June 11, 2026

The Architecture of Resource Coercion: Why Kharg Island Is the Most Strategically Exposed Oil Terminal on Earth

Energy infrastructure has always sat at the intersection of military strategy and economic power. From the oil fields of World War II Europe to the pipeline politics of the post-Soviet era, whoever controls the flow of crude has historically wielded disproportionate geopolitical leverage. What is unfolding in the Persian Gulf in mid-2026 represents a continuation of that logic, but with a scale and directness that has few modern parallels. The question now being asked in trading rooms, foreign ministries, and military planning cells is whether Trump seizing Kharg Island and Iran's oil sector would be a strategic masterstroke, an operational overreach, or something history has never actually seen before.

When big ASX news breaks, our subscribers know first

The Strategic Logic Behind Targeting Kharg Island

To understand why Kharg Island occupies such a critical position in this conflict, it helps to understand what makes it irreplaceable rather than merely important. The island, located approximately 25 kilometres off Iran's southwestern coastline in the northern Persian Gulf, is not simply one of several export terminals. It is the single facility through which roughly 90% of Iran's entire crude export volume is loaded onto tankers.

Iran operates other smaller terminals, including Lavan Island and Sirri Island, but their combined throughput represents a fraction of what Kharg handles. This creates a concentration risk with no real parallel among major oil exporters. Saudi Arabia, by comparison, has developed distributed export capacity across Ras Tanura, Yanbu, and Jubail specifically to avoid a single-point vulnerability.

Kharg's exposure is also layered. It sits inside the Persian Gulf, meaning tankers departing the terminal must still transit the Strait of Hormuz before reaching open ocean. In practical terms, Kharg operates as a chokepoint within a chokepoint. Disrupting the island alone would neutralise Iran's export capability. Disrupting both Kharg and Hormuz simultaneously, which is the current situation, effectively seals the entire Iranian export architecture.

The following comparison illustrates the terminal exposure imbalance:

| Terminal | Location | Estimated Share of Iranian Exports | Current Status |

|---|---|---|---|

| Kharg Island | Northern Persian Gulf, ~25km offshore | ~90% | Subject to military threat |

| Lavan Island | Central Persian Gulf | ~5% | Limited capacity |

| Sirri Island | Southern Persian Gulf | ~3–4% | Minimal throughput |

| Soroush/Norouz | Offshore fields | Minor | Primarily production, not export |

Iran Heavy Crude and the Asian Refinery Problem

Beyond the sheer volume question, there is a qualitative dimension to the Kharg Island disruption that markets often underweight. Iran produces and exports predominantly heavy sour crude grades, most notably Iran Heavy, which has recently been benchmarked near $64–$65 per barrel against Brent spreads that reflect its lower API gravity and higher sulphur content.

Asian refineries, particularly in China, have configured their hydrocracking and desulphurisation units to process exactly these grades. Iranian heavy crude is not easily substituted with light sweet crudes from West Africa or the United States without costly refinery modifications. This means disruption to Kharg Island does not simply reduce global oil supply by X barrels. It specifically removes a crude type that certain refineries require, creating localised processing bottlenecks that a generalised price spike fails to capture.

China's state refiners have historically been among the largest buyers of Iranian crude, partly because discounted pricing under sanctions made Iranian barrels economically attractive, and partly because refinery configurations were built around those grades. With China's oil imports already falling to an eight-year low as the conflict drags on, and strategic reserve drawdowns accelerating, the refinery optimisation problem is compounding an already stressed procurement environment.

Furthermore, OPEC's influence on oil markets has diminished considerably, as collective output from the group has fallen to its lowest level since approximately 2000 as of mid-2026, leaving virtually no spare capacity cushion to absorb a further supply shock from Kharg.

The Venezuela Precedent: Blueprint, Warning, or Neither?

