June 26, 2026

The Geology Behind the Deal: Why Lithium-Boron Co-Deposits Are Rewriting Critical Mineral Economics

In the world of critical mineral development, the rarest geological configurations often yield the most strategically valuable projects. Lithium-boron co-deposits represent exactly this kind of formation, combining two industrially essential commodities in concentrations high enough to support commercial extraction from a single site. Globally, only two such deposits have been identified. One of them sits in the high desert of Nevada, and it is now at the centre of a partnership framework that links U.S. federal financing, South Korean institutional capital, and one of Asia's most experienced engineering firms.

The Ioneer Rhyolite Ridge lithium-boron project LOI with KIND and Hyundai, formalised in June 2026, marks a consequential step in what has been a decade-long development journey. However, to understand why this announcement carries weight beyond a standard non-binding agreement, it helps to start with the geology, and then work outward toward the financial architecture, geopolitical dynamics, and production economics that make this project structurally unlike anything else currently in active development.

When big ASX news breaks, our subscribers know first

What Makes Rhyolite Ridge Geologically Distinct from Every Other Lithium Project in Development

The Dual-Commodity Profile and Why It Changes Project Economics

Most lithium development narratives centre on a binary choice: lithium brines explained, which extract dissolved lithium from underground saline aquifers in South American salars, or hard-rock spodumene extraction, which involves processing lithium-bearing pegmatite ore predominantly sourced from Western Australia. Both approaches produce a single primary commodity. Revenue generation, project financing, and cost recovery all hinge on the lithium price cycle.

Rhyolite Ridge, furthermore, operates under an entirely different economic model. The deposit hosts lithium and boron in the same ore body, with both commodities recoverable at commercial scale from integrated on-site processing. This co-production structure means the project generates two distinct revenue streams from a single extraction operation, fundamentally altering the relationship between production costs and commodity price volatility.

The mineralisation at Rhyolite Ridge occurs in sedimentary lacustrine sequences, where lithium-bearing clays and boron minerals accumulated together in an ancient lake basin environment. This is geologically distinct from the pegmatite and brine environments that dominate global lithium supply, and it is the reason the deposit's dual-commodity characteristics are not replicable simply by exploring adjacent terranes. The formation conditions required to produce co-located lithium and boron at economic grades are exceptionally rare.

Nevada's Regulatory Maturity as a Risk Differentiator

Rhyolite Ridge is located in Esmeralda County, Nevada, a jurisdiction with one of the world's most established mining regulatory frameworks. The project has already achieved fully permitted, construction-ready status, a threshold that the overwhelming majority of greenfield critical mineral projects globally have not yet approached.

For context, the average time from discovery to production for a major mining project globally is commonly cited at 16 to 17 years, with permitting alone consuming several years in complex jurisdictions. Nevada's established processes, experienced regulatory agencies, and precedent-rich permitting history substantially compress sovereign risk compared to emerging-market lithium jurisdictions across Africa, Central Asia, or parts of Latin America.

Construction-ready status, combined with a fully integrated on-site processing model, positions Rhyolite Ridge as one of the most operationally de-risked greenfield lithium projects currently in active development anywhere in the world.

Understanding the LOI Framework: What Non-Binding Actually Means in Major Project Finance

The Agreement Architecture from LOI to Financial Close

Investors and observers unfamiliar with major infrastructure and resource project development sometimes overinterpret the significance of a Letter of Intent, or conversely dismiss it as commercially meaningless. The reality is more nuanced. An LOI is a formal signal of intent that typically initiates structured due diligence, technical evaluation, and commercial term negotiation. It does not create legally enforceable obligations for either party.

The progression pathway from this stage to binding commitment follows a well-understood sequence in project finance:

| Agreement Stage | Legal Enforceability | Targeted Timeline | Primary Function |

|---|---|---|---|

| Letter of Intent (LOI) | Non-binding | Signed June 2026 | Signal intent, initiate due diligence |

| Memorandum of Understanding (MOU) | Semi-formal framework | Targeted July 2026 | Define cooperation scope and commercial terms |

| Binding Commercial Agreement | Legally enforceable | Post-FID | Commit capital and contractual obligations |

| Financial Close | Full capital commitment | H2 2026 (FID target) | Unlock construction financing |

It is critical to note that no certainty exists that the LOIs with KIND or Hyundai Engineering will progress to binding commercial arrangements. The parties have expressed intent, not obligation.

