May 22, 2026

The Economics of Bringing Dead Mines Back to Life

In the global copper market, one of the most underappreciated dynamics is the role of dormant brownfield assets. While the mining industry fixates on greenfield discoveries and exploration frontiers, some of the most economically compelling copper tonnes available in the near term are sitting beneath ground that was once actively mined, then abandoned when economics turned hostile. These are assets with known orebodies, existing shaft infrastructure, and established community relationships. The barrier to reactivation is not geological uncertainty but capital commitment, engineering execution, and the courage to invest in places others walked away from.

This dynamic sits at the heart of the Zambian Copperbelt in 2026. When Konkola reopens Chingola copper mine after an 18-year operational pause, it is not simply a news headline. It is a case study in how Africa's copper ambitions will be built as much on the revival of legacy assets as on the development of new ones.

When big ASX news breaks, our subscribers know first

Why Dormant Mines Are Not Dead Mines

There is a critical distinction in mining between an abandoned mine and a mine placed on care and maintenance. The Chingola "B" Mine, part of KCM's broader Nchanga mining complex in Zambia's Copperbelt Province, falls firmly into the latter category. Operations ceased in 2003 following a prolonged period of depressed copper prices, operational complexity, and constrained investment across the Copperbelt. However, the orebody did not disappear.

The copper grades that made Chingola "B" productive for more than two decades, averaging approximately 2.5% copper across monthly throughput of roughly 60,000 tonnes of ore, remained locked in the sediment-hosted stratiform deposits that characterise Zambian Copperbelt geology. Understanding the copper supply crunch helps explain why reactivating such assets has become a strategic priority.

Sediment-hosted stratiform copper deposits, like those found across the Zambian Copperbelt, are geologically distinct from the porphyry systems that dominate copper production in South America. Rather than disseminated mineralisation spread through large igneous intrusions, Zambian deposits form as relatively flat-lying, laterally continuous ore horizons within sedimentary sequences.

This geometry creates a predictable mining environment, where grade continuity tends to be more consistent than in porphyry systems and underground mining planning is comparatively more straightforward. It is precisely this geological predictability that makes brownfield reactivation in the Copperbelt a lower-risk proposition than recommissioning dormant mines in more structurally complex geological settings.

KCM's Operational Network and the Role of Nchanga

Konkola Copper Mines operates one of the most geographically distributed mining networks in Zambia, with active sites spanning Chingola, Chililabombwe, Kitwe, and Nampundwe. The Nchanga complex, anchored by the now-reactivated Chingola "B" Mine, serves as KCM's central production asset and the focal point of its recovery strategy following years of operational disruption.

KCM is 79.4% owned by Vedanta Resources, the London-headquartered diversified metals and mining group, with the remaining 20.6% held by ZCCM-IH, Zambia's state-owned investment company. This ownership structure is significant beyond simple equity accounting. ZCCM-IH's stake gives the Zambian government a direct financial interest in KCM's operational performance, creating an alignment of incentives between private capital deployment and national production objectives.

It also means that KCM's investment decisions are made within a framework that includes state oversight and reinvestment obligations, which shapes the pace and scale of capital allocation.

