June 20, 2026

The Capital Discipline Paradox: How Staged Investment Unlocks Long-Term Value in Hard-Rock Lithium

Seasoned investors in the resources sector understand a counterintuitive truth: the companies that preserve capital during downturns often emerge as the dominant producers when market conditions recover. In hard-rock lithium, this dynamic is playing out in real time. The producers who avoided committing large tranches of capital during the 2022 to 2024 price correction are now the ones positioned to scale production ahead of the next demand-driven uplift cycle. The question for investors is not simply which assets are the largest, but which operations have the discipline, data, and design flexibility to grow profitably through changing market conditions.

The Liontown Kathleen Valley expansion sits squarely within this framework. It represents a considered, data-informed decision to begin scaling one of Australia's most substantial hard-rock lithium operations at a moment when real operational knowledge, not theoretical modelling, underpins the capital case.

When big ASX news breaks, our subscribers know first

Why Scale and Geology Make Kathleen Valley a Generational Asset

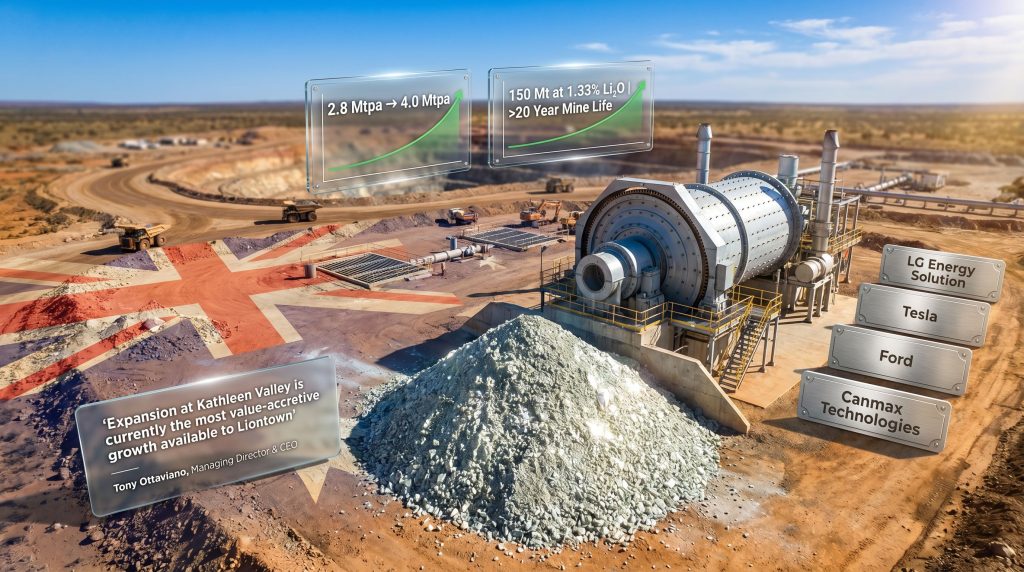

Before assessing the expansion strategy, it is worth understanding what makes the underlying asset exceptional. The Kathleen Valley ore body carries a resource of 150 million tonnes grading at 1.33% Li₂O, which places it firmly within the upper tier of Australian hard-rock lithium deposits by both size and grade. At that resource scale, and assuming the expansion production targets are met, the operation supports a mine life exceeding 20 years — a duration that is genuinely rare in the current development pipeline globally.

The deposit is located approximately 680 kilometres northeast of Perth within Western Australia's premier hard-rock lithium corridor. The geographic context matters: Western Australia hosts the world's largest concentration of spodumene production, with the established ecosystem of contractors, processing expertise, and logistics infrastructure that reduces execution risk relative to greenfield lithium projects in less developed jurisdictions.

What Spodumene Grade Actually Means for Investors

Spodumene extraction (LiAlSi₂O₆) is the process by which the lithium-bearing mineral is recovered at Kathleen Valley. The grade of 1.33% Li₂O represents the concentration of lithium oxide within the mined rock. For context, ore bodies below 1.0% Li₂O are generally considered marginal at current processing costs, while deposits above 1.2% Li₂O tend to generate stronger unit economics at full throughput. A consistent grade above 1.3% across a 150 million tonne resource base is what creates the long-duration economic foundation the expansion investment case rests upon.

The transition to 100% underground lithium mining, completed by December 2025, is operationally significant for several reasons. Underground extraction accesses deeper, higher-continuity mineralisation that open-pit methods cannot economically reach. The paste fill system installed as part of this transition is particularly noteworthy for investors unfamiliar with the technology: paste fill involves processing milled tailings into a thick slurry that is pumped back underground to fill mined voids.