KIND's Institutional Role and What It Signals About Korean Government Priorities

KIND, the Korea Overseas Infrastructure and Urban Development Corporation, is not a conventional private equity or commercial investment entity. It operates as a specialised public institution under South Korea's Ministry of Land, Infrastructure and Transport. Its mandate is to facilitate and co-invest in overseas infrastructure and public-private partnership projects on behalf of the Korean government.

This institutional character matters significantly. When KIND participates in an overseas project, it does so as an instrument of Korean industrial and foreign policy, not purely as a return-seeking investor. KIND has described its involvement in U.S. energy, infrastructure, and critical minerals projects as a strategic priority, framing the Rhyolite Ridge partnership as a meaningful step toward strengthening bilateral cooperation between South Korea and the United States. This elevates the LOI beyond a standard commercial transaction and positions it within the broader context of allied-nation critical mineral supply chain strategy, a trend also reflected in South Korea battery expansion efforts more broadly.

Hyundai Engineering's Role: Why Construction Execution Capability Is the Binding Constraint

Engineering Completion as a Project Readiness Signal

One of the most underappreciated bottlenecks in greenfield critical mineral development is not capital availability but construction execution capability. Major engineering and procurement firms with demonstrated capacity to deliver complex chemical processing facilities on time and within budget are a constrained resource globally. Hyundai Engineering Co. Ltd brings exactly this operational profile to the Rhyolite Ridge partnership.

Hyundai Engineering's LOI covers engineering, procurement, and design participation — the specific functions that translate a fully permitted project into physical construction. The firm's publicly stated assessment of Rhyolite Ridge emphasises permitting status, construction readiness, and long-term supply certainty as the metrics that differentiate this project from other critical mineral development opportunities it has evaluated. For further detail on Hyundai's involvement and project scope, North American Mining provides additional reporting on the partnership framework.

This assessment carries independent technical weight. Hyundai Engineering is not a passive financial participant, and its willingness to signal participation at the EPD level reflects an informed view of the project's execution readiness.

What 70% Advanced Engineering Completion Actually Means

Ioneer has completed more than 70% of its advanced engineering work for Rhyolite Ridge. In practical terms, advanced engineering at this stage encompasses detailed process design, equipment specifications, site layout confirmation, utility system design, and cost estimate refinement.

A critical industry benchmark applies here: at advanced engineering completion levels above 70%, capital cost estimation accuracy typically reaches approximately plus or minus 10 to 15 percent. This is a material shift from the wider confidence intervals that apply at prefeasibility or early feasibility stages, and it has direct implications for lender confidence and equity investor risk assessment.

For comparison:

- Scoping study stage: Cost estimate accuracy of plus or minus 35 to 50 percent

- Prefeasibility study: Plus or minus 25 to 30 percent

- Feasibility study: Plus or minus 15 to 20 percent

- Advanced engineering above 70%: Plus or minus 10 to 15 percent

This narrowing of cost uncertainty is one of the principal reasons institutional capital commitments tend to cluster around the advanced engineering completion threshold rather than earlier project stages.

The DOE Loan Guarantee: Debt Architecture and What It Means for the Capital Stack

A US$996 Million Federal Commitment to Domestic Lithium Supply

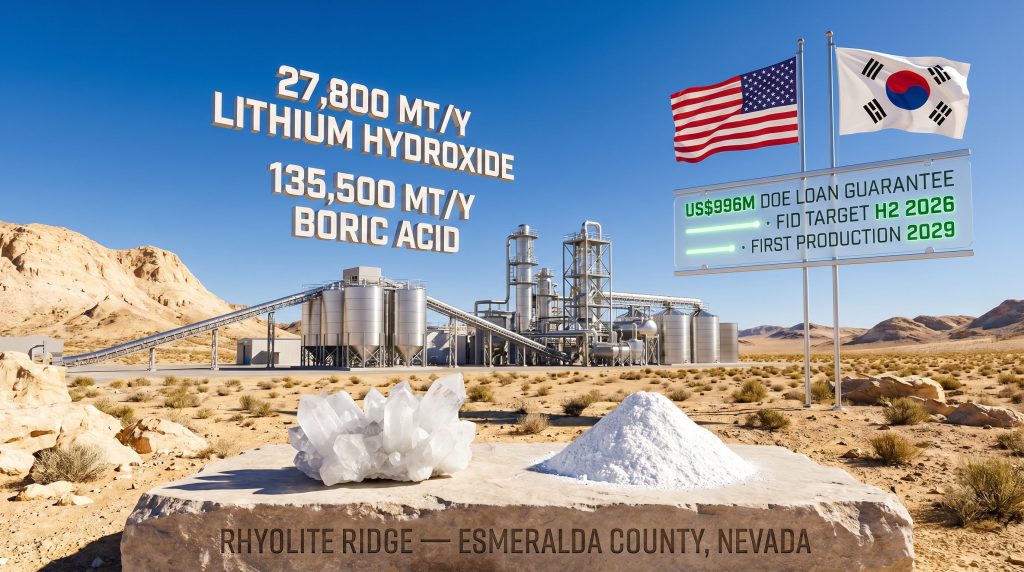

In January 2025, Rhyolite Ridge closed a US$996 million conditional loan guarantee from the U.S. Department of Energy's Loan Programs Office. This facility was structured to support domestic lithium supply for electric vehicle battery manufacturing, consistent with U.S. clean energy industrial policy objectives.

