

-

India has substantially increased its Persian Gulf crude intake in recent years and lacks the short-term flexibility to substitute volumes at the scale required.

-

Japan and South Korea operate highly efficient refinery systems calibrated to specific crude grades, making rapid feedstock substitution technically complex and commercially costly.

European Energy Security Considerations

European markets, still recalibrating their supply architecture following the restructuring necessitated by reduced Russian energy flows, face a compounded vulnerability from any Persian Gulf disruption. LNG import capacity, while expanded in recent years, remains insufficient to fully offset a major crude supply shock at pace. The interaction between a potential oil supply crisis and existing energy security strains in Europe introduces the possibility of concurrent pressure across multiple fuel types.

In addition, the broader US-China trade war impacts on energy demand and supply chains add another layer of complexity to how global markets would absorb a Persian Gulf supply shock of this magnitude.

The OPEC+ Response Calculus

Saudi Arabia and the UAE collectively hold an estimated 3 to 4 million barrels per day of spare production capacity, which represents the most significant available buffer against an Iranian supply disruption. However, deploying that capacity rapidly carries its own complexities:

-

Bringing spare capacity online at maximum speed risks reservoir management complications that Gulf producers have consistently sought to avoid.

-

A rapid Saudi or Emirati response to offset Iranian losses could be interpreted by Tehran as geopolitical coordination with Washington, potentially widening the conflict.

-

Even at maximum deployment pace, full replacement of a complete Kharg shutdown would take weeks, during which market disruption would persist.

Is Seizing Kharg Island Militarily and Legally Feasible?

Military Feasibility Assessment

The distinction between striking Kharg Island from the air and physically seizing and operating it as a controlled asset represents one of the most significant analytical gaps in public commentary on the current crisis. An airstrike, however precise, is a fundamentally different operational proposition from sustained occupation and operational control of an active energy terminal.

Seizing Kharg Island would require establishing and maintaining naval and ground force presence on Iranian territory against active resistance, managing the physical infrastructure of a functioning crude export terminal under conflict conditions, and defending that position against sustained Iranian counterattack. No modern military power has successfully seized and operated hostile energy infrastructure at scale in an active conflict environment. The logistical, legal, and operational challenges involved would represent a commitment orders of magnitude greater than punitive airstrikes.

Legal and International Law Dimensions

The legal framework governing attacks on critical infrastructure during armed conflict is complex, and the seizure scenario introduces questions that extend beyond conventional military law analysis. Furthermore, the trade war impact on oil already reshaping global energy markets means this legal uncertainty arrives at a moment of compounding geopolitical stress.

-

Seizure of sovereign energy infrastructure outside a formal declaration of war raises significant questions under the UN Charter's prohibitions on the use of force.

-

International humanitarian law places constraints on attacks against objects indispensable to civilian economic survival, even in conflict settings.

-

Allied nations and multilateral institutions would face pressure to respond to a seizure of sovereign infrastructure, potentially fracturing coalition support for U.S. regional positioning at a moment of significant geopolitical sensitivity.

"The distinction between denying Iran oil revenue through financial sanctions versus physically controlling Iranian export infrastructure is not merely tactical. It represents a fundamental redefinition of declared war aims with profound implications for international energy law and sovereignty norms."

This legal dimension has practical market consequences. If major international legal authorities characterise infrastructure seizure as unlawful under international law, major energy trading companies, banks providing trade finance, and tanker operators would face significant legal exposure in participating in any commercially-oriented operation of a seized terminal. That friction would substantially complicate the operational and financial logic of infrastructure seizure even if the military action itself succeeded.

How Are Energy Markets Pricing This Risk Right Now?

Oil Price Sensitivity to Persian Gulf Conflict Signals

Energy markets have historically demonstrated rapid but sometimes short-lived price responses to Persian Gulf conflict rhetoric. The pattern is well established: initial price spikes driven by uncertainty and risk premium expansion, followed by moderation as the gap between political statements and operational military action becomes apparent. The credibility of the threat is the central variable traders are assessing in real time.

Trump's dual-channel signalling creates a specific challenge for market participants. Aggressive social media statements followed by more measured television commentary introduce a volatility premium without providing directional clarity. This environment tends to reward positioning strategies that benefit from elevated implied volatility rather than directional crude price bets.

Key Market Indicators to Watch

Sophisticated energy market participants are monitoring several leading indicators that provide real-time insight into institutional threat assessment:

-

Brent crude futures curve shape: Steepening backwardation signals intensifying near-term supply anxiety as spot demand for physical barrels outpaces forward month pricing.

-

Persian Gulf tanker war risk insurance premiums: These premiums, set by the Lloyd's market and other specialist underwriters, represent the shipping industry's quantified assessment of conflict risk and function as a real-time geopolitical risk barometer.

-

IEA and U.S. Strategic Petroleum Reserve posture: Any public signalling of pre-positioning for strategic reserve releases would indicate government-level anticipation of near-term supply disruption at a scale requiring emergency response mechanisms.

-

GCC sovereign wealth fund positioning: Adjustments to Gulf state institutional investment portfolios in equity or commodity markets provide indirect signals about how regional governments themselves are assessing escalation probability.

-

Strait of Hormuz vessel traffic data: Real-time tracking of tanker transit volumes through the Strait provides an operational ground-truth indicator of whether physical shipping disruption is already beginning to materialise independently of political statements.

The next major ASX story will hit our subscribers first

What Are the Prospects for a Negotiated Resolution?

Why Infrastructure Threats Complicate Peace Negotiations

The dynamics of ceasefire negotiation change substantially when existential economic assets are explicitly threatened. Iran's negotiating flexibility is structurally constrained when the primary export terminal underpinning its government budget is publicly designated as a potential military target. Under such conditions, making concessions risks being interpreted domestically as capitulation under existential threat, reducing the political viability of compromise outcomes that might otherwise be achievable.

