June 29, 2026

Why Regional Nickel Platforms Command a Different Valuation Than Single-Mine Developers

Institutional capital does not price mining assets in isolation. It prices them within frameworks of concentration risk, supply chain durability, and the long-term viability of a processing thesis across multiple ore sources. When a developer holds a single deposit in a single jurisdiction, every variable, from geological variance to political risk to metallurgical underperformance, flows directly into the enterprise valuation with nowhere to diversify. That structural vulnerability is precisely why the Lifezone Metals Musongati option deserves attention that extends well beyond its immediate news cycle.

Signed on March 10, 2026, the 14-month exclusivity agreement between Lifezone Metals (NYSE: LZM) and the Government of Burundi grants the company the right to evaluate and potentially acquire the Musongati nickel laterite project without a formal purchase obligation during that period. On its surface, it is a contractual right, not a mine. Beneath that, it is an architectural shift in how the company can be underwritten by lenders, offtake buyers, and strategic investors.

When big ASX news breaks, our subscribers know first

What the Musongati Deposit Actually Represents

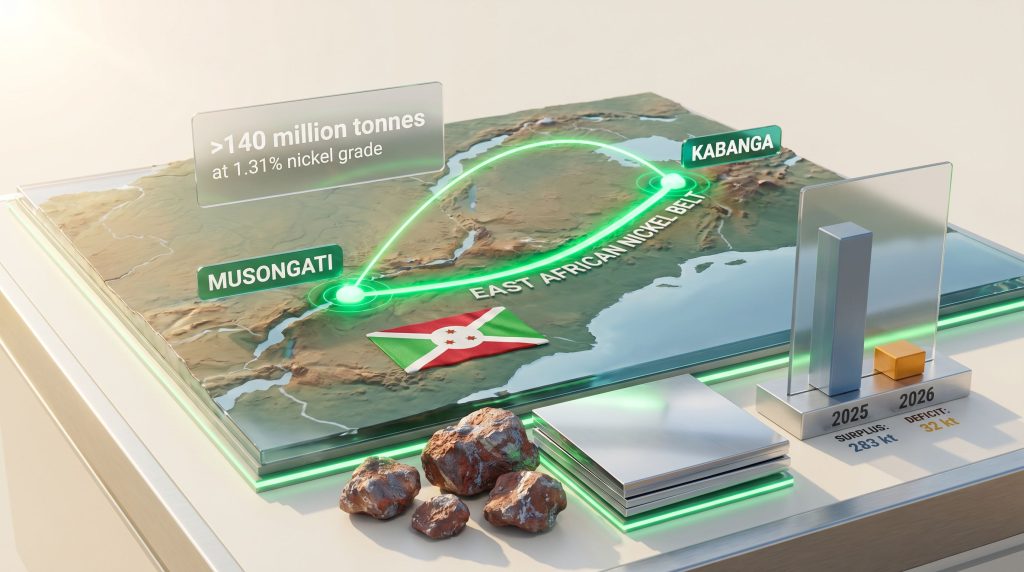

The Musongati project is located approximately 200 kilometres southwest of Lifezone's flagship Kabanga Nickel Project in Tanzania, positioning both assets within the East African Nickel Belt, a geological corridor characterised by significant sulphide and laterite nickel mineralisation running through multiple jurisdictions.

The deposit's technical history spans more than five decades, culminating in a 2011 resource estimate derived from 321 drillholes.

| Parameter | Detail |

|---|---|

| Historical Resource | >140 million tonnes at 1.31% nickel grade |

| Drillhole Basis | 321 historical drillholes |

| Resource Standard | Not verified to current JORC or NI 43-101 standards |

| By-Products Identified | Copper, cobalt, gold, platinum-group metals, scandium |

| Geographic Relationship | ~200 km southwest of Kabanga, Tanzania |

| Exclusivity Duration | 14 months from March 10, 2026 |

The resource classification caveat is critical for investors to absorb. Historical estimates carry no compliance with modern reporting codes, meaning grade continuity, cut-off assumptions, and by-product recovery assumptions have not been independently verified to current standards. The 2011 figure is a starting point for evaluation, not a bankable resource.

Investor Caution: A historical resource estimate that has not been verified to JORC or NI 43-101 standards cannot be used directly in financial modelling, feasibility studies, or project finance applications. Infill drilling is required before any resource forms part of a formal economic assessment.