The DOE Loan Programs Office has historically played a critical role in de-risking first-of-kind or strategically important clean energy projects by providing federal credit support, which reduces the effective cost of debt capital. For Rhyolite Ridge, this guarantee forms the debt-side backbone of the project's capital structure.

A US$996 million federal loan guarantee does not merely provide financing. It functions as a sovereign-level validation of the project's technical credibility and strategic relevance within U.S. domestic supply chain policy.

The Equity Gap: What KIND and Hyundai Are Designed to Fill

Federal loan guarantees address debt financing. Major greenfield projects at this scale require equity partners with both capital and operational capability to reach Financial Close. The KIND and Hyundai Engineering LOIs are specifically positioned to fill this structural gap in the capital stack.

The resulting financing architecture, if both LOIs progress to binding agreements, would combine:

- U.S. federal debt support via the DOE conditional loan guarantee

- Korean sovereign-linked equity interest through KIND's MOLIT mandate

- Engineering execution capacity from Hyundai Engineering's EPD participation

This dual-government backing structure, linking U.S. federal financing with Korean institutional investment, is rarely seen in greenfield critical mineral projects and reflects the elevated strategic priority both nations attach to allied-nation supply chain security.

Production Economics and Why the Boric Acid Revenue Stream Is Systematically Undervalued

Annual Output Targets and Their Market Context

| Product | Projected Annual Output | Primary End-Use Markets |

|---|---|---|

| Lithium Hydroxide | 27,800 metric tons per year | EV battery cathodes, grid-scale energy storage |

| Boric Acid | 135,500 metric tons per year | Industrial glass, ceramics, NdFeB permanent magnets, agriculture, semiconductors |

The lithium hydroxide output figure represents a meaningful contribution to North American lithium hydroxide supply. Most public discourse around Rhyolite Ridge focuses on this number, which is understandable given the prominence of lithium in EV battery narratives. However, the boric acid production figure deserves considerably more analytical attention than it typically receives.

Boron, in the form of boric acid and refined boron compounds, is a critical input for neodymium-iron-boron permanent magnets — the magnet technology used in EV traction motors and direct-drive wind turbines. These applications are growing rapidly alongside EV production capacity expansion and offshore wind deployment. The global boron market is also structurally concentrated, with Turkey historically supplying the majority of global refined boron products. Rhyolite Ridge's 135,500 mt/y of boric acid output would represent a significant diversification of Western-aligned boron supply.

Additionally, recent processing improvements at Rhyolite Ridge have driven a 28% upgrade in projected average annual lithium production across the project's first 25 years of operation, increasing from 19,200 tons to 24,500 tons of lithium carbonate equivalent. This revision demonstrates that the project's production economics are still improving as engineering advances.

The On-Site Integration Advantage

Unlike the majority of global lithium mining operations, which ship ore concentrate to separate processing facilities — often located overseas — Rhyolite Ridge is designed to convert extracted ore into final-grade lithium hydroxide and boric acid entirely on-site. In addition, this integrated model delivers several competitive advantages:

- Logistical simplification: Eliminates the cost and complexity of concentrate shipping and third-party processing

- Supply chain traceability: Enables direct chain of custody from mine to final product, increasingly important under critical mineral sourcing regulations

- Revenue capture: Captures downstream processing margin within the same project economics rather than sharing it with third-party processors

- IRA compliance: Domestically processed, final-form product from a U.S. operation strengthens eligibility for clean vehicle tax credit supply chain requirements

The next major ASX story will hit our subscribers first

Geopolitical Architecture: Why South Korea's Exposure to Critical Mineral Supply Risk Drives This Partnership

South Korea's Structural Vulnerability and Its National Response

South Korea's advanced manufacturing economy, anchored by global leaders in EV battery production, semiconductor fabrication, and specialty steel, is materially exposed to critical mineral supply concentration risk. The country imports virtually all of its lithium requirements, and historically a significant share has been sourced from processing chains with exposure to non-allied-nation geopolitical risk. This vulnerability sits at the heart of growing critical minerals demand pressures facing the region.