Production Trajectory and Throughput Targets

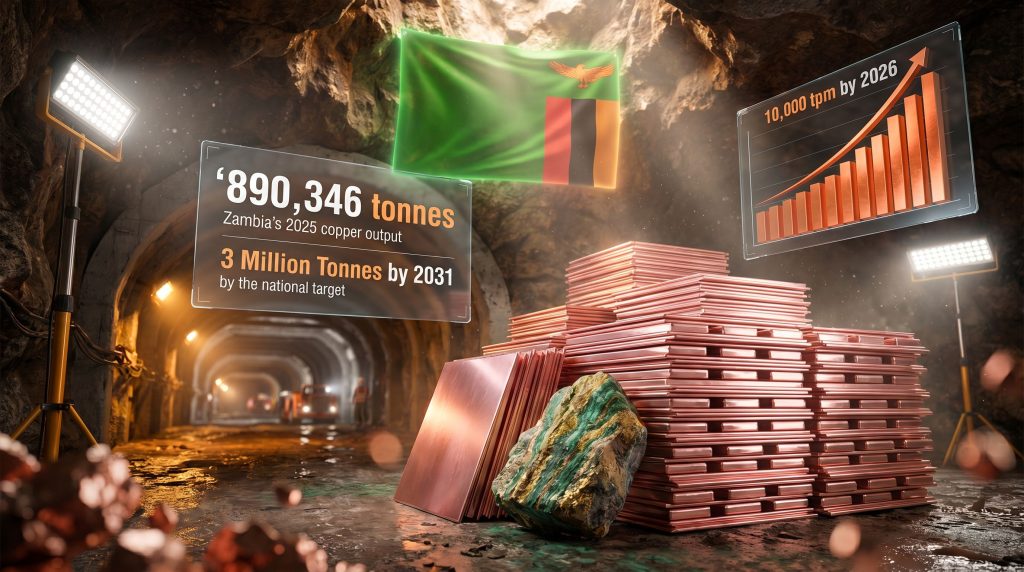

The Chingola "B" restart is the most visible component of KCM's broader operational recovery. The company has recently reached a production milestone of 8,200 tonnes per month of refined copper and has set a target of 10,000 tonnes per month by 2026. Against this backdrop, the Chingola "B" Mine's projected throughput of more than 200,000 tonnes of ore per month is transformative.

That figure represents more than three times the mine's historical monthly ore output and carries profound implications for KCM's ability to feed its existing concentrator and smelter infrastructure.

At the historical copper grade of approximately 2.5%, a throughput of 200,000 tonnes of ore per month implies a theoretical copper-in-concentrate output of roughly 5,000 tonnes per month, before accounting for metallurgical recovery rates. Actual recovered copper will be somewhat lower, depending on the efficiency of the flotation circuit and downstream processing. This output contribution alone would represent a meaningful share of the gap between KCM's current production rate and its 10,000 tpm target.

Raise Boring and Shaft Reactivation: Technical Complexity Beneath the Headlines

One detail that rarely surfaces in general coverage of the KCM revival is the reintroduction of raise boring at the No. 3 shaft of Konkola Mine after a 15-year hiatus. Raise boring is a specialised underground excavation technique used to create vertical or inclined shafts connecting different levels of an underground mine. The method involves drilling a pilot hole and then reaming it upward to the desired diameter using a rotating cutterhead.

It is mechanically intensive, requires specialised equipment, and demands precision engineering to avoid deviations that could compromise shaft integrity. Reintroducing raise boring after a prolonged pause is not a trivial operational decision. It signals that KCM is investing in deep underground access infrastructure, not simply re-entering existing headings. Furthermore, this is a meaningful indicator of the company's long-term commitment to the Copperbelt, as deep shaft development implies production timelines extending well beyond the initial ramp-up phase.

The Technical Hurdles of an 18-Year Reawakening

Recommissioning a mine dormant for 18 years involves a sequence of engineering challenges that are frequently underestimated by observers outside the industry.

-

Dewatering: Underground workings accumulate groundwater during extended care-and-maintenance periods. At depth, the volume and hydrostatic pressure of accumulated water can be substantial. Dewatering requires significant pumping capacity, careful management of water disposal, and ongoing monitoring to prevent inrush events during re-entry.

-

Structural integrity assessment: Shafts, decline entries, underground roadways, and stope hangingwalls deteriorate over time even in care-and-maintenance conditions. Rock mechanics assessments must be conducted before workforce re-entry, and ground support rehabilitation is typically required before mining can resume.

-

Ventilation recommissioning: Deep underground environments require active ventilation systems to control temperature, dust, and the dilution of blasting fumes. Ventilation infrastructure, including fans, ducting, and raise connections, must be inspected, repaired, and tested before production workers can safely operate below surface.

-

Equipment rehabilitation: Mobile mining equipment left in underground environments for extended periods typically requires extensive overhaul or replacement. The decision between rehabilitation and new procurement has direct implications for restart capital expenditure.

-

Workforce reconstruction: Perhaps the most underappreciated challenge is the human capital dimension. An 18-year closure means that most of the experienced underground workforce has either retired or moved on. Rebuilding institutional knowledge, training new operators, and re-establishing safety culture takes considerable time and management focus.

Ore Processing Bottlenecks at Scale

The step-change in targeted ore throughput, from 60,000 tonnes per month historically to more than 200,000 tonnes per month projected, introduces potential processing bottlenecks that KCM will need to navigate carefully. Concentrator plants have defined design throughput capacities. Routing significantly higher ore volumes through existing infrastructure without debottlenecking could result in reduced recovery rates, increased reagent consumption, or equipment wear that erodes operational efficiency.

Grade management also becomes more complex when blending ore from multiple sources across the Nchanga complex, as varying mineralogical characteristics affect flotation circuit performance.

