June 20, 2026

The Processing Gap That Defines the Clean Energy Century

The most consequential competition of the twenty-first century is not being fought in semiconductor fabrication plants or satellite networks alone. It is unfolding across the salt flats of the Atacama, the Amazon basin's red laterite soils, and the Andean copper porphyries stretching from southern Peru to northern Chile. The contest over Latin American critical minerals between G7 and China has quietly become one of the defining industrial and geopolitical fault lines of the energy transition era, and its outcome will shape which nations control the material foundations of the next economy.

What makes this competition unusual is that the battlefield is geological before it is geopolitical. Latin America did not choose its strategic importance; it inherited it through plate tectonics and hydrothermal chemistry accumulated over hundreds of millions of years. Understanding why that matters requires looking at the numbers beneath the headlines.

When big ASX news breaks, our subscribers know first

Latin America's Mineral Endowment: More Concentrated Than Most People Realise

The statistics on Latin American mineral reserves are striking even when encountered repeatedly, but their full significance is rarely absorbed. Consider the following regional snapshot:

| Mineral | Latin America's Estimated Global Share | Key Countries |

|---|---|---|

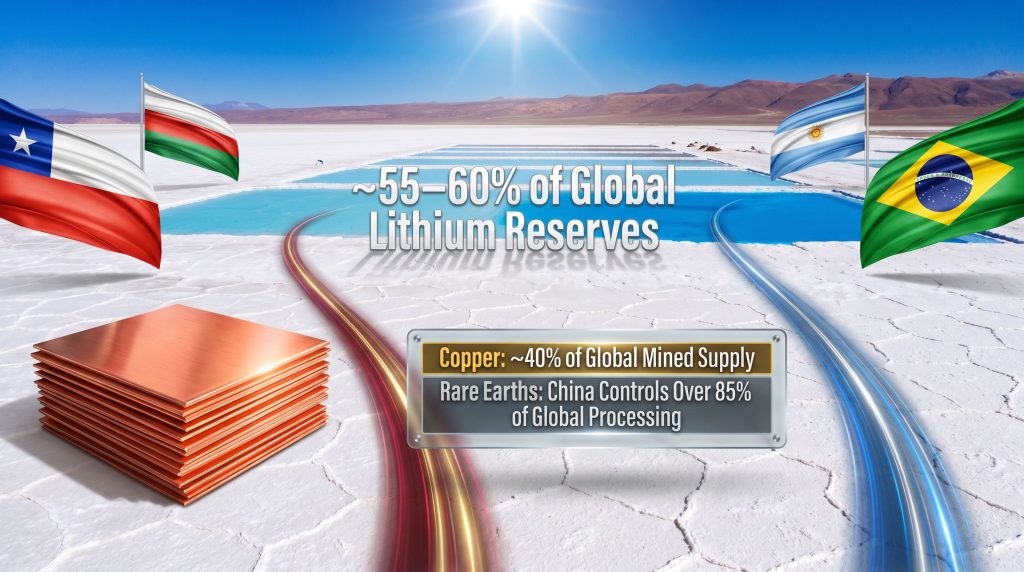

| Lithium | ~55-60% of global reserves | Chile, Argentina, Bolivia |

| Copper | ~40% of global mined supply | Chile, Peru |

| Niobium | ~90% of global production | Brazil |

| Rare Earth Elements | Growing identified deposits | Brazil, Peru |

| Graphite | Emerging battery-grade deposits | Brazil |

| Nickel | Significant laterite deposits | Brazil, Colombia |

Chile alone accounts for roughly 27% of annual global copper mine output, a figure that makes it structurally irreplaceable to every electrification scenario currently modelled by the International Energy Agency. No grid expansion, EV charging network, or offshore wind installation is viable at scale without Chilean copper flowing through the supply chain.

Brazil's position is less understood outside specialist circles. The country holds the largest niobium reserves on Earth, with estimates suggesting it controls more than 90% of global niobium production, a mineral used in high-strength steel alloys for automotive and aerospace applications. Less widely appreciated is that Brazil's rare earth deposits, concentrated in Minas Gerais state and parts of the Amazon basin, include significant ionic clay-type deposits.