The explicit comparison drawn between the proposed Iran operation and what occurred in Venezuela is analytically significant, though not in the way it is often presented. Following the capture of Nicolás Maduro in early 2026, the U.S. administration moved rapidly to establish administrative control over Venezuela's oil sector through a series of OFAC licensing frameworks. American firms were granted authority to invest in and operate Venezuelan oil infrastructure, and crude marketing was routed through U.S.-controlled accounts.

The political framing applied the language of liberation, positioning resource administration as a benefit to the Venezuelan people rather than an act of occupation. Whether that framing is accepted internationally is a separate question from whether the mechanism functioned.

The critical analytical distinction is this: the Venezuela operation involved administrative and commercial control of a subdued state, one in which the leadership had been captured and the government's capacity for organised military resistance was effectively eliminated. Applying that same template to Kharg Island means attempting the same outcome against an active adversary that:

- Retains operational military forces and deterrence capabilities

- Has publicly declared that occupation of its island territories would eliminate all restraint in its response

- Controls the Strait of Hormuz, giving it a direct retaliatory instrument against any seizure attempt

- Has issued formal warnings that energy infrastructure attacks cross established red lines under its deterrence doctrine

The operational complexity of seizing and holding an island terminal under hostile fire, supplying it with ground forces, protecting tankers loading at the facility, and maintaining throughput against an adversary with anti-ship missile capability is qualitatively different from issuing OFAC licences in Caracas. Even U.S. leadership has acknowledged publicly that there is uncertainty about whether domestic political appetite exists for the level of commitment that sustained Kharg Island occupation would require.

Key Analytical Insight: The Venezuela model involved post-capture administrative control of an already-subdued state. Applying that template to an active conflict zone with a functioning military deterrent represents a qualitatively different strategic undertaking — one that markets are not yet fully pricing.

Three Scenarios and What Each Means for Oil Prices

Scenario 1: Controlled Seizure and U.S. Administration

The most optimistic outcome from a U.S. strategic perspective involves a successful military seizure of Kharg Island followed by a managed transition to U.S.-administered crude exports. Probability drivers for this scenario include a complete ceasefire collapse, sustained U.S. air and naval dominance in the Gulf, and Iranian military capacity being sufficiently degraded to prevent effective counterattack.

The economics of this scenario are complex. Asian buyers who currently purchase Iranian crude under sanctions-risk conditions would face a new dynamic: U.S.-administered Iranian barrels with legal clarity but potentially higher pricing, redirected revenues, and significant geopolitical blowback from trading partners. Russian and Chinese responses to U.S. physical control of Persian Gulf oil infrastructure would likely include secondary sanctions pressure, alternative supply arrangements, and potential escalation in other theatres.

Price modelling suggests an initial spike on the military action itself, followed by a medium-term stabilisation if exports genuinely resume under new management. The duration of the transition gap, measured potentially in weeks to months, would determine the severity of the interim supply shock. The geopolitical oil price drivers at play here are unlike anything markets have had to price in decades.

Scenario 2: Destruction Without Seizure

The historical precedent here is instructive. During the 1980s Tanker War, Iranian oil export infrastructure including facilities at Kharg Island sustained significant damage from Iraqi strikes, demonstrating that such infrastructure can be degraded even without ground-force occupation. Full destruction of Kharg's loading and storage infrastructure without physical seizure would eliminate the approximately 90% of Iranian crude normally routed through the terminal.

Infrastructure rebuild timelines for major marine terminal facilities are measured in months to years, not weeks. Analyst projections cited across energy markets suggest Brent crude could reach $150 per barrel under a full ceasefire collapse scenario with sustained export disruption. Secondary effects would include:

- Significant LNG price surges, with Morgan Stanley projecting Asian LNG prices trending toward a 3.5-year high

- Asian spot market dislocations as refineries scramble for alternative crude grades

- Accelerated strategic reserve drawdowns in China and Japan, which have already begun

- Potential demand destruction in price-sensitive economies across South and Southeast Asia

Scenario 3: Ceasefire Holds and Threats Remain Rhetorical

This is the scenario that current futures market pricing most closely reflects. On the day the Kharg Island threat was issued publicly, both Brent and WTI declined approximately 0.6%. That price decline in response to an explicit seizure threat is a revealing signal: traders are pricing deal probability, not escalation probability.