What makes the deposit commercially interesting beyond the nickel tonnage is its by-product complexity. Cobalt carries battery supply chain relevance increasingly valued by processors seeking sources outside Chinese refining networks. Platinum-group metals align with Lifezone's existing PGM Recycling Project ambitions. Scandium, while a niche commodity with limited global primary production, commands pricing leverage precisely because so few primary sources exist. Copper broadens revenue exposure across commodity cycles independent of nickel pricing.

Early Technical Activity Already Underway

One underappreciated element of the Musongati situation is how much preparatory geological work had already been completed before the exclusivity agreement was formalised. During the first quarter of 2026, Lifezone's geological team conducted multiple meetings with Burundian mining officials, reviewed drilling data and historical studies held within the Office Burundais des Mines et Carrières technical library, completed a fact-finding mission to the project area, and began developing a preliminary infill drilling programme.

This level of pre-exclusivity due diligence signals a deliberate, disciplined approach rather than opportunistic deal-making. Companies that secure options without prior technical engagement typically face a longer ramp-up once the exclusivity clock starts. Lifezone entered the 14-month window with geological context already in hand. For investors who spend time interpreting drill results, the quality of historical drillhole data at Musongati will be central to any updated resource assessment.

How the Musongati Option Reshapes Financing Architecture

A common misconception when evaluating options like this is that they represent a distraction from the primary asset's financing path. In Lifezone's case, the structural design actively prevents that outcome.

The Taurus Mining Finance senior secured bridge loan facility of $60 million is explicitly allocated to Kabanga pre-Final Investment Decision activities, early works, and development, with no exposure to Musongati exploration. Musongati activities draw from the April 2026 registered direct offering, which closed on April 23, 2026, generating net proceeds of US$23.3 million from a $25 million gross raise.

That ring-fenced capital is allocated across four workstreams:

- Exploration activities at Musongati in Burundi

- Exploration activities in Tanzania

- Advancement of the PGM Recycling Project in the United States

- Hydromet research and development at Simulus Laboratory

This separation matters for how lenders and project finance institutions model Kabanga's risk profile. Musongati's exploration uncertainty does not attach itself to the bridge facility or to the project finance workstream being led by Societe Generale.

Kabanga's Parallel Financing Workstreams as of Q1 2026

| Financing Track | Counterparty / Instrument | Q1 2026 Status |

|---|---|---|

| Senior Secured Bridge Loan | Taurus Mining Finance | $60M facility, active |

| Project Finance Process | Societe Generale | DFI and ECA pathfinders selected |

| US Development Finance Corp | DFC | Due diligence completed; further workstreams active |

| Strategic Investment Process | Standard Chartered Bank | Multiple offers received from major miners, sovereign investors, private equity |

A company navigating four parallel financing workstreams simultaneously while opening a second large deposit under exclusivity is presenting a materially different enterprise story to institutional capital than a single-asset developer waiting on one financing outcome. Furthermore, the path towards a definitive feasibility study at Kabanga becomes more compelling when supported by a broadening regional asset base.

The Supply Context That Makes East African Nickel Strategically Relevant

The global nickel supply picture shifted dramatically between 2025 and 2026 in ways that elevate the commercial significance of any credible non-Indonesian supply source. The International Nickel Study Group projected a 32 kilotonne nickel deficit in 2026, against a 283 kilotonne surplus in 2025. That reversal was driven in significant part by Indonesian nickel market trends, as government policy reduced the country's 2026 nickel ore mining quota to 270 wet metric tonnes, down from 375 wet metric tonnes in 2025.

For context, Indonesia has dominated global nickel supply growth over the past decade. Any meaningful reduction in quota changes the market's structural balance faster than new greenfield projects can respond. The deficit projection for 2026 reflects that lag.

Buyers underwriting long-term concentrate offtake agreements are no longer evaluating single-project volume alone. They are stress-testing the supply chain for geographic concentration risk, jurisdiction resilience, and the operator's capacity to deliver across multiple ore sources over time.

Lifezone's Q1 2026 disclosures indicated that several long-term concentrate offtake negotiations for Kabanga were well advanced. The existence of a second large deposit under exclusivity within the same East African belt strengthens the supply narrative presented to those buyers, even before Musongati reaches any formal acquisition or development stage. In addition, the broader nickel market recovery underway in 2026 adds further urgency to securing diversified supply sources outside of concentrated geographies.

The Hydromet Question: Does Processing Chemistry Extend to Laterite?

Lifezone's Hydromet technology currently processes sulphide nickel ore at Kabanga and has been extended to the US PGM Recycling Project, where Q1 2026 pilot testwork at Simulus Laboratory achieved recovery rates of up to 99% platinum, 99% palladium, and 95% rhodium.