Ionic clay rare earths are geologically significant because they can be processed using heap leach methods at lower capital cost than hard rock deposits, a technical characteristic that could materially alter Brazil's competitive position in REE supply chains if processing investment follows.

The Lithium Triangle formed by Chile, Argentina, and Bolivia represents the single largest concentration of lithium brine resources on Earth. Brine-hosted lithium is chemically distinct from hard rock spodumene deposits: it requires evaporation ponds and specialist hydrometallurgical conversion rather than conventional flotation, and the resulting cost structures are among the lowest in the global lithium industry when water and energy inputs are well-managed.

Why Ore Grade and Deposit Type Matter More Than Reserve Size Alone

A nuance consistently underweighted in geopolitical analysis is that not all reserves are equal in commercial or strategic terms. For copper, the global average ore grade has been declining for decades. Chilean copper porphyries that once averaged 2% copper now frequently operate at grades below 0.6%, meaning that far more rock must be moved and processed per tonne of metal produced. This grade decline has important consequences:

- Higher energy intensity per unit of output, increasing operating costs and carbon footprint

- Greater water consumption at a time when the Atacama faces severe hydrological stress

- Rising capital requirements for crushing, grinding, and flotation circuits at lower-grade operations

- Longer timelines to bring marginal deposits into production economically

For lithium, brine quality varies significantly across the Lithium Triangle. Chilean brines in the Salar de Atacama are exceptionally concentrated, with lithium grades that make them among the most economic in the world. Argentine and Bolivian brines are generally lower grade and contain higher impurity levels, including magnesium, which complicates conventional evaporation processing and may require direct lithium extraction technology to achieve commercially viable recovery rates.

The G7's Defensive Supply Chain Strategy and Its Structural Limitations

The G7's engagement with Latin American critical minerals is best understood as a reactive posture rather than a proactive industrial strategy. The recognition that allied industrial economies had become structurally dependent on a single jurisdiction for the processing of minerals physically extracted on multiple continents arrived later than the vulnerability itself.

The Mineral Security Partnership, launched in 2022, represents the most institutionally coherent G7 response. It brings together the United States, European Union members, Japan, South Korea, Australia, Canada, and the United Kingdom in a coordinated framework designed to co-finance mineral projects meeting defined environmental, social, and governance standards. Furthermore, development finance institutions including the U.S. International Development Finance Corporation and Export Development Canada have been repositioned to prioritise critical minerals demand project lending across the region.

However, the G7's structural challenge is not primarily about financing volume. It is about processing capacity. Consider the lithium value chain:

- Brine extraction from salt flats (Lithium Triangle operations)

- Solar evaporation and concentration across large evaporation pond systems

- Conversion to lithium carbonate or lithium hydroxide monohydrate

- Battery precursor cathode active material manufacturing

- Cell manufacturing and battery pack assembly

China currently dominates steps 3 through 5 across this chain. Even where G7-aligned companies hold equity in Chilean or Argentine brine operations, the refined intermediate product frequently still moves through Chinese hydrometallurgical infrastructure before it reaches a battery gigafactory in Europe or North America. The processing bottleneck is a structural dependency that upstream mining investment alone cannot resolve.

Critical Gap: Closing the processing deficit requires sustained capital deployment in mid-stream industrial capacity over 10 to 15 year timeframes. This is not a financing problem that can be solved with a single multilateral commitment. It requires the construction of entirely new industrial ecosystems in jurisdictions where they do not currently exist at meaningful scale.

How China Built Its Processing Dominance: A Three-Layer Architecture

China's position in Latin American mineral supply chains was not assembled quickly. It reflects roughly two decades of patient strategic capital deployment operating across three reinforcing dimensions:

| Competitive Dimension | China's Accumulated Advantage | G7 Current Position |

|---|---|---|

| Upstream equity | Early-mover positions in lithium and copper operations | Seeking expansion, competing against established rights |

| Processing capacity | ~60-70% of global lithium refining; >85% of REE processing | Building from near-zero base outside China |

| Offtake agreements | Long-term contracts at early-mover pricing | Developing frameworks, less consistently deployed |

| Infrastructure bundling | Ports, rail, and energy packaged with mineral access | Generally separates infrastructure from resource deals |

| State risk tolerance | State enterprises absorb exploration and development risk | Relies more on private capital with public guarantees |

| Financing speed | Rapid deployment with fewer conditionalities | Slower processes with ESG and governance requirements |