South Korea's government has consequently deployed institutions like KIND as active instruments of overseas critical mineral supply chain development. This is not passive investment — it is sovereign supply chain strategy operationalised through institutional capital.

IRA Compliance and the Commercial Logic for Korean Battery Manufacturers

The U.S. Inflation Reduction Act introduced foreign entity of concern provisions that create material commercial incentives for battery manufacturers supplying U.S. automakers to source lithium from domestic or allied-nation operations. Korean battery producers who supply major U.S. automakers are directly exposed to these incentive structures.

Lithium hydroxide sourced from Rhyolite Ridge, as a U.S.-sited, domestically processed, and operationally IRA-aligned product, carries premium strategic value for Korean battery manufacturers seeking to maintain or expand their U.S. market position. Furthermore, the application of direct lithium extraction technologies continues to evolve alongside these commercial pressures, adding additional context to how allied nations are approaching supply security.

As U.S. trade policy increasingly distinguishes between allied-nation and adversarial-nation critical mineral sources, domestically permitted U.S. projects with allied-nation partners occupy a structurally advantaged position in the bifurcating global critical minerals trade landscape.

Scenario Analysis: Three Pathways from LOI to Financial Close

The June 2026 LOIs initiate a process with multiple possible outcomes. No binding commitments exist. The following scenario framework maps the principal pathways:

Scenario 1: Accelerated Conversion (Base Case)

- MOUs executed with KIND and Hyundai Engineering in July 2026 as targeted

- Technical and commercial due diligence completed through Q3 2026

- Final Investment Decision achieved in H2 2026

- Construction commences late 2026, targeting first commercial production in 2029

Scenario 2: Delayed Conversion (Moderate Risk)

- MOU execution pushed beyond July 2026 due to extended negotiation or due diligence

- FID delayed into H1 2027, compressing the construction schedule

- 2029 production target comes under pressure without timeline recovery measures

Scenario 3: Partial Conversion (Downside Risk)

- One counterparty does not advance beyond the MOU stage

- Ioneer's global partnering process, which launched in July 2025 with Goldman Sachs as financial advisor, remains open to alternative investors

- DOE loan guarantee remains intact as debt support, but equity gap requires resolution before Financial Close

Key Milestones for Tracking Partnership Progression

- MOU execution with KIND, targeted July 2026

- MOU execution with Hyundai Engineering, targeted July 2026

- Advanced engineering completion above 70% (currently confirmed)

- Final Investment Decision, targeted H2 2026

- Construction commencement, post-FID

- First commercial production, targeted 2029

What First Production in 2029 Would Mean for the North American Lithium Supply Chain

The decade-long development journey behind Rhyolite Ridge reflects a structural reality of critical mineral project development: the timelines required to move from discovery through permitting, engineering, and financing to production are measured in years, not quarters. Projects that have already cleared these hurdles carry disproportionate strategic value relative to earlier-stage assets.

By 2029, global lithium demand is projected to have expanded substantially beyond current levels, driven by EV penetration growth across North America, Europe, and Asia. North American lithium hydroxide production from fully integrated domestic operations remains limited relative to anticipated demand. Rhyolite Ridge's 27,800 mt/y of lithium hydroxide, produced on U.S. soil, processed to final grade on-site, and sourced through a partnership framework aligned with allied-nation supply chain policy, represents exactly the type of production capacity that both U.S. and Korean industrial strategies are seeking to bring online.

The Ioneer Rhyolite Ridge lithium-boron project LOI with KIND and Hyundai does not guarantee this outcome. Non-binding agreements carry no enforcement mechanism, and the path from intent to financial close involves material execution risk. However, the convergence of a construction-ready permitted project, a US$996 million federal loan guarantee, advancing engineering completion, and now institutional-level partnership interest from two Korean entities operating at the intersection of sovereign industrial policy and commercial execution represents a project development profile with few contemporaries in the current critical minerals landscape. For additional reporting on the broader significance of this announcement, im-mining.com's coverage provides further context on what the KIND and Hyundai Engineering pacts signal for the project's trajectory.

Readers seeking additional reporting on the Rhyolite Ridge project and its development history can explore related coverage from the Engineering and Mining Journal at e-mj.com. This article contains forward-looking statements and scenario projections that involve assumptions and uncertainties. It does not constitute financial or investment advice.

Want to Catch the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — from critical minerals like lithium to transformative dual-commodity projects — so subscribers can act on actionable opportunities ahead of the crowd. Explore historic discoveries and the returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.