This approach serves two purposes simultaneously. It structurally stabilises the underground workings, reducing ground support requirements, and it eliminates the need for above-ground tailings storage at the same scale, reducing environmental footprint and associated regulatory exposure. Critically, both the ventilation systems and paste fill infrastructure are performing within the parameters defined by the original feasibility study, which validates that the engineering assumptions underpinning the expansion study are grounded in demonstrated reality.

From First Concentrate to Expansion: Reading the Production Trajectory

Spodumene concentrate production commenced at Kathleen Valley in mid-2024, initiating a ramp-up phase that has progressively scaled underground mining rates. The current production target is a mining throughput run rate of 1.5 million tonnes per annum (Mtpa) by the end of Q1 FY2026, representing approximately half of the intended steady-state capacity of 2.8 Mtpa targeted by the end of FY2027.

At full steady-state throughput, the operation is expected to produce approximately 500,000 tonnes per annum of spodumene concentrate. This figure is commercially significant because it places Kathleen Valley within the mid-to-large tier of global spodumene producers once fully ramped. Furthermore, as Liontown financial results have demonstrated, the financial trajectory has already begun reflecting the production scale-up.

Revenue doubled in the December 2025 half-year period as underground production volumes increased, and the inherent operating leverage in mining economics means unit costs are expected to compress as throughput continues rising toward full capacity. This unit cost reduction dynamic is not merely a management aspiration: it is a mathematical consequence of spreading fixed infrastructure costs across a larger volume of ore processed.

Liontown stock performance on the ASX (ticker: LTR) rose 316% over the twelve months to April 2026, compared to approximately 8% for the S&P/ASX 200 Index over the same period, according to Motley Fool Australia. While past share price performance is not indicative of future returns, this outperformance reflects market recognition of the operational de-risking achieved during the ramp-up phase.

Disclaimer: Past performance is not a reliable indicator of future returns. This article contains general information only and does not constitute financial advice. Investors should seek independent advice suited to their personal circumstances before making any investment decisions.

The Liontown Kathleen Valley Expansion: Why Now, and Why Staged

The original Kathleen Valley expansion study was completed in 2021, but the subsequent deterioration in lithium market conditions led management to defer any formal capital commitment. This decision, though disappointing for some investors at the time, ultimately proved disciplined: committing large-scale expansion capital during a price downturn would have destroyed value.

The revival of the expansion study in 2026 is notable precisely because of what has changed. Rather than relying on theoretical pre-production modelling, the refreshed study now incorporates nearly two years of actual operating data accumulated since concentrate production commenced in mid-2024. This transition from engineering assumption to operational evidence is a qualitative improvement that fundamentally changes the reliability of capital cost estimates, production rate assumptions, and equipment utilisation projections.

Liontown's approach to the Liontown Kathleen Valley expansion is structured around a phased capacity addition model rather than a single large capital commitment. This design choice deserves careful analysis, because it is often misread as hesitancy when it actually represents sophisticated capital allocation strategy.

Why Staged Deployment Outperforms All-In Capital Events in Commodity Mining

The logic of staged expansion in cyclical commodity sectors rests on several interconnected principles:

- Optionality preservation: Each completed stage can be evaluated independently, allowing management to accelerate or decelerate based on lithium price movements and balance sheet capacity at each decision point.

- Capital-at-risk reduction: By limiting committed capital at any single point, the company avoids the scenario where a large tranche of growth expenditure is deployed just before a market downturn, destroying returns on that invested capital.

- Operational learning integration: Each production stage generates data that informs subsequent capital decisions, improving cost estimates and reducing engineering risk for later phases.

- Investor credibility: Institutional capital allocators in the battery materials sector increasingly favour staged frameworks because they demonstrate management's willingness to tie capital deployment to market conditions rather than simply to internal enthusiasm.

Breaking Down A$77 Million: What Pre-FID Spending Actually Represents

The Liontown Kathleen Valley expansion has committed up to A$77 million in capital expenditure ahead of the formal Final Investment Decision (FID), targeted for the end of Q1 FY2027. Understanding what this pre-FID spending actually involves is essential for investors assessing execution risk.

| Capital Item | Committed / Expected Amount | Timing |

|---|---|---|

| 5.5MW ball mill procurement | A$12 million | Expenditure over next 12 months |

| Total FY2026 early works expenditure | A$15 to A$18 million | FY2026 |

| Total pre-FID capital ceiling | Up to A$77 million | Through Q1 FY2027 |

| Final Investment Decision | Full scope and capital cost disclosure | End of Q1 FY2027 |

The single largest committed item is the A$12 million procurement of a 5.5MW ball mill, which forms the centrepiece of the plant expansion program. Ball mills are the primary grinding equipment used in mineral processing: they reduce crushed ore to a fine particle size suitable for flotation and concentration. A 5.5MW unit represents significant processing capacity, and its specification as a long-lead item reflects the reality that large grinding mills carry 12 to 24 month manufacturing and delivery timelines in the current global mining equipment market.