The Apache helicopter incident, where Iran shot down a U.S. aircraft near Hormuz triggering a new round of strikes, illustrates the escalation trigger risk embedded in the ceasefire period. Each exchange of fire creates new preconditions for miscalculation. A durable ceasefire framework would require verifiable Iranian commitments on nuclear and military activity, U.S. commitments on sanctions relief sequencing, and third-party guarantors acceptable to both sides — none of which are currently in place.

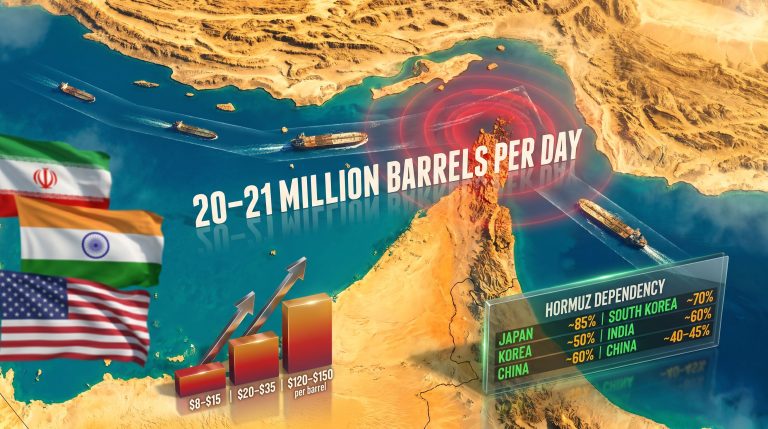

How the Hormuz Closure Has Already Restructured Global Energy Trade

The Strait of Hormuz has been effectively closed since the conflict began in late February 2026. Under normal conditions, the strait handles approximately 20% of global energy trade, making it the most consequential maritime chokepoint in the world economy. The disruption already in motion before any Kharg Island action represents the largest energy supply shock in modern recorded history.

The adaptation strategies being deployed by major consuming nations reveal both the resilience and the fragility of the global energy system:

| Country | Adaptation Strategy | Key Data Point |

|---|---|---|

| India | Increased UAE crude imports, supply secured through August | Fuel demand down 6.5%, LPG consumption down 20% |

| China | Strategic reserve drawdown, LNG imports at post-conflict highs | Oil imports at 8-year low |

| Japan | Reserve releases, new LNG supply agreements, alternative crude sourcing | Major LNG deal secured mid-2026 |

| Malaysia | Full crude supply chain overhaul following Hormuz shutdown | Structural rerouting underway |

| ASEAN broadly | U.S. LNG and LPG reserve releases announced | Emergency supply allocation activated |

India's situation deserves particular attention. A 6.5% contraction in fuel demand and a 20% drop in LPG consumption reflect genuine economic stress cascading through households and industry, not merely a statistical adjustment in crude procurement. The oil price shock is actively weakening India's economic and fiscal position, with energy prices contributing to a three-year high in U.S. inflation through transmission mechanisms that link Gulf disruption to domestic consumer prices.

Dark-mode tanker operations have become increasingly common, with Gulf producers routing shipments without AIS transponders to obscure movements through or near contested waters. This operational adaptation degrades the market's ability to track actual supply flows in real time, contributing to the disconnect between visible inventory data and price behaviour.

The next major ASX story will hit our subscribers first

The Credibility Gap and Market Mispricing

One of the most analytically interesting features of the current environment is the divergence between the scale of the supply disruption and the level of crude prices. The most significant oil supply disruption in modern history is occurring against a backdrop of Brent trading well below $100 per barrel at the time of writing — a level that would have seemed implausibly low given the disruption parameters if modelled in advance.

Several factors explain this apparent anomaly:

-

Deal premium pricing: Futures positioning strongly implies that the majority of market participants expect a negotiated ceasefire. The price reflects probability-weighted outcomes, not the worst-case scenario.