Chinese state-owned enterprises secured equity positions in lithium brine operations in Chile and Argentina during periods when Western institutional capital was largely absent from the sector. Long-term offtake agreements locked in preferential access to future production at terms reflecting early-mover advantage rather than the elevated strategic pricing that would apply today. This temporal advantage is structural: it cannot be erased by simply deploying more capital now.

For rare earths specifically, China's processing dominance is even more pronounced. Controlling an estimated 85% or more of global rare earth refining capacity, Chinese processing infrastructure handles material sourced from multiple continents. Brazilian and Peruvian rare earth concentrates that reach commercial production scale will face rare earth processing challenges that lithium producers confront today unless dedicated mid-stream investment accompanies upstream development.

Resource Nationalism as Strategic Leverage, Not Simply Political Risk

Conventional investor frameworks treat resource nationalism as a risk variable: something that increases the probability of adverse policy change and therefore requires a higher return threshold. This framing, while operationally useful, misses the more important dynamic currently unfolding across the region.

Latin American governments are not passive recipients of external capital competing to offer the most attractive investment conditions. They are active strategic actors deploying their geological endowment as diplomatic leverage in a competition between the world's two largest economies. The intensity of G7-China rivalry has created negotiating power that did not exist a decade ago, and sophisticated resource-holding governments are exploiting it systematically.

Three Distinct Policy Models Emerging Across the Region

State Control and Direct Participation

Bolivia's Yacimientos de Litio Bolivianos model represents the most explicit version of full state ownership, though operational and financing challenges have limited production relative to the scale of the country's lithium endowment. The strategic logic is defensible: avoiding a repeat of the historical pattern in which raw material exporters captured only commodity-price returns while industrial value was created elsewhere.

Hybrid State-Private Frameworks with Value-Addition Conditions

Chile's lithium strategy reforms have positioned CODELCO to play a central role in future lithium development, creating a hybrid between full nationalisation and open FDI. Foreign investors can participate, but on terms that preserve meaningful state enterprise involvement and attach conditions around local processing and technology transfer. Argentina's framework is more fragmented, with provinces retaining significant autonomy over mineral concessions, creating variable investment conditions across a single federal system.

Pragmatic Balancing Without Formal Alignment

Peru and Brazil have demonstrated the most commercially pragmatic approach, engaging with both Chinese and G7 capital without formally aligning with either bloc's supply chain architecture. Brazil's position is particularly strategic given its rare earth, niobium, graphite, and nickel endowment spans minerals that both blocs classify as essential. Consequently, the contest over Latin American critical minerals between G7 and China is most visibly contested in Brazil's policy corridors.

The most precise analytical framing is not that Latin American nations are choosing between the G7 and China. They are running a competitive process between them, using each bloc's strategic anxiety to extract technology transfer commitments, infrastructure investment, and improved fiscal terms that would have been unavailable in a less contested environment.

Value-Extraction Strategies Being Deployed Across the Region

- Technology transfer conditions attached to investment approvals, requiring foreign firms to share processing and refining expertise with domestic enterprises

- Local content mandates specifying minimum percentages of project inputs, labour, and services sourced domestically

- Downstream investment linkages connecting mining concession approvals to commitments for in-country refining or battery material manufacturing

- Infrastructure bundling demands asking Western investors to match the port, rail, and energy packages that Chinese deal structures have historically included

- Royalty and fiscal renegotiation exploiting elevated strategic demand to revise terms established during periods of lower geopolitical interest

The Minerals That Matter Most: A Strategic Assessment

Copper: The Electrification Backbone No One Can Replace

Every kilowatt-hour of electricity generated from wind or solar requires 4 to 5 times more copper per unit of capacity than a natural gas plant, according to data from the International Copper Study Group. EV powertrains use approximately 3 to 4 times more copper than internal combustion vehicles. This demand arithmetic makes copper the most commercially liquid and strategically consequential mineral in the clean energy portfolio.