As reported by World Oil, analysts assessing the situation have concluded that direct action against Kharg would represent a major escalation beyond shipping restrictions and would significantly complicate prospects for any negotiated settlement. This assessment reflects the well-documented phenomenon that targeting economic lifelines tends to harden adversarial resolve rather than incentivise concession.

Third-party mediators historically active in U.S.-Iran back-channel diplomacy, including Oman and Qatar, face increased operational difficulty when infrastructure threats dominate the public narrative. Their effectiveness depends partly on maintaining perceived neutrality and constructive engagement from both parties, conditions that become harder to sustain when one party has publicly framed the other's primary economic asset as a military objective.

Conditions Required for Ceasefire Restoration

A viable pathway back to ceasefire would likely require several concurrent developments:

-

Mutual de-escalation signals from both military command structures, including verifiable stand-downs of offensive postures.

-

Re-engagement of existing back-channel diplomatic frameworks through intermediary nations with credibility on both sides.

-

Suspension of infrastructure-targeting rhetoric as an explicit precondition for substantive talks, allowing both parties to claim progress without conceding on core positions.

-

Potential engagement of international energy institutions including the IEA and OPEC+ as indirect stabilisation mechanisms, providing a framework for discussing supply management that does not require direct bilateral negotiation on the core political disputes.

Frequently Asked Questions: Trump, Kharg Island, and Persian Gulf Energy Security

What is Kharg Island and why does it matter to global oil markets?

Kharg Island is Iran's principal crude oil export terminal, responsible for processing an estimated 85 to 95% of the country's petroleum export volume. Its strategic importance derives not just from its physical capacity but from its irreplaceable position in Iran's export infrastructure. Any sustained operational disruption would directly reduce global oil supply by an estimated 1.5 to 1.7 million barrels per day and trigger significant upward pressure on international crude prices.

What did Trump say about Kharg Island?

On June 11, 2026, President Trump stated publicly that the United States would strike Iran and raised the prospect of the U.S. taking control of Kharg Island and other Iranian oil infrastructure assets. Subsequent television commentary introduced uncertainty about the depth of U.S. operational commitment to such action, creating a pattern of strategic ambiguity that analysts and market participants are actively working to interpret.

How would a strike on Kharg Island affect oil prices?

Price impacts depend entirely on the severity and duration of any action. A limited, targeted disruption could trigger a $10 to $20 per barrel spike in Brent crude. Full incapacitation of the terminal could push prices $40 or more per barrel higher. A scenario involving broader Persian Gulf escalation, particularly any threat to the Strait of Hormuz, could produce extreme and difficult-to-model price volatility across global energy markets.

Could OPEC+ offset an Iranian supply disruption?

Saudi Arabia and the UAE collectively hold an estimated 3 to 4 million barrels per day of spare production capacity, which could partially cushion a supply shock. However, the pace of deployment, reservoir management constraints, and geopolitical sensitivities around being seen to benefit from Iranian losses would all limit the speed and scale of any compensating supply response.

What is the Strait of Hormuz and why does it matter here?

The Strait of Hormuz is the narrow maritime passage connecting the Persian Gulf to global shipping routes. Approximately 20% of globally traded oil transits through this chokepoint. Any Iranian action threatening Strait access would escalate the conflict from a bilateral confrontation into a global energy security emergency affecting every major oil-importing nation on earth.

Key Takeaways: The Strategic Stakes of Kharg Island

-

Kharg Island processes an estimated 85 to 95% of Iran's crude exports, making it the single most economically sensitive target in any U.S.-Iran military confrontation.

-

Trump threatens strikes on Iran's Kharg Island oil export hub in statements that represent a qualitative escalation in declared U.S. objectives, moving from financial sanctions and shipping restrictions toward potential physical infrastructure control.

-

Mixed signals from the administration create strategic ambiguity that functions simultaneously as deterrence and as a source of market uncertainty, rewarding volatility positioning over directional bets.

-

Global oil price risk under this scenario is fundamentally asymmetric: even partial disruption carries significant upward price pressure, while full incapacitation or regional escalation could trigger a supply shock of historic proportions.

-

Diplomatic resolution becomes structurally harder, not easier, when core economic infrastructure is explicitly threatened, narrowing the viable pathways to ceasefire restoration and potentially extending the duration and severity of the underlying conflict.

-

The feasibility gap between striking Kharg Island from the air and physically seizing and operating it as controlled infrastructure represents one of the most consequential and underanalysed dimensions of the current crisis.

-

Asian importers, particularly China, India, Japan, and South Korea, carry disproportionate economic exposure to any sustained Persian Gulf supply disruption despite having limited direct involvement in the political confrontation driving the risk.

-

The geopolitical risk landscape across metals, mining, and energy sectors is being reshaped by this confrontation in ways that extend well beyond crude oil pricing alone.

This article draws on reporting from World Oil (worldoil.com), which covers upstream industry developments and regional energy security topics. The scenario-based price and supply estimates referenced herein are analytical projections based on available information and historical precedent, not confirmed forecasts. Readers should not interpret this article as financial or investment advice. Energy market conditions and geopolitical situations can change rapidly, and all investment decisions should be made in consultation with qualified professional advisers.

Want to Stay Ahead of the Commodity Shocks Reshaping ASX Markets?

Geopolitical disruptions of this magnitude ripple directly into mineral commodity pricing and ASX-listed resource stocks — and Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries so subscribers can act on emerging opportunities before the broader market responds. Explore historic discoveries and their market returns, then begin a 14-day free trial to position yourself ahead of the next major market move.