This is where the pre-FID capital strategy becomes strategically logical rather than financially reckless. By committing A$12 million to the ball mill now, Liontown locks in current equipment pricing and secures a delivery timeline aligned with the post-FID construction schedule. Waiting until after the FID to place the order would compress the construction window by at least 12 months and expose the project to potential cost escalation driven by competing demand for large-capacity milling equipment from other mining projects globally.

The implied spending profile reveals a capital acceleration in the period between FY2026 and Q1 FY2027. With A$15 to A$18 million planned for FY2026, the remaining amount within the A$77 million ceiling represents approximately A$59 to A$62 million to be deployed through to the FID date, suggesting pre-development drilling, infrastructure upgrades, and expanded mine services will intensify considerably as the FID approaches.

Technical Scope: What the 4.0 Mtpa Expansion Study Targets

The refreshed expansion study targets a throughput increase from the current 2.8 Mtpa steady-state target to 4.0 Mtpa, a meaningful step-change in production capacity. Several technical workstreams are being advanced concurrently to achieve this increase.

Mining capacity development includes an evaluation of using the base of the completed open pit to supplement underground feed. This is a genuinely interesting technical concept: once open-pit mining concludes, the excavated void traditionally becomes either a water management feature or a legacy rehabilitation challenge. Utilising the pit floor to access additional ore zones or as a logistics access point to underground workings could, however, reduce the capital intensity of developing new underground mining fronts.

Plant infrastructure upgrades are centred on removing processing bottlenecks that constrain throughput at current capacity levels. The 5.5MW ball mill installation is the primary debottlenecking initiative, but supporting infrastructure modifications throughout the concentrator plant will also be required. In addition, pre-development drilling is progressing to better define ore zones ahead of mining and to support expanded underground development scheduling.

Downstream Integration: Beyond Concentrate Sales

The Kathleen Valley resource supports an eventual downstream pathway to approximately 86 ktpa of battery-grade lithium hydroxide through phased refinery development. Two processing pathways are under evaluation, as detailed in Liontown's downstream expansion plans:

- Lithium sulphate intermediate production: A lower-capital entry into value-added processing, where spodumene concentrate is converted to a lithium sulphate intermediate product that can be further refined by downstream partners.

- Full lithium hydroxide monohydrate production: The battery-ready end product required by cathode active material manufacturers for use in nickel-manganese-cobalt (NMC) and lithium iron phosphate (LFP) battery chemistries.

Key downstream partnerships supporting this pathway include an agreement with LG Energy Solution covering an IRA-compliant United States refinery, and a collaboration with Sumitomo for Japan-based processing.

The next major ASX story will hit our subscribers first

The Offtake Architecture: Who Is Buying Kathleen Valley's Output

Securing offtake agreements before a mine reaches full production is a standard practice in the lithium industry, but the breadth and counterparty quality of Kathleen Valley's commercial arrangements are noteworthy.

| Offtake Partner | Agreement Structure | Strategic Significance |

|---|---|---|

| LG Energy Solution | Extended 10-year agreement | Global top-tier EV battery manufacturer; IRA supply chain alignment |

| Tesla | Offtake agreement | Direct original equipment manufacturer (OEM) exposure |

| Ford | Offtake agreement | Legacy automaker EV transition; North American demand |

| Canmax Technologies | Offtake agreement | Chinese cathode material supply chain integration |

The portfolio design achieves three simultaneous objectives. First, it diversifies across EV battery manufacturers, automakers, and processing intermediaries, reducing single-counterparty concentration risk. Second, the LG Energy Solution partnership specifically positions Kathleen Valley output within supply chains eligible for US Inflation Reduction Act (IRA) manufacturing incentives, which represent a growing commercial premium for Western-aligned lithium producers. Third, multi-geography coverage across the United States, Japan, and China provides commercial resilience across different regional demand growth trajectories.

Funding the Growth: The Financial Architecture

The Liontown Kathleen Valley expansion benefits from a layered funding structure. Furthermore, Australia's first underground lithium mine of this scale has attracted significant government-backed support: the National Reconstruction Fund Corporation (NRFC) contributed A$50 million to support the underground transition, ramp-up phase, and broader operational development. This investment reflects the NRFC's mandate to support Australian industrial capability development and should be understood in that context rather than as project-specific endorsement of any particular expansion outcome.