Zambia's Output Gap and the Scale of the National Challenge

Understanding the Chingola "B" restart requires placing it against Zambia's national copper production context.

| Metric | Current Status | Target |

|---|---|---|

| Zambia 2025 copper output | 890,346 tonnes | 1,000,000 tpa (near-term) |

| Zambia 2031 copper target | N/A | 3,000,000 tpa |

| KCM current production | ~8,200 tpm refined copper | 10,000 tpm by 2026 |

| Chingola "B" ore throughput | Ramp-up phase | 200,000+ tpm |

Zambia produced 890,346 tonnes of copper in 2025, falling short of its stated 1 million tonne annual target. The government's ambition to reach 3 million tonnes per year by 2031 would require more than tripling current output within six years. That trajectory is ambitious by any historical benchmark in the global copper industry.

For context, the table below compares KCM's Nchanga complex against other significant African copper operations.

| Operation | Country | Approximate Annual Output | Primary Operator |

|---|---|---|---|

| Kamoto (KCC) | DRC | ~300,000+ tpa | Glencore |

| Tenke Fungurume | DRC | ~200,000+ tpa | CMOC |

| Sentinel | Zambia | ~200,000+ tpa | First Quantum |

| Lumwana | Zambia | ~130,000 tpa | Barrick |

| Nchanga/KCM complex | Zambia | Ramping toward 120,000+ tpa | Vedanta/KCM |

Note: Figures are approximate and subject to operational variability. Intended for comparative context only.

Achieving Zambia's 3 million tonne target will require not only KCM's revival but sustained investment from First Quantum, Barrick, and new project developers across the Copperbelt. When Konkola reopens Chingola copper mine, it demonstrates that brownfield reactivation is executable, providing a proof-of-concept that may unlock investor confidence across a broader pipeline of dormant assets. Reviewing the largest copper mines globally underscores just how significant a full KCM recovery could be for Zambia's standing in world copper supply.

Brownfield vs. Greenfield: Why the Economics Favour Reactivation

The comparative economics of brownfield reactivation versus greenfield copper development are rarely examined with the precision they deserve.

| Factor | Brownfield Reactivation | Greenfield Development |

|---|---|---|

| Capital requirement | Lower (existing infrastructure) | Higher (full build-out) |

| Time to first production | Faster (months to years) | Slower (5 to 10+ years) |

| Permitting complexity | Moderate (existing approvals) | High (new environmental and social process) |

| Geological risk | Lower (known orebody) | Higher (exploration uncertainty) |

| Community relations | Established (existing workforce base) | Requires full new engagement process |

In a copper price environment where the metal has been trading above $5.60 per pound in mid-2026, the revenue implications of accelerating time-to-production through brownfield reactivation are substantial. Each month of production brought forward translates directly into revenue at current price levels. The copper price drivers underpinning this environment make the speed advantage of brownfield reactivation as strategically important as the capital efficiency advantage, particularly for Zambia's time-bound 2031 output target.

The next major ASX story will hit our subscribers first

The Global Copper Demand Picture and Zambia's Position

The structural drivers behind copper demand growth are well established but worth contextualising specifically for Zambian production.

-

Energy transition infrastructure requires copper-intensive transmission and distribution grid expansion at a scale not seen since post-war industrialisation.

-

Electric vehicle platforms use significantly more copper per unit than internal combustion vehicles, across battery systems, motors, and charging infrastructure.

-

Data centre construction, driven by AI infrastructure buildout, is emerging as a rapidly growing copper demand category that was not a significant factor in copper demand modelling as recently as three years ago.

-

Global grid modernisation across both developed and developing markets requires sustained copper investment over multi-decade timescales.

Against this demand backdrop, the global copper supply pipeline faces structural constraints. Major new discoveries are increasingly rare, with the average grade of newly discovered copper deposits declining over time. Existing major copper system operations face mature orebody profiles, water and energy constraints, and rising political risk in some jurisdictions.

African copper producers in Zambia and the DRC sit at a strategically important position in the global supply picture. The Copperbelt's combination of high-grade sediment-hosted deposits, existing infrastructure, and brownfield development pipeline offers a supply response pathway that few other copper-producing regions can match on both speed and scale.