Chile and Peru together supply approximately 40% of global copper mine production, and their combined reserve base suggests this structural dominance will persist for decades. The copper supply crunch is less about processing — Latin America retains more domestic smelting capacity for copper than for lithium — and more about securing long-term offtake agreements and preventing further Chinese equity accumulation in undeveloped deposits.

Rare Earths and Antimony: The Less-Discussed Strategic Variables

Antimony deserves specific attention as an emerging focal point. Used in flame retardants, ammunition, and increasingly in grid-scale antimony flow batteries, the metal has seen its strategic classification elevated significantly. China controls a dominant share of global antimony production and processing, and Latin American deposits, while not the world's largest, have attracted renewed prospecting interest as supply chain diversification pressure mounts.

Brazil's rare earth story is similarly underappreciated in mainstream coverage. Unlike the heavy rare earth elements concentrated in Chinese ionic clay deposits in Jiangxi province, Brazilian REE deposits tend toward lighter rare earth profiles. However, the presence of neodymium and praseodymium, the principal inputs for permanent magnets used in EV motors and wind turbine generators, gives Brazilian deposits genuine strategic relevance to both G7 battery manufacturing programmes and the broader magnet supply chain.

Three Scenarios for the Critical Minerals Landscape Through 2030

| Scenario | G7 Outcome | China Outcome | Latin America Outcome |

|---|---|---|---|

| Fragmented Bifurcation | Achieves upstream diversification, processing gap persists | Retains processing dominance, faces reduced market access | Higher export revenues, limited downstream capture |

| Latin American Strategic Autonomy | Gains reliable allies, accepts technology transfer costs | Loses some preferential access, maintains processing revenue | Captures mid-stream value, strongest long-term position |

| Chinese Consolidation | Upstream wins offset by mid-stream dependency | Full value chain integration in key minerals | Commodity-price returns despite geological endowment |

The scenario that appears most probable in the near term is a hybrid of all three, differentiated by mineral type and country. Copper is likely to see the most balanced outcome given existing Latin American processing capacity. Lithium processing diversification will prove slower and more costly than current G7 timelines anticipate. Rare earth supply chain independence for the G7 remains the most distant objective given the depth of China's processing advantage.

The next major ASX story will hit our subscribers first

What Investors and Industry Participants Should Understand

Several dynamics in this landscape are consistently underweighted by analysts applying conventional mining investment frameworks. In addition, the broader contest over Latin American critical minerals between G7 and China introduces policy volatility that compounds operational risk across the region.

-

Permitting timelines in the region are structural, not cyclical. Environmental and community consultation processes in Chile and Peru regularly extend mine development timelines by 5 to 10 years. This is not a governance failure that will be resolved by political will alone; it reflects the legal rights of indigenous communities and the procedural requirements of environmental licensing systems.

-

Water scarcity is becoming a binding constraint in the Atacama. Both copper and lithium operations compete for hydrological resources in one of the world's driest environments. Any investment thesis that does not account for water access risk across a 20 to 30 year mine life is materially incomplete.

-

The DLE technology question remains commercially unresolved. Direct lithium extraction, which bypasses conventional evaporation processing and could dramatically accelerate lithium production from lower-grade brines, has attracted significant investment but has not yet demonstrated full commercial validation at scale. The G7's financing commitments for DLE and related technologies will materially affect the competitive position of Argentine brine projects relative to Chilean operations.

-

Niobium is the region's most underanalysed strategic asset. Brazil's near-total control of global niobium production, and niobium's expanding applications in high-strength steel, superconducting materials, and potentially battery technology, makes it a mineral worth watching significantly more closely than current analyst coverage reflects.

Disclaimer: This article contains forward-looking analysis and scenario projections based on publicly available information as of mid-2026. Mineral reserve estimates, production statistics, and geopolitical assessments are subject to revision. Nothing in this article constitutes investment advice. Readers should conduct independent due diligence before making investment decisions related to any minerals, mining companies, or related sectors discussed.

Want to Track the Next Major ASX Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — from copper and lithium to rare earths and niobium — instantly converting complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.