The improving revenue trajectory, with the December 2025 half-year result showing doubled revenue relative to the prior period, demonstrates that the operation is increasingly capable of contributing internal cash generation to fund early works expenditure. The unit cost reduction expected as throughput scales toward 2.8 Mtpa creates additional operating leverage that improves the internal funding capacity for subsequent expansion stages.

The staged capital model is also inherently financing-friendly: by limiting peak capital requirements at any single decision point, the company avoids the need to raise large tranches of external capital simultaneously, which in a volatile lithium market could be both dilutive and poorly timed.

Risk Framework: What Could Derail the Expansion Timeline

Balanced assessment of the expansion program requires honest engagement with the risks that could alter the trajectory.

| Risk Category | Specific Risk | Mitigation in Place |

|---|---|---|

| Commodity price | Lithium price weakness delays FID or reduces project economics | Staged approach limits capital-at-risk; offtake agreements provide partial price floor protection |

| Equipment supply | Ball mill delivery delays compress post-FID construction schedule | A$12M procurement already placed, locking in delivery timeline |

| Capital cost escalation | Construction inflation erodes expansion returns | Pre-FID spending locks current pricing for critical long-lead items |

| Operational execution | Underground mining rates underperform throughput targets | Two years of actual operating data now underpins study assumptions |

| Regulatory and permitting | Approval delays affect early works or post-FID construction | Early works structured within existing approvals framework where possible |

The lithium price cycle risk deserves particular attention. The expansion study revival implicitly signals management's conviction that the market is stabilising or approaching a recovery inflection point. However, lithium price forecasting carries significant uncertainty, and investors should be cautious about treating any expansion timeline as immune to commodity market developments. Staged capital deployment is explicitly designed to preserve flexibility in the event market conditions deteriorate before or after the FID.

Key Milestones: The Roadmap to the Final Investment Decision

For investors tracking the expansion, the following waypoints define the near-term catalyst calendar:

- FY2026 (currently active): Early works, long-lead procurement, pre-development drilling, and plant infrastructure upgrades progressing with A$15 to A$18 million in planned expenditure.

- Ongoing through FY2026 into Q1 FY2027: Capital acceleration as pre-FID spending approaches the A$77 million ceiling.

- End of Q1 FY2027 (target): Final Investment Decision announcement, expected to include total expansion capital cost estimate, revised production targets beyond 2.8 Mtpa, throughput ramp schedule toward 4.0 Mtpa, and updated unit cost guidance.

- Post-FID: Staged construction commences, with specific timelines to first incremental production increases from the expanded capacity to be confirmed at the time of the FID announcement.

The FID announcement represents the defining catalyst event for this expansion program. Until that disclosure, investors are working with a capital cost ceiling (A$77 million pre-FID) and production target range (2.8 to 4.0 Mtpa), but not a complete capital and returns picture.

Frequently Asked Questions: Liontown Kathleen Valley Expansion

What exactly is the Kathleen Valley expansion project?

The Kathleen Valley expansion is a staged program to increase mine throughput capacity from the current 2.8 Mtpa steady-state target toward 4.0 Mtpa, through plant debottlenecking, equipment additions including a 5.5MW ball mill, pre-development drilling, and expanded underground mining capacity.

How much capital has been committed before the FID?

Liontown has committed A$12 million to long-lead equipment procurement, with total FY2026 early works expenditure of A$15 to A$18 million expected. The total pre-FID capital ceiling is A$77 million through to the end of Q1 FY2027.

When is the Final Investment Decision expected?

The FID is targeted for the end of Q1 FY2027. This announcement will disclose full capital costs, production uplift targets, and the construction timeline for the expanded operation.

What is the long-term production potential of Kathleen Valley?

The 150 million tonne resource at 1.33% Li₂O supports a mine life exceeding 20 years. Downstream integration potential extends to approximately 86 ktpa of battery-grade lithium hydroxide through phased refinery development, with two processing pathway options currently under evaluation.

Why was the expansion study previously deferred?

The 2021 expansion study was deferred due to deteriorating lithium market conditions. Its revival in 2026 reflects both improved market stability and the availability of nearly two years of actual operating data to support a more robust and reliable capital study.

What are the key risks to the expansion timeline?

Primary risks include lithium price volatility affecting the FID economics, equipment supply chain delays, capital cost escalation in the mining construction sector, and underground mining rate performance relative to feasibility study targets. Each of these risks has specific mitigation strategies embedded in the staged capital deployment framework.

Want to Identify the Next Major ASX Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery-driven returns and begin your 14-day free trial today to position yourself ahead of the next major market-moving announcement.