Whether Hydromet's processing chemistry is applicable to Musongati's laterite ore type remains an open technical question. This distinction matters because laterite nickel ores require fundamentally different processing pathways than sulphide ores.

Sulphide ores are typically amenable to flotation concentration followed by smelting and refining. Laterites, by contrast, require either high-pressure acid leach, heap leach, or pyrometallurgical treatment, each of which carries different capital cost profiles, reagent consumption rates, and environmental footprints. The capital intensity of laterite processing has historically been the primary reason large laterite deposits remain undeveloped despite their scale.

If Lifezone's Hydromet platform can be adapted for laterite chemistry, the implications extend well beyond the Lifezone Metals Musongati option. It would represent a meaningful differentiation of the processing technology and a material expansion of the addressable deposit universe. That possibility is speculative at this stage, and investors should treat it as an open variable rather than an assumed outcome.

The next major ASX story will hit our subscribers first

Three Scenarios for the 14-Month Exclusivity Window

Rather than treating the Musongati option as a binary outcome, the most analytically useful frame is a scenario distribution based on the geological and commercial variables that will emerge over the exclusivity period.

| Scenario | Trigger Condition | Strategic Implication |

|---|---|---|

| Full Acquisition | Infill drilling validates historical resource; acquisition terms disclosed | Lifezone transitions to dual-asset developer; financing leverage improves materially |

| Extended Evaluation | Preliminary drilling warrants further study; exclusivity extended by agreement | Regional thesis preserved; capital allocation remains disciplined |

| Option Lapses | Geological or economic data does not support acquisition | Kabanga thesis unchanged; Musongati capital treated as sunk exploration cost |

The key insight across all three scenarios is that the downside is bounded. If Musongati does not convert, Kabanga's valuation, FID timeline, and existing financing structure remain intact. The cost of maintaining 14 months of exclusivity on a deposit exceeding 140 million tonnes at 1.31% nickel is structurally low relative to the upside optionality it preserves.

Key Milestones Investors Should Track

Five specific outcomes will determine how the Musongati option evolves within the exclusivity window:

- Infill drilling results: Does updated geological work support, revise, or upgrade the 2011 historical resource estimate?

- Formal acquisition term disclosure: Are commercial terms between Lifezone and the Government of Burundi made public within the exclusivity period?

- Hydromet applicability assessment: Does Simulus Laboratory testwork extend to Musongati's laterite ore type, and what recovery rates are achievable?

- Kabanga FID timeline: Does the regional consolidation thesis accelerate or complicate the strategic partnership and project finance discussions already underway?

- Offtake agreement finalisation: Do long-term concentrate buyers incorporate Musongati's optionality into commercial terms for Kabanga?

The Regional Platform Thesis: What Changes and What Does Not

It is worth being precise about what the Lifezone Metals Musongati option does and does not alter in the near term. Consequently, investors evaluating this story must separate near-term asset fundamentals from the longer-horizon structural narrative.

What does not change:

- Kabanga's near-term valuation and cash flow profile

- The FID timeline, which is governed by its own financing workstreams

- The Taurus bridge facility allocation and its exclusivity to Kabanga activities

What does change:

- Lifezone's long-term enterprise profile as presented to project finance lenders, DFIs, ECAs, and strategic investors

- The supply chain narrative available to offtake buyers evaluating ex-Indonesian diversification

- The institutional risk underwriting framework, which shifts from single-asset concentration to regional platform optionality

- The potential scope of Hydromet as a multi-ore-type processing technology

Two large-scale deposits within the East African Nickel Belt, under a single operator with a disclosed consolidation strategy, create the structural conditions for infrastructure and operational overlap that independent development of each project could not achieve. This dynamic is highly relevant to the broader critical minerals demand story unfolding across global energy transition timelines. Whether that potential is realised depends on the geological, technical, and commercial work that unfolds across the next 14 months.

The strategic value of the Musongati option is not measured in near-term cash flow. It is measured in how institutional capital underwrites a regional platform versus a single mine, and whether the processing technology underpinning both assets can evolve to match the geological opportunity.

However, for a broader market perspective, Mining Weekly's coverage of the exclusivity agreement provides useful context on how the transaction is being received across the wider mining investment community.

This article contains forward-looking statements and scenario analysis based on publicly disclosed information from Lifezone Metals' Q1 2026 financial results and presentations. It does not constitute financial advice. The Musongati resource estimate referenced is a historical estimate that has not been verified to current JORC or NI 43-101 standards. Investors should conduct their own due diligence before making investment decisions.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex geological data into actionable investment insights — explore historic examples of exceptional discovery returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.