-

Short-position accumulation: A structural short position has built up in oil futures as ceasefire optimism dominated sentiment over recent weeks. This positioning creates significant reversal risk if the ceasefire fails.

-

Venezuela comparison effect: The framing of the Venezuela precedent as a successful template may be actively suppressing risk premiums by suggesting that even if Kharg is seized, exports eventually resume under new management.

-

Strategic reserve buffer: Coordinated drawdowns in China, Japan, and releases from U.S. reserves to ASEAN nations have provided a temporary supply bridge that softens the immediate price signal.

Important Investor Consideration: The structural short position in oil futures means that a rapid repricing event, triggered by ceasefire collapse or a confirmed Kharg Island military operation, could produce an exceptionally sharp and fast upward price move as short positions are forcibly covered. The asymmetry here favours volatility, not calm.

The Doctrine Question: Is Resource Coercion Through Force Economically Viable?

The emerging pattern across Venezuela and now potentially Iran raises a question that extends well beyond this specific conflict: is a doctrine of resource administration through military action economically sustainable for the power that deploys it? The trade war impact on oil has already demonstrated how economic coercion can rapidly reshape supply chains, however direct military seizure of infrastructure operates in an entirely different risk category.

The revenue arithmetic is instructive. Iran's crude export revenues at pre-conflict production levels were substantial, representing a significant share of government finances. However, the cost of sustained military presence on a defended island terminal, including force protection, logistics, anti-missile defence, tanker escort, and diplomatic management of international condemnation, must be set against that revenue figure.

International humanitarian law draws a distinction between legitimate military targets and civilian economic infrastructure. Legal scholars have noted that facilities providing a significant share of Asian refining capacity carry obligations under international humanitarian jurisprudence that go beyond straightforward military targeting calculus. The legal exposure associated with disabling such infrastructure represents a real constraint on the doctrine's operational viability.

Important Context: Analysts and legal scholars have noted that actions targeting civilian energy infrastructure carry significant obligations under international law. The legal architecture surrounding such actions remains a contested and evolving area of international humanitarian jurisprudence.

For other resource-rich states operating under U.S. sanctions or strategic pressure, the signal being sent by both the Venezuela operation and the Iran threat is already influencing infrastructure hardening decisions, alternative reserve currency arrangements, and accelerated diversification of military deterrence.

What Comes After Hormuz: The Post-Conflict Energy Architecture

Regardless of how the current conflict resolves, the global oil trade is unlikely to return to its pre-2026 configuration. The Hormuz closure has forced consuming nations to make structural adaptations that will outlast any ceasefire. Trans-Mountain pipeline capacity from Canada has reportedly hit full utilisation as Asian buyers seek Pacific-facing alternatives. Alternative routing through pipeline systems across the Arabian Peninsula has exposed capacity constraints that were theoretical before the conflict made them operational realities.

The structural acceleration of energy diversification among Asian importers represents a lasting shift in procurement strategy. Energy infrastructure assets that provide routing alternatives to Hormuz, including East African terminals, expanded Red Sea capacity once security conditions allow, and Pacific-facing pipeline infrastructure, have gained strategic and investment value that did not exist at this scale before February 2026.

Whether Trump seizing Kharg Island and Iran's oil sector represents a genuine policy intention or calibrated coercive signalling, the consequences for global energy architecture are already unfolding regardless of what happens next. The current crude oil market overview makes clear that supply chains being rebuilt under emergency conditions today will not simply revert. The market structure that emerges from this conflict will be shaped by decisions being made right now, in procurement offices in Beijing, Mumbai, and Tokyo, as much as in Washington or Tehran.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Price projections, scenario modelling, and market analysis referenced herein involve significant uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct independent research and consult qualified advisers before making any investment or strategic decisions related to energy markets.

Want to Track the Investment Opportunities Emerging From Global Energy Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex market data into actionable investment insights — including opportunities arising from commodity supply shocks like the current Hormuz crisis. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.