Key Production Milestones to Watch at KCM

Investors and industry observers tracking KCM's progress should focus on the following operational markers.

| Milestone | Target Metric | Strategic Significance |

|---|---|---|

| Ore flow established at Chingola "B" | Confirmed recommissioning | Validates the restart thesis |

| 100,000 tpm ore throughput | 50% of nameplate capacity | Early ramp-up confirmation |

| 200,000 tpm ore throughput | Full nameplate capacity | Full investment thesis validation |

| KCM group output: 10,000 tpm copper | Company-wide 2026 target | Signals operational recovery completion |

| Zambia national output: 1M tpa | Missed 2025 benchmark | Near-term national credibility test |

| Zambia national output: 3M tpa | 2031 national target | Long-term strategic viability of the Copperbelt revival |

Structural Constraints That Cannot Be Ignored

The optimism surrounding the Chingola restart and Zambia's broader copper ambitions must, however, be tempered by an honest assessment of the structural constraints that could impede the trajectory.

Power supply reliability remains one of the most persistent operational risks in the Zambian Copperbelt. Underground mining and ore processing are energy-intensive activities. Zambia's hydropower-dependent grid is vulnerable to drought conditions, and extended power interruptions can disrupt mine dewatering systems, ventilation, and ore processing continuity in ways that create significant operational and safety complications.

Water management in deep underground environments presents ongoing technical challenges, particularly in the wet season when groundwater inflows increase.

Skilled workforce availability is a medium-term constraint for the entire Copperbelt, not just KCM. Tripling national output by 2031 would require a substantial expansion of the skilled mining workforce, including underground operators, metallurgical engineers, and mine planners, at a pace that training institutions in Zambia will struggle to match without significant investment.

Fiscal terms for foreign investors remain a factor influencing the pace of capital deployment. Vedanta's willingness to commit further capital to KCM's expansion will depend in part on the long-term stability of Zambia's royalty and taxation framework for mining. In addition, those evaluating copper investment strategies for African assets will be closely monitoring how these fiscal frameworks evolve.

Frequently Asked Questions: Konkola Copper Mines and the Chingola Restart

What is the Chingola "B" Mine and why did operations stop in 2003?

The Chingola "B" Mine is part of KCM's Nchanga mining complex in Zambia's Copperbelt Province. A combination of persistently low copper prices through the late 1990s and early 2000s, compounded by operational challenges and constrained investment across the Copperbelt, made the mine uneconomic to operate. It was placed into care-and-maintenance status around 2003 and remained dormant for approximately 18 years before recommissioning began in 2026.

How much copper could the Chingola "B" Mine produce at full capacity?

At the projected throughput of more than 200,000 tonnes of ore per month and the historical copper grade of approximately 2.5%, the mine has the theoretical capacity to deliver roughly 5,000 tonnes of copper per month in concentrate form, subject to metallurgical recovery rates. Actual output will depend on grade consistency, processing circuit performance, and integration with KCM's broader operations. Reuters reported on the significance of KCM resuming copper production as part of this broader revival.

Who owns Konkola Copper Mines?

KCM is 79.4% owned by Vedanta Resources and 20.6% owned by ZCCM-IH, Zambia's state investment vehicle. This structure gives the Zambian government a direct financial stake in KCM's operational and commercial performance.

Can Zambia realistically reach 3 million tonnes of copper per year by 2031?

Zambia produced approximately 890,346 tonnes in 2025, below even its 1 million tonne near-term target. Reaching 3 million tonnes by 2031 would require a more than threefold increase in output within six years. While the geological and infrastructure foundations exist to support this ambition, it will require sustained capital investment from multiple operators, resolution of power supply constraints, and a stable investment environment for foreign mining companies.

Konkola reopens Chingola copper mine as a positive signal, but this represents only one component of a much larger production growth challenge. Consequently, the entire industry will be watching how swiftly and successfully this restart scales to full capacity.

How does the Zambian Copperbelt compare geologically to the DRC's copper basin?

Both regions share the same fundamental geological origin, the Central African Copperbelt, formed by sediment-hosted mineralisation in the Katanga Supergroup. Zambia's deposits tend to exhibit consistent grade profiles within relatively predictable stratiform ore horizons, which supports reliable mine planning. The DRC's deposits, while often higher-grade, can be more structurally complex in certain areas. Both jurisdictions face infrastructure and energy challenges, but Zambia has historically offered a more stable regulatory environment for foreign mining investment.

Disclaimer: This article contains forward-looking statements, production targets, and financial data sourced from publicly available information as of May 2026. Mining production targets are subject to geological, operational, regulatory, and market risks. This content is intended for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence before making any investment decisions.

Want To Stay Ahead of Major Copper Discoveries on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries — including copper — are announced on the ASX, transforming complex data into actionable insights for both short-term traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself ahead of the market.